Bridge Report:(2884)Yoshimura Food the Fiscal Year February 2020

![]()

Representative director and CEO Motohisa Yoshimura | Yoshimura Food Holdings K.K. (2884) |

|

Corporate Information

Exchange | TSE 1st Section |

Industry | Food products (manufacturing) |

Representative director and CEO | Motohisa Yoshimura |

Address | 18F, Fukoku Seimei Bldg., 2-2-2, Uchisaiwai-cho, Chiyoda-ku, Tokyo |

Year-end | February |

URL |

Stock Information

Share price | Shares Outstanding | Total Market Cap | ROE(Actual) | Trading Unit | |

¥973 | 22,171,795 shares | ¥21,573 million | 4.6% | 100 shares | |

DPS (Estimate) | Dividend Yield(Estimate) | EPS(Estimate) | PER (Estimate) | BPS(Actual) | PBR(Actual) |

¥0.00 | - | ¥18.95 | 51.3 times | ¥154.54 | 6.3 times |

*Share price is as of closing on April 30. Each figure was taken from the brief report on results for the term ended Feb. 2020.

Earnings Trends

Fiscal Year | Net Sales | Operating Income | Ordinary Income | Net Income | EPS | DPS |

February 2017 (Actual) | 16,241 | 493 | 530 | 353 | 16.28 | 0.00 |

February 2018 (Actual) | 20,035 | 494 | 554 | 419 | 19.19 | 0.00 |

February 2019 (Actual) | 23,716 | 354 | 420 | 263 | 12.04 | 0.00 |

February 2020 (Actual) | 29,875 | 808 | 740 | 177 | 8.02 | 0.00 |

February 2021 (Estimate) | 30,900 | 910 | 922 | 420 | 18.95 | 0.00 |

*Unit: Million yen. The estimated values were provided by the company.

This Bridge Report presents Yoshimura Food Holdings K.K.’s earnings results for the fiscal year ended February 2020, etc.

Table of Contents

Key Points

1. Company Overview

2.Fiscal Year ended February 2020 Earnings Results

3.Fiscal Year ending February 2021 Earnings Estimates

4.Business Strategy

5.Conclusions

<Reference: Regarding Corporate Governance>

Key Points

- The company has developed an original business model in the food industry and pursues growth with two engines: “the increase in the number of group companies” and “the expansion of business of existing group companies.”

- For the term ended February 2020, sales were 29,875 million yen, up 26.0% year on year, and operating income was 808 million yen, up 127.7% year on year. EBITDA increased 68.5% year on year to 1,623 million yen. The existing domestic businesses were sluggish as the cost of ingredients and materials remained high and personnel and transportation expenses rose, but sales and profit increased substantially thanks to SIN HIN, which was Singaporean enterprise and acquired through M&A in the previous term, and the two companies (PACIFIC SORBY and Mori Yougyojou), which were acquired through M&A this term. The results exceeded the initial estimates. Meanwhile, net income fell 32.8% year on year to 177 million yen, which was below the initial forecast, due to fluctuations in exchange rates on the settlement date and the reversal of deferred tax assets of subsidiaries.

- For the term ending February 2021, sales are estimated to be 30,900 million yen, up 3.4% year on year, and operating income is projected to be 910 million yen, up 12.6% year on year. EBITDA is estimated to be 1,739 million yen, up 7.1% year on year. Both sales and profit are expected to mark a record high. The companies that were acquired in the previous term will contribute to the results for the full year. While profits will increase in the domestic business due to the improved performance of the manufacturing business, the overseas business was forecasted conservatively, considering the impact of the new coronavirus pandemic. No new M&A is expected.

- The effects of the new coronavirus pandemic as of April 15, 2020 are as follows.

- In Japan, sales to supermarkets and mass retailers are on the rise due to the increase in meals at home following the stay-at-home advisories in response to the new coronavirus pandemic. Because most of the company’s domestic sales target supermarkets and mass retailers, the demand for dry noodles, jellies, peanut butters, shumais and dumplings increased until March. However, it does not anticipate that this trend will continue. Therefore, it did not include the impact of the latest increase in demand in the forecasts.

- The main sales destinations in Singapore are supermarkets, hotels and restaurants. Sales to supermarkets are on an increasing trend, as people are refraining from going out to cope with the new coronavirus pandemic, as in Japan. On the other hand, sales to hotels and restaurants are on a declining trend because of the decrease of tourists and the stay-at-home advisories. The forecasts for the current term are conservatively prepared on the assumption that the current trend of sales decline will continue for the full year.

- The company is not the only one which is affected by the new coronavirus pandemic and future outlook remains uncertain for all companies. In the short run, it will be difficult to externally judge the rationality of the forecasts for this term as of April. Therefore, although the company revised its strategies and decided that “Listing of YOSHIMURA FOOD HOLDINGS ASIA on the Singapore market would be postponed,” we would like to pay attention to how it will pursue growth strategies with two engines: “the increase in the number of group companies” and “growth through the expansion of business of existing group companies” from the next term. In particular, it may be in a favorable environment for securing excellent human resources to strengthen the support system for the group companies.

1.Company Overview

Yoshimura Food Holdings acquires small and medium-sized food products makers, facing various issues such as the difficulty in finding successors, through M&A at the same time as they possess excellent products and technologies. It also facilitates the growth of the entire corporate group by solving problems with their core skill, “a platform for supporting small and medium-sized enterprises (SME Support Platform),” and energizing each group company. Its strengths are an overwhelming advantage compared to investment funds and large companies as well as a high entry barrier. In recent years, the company has been concentrating on overseas M&A. As of the end of February 2020, there are 19 major consolidated subsidiaries.

【1-1 Corporate History】

One day, a food company that was facing financial difficulties and could not find a buyer was introduced to Mr. Yoshimura, who was managing the listed companies’ fundraising and M&A in the corporate business division at Daiwa Securities Co. Ltd. and Morgan Stanley Securities Co., Ltd.

Mr. Yoshimura took on this food company and established L Partners Co., Ltd. on his own in March 2008, which was the predecessor of Yoshimura Food Holdings K.K. because he strongly felt that Japan could be more appreciated through its “food” since his MBA days in the USA while working for Daiwa Securities. Through his efforts to revitalize the company using his experience and network, he succeeded in turning a profit.

Many food SMEs started seeking help from Mr. Yoshimura upon learning about his reputation. He thought that it was possible to efficiently achieve results if the companies complemented each other in various functions, such as product development, production, and sales under a holding company system, instead of working on each company individually. Hence, he named the corporate Yoshimura Food Holdings K.K. in August 2009.

