| Pressance Corporation Co., Ltd. (3254) |

|

||||||||

Company |

Pressance Corporation Co., Ltd. |

||

Code No. |

3254 |

||

Exchange |

TSE 1st Section |

||

Industry |

Real estate business |

||

President |

Shinobu Yamagishi |

||

Address |

Crystal Tower, 1-2-27 Shiromi, Chuo-ku, Osaka |

||

Year-end |

End of March |

||

URL |

|||

*The share price is the closing price on December 16. The number of shares issued was taken from the latest brief financial report.

ROE and BPS are the values for the previous term. *4-for-1 share split was conducted on Oct. 1, 2016. The DPS and dividend yield are annual values obtained without taking into account the share split. |

||||||||||||||||||||||||

|

|

* The forecast is from the company.

* From the FY 3/16, net income is profit attributable to owners of the parent. Hereinafter the same applies. * 4-for-1 share split was conducted on Oct. 1, 2016. The DPS and dividend yield are annual values obtained without taking into account the share split. |

| Key Points |

|

| Company Overview |

|

In 2002, the company was renamed "Pressance Corporation Co., Ltd." From the Kinki region, the company expanded its business area and released "Pressance Nagoyajo-mae," the first originally developed condominium in the Tokai area, in 2003, expanding its operations steadily. Then, it was listed in the second section of Tokyo Stock Exchange in 2007. In 2008, it opened Tokyo Branch, commencing business operation in the Tokyo Metropolitan Area. Thanks to the steady expansion of its business area, the company withstood the effects of the bankruptcy of Lehman Brothers, and kept growing. Then, it was listed in the first section of the Tokyo Stock Exchange in 2013. The "Light up your corner" spirit  ◎ Market environment According to the company's data (source: Real Estate Economic Institute) in the category of condominiums for sale, the company enjoys high market shares; it ranks first in the Kinki region for the sixth consecutive year (1,669 in 2015), ranks first in the Tokai and Chukyo regions for the fifth consecutive year (695 in 2015), and ranks sixth nationwide (2,512 in 2015).  ◎ Competitors

Pressance Corporation was compared with the enterprises listed in the above table from various aspects.

Meanwhile, PBR exceeds 1, but PER remains low despite that its share price has risen. It is necessary to further increase investors' awareness of the company and to promote understanding of its growth strategy. ◎ Product mix

The outlines of the condominiums handled by the company are as follows:The approximate average price is 16 million yen for single-room condominiums and 32 million yen for family condominiums.   * The sale of condominium buildings means the wholesale of the whole or part of each condominium building to condominium dealers.

* The sale of other housing means the sale of houses, including used houses and single-family houses, other than newly built condominiums.

* The sale of other real estate means the sale of real estate, including commercial stores and sites for development, other than housing.

* Business accompanying real estate sale includes the agent commission for condominium sale and paperwork accompanying real estate sale.

◎ Sales by region

The cumulative sales volume during a period from November 1998, in which the company started selling original brand condominiums, to the end of September 2016 are 470 buildings and 30,512 condominium units nationwide, especially in the Kinki, Tokai, and Chukyo regions.

Pressance Corporation targets the Kinki, Tokai, and Chukyo regions for selling single-room condominiums, and Tokyo and Okinawa in addition to the above regions for selling family condominiums. The Tokyo Metropolitan Area has a large market scale, but considering land procurement cost, selling prices, etc., the company refrains from handling single-room condominiums, but sells family condominiums only. The company plans to enhance its brand power and market share further in the Kinki, Tokai, and Chukyo regions and to proceed with deployment in new regions, such as Hiroshima and Hakata. (1) Plentiful experience of supplying condominiums and large market share Its large share brings some significant advantages, including the reduction in construction cost and the enhancement of information gathering capability, with the advantage of scale. (2) Strong selling power

As for the sale of single-room condominiums, the entire sales section is selling the same real estate intensively. Because all of the sales staff sell real estate under the same conditions, in-company competitions are intensified and the morale of sales staff improves.Since sales staffs sell only the same brand developed in-house, they are versed in the specs and features of real estate, and so they won the trust of customers. In addition, the company makes efforts to find potential users in various ways, and flexibly responds to the changes in demand and market situations. Personnel are the driving force for strengthening and growing sales capabilities. Therefore, the company puts considerable energy into personnel education. The strong selling capability of the company originates from the educational capability of the company. It is important to train new employees so that they will become helpful in actual business as soon as possible. To do so, the company instructs new employees to accompany their seniors, to see, listen to, and experience all kinds of scenes till sale, including telephone responses to customers, the preparation of documents, and talks with visitors, repeatedly. By accumulating successful experiences, new employees will grow by themselves and become able to complete each project. Thanks to these factors, the company sells out condominiums early and has stable sales. (3) Sound financial position

Pressance Corporation keeps capital-to-asset ratio high, based on high profit rate, the small amount of completed inventory, early recouping of funds, early repayment of project loans, etc., and can procure land in an advantageous manner.

