Bridge Report:(3299)MUGEN ESTATE the fiscal year ended December 2020

![]()

Shinichi Fujita, President | MUGEN ESTATE Co., Ltd.(3299) |

|

Company Information

Market | TSE 1st Section |

Industry | Real Estate |

President | Shinichi Fujita |

HQ Address | 16th floor, Otemachi Financial City South Tower, 1-9-7 Otemachi, Chiyoda-ku, Tokyo |

Year-end | December |

Homepage |

Stock Information

Share Price | Shares Outstanding | Total market cap | ROE Act. | Trading Unit | |

¥486 | 24,361,000 shares | ¥11,839 million | 2.6% | 100 shares | |

DPS Est. | Dividend yield Est. | EPS Est. | PER Est. | BPS Act. | DPS Est. |

¥10.00 | 2.1% | ¥27.17 | 17.9x | ¥939.11 | 0.5x |

*Stock price as of close on March 8 2021. Numbers are taken from the earnings announcement documents of the fiscal year ended December 2020.

Earnings Trend

Fiscal Year | Sales | Operating Profit | Ordinary Profit | Net Profit | EPS | DPS |

December 2017 (Act.) | 63,568 | 7,122 | 6,478 | 4,276 | 175.61 | 25.00 |

December 2018 (Act.) | 53,931 | 5,985 | 5,237 | 3,356 | 137.80 | 30.00 |

December 2019 (Act.) | 39,677 | 3,157 | 2,493 | 1,688 | 69.38 | 30.00 |

December 2020 (Act) | 34,858 | 2,465 | 1,785 | 599 | 24.98 | 10.00 |

December 2021 (Est.) | 35,412 | 1,916 | 1,315 | 651 | 27.17 | 10.00 |

*Unit: million yen, yen. Forecasts are those of the Company. The definition for net profit is net profit attributable to parent company shareholders. The same applies below.

We present this Bridge Report reviewing the fiscal year ended December 2020 earnings results of MUGEN ESTATE Co., Ltd.

Table of Contents

Key points

1. Company Overview

2. Fiscal Year ended December 2020 Earnings Results

3. Fiscal Year ending December 2021 Earnings Forecasts

4. Three-year Mid-term Management Plan

5. Conclusions

<Reference:Regarding Corporate Governance>

Key Points

- Sales for FY 12/20 were 34,858 million yen, down 12.1% year on year, and operating profit was 2,465 million yen, down 21.9% year on year. The number of units sold of both real estate for investment and real estate for residence declined. Although sales of real estate for investment are gradually recovering, they were not able to make up for the decline in sales in the second and third quarters, which were affected by the spread of COVID-19. However, sales exceeded the earnings forecasts, which considered the conditions up to the third quarter. Net profit declined 64.5% year on year to 599 million yen. After careful consideration of the recoverability of deferred tax assets, part of the deferred tax assets was reversed, and the amount of corporate tax adjustment was recorded at 535 million yen.

- Sales for FY 12/21 are expected to increase 1.6% year on year to 35,412 million yen, and operating profit is projected to decrease 22.3% year on year to 1,916 million yen, resulting in a slight rise in sales and a decline in profit. Although there is uncertainty due to the impact of COVID-19, the demand recovery, which started in the second half of the previous term, is forecasted to continue this term. Sales of real estate for investment will remain at the same level as the previous term, and sales of real estate for residence are planned to be slightly conservative due to the intensity of the competitive environment. Gross profit margin is estimated to decrease 0.5 points from the previous term due to the conservative plan for the gross profit margin of the purchase and resale business. Also, due to the impact of the partial amendment to the Consumption Tax Act, taxes and dues will increase. Thus, operating profit margin is estimated to decrease 1.7 points. The dividend is to be 10.00 yen/share, unchanged from the previous term. The expected payout ratio is 36.8%.

- The recovery in the fourth quarter was much higher than expected at the end of the third quarter for the sales of both real estate for investment and real estate for residence. It is projected that demand recovery, which started at the end of the second half of the previous term, will continue in this term, too. However, it is difficult to anticipate the recovery of the demand from overseas investors, and the movement of investors seems to be slowing down, so a rapid recovery is challenging. If we simply divide the forecasted sales of 35.4 billion yen for this term by four, it will be about 8.8 billion yen in each quarter. For the time being, we would like to confirm whether sales will reach that level after the first quarter (January-March).

