Bridge Report:(2462)LIKE Fiscal year ended May 2021

![]()

Yasuhiko Okamoto, President | LIKE, Inc. (2462) |

|

Company Overview

Exchange | Tokyo Stock Exchange, First Section |

Industry | Service |

President | Yasuhiko Okamoto |

HQ Address | Shibuya Mark City West 17F, 1-12-1 Dogenzaka, Shibuya-ku, Tokyo |

Year-end | The end of May |

HP |

Stock Information

Share Price | Shares Outstanding (excluding treasury shares) | Market Cap | ROE (Act.) | Trading Unit | |

¥1,773 | 19,113,148 shares | 33,888 million | 29.6% | 100 shares | |

DPS (Est.) | Dividend Yield (Est.) | EPS(Est.) | PER (Est.) | BPS (Act.) | PBR (Act.) |

¥52.00 | 2.9% | ¥172.66 | 10.3x | ¥624.73 | 2.8x |

* The share price is the closing price on August 30. The number of shares issued at the end of the latest quarter excludes its treasury shares.

* ROE and BPS are results for FY 5/21, EPS and DPS are forecasts for FY 5/22, and figures rounded.

Earnings Trends

Year | Sales | Operating Profit | Current Profit | Net Profit | EPS | DPS |

May 2018 | 45,663 | 1,915 | 3,889 | 1,532 | 81.49 | 29.00 |

May 2019 | 47,797 | 1,746 | 3,753 | 1,595 | 84.58 | 26.00 |

May 2020 | 51,072 | 2,000 | 4,067 | 1,793 | 94.41 | 28.00 |

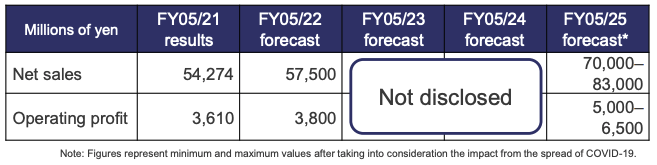

May 2021 | 54,274 | 3,610 | 5,341 | 3,262 | 171.10 | 50.00 |

May 2022 Est. | 57,500 | 3,800 | 5,500 | 3,300 | 172.66 | 52.00 |

* Estimates are those of the company. Unit is million yen, EPS and DPS are yen. Net profit is profit attributable to owners of the parent. Hereinafter the same shall apply.

* EPS reflects the change made after a 2 for 1 stock split was conducted in September 2017.

This Bridge Report presents details of the fiscal year ended May 2021 earnings results and fiscal year ending May 2022 earnings forecast for LIKE, Inc.

Table of Contents

Key Points

1. Company Overview

2. Fiscal Year ended May 2021 Earnings Results

3. Fiscal Year ending May 2022 Earnings Forecast

4. Conclusions

<Reference: Regarding Corporate Governance>

Key Points

- Sales and ordinary profit grew 6.3% and 31.3%, respectively, year on year in the term ended May 2021. The Childcare Support Service and the Nursing Care Service generated healthy sales regardless of the spread of the novel coronavirus. The company managed to minimize the negative impact in the Comprehensive Human Resources Service by reconsidering which industries to focus on in the early stage. In terms of profit, operating profit margin increased from 3.9% to 6.7% because gross profit margin improved from 16.4% to 18.0% year on year, and streamlining recruitment activities allowed the ratio of SG&A expenses on sales to decline from 12.5% to 11.4%. The year-end dividend was 35.00 yen per share, which significantly increased the annual dividend by 22.00 yen year on year to 50.00 yen per share.

- Sales and ordinary profit are forecasted to grow 5.9% and 3.0%, respectively, year on year in the term ending May 2022. The company plans to open about 12 authorized nursery schools in the Childcare Support Service Business. It aims to expand business dramatically in the Comprehensive Human Resources Service Business through intensive investment in growing markets. In the Nursing Care Service Business, the company will continue opening new facilities, including fee-based nursing care centers for assisted living, to fulfill escalating demand for nursing care service in the Tokyo metropolitan area. In addition, it will maximize the group’s synergy through collaboration between the Comprehensive Human Resources Service Business and the Nursing Care Service and Childcare Support Service Businesses in securing human resources. The company plans to pay an annual dividend of 52.00 yen per share, up 2.00 yen year on year.

- Current profit and operating profit in term ended May 2021 exceeded the initial forecasts by 30% and 68%, respectively, demonstrating that the company’s strategy of focusing on “must-haves” bore fruit even amid the novel coronavirus pandemic. The forecast of single-digit increases in each profit for the term ending May 2022 appears to be conservative, but the fact is that profits were initially projected to grow only by a single digit also in the term ended May 2021. Earnings per share (EPS) is estimated at about 200 to 250 yen in the medium-term business plan, and the company intends to aggressively pursue mergers and acquisitions (M&A), and business alliances. The plan presumably has a tremendous amount of hidden potential. Demand from investors for efforts at the Sustainable Development Goals (SDGs) has been rising recently. The company’s businesses are perfect for investment in the SDGs and Environment, Social, and Corporate Governance (ESG) because they each can play a role in creating a sustainable society. Its posture on shareholder return with shareholder benefits as well as considerable increases of dividends is received well by individual investors, due probably to which its shareholders feel inseparable from the company. Its share price has been on a downward trend since the company announced its financial results, decreasing price earnings ratio (PER) to 10, which falls greatly behind the average in the first section of the Tokyo Stock Exchange (which is 16). In this regard, given three factors, which are that LIKE, Inc. (1) is indispensable to society, (2) is a company that shareholders feel inseparable from because primarily of its efforts at the SDGs, and (3) has formulated a meaningful medium-term business plan, we have to say that the company is underestimated.