Since then, the company has continued acquiring companies facing problems with business succession or failing to handle management on their own. Due to the high reputation of the company for its unique position of not competing with major food companies and investment funds and its policy of not selling the companies it acquired, it received financing from Japan Tobacco (JT) and expanded its business. In March 2016, it was listed on the Mothers of Tokyo Stock Exchange, and in March 2017, it was listed in the first section of Tokyo Stock Exchange.

The company is pursuing further growth by acquiring not only Japanese companies, but also overseas companies in Singapore, Malaysia, etc.

【1-2 Market Environment and the Background of the Company’s Establishment】

As a company aiming for supporting and revitalizing SMEs throughout Japan, Yoshimura Food Holdings explained the conditions of the food SMEs as follows:

(Investment Bridge extracted, summarized and edited the information from Yoshimura Food Holdings’ annual securities reports and reference material)

(The Conditions of the Food SMEs)

*Japanese cuisine has been highly appreciated worldwide and is attracting attention. Also, on the national level, the food manufacturing industry has been one of the largest industries based on its number of business establishments, number of employees and GDP since the 1990s and it is one of the key industries that Japan is proud of.

*99% of the companies are SMEs where each one of them has strong products and technical skills.

*However, the domestic market scale is shrinking and some of the food SMEs find it hard to survive on their own as the business environment remains stringent due to the falling birthrate and aging population.

*Therefore, many companies give up on continuing their businesses and end up choosing to close down or suspend their business.

(Conditions of the SMEs’ Business Succession)

*The average age of managers is 59.7, and it is expected that around 50% of the managers will reach the average retirement age in the upcoming 10 years as the average retirement age of managers is around 70.

*Under such conditions, two-thirds (66.4%) of domestic companies do not have a successor. The percentage of companies, with presidents in their 60s, which have finished the business succession or prepared for business succession is only around 36%. Thus, the preparation for business succession has not progressed.

*Moreover, in 2018, the number of SMEs that suspended or discontinued business doubled to reach 46,724 in comparison with the previous year where that number was around 21,000.

(According to SME Agency “White Paper on Small and Medium Enterprises” (2019 Edition), Teikoku Databank, “Analysis of the age of company presidents in Japan (2019),” Teikoku Databank, “Survey of Trends on ‘Companies without a Successor’ in Japan” (2018), Teikoku Databank, “Survey of Companies’ Attitude towards Business Succession” (2017) and data from Tokyo Shoko Research, Ltd.)Ltd.Ltd.Ltd.

(Conditions of Business Succession of Food SMEs through Acquisition)

*Although there are increasing needs for business succession from food SMEs, the number of companies and organizations that would acquire them is small.

*The scale of many food SMEs is too small for major companies to acquire.

*Furthermore, investment funds’ primary aim is to rapidly grow independent companies and sell them off within a few years. Therefore, the mature market of food SMEs tends not to be one of their investment targets.

*Under these conditions, there is a tremendous shortage in the bearers of the responsibility of taking on the business of the SMEs.

【1-3 Business Description】

Having Yoshimura Food Holdings as its holding company, the corporate group consists of 19 group companies.

Yoshimura Food Holdings aims to support and revitalize SMEs that manufacture and sell food products by creating a corporate group, composed of the food SMEs that are facing problems in securing a successor, through M&A. Yoshimura Food Holdings is responsible for business strategies’ design and implementation, as well as the business management of each company in the group. It also supports and supervises their sales, manufacturing, procurement, distribution, product development, quality control, and business management.

① Business Model

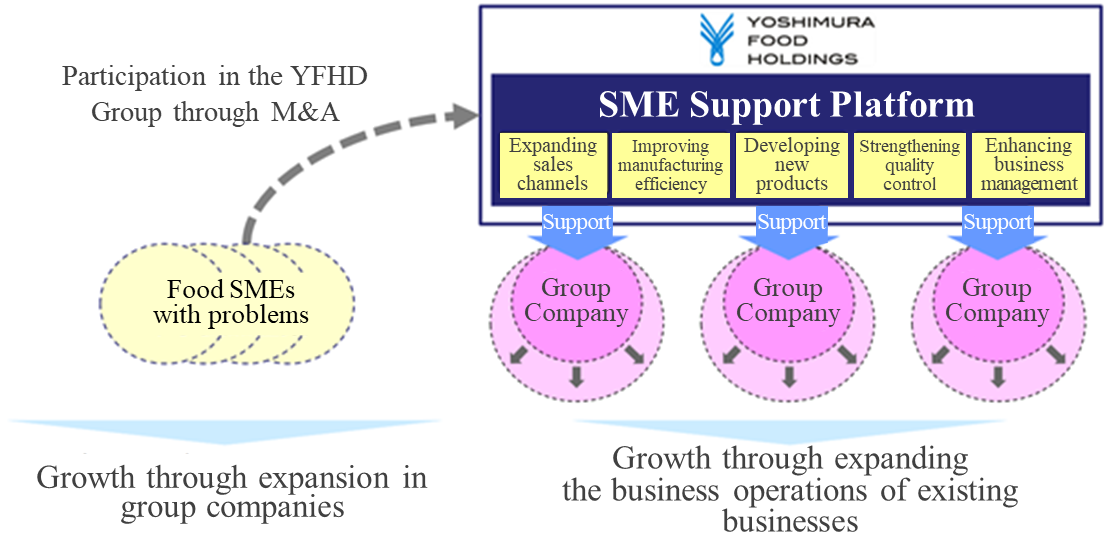

The company developed a unique business model in the food industry and is pursuing growth based on two engines.

One of them is the increase in the number of group companies.

Since its establishment in 2008, the company prevented food SMEs that had business succession and financial problems from shutting down or facing business suspension by acquiring them. Thus, it has managed to solve their problems.

As of February, 2020, the company had 19 group companies. It is recently focusing on adding not only Japanese companies to the group, but also overseas ones.

Target companies are found by mainly M&A mediating companies, local financial institutions such as regional banks, lawyers and accountants. The company plans to improve its own function for finding target companies from the aspect of costs as well.

The other one is the expansion of business of existing group companies.