- A demand from the popularization of remote working is emerging, and this is a tailwind for MUGEN ESTATE, which specializes in areas around the city center. Nevertheless, recovery of real estate for investment is essential in the current business structure. We would like to see how the various initiatives, such as converting rental condominiums to condominiums for sale, will contribute to profits. We are also looking forward to the progress of development projects which entail the construction of four buildings.

1. Company Overview

MUGEN ESTATE is a pioneer in the resale business of used real estate, where used condominiums and other properties are purchased and then their exteriors and interiors are refurbished as a means of raising their value prior to resale. A characteristic of the Company is to have a single employee in charge of the entire business process including purchase, refurbishment, and sale. MUGEN ESTATE also boasts of a unique position within the industry, based upon its wide range of product offers that accurately match the needs of its customers.

1-1 Corporate History

Susumu Fujita, currently the Chairman of MUGEN ESTATE, founded the Company in 1990 for the acquisition of used condominiums to be refurbished for resale to first time purchasers. This marked the start of the used condominium refurbishment business.

Amidst the expansion of the used condominium market, MUGEN ESTATE has been able to carry on without outside capital by cultivating staff on its own to achieve steady growth. The subsidiary FUJI HOME Co., Ltd. was established in 1997 to provide real estate brokerage. The Company has been able to overcome various difficulties including the Lehman Shock and the Great East Japan Earthquake, and listed its shares on the Mothers Market of the Tokyo Stock Exchange in June 2014, and on the first section of the Tokyo Stock Exchange in February 2016.

Since its listing, the company has been striving to grow further with the used condominium refurbishment business as its core business, and planning to diversify and expand its business domain through acquisition of the permission of the real estate specified joint enterprise business, establishment of a funding firm, etc.

1-2 Management Philosophy

The corporate philosophy is reflected in its name “MUGEN” (“Dream comes true”; Japanese word) and calls for “the pursuit of ideals, realization of dreams.” MUGEN ESTATE’s goal is to help customers realize their own dreams by owning a house of their own, while also striving to realize dream through ongoing growth of the Company and of its employees.

VISION | Helping create a society that will inspire dreams through the real estate business |

MISSION | Helping customers make their dreams come true and growing with customer. |

<Corporate Philosophy>

We will help society prosperity and will continue to grow |

We will ensure compliance in our management |

We will strive to enhance stakeholder satisfaction |

<Code of Conduct>

1.Take benefits for sellers, buyers, and society into consideration at the same time |

2.Emphasize the value of “MOTTAINAI” |

3.Value a sense of gratitude |

4.Continue to consider reforms and focus on taking on new challenge |

5.Maintain trust |

6.Act immediately, be sure to act, and follow through until the end |

7.Emphasize compliance |

1-3 Market Environment

◎ Expanding Market for Used and Renovated Residential Properties

According to the Ministry of Land, Infrastructure, Transport, and Tourism’s "Vitalization of the Existing Housing Market" announced in May 2020, the distribution share of existing housing in Japan's total housing distribution volume was 14.5% in 2018, which has declined by about 3% in the last ten years and is at an extremely low level compared to the United States (81.0%), the United Kingdom (85.9%), and France (69.8%).

With the declining birthrate and aging population, the number of housing stocks exceeds the number of households, and the number of vacant houses is increasing. Due to these circumstances, the government considered the need to improve the environment of the existing housing distribution and renovation market, and the "Basic Plan for Housing (National Plan)" was decided by the Cabinet in March 2016.

(Currently under review to incorporate measures to respond to the apparent changes in the socio-economic situation and the housing environment)

* Points of Basic Plan for Housing (March 2016)

The following three points are the main factors of the plan, which "presents a new direction of housing policy that directly addresses the declining birthrate, aging population, and the declining population."

(1) Achieve a residential life in which young and child-rearing households and the elderly can live with peace of their mind

(2) Promote distribution of existing houses and utilization of vacant houses, and accelerate conversion to a market that utilizes housing stocks

(3) Revitalize the housing industry that supports housing and as a leader to achieve a strong economy

In "(2) Promote distribution of existing houses and utilization of vacant houses, and accelerate conversion to a market that utilizes housing stocks," the government aims to create a new flow in which existing houses are distributed and inherited as assets by the next generation through improving the quality of existing houses and attract more people who want to live in and buy them.

Specifically, the government will promote the rebuilding and refurbishment of condominiums that are deteriorating and becoming vacant and will increase the number of condominium rebuilding projects (cumulative from 1975) from approximately 250 in 2014 to about 500 in 2025.