1. Company Overview

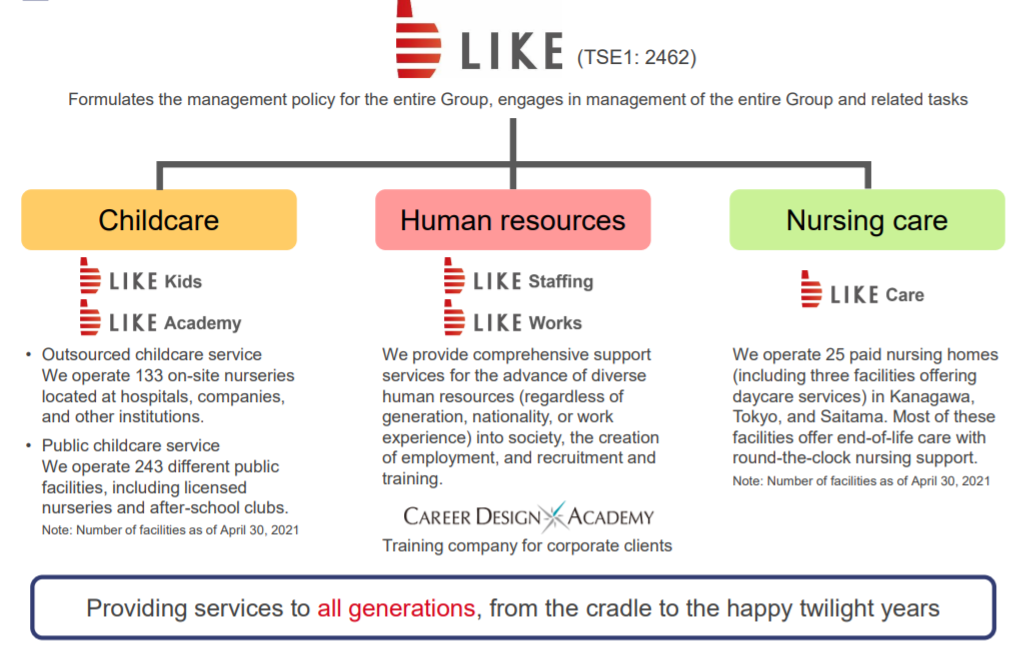

Based upon its corporate management philosophy of “Planning the Future – Leveraging Human Resources to Create the Future,” LIKE endeavors to create an “indispensable corporate group structure” that is capable of providing vital services at every stage of life (from the cradle to the happy twilight years) in the operating realms of child and nursing care, human resources and other services.

(Source: the company)

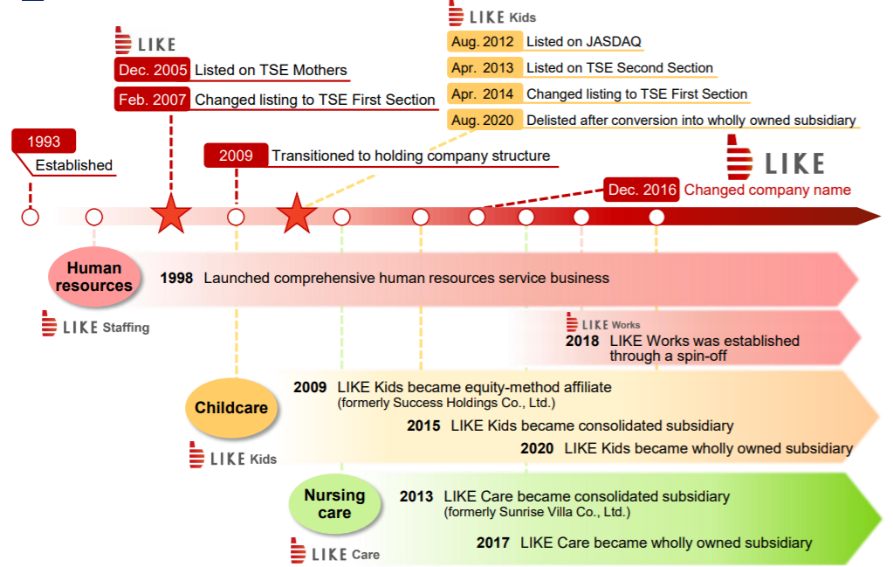

【1-1 Corporate history】

LIKE was established in 1993 for the purpose of operating the travel package planning business. The foothold for the current main business is the comprehensive human resources service business, which was launched in 1998. The company was listed on Mothers in 2005 and moved to the first section of the Tokyo Stock Exchange in 2007. In 2009, the company shifted to a holding company structure and expanded its business domain to include childcare services and nursing care-related services through acquisitions.

(Source: the company)

【1-2 Business Segments and LIKE Group Companies】

LIKE’s business segments are divided into operation of public childcare facilities and child-rearing support services on consignment, the comprehensive human resources services business, which includes human resources dispatch, business process consignment, dispatched worker for employment and job placement, hiring and training support services, the childcare support services business, which includes consigned operation of public and private childcare facilities, the nursing care services business, which includes nursing facility operations.

(Source: the company)

The LIKE Group is comprised of the holding company LIKE, Inc., five consolidated subsidiaries and one non-equity accounting method affiliate. The consolidated subsidiaries include LIKE Kids, Inc. and its subsidiary, LIKE Academy, Inc., which is engaged in contracted childcare and public childcare services (operation of authorized nursery schools, etc.), LIKE Staffing, Inc., which provides worker dispatch and business process consignment services to cellular telephone shops within its comprehensive human resources services business, LIKE Works, Inc. providing comprehensive human resources services to the logistics and manufacturing industries and LIKE Care, Inc, which operates nursing-care facilities. In addition to these, a joint venture company called Career Design Academy, Inc., has been created to provide corporate training services with LIKE Staffing, Inc. and T-Gaia Corporation (Tokyo Stock Exchange, First Section, Stock code:3738) providing 20% and 80% of the capital, respectively.

【1-3 Medium Term Business Plan】

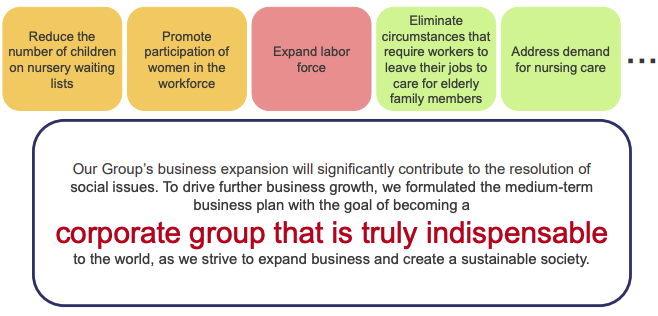

The company formulated a new medium-term business plan in January. In light of the impact of the novel coronavirus, the company has disclosed a range of plans for the term ending May 2025, which is the final year of the medium-term business plan.