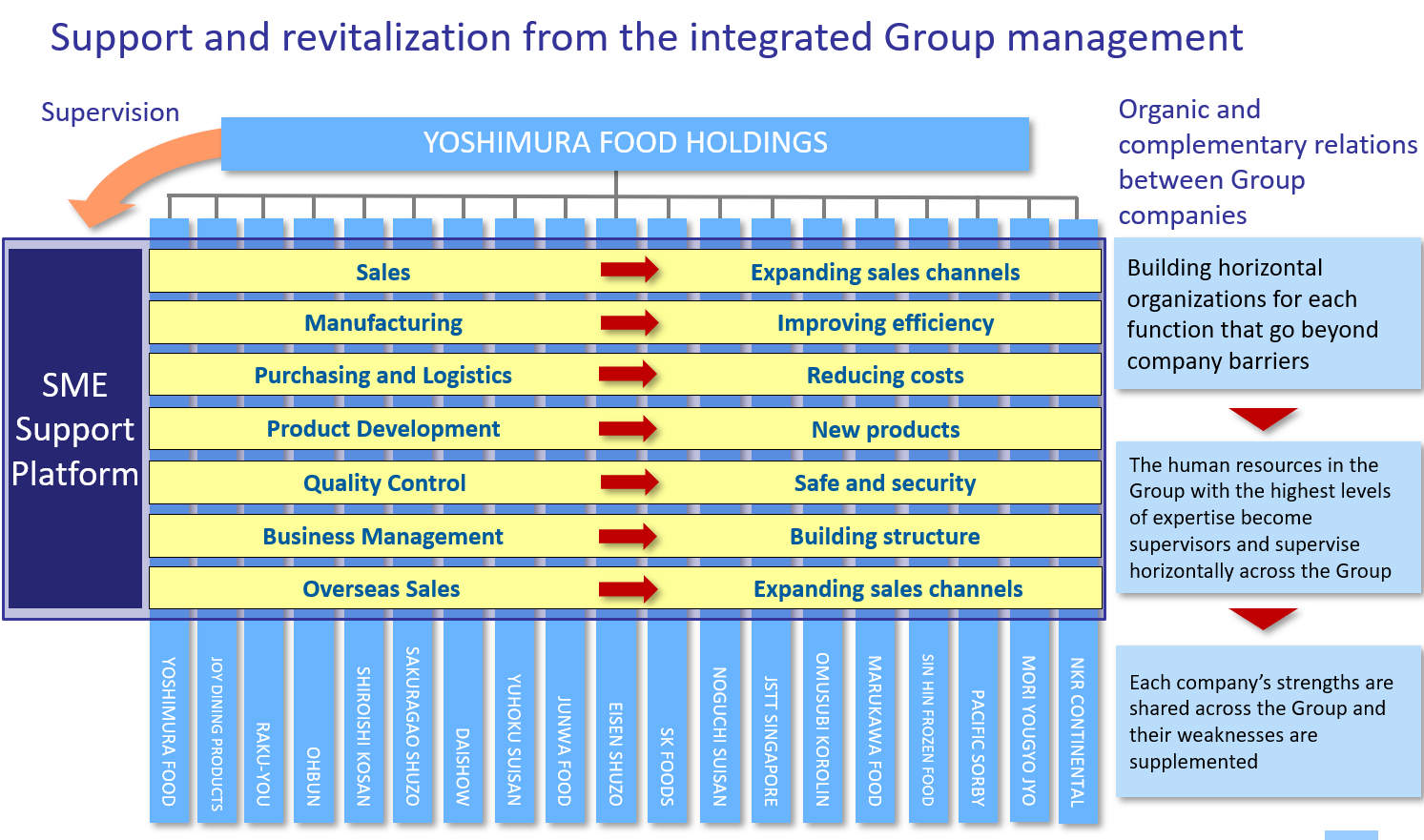

Yoshimura Food Holdings supports the expansion of business operations of each company and solves problems by supervising each function of these companies, which have excellent products and technologies but could not achieve growth for reasons such as the lack of sales channels, labor shortage or poor business management, through the “SME Support Platform.”

(Taken from the reference material of the company)

What is the SME Support Platform?

The core of this unique business model is the “SME Support Platform,” a product of the company’s accumulation of know-how and achievements through its specializing in food manufacturing and sales.

As a holding company, Yoshimura Food Holdings is responsible for business strategies’ design and implementation, as well as the business management of each subsidiary in the group. It also aims to strengthen the business foundation of each subsidiary through the company supervisor’s horizontal supervision of its functions (sales, manufacturing, procurement, distribution, product development, quality control and business management) in a manner that goes beyond the company barriers and through his support for the business by building organic relations between subsidiary companies.

For example, Company A which has an excellent product but is worried about sales growth can use the sales channels and sales know-how of Company B that has a nationwide sales network. Also, it can achieve a stable financial position by using the creditworthiness of Yoshimura Food Holdings which is listed in the stock market to raise funds.

This cooperation is made to be more effective through appointing the personnel in the group with the highest levels of expertise as supervisors.

Hence, the “SME Support Platform” is a system in which each company’s “strengths” such as strong products and technologies, sales channels, and manufacturing know-how are shared across the group and their “weaknesses” such as a shortage in personnel, funds, or sales channels are supplemented.

(Taken from the reference material of the company)

② Segments

The company has two segments: “manufacturing business segment” and “sales business segment.”

◎ Manufacturing Business Segment

Each company develops, manufactures and sells its unique products mainly through wholesalers to supermarkets, convenience stores, drug stores, hotels, restaurants, etc. in Japan.

(Group Companies within the Manufacturing Business Segment)

Company Name | Features |

RAKU-YOU INC. (Adachi Ward, Tokyo)

| Six factories in Japan manufacture and sell chilled shumai and chilled dumpling. It has the largest share of chilled shumai production in Japan. In the term ended February 2019, the company sold approximately 28.12 million packages of its main product, chilled shumai. |

Ohbun Co., Ltd. (Shikokuchuo City, Ehime Prefecture) | It has an independent route to procure oysters with a limited supply from Hiroshima Prefecture. Fried oysters are its leading product, but it also manufactures and sells other products such as deep-fried chicken cutlets and fried chicken breast. |

Shiroishi Kosan, Inc. (Shiroishi City, Miyagi Prefecture) | Founded in 1886. Its leading product is Shiroishi hot noodles, which are a specialty of Shiroishi City. The company also sells dry noodles and other products using traditional manufacturing methods. |

Daishow Co., Ltd. (Tokigawa-machi, Hiki-gun, Saitama Prefecture) | It is a pioneer in the peanut butter industry. “Peanut Butter Creamy” made by its own unique manufacturing methods has been continuously a long-selling product since started being sold in 1985. |

Sakuragao Shuzo K.K. (Morioka City, Iwate Prefecture) | It was established in 1973 as a collective of 10 local breweries in Iwate Prefecture. Its sake which is brewed using the skills of the biggest Toji (head brewers) group in Japan, Nanbu Toji, has a high reputation for its fruity taste. |

Yuhoku Seafood Processing Co., Ltd. (Oi-machi, Ashigarakamigun, Kanagawa Prefecture) | The company manufactures and sells negitoro and tuna slices using tuna that is immediately frozen on the ship at minus 50-60 degrees as soon as it is caught. |