Furthermore, the government will limit the increase in the number of vacant houses by about 1 million units by promoting the distribution of existing houses.

Additionally, in "(3) Revitalize the housing industry that supports housing and as a leader to achieve a strong economy," the government is promoting the supply of wooden houses and improving the production system (securing and training workers and developing technologies). Also, by revitalizing the housing stock business, the government aims to grow the scale of the existing housing distribution market from 4 trillion yen in 2013 to 8 trillion yen in 2035, and the renovation market from 7 trillion yen to 12 trillion yen, totaling 20 trillion yen.

◎Attractive Real Estate Market in Tokyo Metropolitan Region

Huge Latent Market:

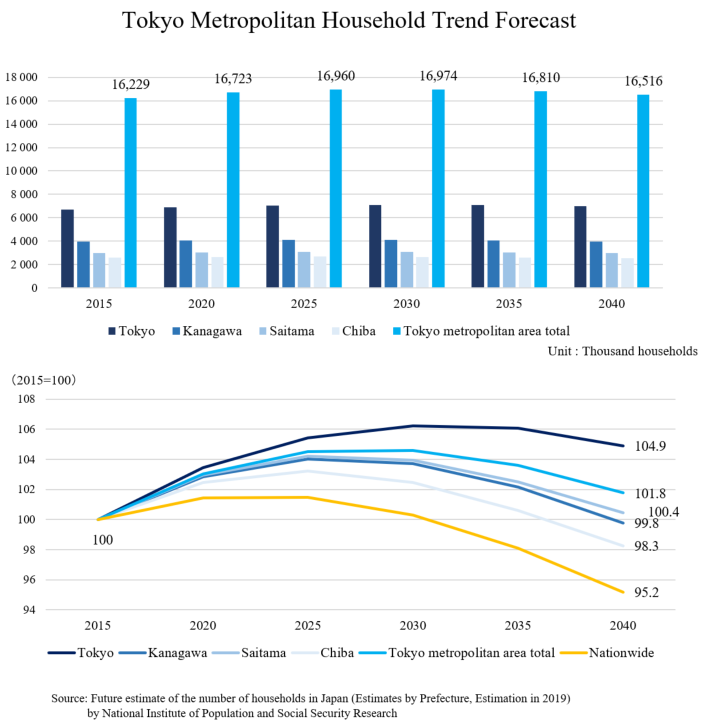

According to the “2018 House and Land Statistics Survey” published by the Ministry of Internal Affairs and Communications, the number of “non-wooden residential properties” in the Tokyo and greater metropolitan region (Tokyo, Kanagawa, Saitama and Chiba) stood at 8.24 million units. Given that the Company purchased 332 units of properties for investments and for residence during fiscal year December 2020, the latent market potential for MUGEN ESTATE remains huge.

Household Numbers in The Tokyo Metropolitan Region basically on The Rise:

Moreover, the population will inevitably decrease in Japan as a result of the declining birthrate. According to estimates by the National Institute of Population and Social Security Research in 2019, by 2040, the number of households in Japan will decrease, while the number of households in the Tokyo metropolitan area is expected to increase in the future due to the ongoing concentration of population in Tokyo. However, it is unclear at this point how the spread of COVID-19 will affect Japanese people's lifestyle consciousness and behavior in the future.

◎ Competitiveness of highly reliable suppliers is relatively on rise.

While the real estate market has been booming for the past few years because of robust demand, people’s willingness to invest and purchase is expected to fall with rising land prices and recent various distortions coming to light, such as the violation of the Building Standards Act by major apartment construction contractors and leasing companies, illegal lending of apartment loans by regional banks, inappropriate lending by new real estate firms through falsification of savings records, etc.

The market may not be as booming as before, but there is still a strong need for good-quality properties for actual acquisition and investment as interest rates remained at a low level, and the previously mentioned scandals have made highly reliable suppliers relatively more competitive, as a result of which they have entered a stage where they are being selected by investors and buyers.