Purpose in formulating the Medium-Term Business Plan

The spread of the novel coronavirus provided the company with an opportunity to reacknowledge that the LIKE Group’s services are needed by the society and closely related to resolving social issues.

(Source: the company)

Earnings objectives in the Medium-Term Business Plan

(Source: the company)

<Points of the earnings objectives>

➢ The objectives will be achieved through organic growth in the existing businesses.

➢ Business will be expanded through enrichment of the existing nursery schools and opening of new schools in the childcare business.

➢ Growth in the areas of logistics and manufacturing, nursing care, construction, and foreign human resources is expected in the human resources business.

➢ New nursing care facilities will be opened and synergy with the area of foreign human resources will be exerted in the nursing care business.

➢ The company aims to push up sales to over 100 billion yen through M&A and business alliances.

Policies aimed at attaining the Medium-Term Business Plan’s objectives

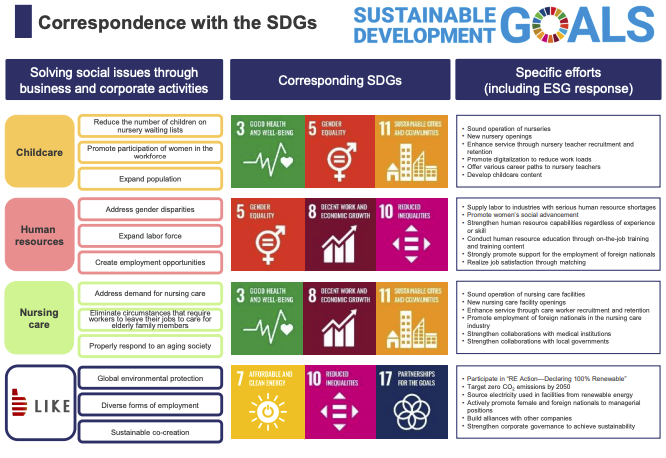

SDGs Initiatives |

➢ Efforts have been intensified to realize a sustainable society.

(Source: the company)

(Source: the company)

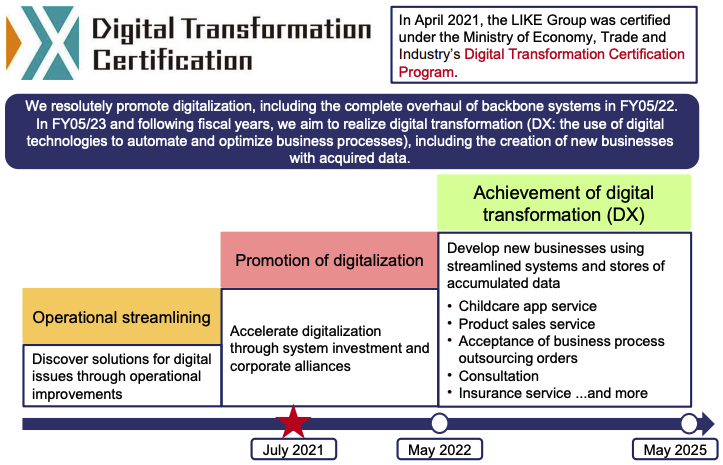

Promotion of Digital Transformation (DX) |

➢ There is room for digitization because LIKE’s businesses are labor-intensive.

➢ The company begins with promoting digitization, and then creates new businesses using data obtained.

(Source: the company)

M&A and Business Alliances |

➢ The company possesses knowledge with which it has grown the childcare and nursing care businesses as the corporate group’s core businesses.

➢ The company aims to expand business further through continuous and proactive discussion.

<<Childcare>>

➢ The company proactively opens new nursery schools to resolve the issue of long waiting lists for childcare service.

➢ The company propels forward such measures as implementation of strategic M&A, digitization, and establishment of working environments in anticipation of a business environment of more intense competition.

<<Human resources>>

➢ The company selects business areas based on its strategy of “must-haves.”

➢ The company focuses its business resources on growing markets.

➢ The company focuses particularly on the areas of logistics and manufacturing, nursing care, construction, and foreign human resources.

<<Nursing care>>

➢ The company opens three to five fee-based nursing care centers for assisted living (specified facilities) annually in the Tokyo metropolitan area.

➢ The company establishes synergy with the foreign human resources area of the human resources business.

【1-4 Shareholder Benefit Program】

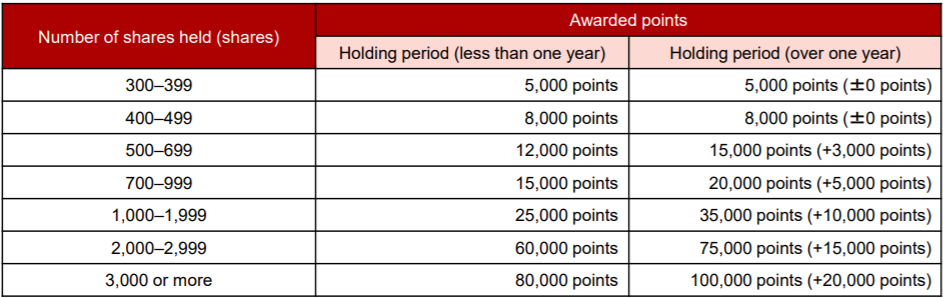

Provides the “LIKE Premium Benefit Club.”

Targets: Shareholders who are listed on the shareholder list as of the end of May every year and possess 300(3 lots) or more shares of LIKE.

Contents: Points are given to shareholders every July, based on the table below. In the special website (https://like.premium-yutaiclub.jp), shareholders can exchange their shareholder’s benefit points for some of over 2,000 kinds of complimentary items, including food products, home appliances, gifts, and miscellaneous goods.

The “LIKE Premium Benefit Club” has been changed (announced on January 12, 2021).

The number of points awarded has significantly increased. For example, if you hold 500 shares for less than one year, you will receive 12,000 points instead of 7,000 points, and if you hold 500 shares for one year or longer, you will receive 15,000 points instead of 7,700 points.