JUNWA FOOD Corporation (Kumagaya City, Saitama Prefecture)

| It has constructed a perfect quality control system, including having acquired the Saitama Prefecture HACCP. Although it is a jelly manufacturing start-up company, it has an established reputation by major hypermarkets for its products’ quality and technological capabilities. |

Eisen Shuzo Co., Ltd. (Bandai-machi, Yama-gun, Fukushima Prefecture) | It was established in Aizu Wakamatsu in 1869. In a serene natural environment, the company brews delicious sake with a smooth taste that you would never get tired of drinking by employing traditional handmade techniques that have been inherited through generations to utilize the five senses to the maximum and using the crystal clear water from “the natural springs in the western foot of Mt. Bandai that has been designated as one of the Best 100 Natural Water Resources in Japan.” |

SK Foods Co., Ltd. (Yorii-machi, Osato-gun, Saitama Prefecture) | It mainly manufactures and sells chilled and frozen pork cutlet and makes products that meet customer needs. Also, it conducts direct procurement and direct sales without depending on any trading companies. |

Yamani Noguchi Suisan K. K. (Rumoi City, Hokkaido Prefecture) | For half a century, the company has manufactured and sold Hokkaido Prefecture’s specialties such as salmon jerky and herring that are prepared by its skilled workers who use unique manufacturing techniques. |

JSTT SINGAPORE PTE. LTD. (Singapore) | The company located in Singapore manufactures and sells sushi, makimono, rice balls, etc. by using fresh Japanese seafood transported by air. |

Omusubi Kororin Honpo K.K. (Azumino City, Nagano Prefecture) | Using its own freeze-dry device, it manufactures ingredients for confectionery, emergency food, etc. The company’s “Mizu Modori Mochi” (rice cakes that can be prepared by adding water) is famous for being used in the Space Shuttle Endeavour. |

Marukawa Shokuhin Co, Ltd. (Iwata City, Shizuoka Prefecture) | A famous dumpling shop in Hamamatsu area. It manufactures and sells dumplings using carefully selected ingredients and a secret recipe the company has been following since its establishment. |

PACIFIC SORBY PTE. LTD. (Singapore) | The company procures frozen seafood and fresh fish, and it processes and sells them by wholesale to hotels and hospitals in Singapore. The products the company mainly handles are frozen seafood, such as crab, lobster, shrimp and salmon, and fresh fish caught in the sea around Singapore. |

Mori Yougyojou Co., Ltd. (Ogaki City, Gifu Prefecture) | An ayu (sweetfish) farming company that runs three fisheries in Gifu Prefecture and possesses the best scale and high-level facilities among fish farming companies in Japan. As an old-established company that has been running a business for more than 50 years, it raises high-quality ayu (sweetfish) using advanced fish farming technologies, the plentiful groundwater of “the Land of Pure Water Gifu,” and the large-scale farming facilities that are managed by technicians. |

NKR CONTINENTAL PTE. LTD. (Singapore) | The company designs, manufactures and sells commercial kitchen equipment mainly to luxury hotels and restaurants in Singapore and Malaysia. |

◎ Sales Business Segment

Having sales and planning functions as its strengths, the section of this business plans and develops products that meet the consumer needs and mainly sells its products to industrial channels and supermarkets.

(Group Companies within the Sales Business Segment)

Company Name | Features |

Yoshimura Food Co., Ltd. (Koshigaya City, Saitama Prefecture) | Mainly conducts the planning and sales of industrial food ingredients. It does not have distribution channels, but it has constructed a business model where it sends products directly to customers. |

Joy Dining Products Co., Ltd. (Koshigaya City, Saitama Prefecture) | It conducts the planning and sales of frozen foods. Also, it has direct accounts with consumer co-ops throughout Japan and utilizes them to sell the products of the group companies. |

SIN HIN FROZEN FOOD PRIVATE LIMITED (Singapore) | It procures high quality, safe and trusted frozen seafood products and processed seafood products from the influential seafood companies in various parts in Asia. |

【1-4 Characteristics and Strengths】

①The Advantage in Business Succession through Acquisition

There are influential players in the M&A, such as major food companies and investment funds; however, this company has three main points that form strong competitive advantages, which are explained below.

*Ability to Acquire Companies of Various Scales

The company does not aim to sell the companies it acquired. It aims to not only achieve short term business recovery, but also achieve sustainable growth from a medium to long term perspective. Therefore, the company can acquire a variety of SMEs, including those with a small business scale that would take time to achieve growth and those that lack management resources for growth. This point creates a huge difference between the company and other major food companies and investment funds that need the companies they will acquire to be of a certain scale. Moreover, it is not easy for investment funds aiming to generate capital gains from selling companies to gain the trust of owners and managers of food SMEs. Regarding this point, this company operating company groups with the aim of achieving sustainable growth from a medium-term perspective also has a huge advantage.

*Advanced Capability of M&A

Since its establishment, the company has worked on creating many company groups out of food-related SMEs and later has achieved re-growth of these companies. Thus, it has thorough knowledge of the market environment of the food industry, business practices and risks that are peculiar to food SMEs, and strong assessment abilities, which enable the company to choose companies that have strengths from a large number of SMEs.

Also, the company has an extremely high capability of M&A since it has great expertise and accumulated knowledge in due diligence and negotiations.

*Rich and High-Quality M&A Data through its Wide Network

The company can gather plenty of M&A data on the food SMEs since it has a wide network of financial institutions, such as city banks, regional banks, credit associations, securities companies and companies that provide M&A advisory services.

Furthermore, “the company’s specialization in the food industry” and “the reassurance that the company is not aiming to sell” are the two factors allowing the company to access not only to a huge amount of data, but also high-quality data that meets its needs.

②Core Skill: SME Support Platform

The company revitalizes the group companies through the “SME Support Platform” in which each group company’s “strengths” such as strong products and technologies, sales channels, and manufacturing know-how are shared across the group and their “weaknesses” such as a shortage in personnel, funds or sales channels are supplemented. These achievements are highly evaluated.

【1-5 Dividend Policy and Shareholders’ Benefit System】

(Dividend Policy)

Although payout to shareholders is one of the important business challenges, it is thought that allocating the cash to investment in the facilities to actively expand the business and to strengthen the business foundation by expanding the platform is what would lead to the highest payout to the shareholders because the company is considered to be within the growth process.

Therefore, the company has not provided dividend payout to its shareholders since its establishment and as of the time being, it plans to continue on using the cash to invest in business expansion and as necessary operating capital for the existing companies. The company is planning to look into providing dividend payouts to its shareholders while considering the operating performance and financial conditions for each business year.