<Peer Company Comparison>

|

| Sales | YY Change | Operating Profit | YY Change | Profit margin | Total market cap | PER | PBR | ROE |

2975 | Star Mica Holdings Co., Ltd. | 40,013 | +1.1% | 2,982 | -9.1% | 7.5% | 22,385 | 14.2 | 1.1 | 9.1% |

3288 | Open House Co., Ltd. | 767,600 | +33.3% | 83,800 | +34.9% | 10.9% | 538,598 | 9.0 | 2.3 | 32.0% |

3294 | E’Grand Co., Ltd. | 20,500 | +0.2% | 1,350 | -7.0% | 6.6% | 5,964 | 7.1 | 0.8 | 12.3% |

3299 | MUGEN ESTATE Co., Ltd. | 35,412 | +1.6% | 1,916 | -22.3% | 5.4% | 11,839 | 17.9 | 0.5 | 2.6% |

8923 | Tosei Corp. | 69,535 | +8.8% | 8,707 | +35.5% | 12.5% | 51,167 | 9.5 | 0.8 | 6.1% |

8934 | Sun Frontier Fudosan Co., Ltd. | 70,000 | -4.4% | 6,930 | -58.2% | 9.9% | 49,974 | 12.2 | 0.8 | 16.8% |

8940 | INTELLEX Co., Ltd. | - | - | - | - | - | 5,341 | - | 0.5 | 4.9% |

* Unit: Million yen, Times. Sales and operating profit are forecasts taken from each of the respective companies. ROE are actual data taken from the most recently ended fiscal year. Market capitalization, PBR and PER are based upon the closing share price on March 8, 2021.

INTELLEX Co., Ltd. have not yet forecasted the performance in the current term.

1-4 Business Description

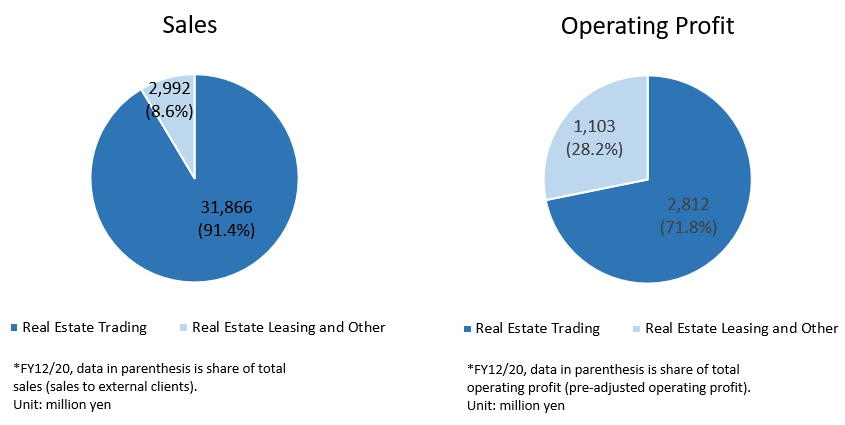

MUGEN ESTATE’s business is divided between the two segments of “real estate trading” and “real estate leasing and other” businesses, with the real estate trading segment business accounting for about 91% of total sales during fiscal year December 2020. The Company plans to promote efforts to expand its earnings deriving from the real estate leasing and other business segment.

<Real Estate Trading Business>

The real estate trading business segment includes the three services of real estate resale, interior and exterior refurbishment and construction, and real estate distribution with the main service being the resale of real estate.

◎ Purchases and Resale Business

The Company purchases used condominiums for sectional ownership, real estate for investment, and detached housing properties in the Tokyo Metropolitan Areas, including Tokyo, Kanagawa, Saitama and Chiba. To increase their value, the Company then has the subsidiary FUJI HOME, and some others, refurbish them in accordance with their age, space, layout, location and management condition.

Main Value Addition Activities

*Refurbishment of exteriors and interiors

*Improve management conditions of buildings

*Restoration of wear and tear caused by age

*Leasing of vacant rooms

*Collection of unpaid rent

After having increased real estate values as “real estate for resale” through any of the activities, the Company then sells to first time purchasers, individual investors, and small to medium sized companies.

Source : MUGEN ESTATE

The purchase and sale of real estate is performed by real estate brokers, but some of the transactions are undertaken by FUJI HOME in order to obtain a feel for the diversifying needs of customers and market trends.

In order to respond quickly and accurately to the needs of customers, MUGEN ESTATE maintains a diverse lineup of condominiums for sectional ownership, real estate for investment (rental condominiums, apartments and office buildings) and detached housing. Properties are divided into two categories of real estate for investment and real estate for residence. Real estate for investment is properties purchased by investors for the purpose of deriving returns, which include whole rental condominium complexes, offices and apartment buildings, as well as condominiums for sectional ownership and others. The average price for real estate for investment is between ¥0.1 to ¥0.2 billion.