2. Fiscal Year ended May 2021 Earnings Results

(1) Consolidated Earnings

| FY 5/20 | Ratio to sales | FY 5/21 | Ratio to sales | YoY | April forecast | Difference from previous forecast |

Sales | 51,072 | 100.0% | 54,274 | 100.0% | +6.3% | 54,000 | +0.5% |

Gross Profit | 8,383 | 16.4% | 9,778 | 18.0% | +16.6% | - | - |

SG&A | 6,383 | 12.5% | 6,167 | 11.4% | -3.4% | - | - |

Operating Profit | 2,000 | 3.9% | 3,610 | 6.7% | +80.5% | 3,150 | +14.6% |

Current Profit | 4,067 | 8.0% | 5,341 | 9.8% | +31.3% | 4,700 | +13.6% |

Net Profit | 1,793 | 3.5% | 3,262 | 6.0% | +81.9% | 2,600 | +25.5% |

*Units: million yen

*Figures include reference figures calculated by Investment Bridge Co.; Ltd. Actual results may differ (Abbreviated hereafter).

Sales and ordinary profit increased 6.3% and 31.3%, respectively, year on year

Sales were 54,274 million yen, up 6.3% year on year. The Childcare Support Service and the Nursing Care Service generated healthy sales regardless of the spread of the novel coronavirus. The company managed to minimize the negative impact in the Comprehensive Human Resources Service by reconsidering which industries to focus on in the early stage.

In terms of profit, in the Childcare Support Service, the company started operating English schools and children’s gymnastics schools on its own, which it had outsourced before, in the wake of the spread of the novel coronavirus infection, following which gross profit margin improved to 18.0% from 16.4% in the previous term. Changes in the trend in the human resources market driven by the novel coronavirus pandemic helped the company streamline its recruitment activities and cut down on recruitment and education costs, resulting in a reduction in the SG&A-to-sales ratio to 11.4% from 12.5% in the previous term. Consequently, operating profit margin rose to 6.7% from 3.9% in the previous term, increasing operating profit by 80.5% year on year to 3,610 million yen. Regarding non-operating profit, a decline in proceeds from equipment subsidies raised current profit 31.3% year on year to 5,341 million yen. Net profit grew 81.9% year on year to 3,262 million yen owing to the headquarters relocation expenses posted in the previous term under extraordinary loss.

Regardless of the upward revisions to the forecasts of each profit in April, all of them exceeded the revised forecasts significantly as mentioned above. Operating profit, current profit, and net profit exceeded the initial forecasts by 1,460 million yen (up 67.9%), 1,241 million yen (up 30.3%), and 1,362 million yen (up 71.7%), respectively. The Childcare Support Service and the Nursing Care Service were not affected very much by the spread of the novel coronavirus and both sales and profit exceeded the forecasts thanks to the existing nursery schools and nursing care facilities that were enriched and operated on a steady and healthy basis. In the Comprehensive Human Resources Service, although the sales results did not reach the forecast due to the novel coronavirus pandemic that reduced sales in the fashion industry (apparel and cosmetics) and the manufacturing industry dealing with orders from overseas and forced sales promotion events to be cancelled in the mobile industry; however, the company strived to control costs and managed to reach the profit forecast.

The year-end dividend was 35.00 yen per share, which increased the annual dividend significantly by 22.00 yen year on year to 50.00 yen per share.

(2) Segment Earnings Trends

| FY 5/20 | Ratio to sales | FY 5/21 | Ratio to sales | YoY |

Childcare Support | 22,966 | 45.0% | 26,396 | 48.6% | +14.9% |

Comprehensive Human Resources | 20,814 | 40.8% | 20,301 | 37.4% | -2.5% |

Nursing Care | 6,984 | 13.7% | 7,252 | 13.4% | +3.8% |

Others | 307 | 0.6% | 323 | 0.6% | +5.4% |

Sales, Total | 51,072 | 100.0% | 54,274 | 100.0% | +6.3% |

Childcare Support | 514 | 18.7% | 2,118 | 47.8% | +311.9% |

Comprehensive Human Resources | 1,902 | 69.2% | 1,922 | 43.4% | +1.0% |

Nursing Care | 297 | 10.8% | 347 | 7.9% | +16.7% |

Others | 33 | 1.2% | 40 | 0.9% | +21.7% |

Adjustments | -747 | - | -818 | - | - |

Operating Profits, Total | 2,000 | - | 3,610 | - | +80.5% |

*Units: million yen

*“Others” indicates businesses which are not included in the report segment. Operating profit ratio refers to pre-adjusted consolidated operating income as 100%.

Childcare Support Service Business

Sales were 26,396 million yen (up 14.9% year on year) and operating profit stood at 2,118 million yen (up 311.9% year on year).

Steady enrichment and operation of the existing nursery schools resulted in the sales increase. The impact of the spread of the novel coronavirus infection forced the company to reduce the number of authorized nursery schools to open to 12 from 22 in the year before. The decline in the cost of opening new nursery schools increased profit significantly.

Demand for childcare service continues to remain at a high level even amid the novel coronavirus pandemic. The company has reinforced its management system so that it can offer services stably even in an unstable situation. It newly opened 12 authorized nursery schools in the term ended May 2021 (one of which was a ward-run school but has been converted to a private school, and another of which was closed permanently because the specified operation period ended).

Comprehensive Human Resources Service Business

Sales were 20,301 million yen (down 2.5% year on year) and operating profit was 1,922 million yen (up 1.0% year on year).

Sales shrank due to cancellation of sales promotion events in the mobile industry and to strategic withdrawal from the apparel industry. Meanwhile, profit grew because of the company’s efforts at cost control which reduced SG&A expenses.

The number of staff members working at the end of the term was 7,119, up 12.4% from the end of the previous term. In the term ended May 2021, sales growth was sluggish, but the number of staff members who were at work rose considerably.

Details by industry are as follows:

Mobile: While cancellation of sales promotion events caused a sharp sales decrease, demand for human resources is enormous due to the entry of the fourth mobile phone carrier.

Logistics/manufacturing: Orders for workers are growing in number following the start of operation of a large-scale logistics center.

Apparel: A strategic withdrawal from the industry resulted in a year-on-year decline by 1,005 million yen.