In addition, land was procured actively, increasing debts and then decreasing capital-to-asset ratio, but this was not so serious as to affect the financial soundness of the company. (4) Excellent product competitiveness

The satisfaction level of buyers is high in the three aspects of "locations," "specs," and "prices." As for "locations," the company puts importance on convenience and advance property, and rigorously selects real estate within 10 minutes on foot from a major station in the urban area. As for "specs," the company puts emphasis on luxury, comfort, and functionality, and places high added value on real estate by equipping condominiums with a modular bathroom with a built-in dryer ventilator, floor heating systems based on gas-heated hot water, soundproof sashes, and noise insulation wooden floors as standard amenities. As for "prices," the company has achieved high cost-effectiveness by setting reasonable prices while keeping luxury. Through these efforts, its condominiums possess high asset and brand values in the long term.  (5) Outstanding information gathering capability

For condominium developers with the desire for business expansion, it is essential to gather information on good sites for building condominiums from brokers, financial institutions, etc. ahead of any other competitors.In the wake of the bankruptcy of Lehman Brothers, while many competitors became unable to procure land, Pressance Corporation had good financial standing, so it actively procured land by taking advantage of the situation. For brokers, etc., the existence of Pressance Corporation, which actively procured land amid the economic downturn, was very important. In addition, the company could make a swift decision compared with leading developers, which also was very attractive to brokers, etc. Accordingly, Pressance Corporation won a reputation as "a trade partner that would bring significant advantages." Consequently, brokers, etc. started "offering the latest information on land to Pressance." This relation is even stronger now after the aftershock of Lehman's fall subsided, which is one of the reasons why the company is highly competitive. Because of Pressance Corporation's swift decision-making and improved brand power, an increasing number of clients first contact Pressance even for large-scale projects, rather than leading developers. (6) Stable earning capability

Pressance Corporation was listed in the stock market in December 2007, and it has released its financial statements 8 times from the term ended March 2009 to the term ended March 2016. The comparison between the initial estimates and actual results of sales and ordinary income indicates that sales did not reach the initial estimates 4 times, while ordinary income has never failed to reach the initial estimates since the listing in the stock market.Without being affected by the real estate market situation, the company can earn profit stably and continuously. This is a remarkable characteristic of this company.   Since the three indices (i.e. operating income, ROE, and market capitalization) in the past 3 years satisfied certain criteria, Pressance Corporation was included in JPX-Nikkei Index 400* in August 2015. In addition, the stock of the company was designated as one of the stocks used for determining the new index "JPX-Nikkei Mid and Small Cap Index *2" in Dec. 2015. The company plans to make efforts to keep ROE high. * JPX-Nikkei Index 400

This is the share price index composed of the shares of "400 companies with high appeal for investors" which meet requirements of global investment standards, such as efficient use of capital use and investor-focused management perspectives. *2 JPX-Nikkei Mid and Small Cap Index The range of small- to medium-sized stocks is determined according to market cap and trading volume, and they are ranked according to ROE and cumulative operating income in the past 3 years. This is a share price index based on 200 stocks of companies that are attractive from the viewpoint of investment, considering the qualitative conditions, such as the company having more than one independent outside director and producing the English versions of documents. |

| First Half of Fiscal Year March 2017 Earnings Results |

Sales and profit dropped, but exceeded initial estimates, indicating healthy progress

Sales are 61,498 million yen, down 1.3% year on year. The performance of single-room condominiums remained healthy, but the number of completed family condominiums that can be included in sales was smaller as compared with the same period of the previous year, and sales declined. Due to the augmentation of construction work cost, etc., gross profit rate decreased 1.4%. As sales dropped, the augmentation of SG&A was not covered, resulting in an operating income of 11,997 million yen, down 15.6% year on year, and an ordinary income of 11,910 million yen, down 15.8% year on year. Sales and profit decreased year on year, but the progress rate toward the full-year forecast is healthy as a whole.  (Real estate sale business)

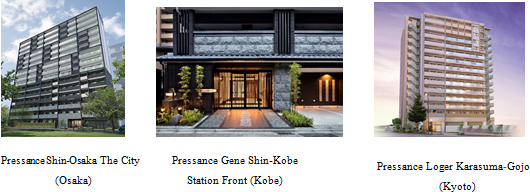

The sale of Pressance Shin-Osaka The City (a total of 186 units), etc. of the single-room condominium "Pressance Series" progressed healthily, but as mentioned above, the number of family condominiums handed over to customers decreased year on year.