(Shareholders’ Benefit System)

The company offers special benefits to the shareholders mentioned below according to the number of shares they hold.

Number of Shares | Number of Times to Receive Special Benefits | Special Benefit Content |

300 shares to 499 shares | Once a year (Shareholders recorded in the shareholder register as of the end of February of every year) | Products worth 800 yen from the group companies |

500 shares to 2,499 shares | Once a year (Shareholders recorded in the shareholder register as of the end of February of every year) | Products worth 1,500 yen from the group companies |

2,500 shares or more | Twice a year (Shareholders recorded in the shareholder register as of the end of February and on the 31st of August of every year) | Products worth 4,000 yen from the group companies each time |

Special Benefit Content(the photo is for illustrative purposes only)

|

(According to the company’s website)

2.Fiscal Year ended February 2020 Earnings Results

(1) Consolidated results

| FY 2/19 | Ratio to sales | FY 2/20 | Ratio to sales | YOY | Difference from the initial estimate |

Net sales | 23,716 | 100.0% | 29,875 | 100.0% | +26.0% | +6.0% |

Gross profit | 5,087 | 21.5% | 6,025 | 20.2% | +18.4% | - |

SG&A expenses | 4,732 | 20.0% | 5,216 | 17.5% | +10.2% | - |

Operating income | 354 | 1.5% | 808 | 2.7% | +127.7% | +25.1% |

Ordinary income | 420 | 1.8% | 740 | 2.5% | +76.1% | +12.1% |

Net income | 263 | 1.1% | 177 | 0.6% | -32.8% | -48.1% |

EBITDA | 963 | 4.1% | 1,623 | 5.4% | +68.5% | +39.3% |

*Unit: Million yen. Net income is profit attributable to owners of the parent. Expenses for M&A is not included in the EBITDA.

Sales and profit increased substantially, exceeding the initial forecast.

Sales were 29,875 million yen, up 26.0% year on year, and operating income was 808 million yen, up 127.7% year on year. EBITDA increased 68.5% year on year to 1,623 million yen. The existing domestic businesses were sluggish as the cost of ingredients and materials remained high and personnel and transportation expenses rose, but sales and profit increased substantially thanks to SIN HIN, which was Singaporean enterprise and acquired through M&A in the previous term, and the two companies (PACIFIC SORBY and Mori Yougyojou), which were also acquired through M&A this term. The results exceeded the initial estimates. Meanwhile, net income fell 32.8% year on year to 177 million yen, which was below the initial forecast, due to fluctuations in exchange rates on the settlement date and the reversal of deferred tax assets of subsidiaries.

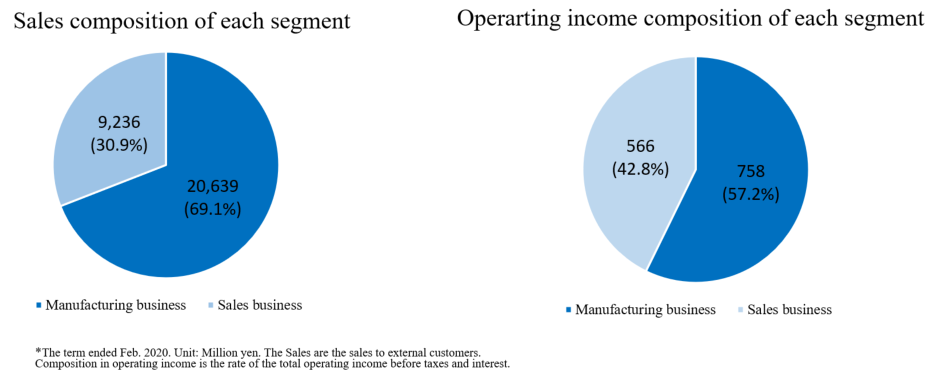

(2) Results of each segment

| FY 2/19 | Composition ratio | FY 2/20 | Composition ratio | YOY |

Net sales |

|

|

|

|

|

Manufacturing business | 17,165 | 72.4% | 20,639 | 69.1% | +20.2% |

Sales business | 6,550 | 27.6% | 9,236 | 30.9% | +41.0% |

Total | 23,716 | 100.0% | 29,875 | 100.0% | +26.0% |

Operating income |

|

|

|

|

|

Manufacturing business | 477 | 2.8% | 758 | 3.7% | +58.9% |

Sales business | 327 | 5.0% | 566 | 6.1% | +72.9% |

Adjusted amount | -449 | - | -516 | - | - |

Total | 354 | 1.5% | 808 | 2.7% | +127.7% |

*Unit: Million yen. The composition ratio of operating income means the ratio of operating income to sales.

*Manufacturing business segment

The two companies, PACIFIC SORBY and Mori Yougyojou, which were acquired through M&A, contributed to the result.

The steady growth in sales of national brand and exported products of JUNWA FOOD contributed to increased sales.

JSTT saw a temporary decline in sales due to the renovation and relocation of the main store.

*Sales business segment

SIN HIN, which newly joined the Group, contributed during the entire fiscal year.

(3) Financial conditions and cash flow

◎Main balance sheet

| End of 2/19 | End of 2/20 |

| End of 2/19 | End of 2/20 |

Current assets | 9,643 | 14,148 | Current liabilities | 7,248 | 9,749 |

Cash and deposits | 2,085 | 3,015 | Notes and accounts payable - trade | 2,298 | 2,757 |

Notes and accounts receivable - trade | 3,525 | 5,585 | Short term interest-bearing liabilities | 3,565 | 4,608 |

Inventories | 3,766 | 5,350 | Non-current liabilities | 3,336 | 7,449 |

Non-current assets | 5,537 | 9,729 | Long term interest-bearing liabilities | 3,183 | 7,119 |

Property, plant and equipment | 2,312 | 4,128 | Liabilities | 10,585 | 17,199 |

Intangible assets | 2,794 | 4,811 | Net assets | 4,595 | 6,678 |

Investments and other assets | 430 | 789 | Retained earnings | 2,038 | 2,216 |

Total assets | 15,180 | 23,877 | Total liabilities and net assets | 15,180 | 23,877 |

|

|

| Total interest-bearing liabilities | 6,748 | 11,728 |

*Unit: Million yen

Thanks to M&A, etc., total assets grew 8.6 billion yen from the end of the previous term to 23.8 billion yen.

Interest-bearing liabilities augmented 4.9 billion yen from the end of the previous term due to M&A, and total liabilities rose 6.6 billion yen from the end of the previous term to 17.1 billion yen.

Net assets increased 2.0 billion yen from the end of the previous term to 6.6 billion yen as retained earnings grew.