Childcare/nursing care:

・LIKE Kids: 259 million yen (down 37 million yen year on year)

・LIKE Care: 218 million yen (up 12 million yen year on year)

Sales Breakdown by Industry of Comprehensive Human Resources Service Business

Sales by Industry (Units: million yen) | FY 5/20 | FY 5/21 | YoY | |||

Sales | Ratio to sales | Sales | Ratio to sales | Increase/decrease | Rate of change | |

Mobile phone | 13,120 | 63.0% | 12,139 | 59.8% | -980 | -7.5% |

Manufacturing and logistics | 3,821 | 18.4% | 4,716 | 23.2% | +894 | +23.4% |

Call center | 1,348 | 6.5% | 1,378 | 6.8% | +30 | +2.3% |

Childcare | 371 | 1.8% | 330 | 1.6% | -41 | -11.1% |

Nursing care | 262 | 1.3% | 217 | 1.1% | -45 | -17.2% |

Construction | 125 | 0.6% | 198 | 1.0% | +73 | +58.4% |

Others | 1,763 | 8.5% | 1,319 | 6.5% | -443 | -25.2% |

Total | 20,814 | 100.0% | 20,301 | 100.0% | -512 | -2.5% |

*Due to reclassification, part of Call center is changed to Mobile phone (First half 163 million), apparel is included in Others.

(Made by Investment Bridge referring to company website)

Nursing Care Service Business

Sales stood at 7,252 million yen (up 3.8% year on year) and operating profit was 347 million yen (up 16.7% year on year).

Both sales and profit increased because the company operated its nursing care facilities on a steady basis even amid the novel coronavirus crisis. The occupancy rate is satisfactory for the new facility opened in March (Higashi-terao, Yokohama City: 72 rooms).

Others (The Multimedia Service Business, excluding other businesses than the multimedia service one)

Sales were 322 million yen (up 5.4% year on year) and operating profit was 39 million yen (up 22.5% year on year).

In the Multimedia Service Business, the company operates a mobile phone shop as a showroom for services of the Comprehensive Human Resources Service Business that are targeted at the mobile communications industry.

(3) Financial Conditions and Cash Flow

◎Financial Condition

| May 2020 | May 2021 |

| May 2020 | May 2021 |

Cash | 13,092 | 9,536 | Accounts payable | 3,263 | 3,161 |

Receivables | 4,258 | 4,879 | Taxes Payable | 1,431 | 1,614 |

Current Assets | 19,617 | 16,126 | Security Deposits | 976 | 861 |

Tangible Assets | 13,346 | 15,068 | Interest Bearing Liabilities (Inc. Leases) | 17,372(1,289) | 16,736(2,197) |

Intangible Assets | 1,554 | 1,084 | Liabilities | 25,670 | 25,770 |

Investments, Others | 5,305 | 5,431 | Net Assets | 14,154 | 11,940 |

Noncurrent Assets | 20,207 | 21,584 | Total Liabilities, Net Assets | 39,825 | 37,711 |

*Units: million yen

Total assets at the end of the term ended May 2021 stood at 37,711 million yen, down 2,113 million yen from the end of the previous term.

Current assets stood at 16,126 million yen, down 3,491 million yen from the end of the previous term. This decline is because primarily of a decrease in cash by 3,555 million yen following repayment of short-term debts.

Noncurrent assets grew 1,377 million yen from the end of the previous term to 21,584 million yen, which is due in part to an increase in tangible assets by 1,722 million yen following the opening of new nursery schools in the Childcare Support Service Business and a drop by 444 million yen as a result of amortization of goodwill.

Current liabilities shrank 5,212 million yen from the end of the previous term to 11,215 million yen mainly because of a rise of current portion of long-term debts by 455 million yen, an increase in income taxes payable by 308 million yen, and a decline in short-term debts by 6,400 million yen.

Noncurrent liabilities were 14,555 million yen, up 5,312 million yen from the end of the previous term. This is attributable primarily to increases in long-term debts by 4.4 billion yen and lease obligations by 907 million yen.

Net assets stood at 11,940 million yen, down 2,214 million yen from the end of the previous term, which is because primarily of net profit recorded at 3,262 million yen, dividends paid which amounted to 552 million yen, a decline in non-controlling interests by 4,071 million yen resulting from the acquisition of all the shares of a consolidated subsidiary, LIKE Kids, Inc., on August 28, 2020, and a decrease in capital surplus by 957 million yen following the change in ownership interest of parent due to transactions with non-controlling interests.

Capital-to-asset ratio went up 6.4 points from the end of the previous term to 31.7%.

◎ Cash Flow

| FY 5/20 | FY 5/21 | YoY | |

Operating CF | 3,450 | 5,695 | +2,244 | +65.0% |

Investing CF | -3,655 | -1,806 | +1,848 | - |

Free CF | -204 | 3,888 | +4,092 | - |

Financing CF | 5,667 | -7,444 | -13,112 | - |

Cash and Cash Equivalents | 13,072 | 9,516 | -3,555 | -27.2% |

*Units: million yen

As of the end of the term ended May 2021, cash and equivalents shrank 3,555 million yen from the end of the previous term to 9,516 million yen. Such negative factors as income taxes paid, purchase of tangible assets, net decrease in short-term debts, repayment of long-term debts, and payments from changes in ownership interests in subsidiaries that do not result in change in scope of consolidation outstripped positive factors including recording of net profit before income taxes.

The operating cash flow stood at 5,695 million yen, resulting primarily from net profit before income taxes recorded at 5,354 million yen, depreciation posted at 1,247 million yen, amortization of goodwill posted at 444 million yen, and income taxes paid of 1,837 million yen.

The investing cash flow was 1,806 million yen, which was due mainly to proceeds from sales and redemption of securities and investment securities of 85 million yen and purchase of tangible assets of 1,934 million yen following the opening of new nursery schools in the Childcare Support Service Business.

The financing cash flow amounted to 7,444 million yen because in part of proceeds from long-term debts of 7,116 million yen, net decrease in short-term debts of 6,400 million yen, repayments of long-term debts of 2,259 million yen, payments from changes in ownership interests in subsidiaries that do not result in change in scope of consolidation of 5,256 million yen, and dividends paid of 552 million yen.

3. Fiscal Year ending May 2022 Earnings Forecast

(1) Consolidated Earnings

| FY5/21 Actual | Ratio to sales | FY5/22 Est. | Ratio to sales | YoY |

Sales | 54,274 | 100.0% | 57,500 | 100.0% | +5.9% |

Operating Profit | 3,610 | 6.7% | 3,800 | 6.6% | +5.3% |

Current Profit | 5,341 | 9.8% | 5,500 | 9.6% | +3.0% |

Net Profit | 3,262 | 6.0% | 3,300 | 5.7% | +1.2% |

*Units: million yen

Sales and ordinary profit are forecasted to grow 5.9% and 3.0%, respectively, year on year in the term ending May 2022

Sales and current profit are forecasted to rise 5.9% and 3.0% year on year to 57.5 billion yen and 5.5 billion yen, respectively, in the term ending May 2022.