* The sale of condominium buildings means the wholesale of the whole or part of each condominium building to condominium dealers.

* The sale of other housing means the sale of houses, including used houses and detached houses, other than newly built condominiums.

* The sale of other real estate means the sale of real estate, including commercial stores and sites for development, other than housing.

* Business accompanying real estate sale includes the agent commission for condominium sale and paperwork accompanying real estate sale.

(Others)

The real estate for lease owned by the company was operated in a healthy manner, increasing the income from rents.

As short-term and long-term interest-bearing liabilities augmented, total interest-bearing liabilities augmented by 13,199 million yen from the end of the previous term to 69,905 million yen. As a result, equity ratio dropped by 1.0% from the end of the previous term to 39.4%. The inventory assets for acquired land, which is calculated by subtracting construction prices, etc. from the inventory assets in BS (sum of real estate for sale and real estate for sale in process), was 18,766 million yen (5,287 units) for single-room condominiums, and 36,610 million yen (5,004 units) for family condominiums. When it is assumed that 1,600-1,700 single-room condominium units and 1,500-1,800 family condominium units will be handed over to customers every term from this term, it can be said that the company has already secured the land for three terms till the term ending Mar. 2019.  Since the income from long-term debt grew, financial CF increased further. The cash position improved. |

| Fiscal Year March 2017 Earnings Estimates |

There is no change to the earnings forecast. Sales and profit will grow for 7 consecutive terms, marking a record high.

The full-year earnings forecast has not been revised. Sales are estimated to grow 27.7% year on year to 100,839 million yen, exceeding 100 billion yen. The cost of acquiring land for development rose and the cost of constructing condominiums remains high, but the system for supporting the acquisition of a house will be continued and the employment condition is improving. The company expects that the contract rate for urban condominiums will remain healthy. Due to the augmentation of the costs for acquiring land and building condominiums, gross profit rate is forecasted to drop this term, too; the cost of sales promotion, including advertisement and model condominiums, will augment; and the company plans to hire more employees, as its business scale will expand. Accordingly, SG&A is estimated to augment about 30%, but it will be offset by sales growth, and operating income is projected to rise 10.0% year on year to 15,466 million yen. The company carried out 4-for-1 share split on Oct. 1, 2016. Its term-end dividend is to be 8.75 yen/share, or 35 yen/share when the share split is not taken into account. When an interim dividend of 35 yen/share is added, the annual dividend will be 70 yen/share, up 10 yen/share from the previous term. Payout ratio is projected to be 10.0%.  Since the sales of single-room condominiums are healthy, the progress rate is higher than usual. The reason the progress rate of sale of buildings exceeds 100% is that the noncurrent assets owned by the company were transferred to real estate for sale in the first quarter and sold in the second quarter.  |

| Future Growth Strategy |

|

(1) Family condominium business

The progress of sale in major projects is as follows.

◎ Pressance Legend Sakaisuji-honmachi Tower

This is a project to build an earthquake-resistant residential skyscraper, the first of its kind in Osaka, which is 30 stories tall with 337 units. The size of each unit is planned to range from a 40 m2 compact type to an over 130 m2 family type. This tower condominium is also planned to have various shared facilities such as a party room, sky lounge and fitness room.The company started selling them in Jan. 2016, and 229 units (68%) were sold by the end of Sep. 2016. Sales activities are progressing healthily before they are handed over to buyers in late Jan. 2018. In the third phase, the company plans to start selling condominiums in Jan. 2017.  ◎ Pressance Legend Lake Biwa

The company will construct a family condominium building with a total of 486 units beside the Lake Biwa in Shiga Prefecture. This is the largest condominium project around the Lake Biwa, and all of the units will have a lake view. It has easy access to Kyoto City as well as Osaka, and is near to a large shopping center, etc. to enrich the lifestyles of residents. The company started selling condominiums in Aug. 2016, and sold 168 prioritized units (35%) in two months till the end of Sep. 2016. Sales activities began favorably before the units are handed over to buyers in early May 2018. In the first phase, the company plans to start selling them in Jan. 2017.  (2) Area strategy - foray into new areas