Capital-to-asset ratio dropped 14.0% from the previous term to 14.3%.

◎Cash flows

| FY 2/19 | FY 2/20 | Change |

Operating CF | 250 | 603 | +352 |

Investing CF | -2,075 | -5,004 | -2,928 |

Free CF | -1,824 | -4,401 | -2,576 |

Financing CF | 2,370 | 4,816 | +2,445 |

Balance of cash and cash equivalents | 2,072 | 2,495 | +422 |

*Unit: Million yen

The surplus of Operating CF increased due to the rise in income before taxes, etc. Investing CF and free CF saw a substantial increase in deficit as the expenses incurred for acquisition of shares of subsidiaries largely expanded.

The surplus of financing CF increased significantly as a result of a rise in borrowings. The cash position improved.

(4) Topics

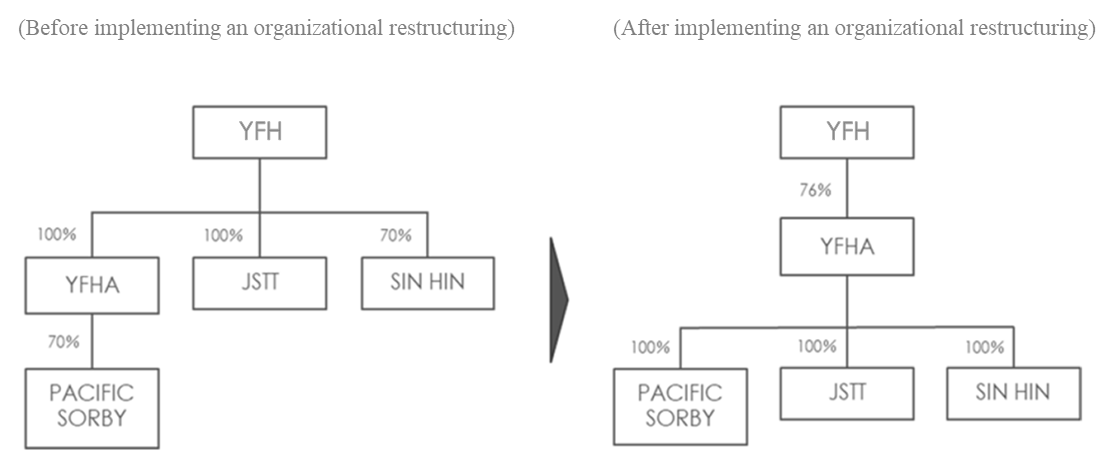

◎ Implementing an organizational restructuring in Singapore

The company established YOSHIMURA FOOD HOLDINGS ASIA PTE. LTD. as the regional headquarters in Singapore in April 2019. To expand the business in the Asian region, where market growth is expected to continue, and to establish an efficient and strong management system, it decided to restructure 3 companies that carry out businesses in Singapore, namely, JSTT SINGAPORE, SIN HIN FROZEN FOOD, and PACIFIC SORBY.

The above three companies became wholly owned subsidiaries of YOSHIMURA FOOD HOLDINGS ASIA by the in-kind investment of their own shares of YOSHIMURA FOOD HOLDINGS ASIA by shareholders and the corresponding issuance of new shares by YOSHIMURA FOOD HOLDINGS ASIA.

(Taken from the reference material of the company)

While continuing to aim for getting listed on the Singapore securities market, it intends to work on further business development by leveraging this restructuring.

◎ NKR, a company that manufactures, imports, sells and maintains commercial kitchen equipment, became a subsidiary

In January 2020, YOSHIMURA FOOD HOLDINGS ASIA PTE. LTD., which manages overseas business, made NKR CONTINENTAL PTE. LTD. its subsidiary, which manufactures, imports, sells and maintains commercial kitchen equipment in Singapore and Malaysia.

(Overview of NKR CONTINENTAL)

NKR CONTINENTAL is a group that designs, sells and installs commercial kitchen equipment purchased from manufacturers in the United States, Europe, and Japan and commercial kitchen equipment manufactured at its own factories, mainly in Singapore and Malaysia, to luxury hotels, hospitals, fast food chains, and restaurants.

*Major indicators of the term ended December 2018

Sales | 2,556 million yen |

Net income | 155 million yen |

Total assets | 3,329 million yen |

Net assets | 2,700 million yen |

*From the disclosed information of Yoshimura Food Holdings

*Major strengths

① Established position

It boasts a business history of more than 40 years in Singapore and Malaysia. It has been establishing trust relationships with major hotels (mainly 4-star and 5-star hotels) and major restaurant chains, and has accumulated technology and know-how. For this reason, it is well known and has gained trust in the commercial kitchen equipment industry to build its unique position and a stable profit base.

② Consistent service from design, manufacturing to installation

Since it has a specialized in-house team of design, manufacturing, installation management, installation, and maintenance, it can provide one-stop, high-quality and prompt services to customers. In particular, since it has its own factories in Singapore and Malaysia, it can quickly respond to the detailed requests from customers, and it has a high level of technical capability to manufacture and construct equipment with high-quality and complicated designs.

③ Prompt maintenance service

Because its maintenance department has several experienced technical personnel and parts inventories, it can quickly respond to a sudden equipment breakdown for customers. In other words, the company has established business bases. Because of this, it is obtaining high praise from the customers and continuing with transactions and receiving new orders.

(Background of making a subsidiary: Expected synergistic effects)

The company decided to acquire shares because it believes that it can achieve growth further with the following synergistic effects.

① Sharing channels with PACIFIC SORBY and SIN HIN

NKR CONTINENTAL has sales channels for major hotels, hospitals and restaurants in Singapore and Malaysia.

Meanwhile, PACIFIC SORBY, a subsidiary of YOSHIMURA FOOD HOLDINGS, established sales channels for hotels and hospitals in Singapore, and SIN HIN for restaurants in Singapore, respectively. By sharing each other’s sales channels, the total sales will grow. A major hotel in Singapore was introduced to PACIFIC SORBY by NKR CONTINENTAL, and the transaction has already started.

② Collaboration with the group companies of Yoshimura Food Holdings in Japan

Especially through the sales channel of NKR CONTINENTAL in Malaysia, where Yoshimura Food Holdings is currently developing businesses, sales growth is expected by selling products of the group companies in Japan.

(Overview of stock acquisition)

In January 2020, it acquired 70% of the issued shares from major shareholders such as the representative of NKR CONTINENTAL, and the current management continues to hold the remaining of 30%.

By building cooperative relationships and exerting synergistic effects, they will collaboratively expand business in the Asian region.