In terms of the market trend in the Childcare Support Service Business, while the number of children being put on the waiting list for childcare facilities is on the decline, the issue remains thorny mainly in the Tokyo metropolitan area. The downward trend is expected to remain deep-seated given Japan’s demographics. The Ministry of Health, Labour and Welfare, therefore, has drawn up Shin Kosodate Anshin Plan, a new child-rearing program aimed at ensuring childcare facilities and services for approximately 140,000 children for the four years from fiscal year 2021 to the end of fiscal year 2024 to resolve the issues of long waiting lists for childcare service as swiftly as possible. As of April of 2021, the job-to-applicants ratio for childcare workers is 2.04, remaining higher than 1.04, the average of all occupations, and this means that the lack of childcare providers continues to be a pressing issue to tackle. Under these circumstances, in the Childcare Support Service Business, the company will act proactively also in the term ending May 2022 with the intention of opening about 12 authorized nursery schools. Regarding securing childcare workers, it intends to attract excellent human resources and enhance the quality of its childcare service by generating synergy with its corporate group’s Comprehensive Human Resources Service Business. In addition, given the fact that the percentage of joint-stock companies in the industry is still low, LIKE, Inc. will further expand business, as well as achieve self-sustained growth by utilizing its internal resources through agile M&A.

The market trend for the Comprehensive Human Resources Service Business indicates that the growth potential of the market in which LIKE, Inc. operates business is tremendous, including the entry of the fourth mobile phone carrier in the mobile industry, soaring demand for human resources at call centers and start of operation of a large-scale logistics center resulting from growth of the e-commerce market, the nursing care and construction industries that are expected to run low on hundreds of thousands of workers in the future, and demand for foreign workers for making up for the labor shortage. In this situation, the company aims to grow the Comprehensive Human Resources Service Business dramatically by investing more business resources in the realms of logistics and manufacturing, nursing care, construction, and foreign human resources in which strong demand for human resources and enormous growth potential are expected and making intensive investment in growing markets while focusing on the mobile industry that is its core business area with which the company’s business originates.

Regarding the market trend in the Nursing Care Service Business, demand for nursing care service is expected to rise certainly in such areas as the Tokyo metropolitan area because the rate of aging is projected to climb with a growing population aged 75 and over, and an increasing population size of people aged 65 and over in urban cities. Furthermore, nursing care providers who fulfill the nursing care demand are expected to be insufficient significantly. Japan cannot afford to deal with these social issues only with its domestic workforce. Thus, in order to meet the escalating demand for nursing care service in the Tokyo metropolitan area, the company will continuously open new facilities, including fee-based nursing care centers for assisted living, and maximize its group’s synergy primarily by accepting technical intern trainees with foreign nationalities to its facilities in Japan at a further accelerating rate and cultivating knowledge so that it can accept foreign workers on a large scale as a way out of the issue of nursing care provider shortages through collaboration with the corporate group’s Comprehensive Human Resources Service Business.

Based on the policy aimed at a consolidated payout ratio of approximately 30%, the interim dividend and the year-end dividend are to be 26.00 yen per share each, resulting in an annual dividend of 52.00 yen per share, up 2.00 yen year on year.

(2) Market Trend and Strategies by Business

- Childcare Support Service -

Overview

➢ The company is aware of the issue of the high rate of turnover of female workers because of childcare in the Comprehensive Human Resources Service with which it started off.

➢ Sales have grown about 14 times for the past 14 years compared to the years before the company acquired capital.

➢ Operating profit also increased significantly to 2,118 million yen in FY 5/21 from a deficit of 40 million yen in FY 5/16 when the company began to prepare consolidated financial statements.

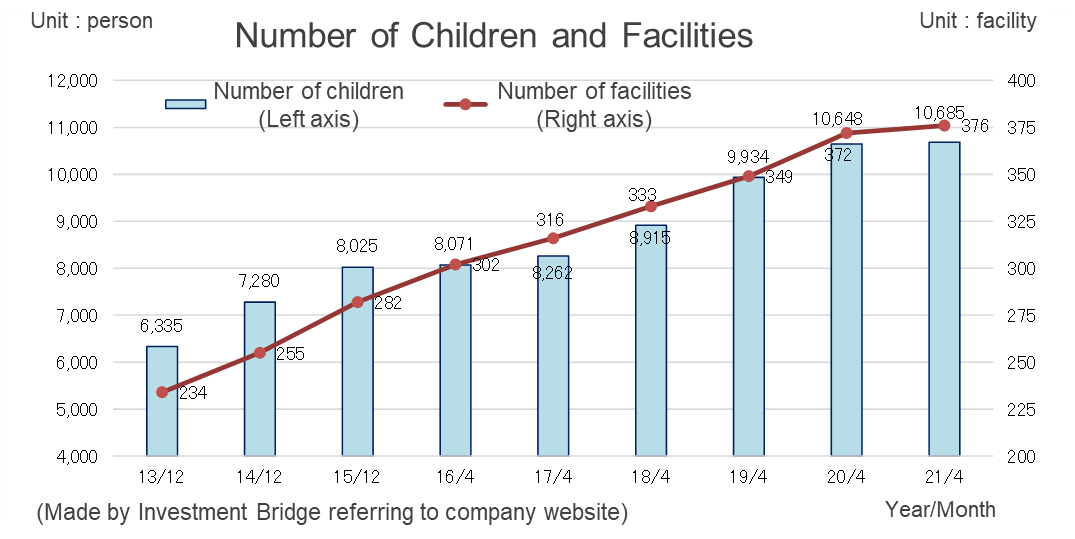

➢ The company operates 376 nursery schools mainly in the Tokyo metropolitan area that take care of over 10,600 children, generating the second largest sales in the industry.

Strengths/characteristics

➢ Recruitment capacity: The company develops human resources through synergy with the human resources department and cross-sectional adoption of training contents.