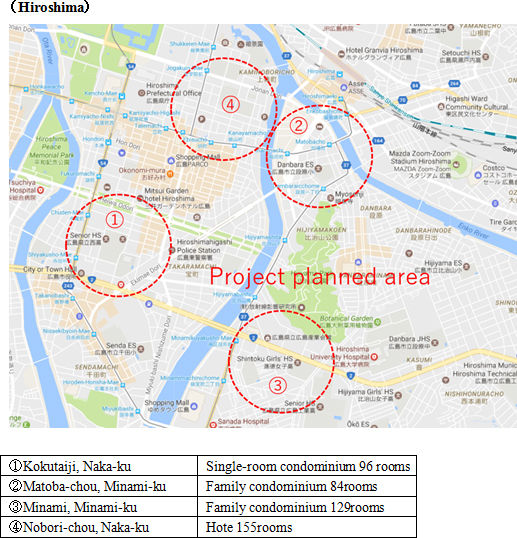

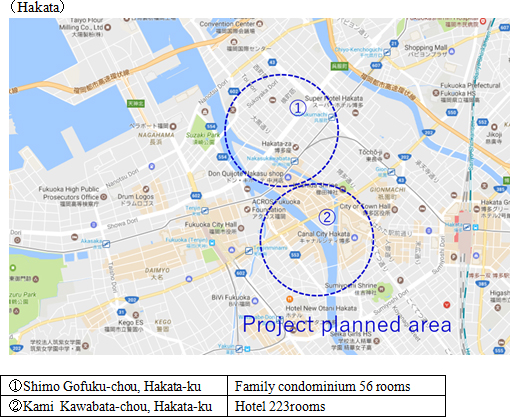

The company decided to make inroads into "Hiroshima" and "Hakata" as new target areas of its business, and is proceeding with some projects. Both areas have large populations, and enterprises, schools, commercial facilities, etc. are concentrated there. Accordingly, promising condominium markets exist there. These areas are also well-known as sightseeing spots, and visitors from foreign countries are expected to increase. Therefore, the company is operating hotel business, too. Like the business operation in the Tokai and Chukyo regions, the company plans to supply products suited for each region, including single-room, family, and combined condominiums, hotels, and single-family houses, and expand its market share steadily based on its community-based business.   (3) M & A Strategy

In Nov. 2016, the company reorganized Sanritsu Precon Co., Ltd., which has supplied a total of 172 condominium buildings and 4,026 units mainly in Okazaki City, Aichi Prefecture, into a 100% subsidiary.Sanritsu Precon Co., Ltd. was founded in 1976. It keeps high price competitiveness based on its integrated system for procuring land for condominiums, planning, designing, constructing, selling, and managing condominiums. Its presence is strong in the Higashimikawa region (including Toyohashi, Toyokawa, and Gamagori; about 760,000 people) and Hamamatsu (about 800,000 people) where there are few condominium developers and populations are large. Pressance Corporation believes that the business area of Sanritsu Precon will help expand the condominium business throughout the Tokai region and improve brand power further. It is expected that the information on land for condominiums will be shared and Sanritsu Precon will construct condominiums of Pressance Corporation at lower cost, producing some synergetic effects. (4) Operation of Hotel business

The company is developing the 11 hotels tabulated below.While considering the following three plans, the company will accumulate its track record continuously, and proceed with the hotel business in a multifaceted manner, while considering the sale to REIT and funds.   (5) Overseas business

In Sep. 2016, the company founded the new company "Prosehre Co., Ltd.," which aims to finance the real estate development projects, etc. conducted by competent local business partners around ASEAN countries, through the joint capital injection with Sanei Architecture Planning Co., Ltd. (1st section of TSE, 3228). Prosehre Co., Ltd. established a joint venture "Tien Phat Tan Thuan Corporation" with Tien Phat, which belongs to the corporate group of a leading Vietnamese private comprehensive construction company. It will join the project for developing condominiums organized by Ho Chi Minh City. As the Vietnamese economy has grown steadily, its population is now concentrated in urban areas, and it is expected that middle-income citizens will increase. Accordingly, the needs for condominiums in urban areas are growing. As the amended housing act was enforced in Jul. 2015, the regulations on the purchase of real estate by foreign people were eased, and the market for condominiums is expected to grow further. In this environment, the company plans to actively carry out business outside Japan, too. |

| Conclusions |

|

|

| <Reference: regarding corporate governance> |

◎ Corporate governance report

Pressance Corporation submitted the latest corporate governance report on June 23, 2016.

Disclaimer

This report is intended solely for information purposes, and is not intended as a solicitation to invest in the shares of this company. The information and opinions contained within this report are based on data made publicly available by the Company, and comes from sources that we judge to be reliable. However, we cannot guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness or validity of said information and or opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration.Copyright(C) 2017, Investment Bridge Co., Ltd. All Rights Reserved. |