The acquisition cost was about 2 billion yen, which was covered by cash on hand and loans from banks.

3.Fiscal Year ending February 2021 Earnings Estimates

(1) Full-year earnings forecasts

| FY 2/20 | Ratio to sales | FY 2/21 (Estimate) | Ratio to sales | YOY |

Net sales | 29,875 | 100.0% | 30,900 | 100.0% | +3.4% |

Operating income | 808 | 2.7% | 910 | 2.9% | +12.6% |

Ordinary income | 740 | 2.5% | 922 | 3.0% | +24.6% |

Net income | 177 | 0.6% | 420 | 1.4% | +137.2% |

EBITDA | 1623 | 5.4% | 1,739 | 5.6% | +7.1% |

*Unit: Million yen. The estimates are provided by the company.

Sales and operating income are estimated to increase, hitting a record high.

Sales are estimated to be 30,900 million yen, up 3.4% year on year, and operating income is projected to be 910 million yen, up 12.6% year on year. EBITDA is estimated to be 1,739 million yen, up 7.1% year on year. Both sales and profit are expected to mark a record high. The companies that were acquired in the previous term will contribute to the results for the full year. While profits will increase in the domestic business due to the improved performance of the manufacturing business, the overseas business was forecasted conservatively, considering the impact of the new coronavirus pandemic. No new M&A is expected.

(2) Impact of the new coronavirus pandemic (as of April 15, 2020)

① Japan

Sales targeting supermarkets and mass retailers are on the rise due to the increase in meals at home following the stay-at-home advisories to prevent the spread of the new coronavirus. Because most of the company’s domestic sales are to supermarkets and mass retailers, demand for dry noodles, jellies, peanut butters, shumais and dumplings increased until March.

However, it does not anticipate that this trend will continue. Therefore, it did not include the impact of the latest increase in the demand in the forecasts for the current term.

② Singapore

The main sales destinations in Singapore are supermarkets, hotels and restaurants, etc. Sales to supermarkets are increasing because people are refraining from going out to cope with the new coronavirus pandemic, as in Japan. On the other hand, sales to hotels and restaurants are on a declining trend because of the decrease in tourists and the stay-at-home advisories.

The forecasts for the current term are conservatively prepared on the assumption that the current trend of sales decline will continue for the full year.

4.Business Strategy

Yoshimura Food Holdings has established an original business model in the food industry, and pursues growth with two engines: “the increase of the number of group companies” and “the expansion of business of existing group companies.”

Furthermore, the company makes efforts to secure and develop human resources to ensure sustainable growth of the business.

(1) Growth strategy

In response to the impact of the new coronavirus pandemic, the company had to undertake revisions for the current progress and the efforts as follows, but there is no change in the basic growth strategy based on the recognition of the business environment.

*Domestic M&A

The number of companies that are sold off is increasing due to the uncertain outlook in association with the new coronavirus pandemic, but the company will examine M&A projects more carefully than ever before and focus on high quality projects.

*Overseas M&A

The company will judge M&A in Singapore carefully based on the situation.

The listing of YOSHIMURA FOOD HOLDINGS ASIA in the Singapore market will also be postponed to the next term onwards, waiting for the market to settle down.

Meanwhile, it recognizes that the support system for the group companies is the most important function and is the source of its own competitiveness. Therefore, it will strengthen the system through aggressive investment (i.e. increasing personnel).

① Growth through the increase in the number of group companies

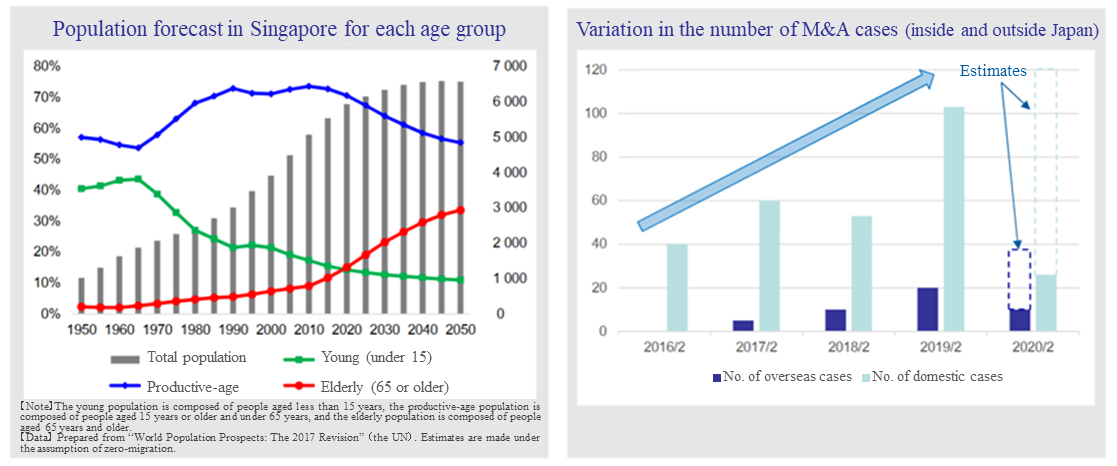

As mentioned in Section 1-2 “Market Environment and the Background of the Company’s Establishment,” the problem of business succession is getting more serious. The company gave over 100 M&A proposals in the term ended February 2019. As you can see, the number of M&A cases is increasing.

The ratio of cases attributable to the lack of successors is growing as well.

Due to the external environment and the increase in popularity of the company through listing, the number of M&A cases is expected to keep increasing. By taking advantage of the function to deal with business succession, the company will surely increase M&A.

Yoshimura Food Holdings, which acquired two Singaporean enterprises, JSTT in 2017 and SIN HIN in 2018, then acquired PACIFIC SORBY PTE. LTD. in 2019, and NKR CONTINENTAL in 2020.

As the network between the owners is strong in Singapore, the company expects to get various projects in the future as well.

Moreover, as the relationship has been good since the beginning, the company also expects to get benefits, such as the utilization of sales channels and other synergy effects, from its acquisition.

It will pursue growth through M&A outside Japan as well.

In Singapore, the aging of the population has been accelerated since 2015, and the productive-age population is estimated to decline. Therefore, the needs for M&A are expected to grow due to the lack of successors, similarly to the situation in Japan.

Over the past several years, the number of cross-border transactions between Yoshimura Food Holdings and overseas enterprises has been growing. Despite the aging population, which is an external factor, the company considers that its active stance is evaluated positively outside Japan as it has acquired JSTT and SIN HIN.

Since Taiwanese enterprises are suffering from the lack of successors as well, the same kinds of needs exist there. Accordingly, the Taiwanese market is considered promising.