➢ Dominance: The company operates nursery schools primarily in the Tokyo metropolitan area and establishes a comfortable working environment by offering its workers a flexible choice of places of work.

➢ Economies of scale: The company reduces cost and provides diverse career paths through operation of a number of nursery schools.

➢ Facility location: The company has advanced development capabilities thanks to close relationship with developers.

Market trend

➢ The number of births stood at approximately 840,000 in 2020, which is the lowest since records began, but the population size by prefecture is expected to grow in the Tokyo metropolitan area according to the estimate of the latest census.

➢ While children being put on the waiting list for childcare facilities are decreasing in number, the issue remains thorny mainly in the Tokyo metropolitan area. A new child-rearing support plan called Shin Kosodate Anshin Plan, therefore, was launched in fiscal year 2021 with the aim of securing childcare facilities and services for about 140,000 children as a national policy.

➢ The job-to-applicants ratio for childcare providers is on the decline; however, the ratio is 2.04 as of April 2021, which is higher than 1.04, the average of all occupations.

➢ The percentage of joint-stock companies operating childcare facilities is 6.2% as of 2017. Many of the childcare facilities in the industry are still run by non-commercial corporations even though more stock companies are entering the industry.

Strategies

(Source: the company)

| New nursery openings | ➢ The company proactively considers operating nursery schools regardless of whether run on consignment or publicly. ➢ In FY 5/22, the company plans to open as many authorized nursery schools as in FY 5/21 (when it opened 12 authorized nursery schools). |

| Nursery teacher recruitment and retention | ➢ The company exerts synergy with the Comprehensive Human Resources Service. ➢ The company offers diverse workstyles, such as Miraikuru Nursery Teachers. |

| M&A | ➢ The company has acquired the childcare and nursing care businesses as its corporate group’s businesses through M&A. ➢ The company possesses knowledge ranging from selecting M&A projects to tasks after M&A. |

- Comprehensive Human Resources Service -

Overview

➢ The company expands the scale of this business, with which the corporate group started off, through staffing service targeting mobile phone distributors.

➢ The company has 15 business bases throughout Japan.

➢ The number of staff members in operation is over 7,000 and the number of client companies is over 600.

➢ The company has the fourth largest share in the human resources industry (sales and marketing support human resources business section).

Strengths/characteristics

➢ Development knowledge: The company has its own knowledge with which it has nurtured unqualified and unexperienced job seekers as work-ready workers.

➢ Industry-specific: The company has focused on this promising and essential industry.

➢ Number of client companies: The company ensures stability by securing a number of client companies even though its business model is industry-specific.

➢ Group synergy: The company has ensured specialization through collaboration with the childcare and nursing care businesses.

Market trend

Mobile phone | ➢ The entry of Rakuten Mobile, Inc. has intensified competition among the carriers. |

Call centers | ➢ Demand for human resources has risen due to the growth of e-commerce. |

Logistics and manufacturing | ➢ Operation of a logistics center employing 1,000 workers, which is run by a major client, was newly started. ➢ It was decided that a total of three facilities will be newly opened between Sep. and Dec. of 2021. |

Childcare and nursing care | ➢ The job-to-applicants ratio remains at a high level. ➢ Expected labor shortages particularly in the nursing care segment is a serious issue. |

Construction | ➢ Sales of the industry’s leading company: approx. ¥37 billion; Estimated market scale: ¥400 billion ➢ Workers in this industry are aging, causing chronic labor shortages. |

Foreign national human resources | ➢ The major premise is that the issue of labor shortages must be resolved in not only the nursing care and construction industries, but other industries. ➢ Regardless of the travel restrictions placed in the wake of the spread of the novel coronavirus, demand for foreign workers will rise certainly in the future. |

Strategies

(Source: the company)

| Logistics and manufacturing | ➢ The company continues proactively fulfilling demand for human resources that is driven by opening of a logistics center. ➢ The company sends human resources in units of 100 workers per newly opened facility. |

| Construction | ➢ Labor shortages in the industry will become more serious in the future. ➢ The company fulfills demand for human resources by sending foreign workers as well as with its domestic workforce. |

| Nursing careForeign national human resources | ➢ The company begins with focusing on the domestic workforce with specific skills. ➢ The company employs workers at its group’s nursing care facilities and introduces workers to other companies. |

- Nursing Care Related Service -

Overview

➢ The company operates 25 facilities mainly in Kanagawa and Tokyo with about 1,400 users.

➢ The major form of facility that the company operates is fee-based nursing care centers for assisted living (16 of the total of 25 facilities).

➢After acquisition of this business, the company improved the occupation rate from the 60%-level to over 90% through synergy with the human resources department.

➢ Operating profit grew to 347 million yen in FY 5/21 from a deficit of 217 million yen in FY 5/14 when the company began to prepare consolidated financial statements.

Strengths/characteristics

➢ End-of-life care: The company has built a strong relationship with medical institutions, which enables almost all of its nursing care facilities to offer end-of-life care service.

➢ 24 Nurse: Nurses provide 24/7 nursing support at some of the company’s facilities.

➢ Recruitment capacity: The company secures workers and realizes enriched support through synergy with the human resources department.

➢ Facility location: The company adopts its facility development capability of the childcare business to this business and operates nursing care facilities mainly in the Tokyo metropolitan area.

Market trend

➢ The Annual Report on the Aging Society compiled by the Cabinet Office expects that the rate of aging, which indicates the percentage of people aged 65 and over to Japan’s total population, will increase year by year with the population size of people aged 75 and over, in particular, being projected to grow in the future.

➢ The ratio of population aged 65 and over by city scale is forecasted to increase in urban cities and reach 133.4 in large cities in 2045 compared to 2015 whose ratio is taken as 100. This means that demand for nursing care service will rise increasingly in the Tokyo metropolitan area.

➢ The number of nursing care providers necessary for fulfilling the demand for nursing care service will grow by about 690,000 to about 2,800,000 in fiscal year 2040 from about 2,110,000 in fiscal year 2019.