(Taken from the reference material of the company)

② Growth through the expansion of business of existing group companies

The company will keep brushing up the mutual complement and growth functions of SME Support Platform and will strongly support new group companies while expanding operation of the existing businesses.

In addition, the company will work on the expansion of its overseas business as well based on this growth strategy.

JSTT sells sushi and rice balls produced at its own factory as well as importing and selling Japanese products at the sushi section of major supermarkets in Singapore. It also handles or sells the jelly of JUNWA FOOD, the sake of Sakuragao Shuzo, the furikake (dry Japanese seasoning) of Omusubi kororin, the salmon roes of Yamani Noguchi Suisan, the deep-fried oyster of Ohbun, the peanut butter of Daishow, and so on.

Especially, jelly of JUNWA FOOD sells well even when it is made in Japan, exported to Singapore, charged a handling fee and sold at a price that can yield sufficient profit, which indicates its high competitiveness.

The company plans to make various Japanese products available overseas without any preconception.

SIN HIN procures high-quality frozen seafood from major suppliers in Asia and sells it to wholesalers, retailers, restaurants, etc. in Singapore and other Asian countries. SIN HIN also supplies ingredients for sushi to JSTT, contributing to the procurement cost reduction of JSTT, and sells the jelly of JUNWA FOOD and the oyster of Ohbun.

Meanwhile, PACIFIC SORBY, which became a group company in April 2019, sells ingredients processed in-house to the clients of SIN HIN and proceeds with joint purchase with SIN HIN. In addition, the company aims to sell the sushi and rice balls produced by JSTT and the products of Japanese group companies via PACIFIC SORBY’s sales channels to hotels and hospitals. Further, the company started selling their products to SIN HIN’s customer.

NKR CONTINENTAL, which became a group company in January 2020, introduced a major Singapore hotel to PACIFIC SORBY, and the trading has already begun.

In such a way, Yoshimura Food Holdings aims to expand its business further in Asia in which market is expected to keep growing, and it established YOSHIMURA FOOD HOLDINGS ASIA PTE. LTD. in Singapore in April 2019 to manage local business by establishing an efficient, robust management system.

The company will apply its business model conducted in Japan, which is to grow business through M&A and synergy using SME Support Platform, to Asian markets based in Singapore.

The company is considering to list in overseas markets, such as Singapore Exchange (SGX) and Hong Kong Exchanges and Clearing, and aims to grow by enhancing its capability of fund procurement, credibility, and popularity.

Founders can first cash out some of their shares and expect that their share prices will rise through listing. Accordingly, the company considers that this is effective as an incentive for selling their companies.

(2) Strengthening the management base

In order to implement the above two growth strategies effectively, the most important task is to secure and develop human resources.

The company has , so far, been focusing on selecting and developing excellent human resources from inside the company, in a view to appropriately handle the work at owners’ SMEs.

However, the company has also started making efforts to recruit external human resources for dealing with an urgent need for enhancement of support systems in response to the increase of the number of group companies. It mainly focuses on recruiting personnel with a great deal of experience at major food companies and general trading companies.

5.Conclusions

The company is not the only one which is affected by the new coronavirus pandemic and future outlook remains uncertain for all companies. In the short run, it will be difficult to externally judge the rationality of the forecasts for this term as of April. Therefore, although the company revised its strategies and decided that “Listing of YOSHIMURA FOOD HOLDINGS ASIA on the Singapore market would be postponed,” we would like to pay attention to how it will pursue growth strategies with two engines: “growth through the increase in the number of group companies” and “growth through the expansion of business of existing group companies” from the next term. In particular, it may be in a favorable environment for securing excellent human resources to strengthen the support system for the group companies.

<Reference: Regarding Corporate Governance>

◎Organization type, and the composition of directors and auditors

Organization type | Company with an audit and supervisory board |

Directors | 5 directors, including 2 outside ones |

Auditors | 3 auditors, including 3 outside ones |

◎Corporate Governance Report

The latest update: May 31, 2019

<Basic Policy>

Our company believes that our sustainable growth and creation of mid/long-term corporate value can be achieved especially through the trusting relationships and cooperation with our stakeholders, including shareholders, clients, business partners, employees, and local communities.

Accordingly, we consider that the most important mission in management is to keep tightening corporate governance as a base for securing the soundness, transparency, and efficiency of business administration. We will strive to secure the transparency and fairness of our company and timely disclose information to all stakeholders by streamlining the decision-making process, improving the supervisory function for business execution, strengthening the function to oversee directors, and developing an internal control system.

<Principles that have not been followed and the reasons>

Principle | Reason for not following the principle |

<Supplementary Principle 1-2-4> | We have not adopted the electronic exercise of voting rights. We do not translate convocation notices into English, either. We will think of them while considering the ratio of overseas shareholders, etc. |

<Supplementary Principle 4-1-2> | Although our company has formulated a mid-term management plan, we do not disclose it as of now because it is difficult to estimate the effects of M&A, which is the pillar of our business. From now on, we will consider announcing our mid/long-term vision for growth, so as to gain a further understanding of shareholders. |

<Disclosure Based on the Principles of the Corporate Governance Code (Excerpts)>

Principle | Disclosed information |

<Principle 1-4 Strategically held shares> | For the purpose of maintaining and strengthening transaction relations, we hold shares strategically to a limited extent. In this case, we judge whether or not to invest, while comprehensively considering the benefits, risks, capital costs, etc. arising out of the maintenance and strengthening of transaction relations, and whether they would contribute to the increase in our corporate value. The board of directors examines economic rationality of individual strategically held shares every year, such as whether the benefits and risks arising out of strategic holding of each stock will recoup capital cost and whether it will increase our corporate value from the mid/long-term viewpoint. We will try to reduce the number of shares we hold if we determined that the significance of holding of that stock is not sufficient. We exercise voting rights appropriately with the criteria considering whether it will lead to the increase in corporate value from the mid/long-term viewpoint or whether it will degrade the significance of shareholding. We will not agree with any proposals by the company or a shareholder that would degrade the share value. |

<Principle 5-1 Policy for promoting constructive dialogue with shareholders>

| Our IR activities are led by the representative director and CEO, and operated by the management department. For shareholders and investors, we regularly hold a briefing session, targeting analysts and institutional investors, to enrich the dialogue with shareholders, and the results of each session are reported to directors and the management. |

This report is intended solely for information purposes, and is not intended as a solicitation to invest in the shares of this company. The information and opinions contained within this report are based on data made publicly available by the Company, and comes from sources that we judge to be reliable. However, we cannot guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness or validity of said information and or opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration. Copyright (C) 2020 Investment Bridge Co., Ltd. All Rights Reserved. |