Strategies

(Source: the company)

| new facility openings M&A | ➢ The company considers opening about three to five nursing care facilities annually in the Tokyo metropolitan area. ➢ At the same time, the company proactively conducts M&A to expand business scale. |

| Recruit and retain care workers | ➢ The company exerts synergy with the Comprehensive Human Resources Service. ➢ The company clearly differentiates its services from other companies’ services by securing human resources. |

| Collaboration with the human resources business | ➢ The company proactively accepts foreign workers at its facilities. ➢ The company cultivates knowledge in preparation for expanding the foreign human resources business. |

4. Conclusions

Current profit and operating profit in the term ended May 2021 exceeded the initial forecasts by 30% and 68%, respectively, demonstrating that the company’s strategy of focusing on “must-haves” bore fruit even amid the novel coronavirus pandemic. Although profit increased significantly, the impact of the novel coronavirus seemingly reduced the number of nursery schools to open in the Childcare Support Service, which cut down on cost. Meanwhile, the company is promoting more streamlined recruitment activities. The forecast of single-digit increases in each of the profit for the term ending May 2022 appears to be conservative, but the fact is that profits were initially projected to grow only by a single digit also in the term ended May 2021. Numerical objectives in the medium-term business plan are provided in ranges, with EPS being estimated at around 200 to 250 yen. Bringing sales of 100 billion yen into perspective, the company will aggressively pursue M&A and business alliances. The medium-term business plan presumably has a tremendous amount of hidden potential.

Demand from investors for efforts at the SDGs has been rising recently. The company’s businesses are perfect for investment in the SDGs and ESG because they each can play a role in creating a sustainable society. Its posture on shareholder return with shareholder benefits as well as considerable increases of dividends is received well by individual investors, due probably to which its shareholders feel inseparable from the company.

Its share price has been on a downward trend since the company announced its financial results, decreasing PER to 10, which falls greatly behind the average in the first section of the Tokyo Stock Exchange (which is 16). In this regard, given three factors, which are that LIKE, Inc. (1) is indispensable to society, (2) is a company that shareholders feel inseparable from because primarily of its efforts at the SDGs, and (3) has formulated a meaningful medium-term business plan, we have to say that the company is underestimated.

<Reference: Regarding Corporate Governance>

◎ Organization type, and the composition of directors and auditors

Organization type | Company with an audit and supervisory committee |

Directors | 7 directors, including 3 outside ones |

◎ Corporate Governance Report:Updated on August 30, 2021

Basic Policy

Our company aims to be a corporate group that is indispensable to society at any stage of life with a group mission of “planning the future – Developing people and creating the future –” and recognizes the initiatives for corporate governance as an essential management task. For its realization, we make use of our holding company structure and consolidate the compliance system in the holding company so that executives, employees and service users of our group can take fair and efficient actions at all times, and attempt to strengthen corporate governance of the whole group by centralizing the functions of the holding company by the management of the entire group.

1. Ensuring the rights and equality of shareholders

We take appropriate measures so that the rights of shareholders, including the voting rights at the general shareholders meeting, are substantially ensured.

2. Appropriate cooperation with stakeholders excluding shareholders

On the basis of our group mission, we will continue to enhance our corporate value by acting in good faith with all stakeholders including service users, clients, shareholders and employees, keeping in mind the Code of Conduct and principles of action.

3. Appropriate disclosure of information and ensuring transparency

We will make appropriate disclosure of information based on laws and ordinances and actively provide non-financial information and information other than the information disclosed based on laws and ordinances.

4. Responsibilities of the Board of Directors and others

The board of directors formulates the basic policy and strategies for the management of the group and manages and supervises the business firm. It operates as a body that supervises the management decision-making in the entire group and the business execution by the board of directors. In addition, the independent outside director works to strengthen the management discipline and increase the transparency further.

5. Dialogue with shareholders

Our company puts importance on dialogue with shareholders for maximizing our corporate group’s value, and we deal with requests from shareholders for dialogue at any time. The department in charge of investor relations, the officer in charge of investor relations, and the management executives have dialogue with shareholders as necessary.

Implementation Status of Principles of Corporate Governance Code

<The number of principles of Corporate Governance Code the Company does not comply with: 3, including the following>

【Supplementary principle 1-2-4】

Our company currently does not have any infrastructure that allows the exercise of electronic voting; however, we will consider using electronic voting by taking into account the proportion of institutional and overseas investors to the total number of shareholders.

【Supplementary principle 4-10-1】

Although we have not set up any independent advisory committee, our company explains nomination of candidates for directors and remuneration of directors to independent outside directors and obtain appropriate advice from them prior to a resolution by the board of directors. Since we obtain appropriate involvement and advice of independent outside directors regarding nomination of candidates for directors and directors’ remuneration as mentioned above, we consider that the independence, objectivity, and accountability of the functions of our board of directors pertaining to the aforementioned matters have been sufficiently secured.

<Disclosure Based on the Principles of the Corporate Governance Code (Excerpts)>

【Principle 1-4】

We will consider strategically holding shares of any listed company only when synergy of corporate value improvement has been recognized. Our company has confirmed the significance of the strategically held shares that we are currently possessing. Furthermore, with regard to the exercise of our voting rights as to those strategically held shares, we will declare our intention to approve or disapprove a case by taking into account whether the relevant company’s corporate value is improved and whether the exercise impacts our company.

【Principle 2-6】

Our company has not adopted a corporate pension plan.

【Principle 5-1】

-Our company promotes constructive dialogue with shareholders by designating a department and an officer in charge of investor relations so that they carry out our group’s overall investor relations activities.-Our company strives to disclose information in a fair, timely, and proper manner pursuant to the Disclosure Policy that we have formulated for organizing our basic ideas.

-The Disclosure Policy is disclosed on our website (https://www.like-gr.co.jp/ir/policy.html).

-Details of our investor relations activities are as mentioned in Section 2 “Implementation Status of Policies Regarding Shareholders and Other Stakeholders” of the CGC report.

Tokyo Stock Exchange Corporate Governance Information Service:

https://www2.tse.or.jp/tseHpFront/CGK010010Action.do?Show=Show

This report is intended solely for information purposes, and is not intended as a solicitation to invest in the shares of this company. The information and opinions contained within this report are based on data made publicly available by the company, and comes from sources that we judge to be reliable. However, we cannot guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness or validity of said information and or opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration. Copyright(C) Investment Bridge Co., Ltd. All Rights Reserved. |

To view back numbers of Bridge Report on LIKE, Inc. (2462) and other companies and to see IR related seminars of Bridge Salon, please go to our website at the following url:www.bridge-salon.jp/