The residential-type properties are those which purchased by consumers for the purpose of living in them, which include detached housing in addition to its main item of condominiums for sectional ownership. These properties are bought primarily by first time purchasers and their prices are mostly in the ¥0.02 to ¥0.03 billion range. MUGEN ESTATE sold over the course of fiscal year December 2020, 184 units of real estate for investment and 148 units for residence, 332 in total.

MUGEN ESTATE boasts of a unique business process where one sales person is responsible for the acquisition, refurbishment and sale of real estate. Furthermore, the Company’s sales staff visit real estate brokers such as Mitsui No Rehouse, Nomura Real Estate Urban Net Co., Ltd., Sumitomo Real Estate Sales Co., Ltd., Tokyu Livable Co., Ltd. and others in the Tokyo metropolitan region to obtain information about real estate for sale by both individuals and corporations. By visiting these real estate companies, sales staff are able to obtain real estate information on superior properties that have yet to be released through public channels.

After obtaining information on real estate for sale, analysis is conducted regarding the properties’ potential for increased value and resale at higher prices after renovation and refurbishment. If MUGEN ESTATE finds that there is that potential, then they acquire the properties and then outsource the task of refurbishment to a subcontracting company under the supervision of its subsidiary, FUJI HOME.

An analysis of the potential customer base specific to the location of the property is conducted by sales staff to determine the price and other needs of the customers, and in some instances a three-bedroom used condominium maybe converted into a two-bedroom condominium and other refurbishments are undertaken to raise the attractiveness of the property (Refurbishments are conducted with a view to the end sale price and ensuring profitability on the sale).

Sales staff responsible for purchasing the real estate adhere to standards established by the Company. These internal standards are comprised of various factors including specific balance between acquisition price and management fees, proximity to train stations and no properties requiring bus rides, and other specific information known internally as the “12 purchase conditions,” which have been developed over the history of the Company’s operations and are effective as a context for the conduct of its business. At the same time, this standard developed on MUGEN ESTATE’s own unique knowhow also serves to support less experienced sales staff in making the correct analysis and purchase of real estate. In addition, sales staff consult with their managers and superiors to obtain appropriate advice on how to carry on their business process. And while high commission involved in sales activities for condominiums tends to lead sales staff to act discretionally in general in the industry, MUGEN ESTATE maintains a culture of team work, where sales staff consult each other for advice and superiors lead their subordinates in the right direction on the business process. Also, the company pays commission for sales representatives based on profit gained at the time of resale rather than the resale price itself, so the risk of being stuck with unsold merchandise is relatively low when compared with other companies.

◎ Interior and Exterior Refurbishment Business

The subsidiary FUJI HOME conducts refurbishment of both the interiors and exteriors of purchased used real estate. FUJI HOME boasts of bountiful knowhow in refurbishment services based upon over 500 refurbishment projects conducted through accurate surveys and analysis of real estate properties by its highly skilled staff, including first class registered architects. Orders from MUGEN ESTATE currently account for over 90% of FUJI HOME’s total orders, but it is endeavoring to expand orders from external clients.

◎ Brokerage Business

Information about real estate purchased for resale by MUGEN ESTATE is handled by FUJI HOME. In addition to the company website, they have also put it up on other portal sites for used real estate information operated by other companies. Furthermore, they also provide mediation services for MUGEN ESTATE in their acquisition of real estate properties. Also, synergies with the Company’s real estate resale business can be realized by gathering accurate information about the needs of used real estate purchasers.

In addition to the above-mentioned business, the company initiated the development business and the real estate specified joint enterprise business with the aim of evolving into a company group which can continue to grow further.

<Real Estate Leasing and Other Business>

Optimization of the sales function of the real estate resale business is being pursued.

◎ Leasing Business

Real estate purchased as investment-type properties and as fixed asset properties are leased to end users. In principle, real estate is purchased with the objective of sales. However, renting and leasing is used as a means of deriving profit until the properties are sold.

◎ Property Management Business

Management services for leased real estate that have been acquired as investment-type properties and fixed asset properties are conducted. Improvement in the management of structures, restoration of wear and tear caused by age, leasing of vacant rooms, collection of outstanding rent, and other measures are implemented as part of a strategy of increasing the value of properties and improving the return on investment-type properties. In the real estate trading resale business, depending on the intentions of the buyer of real estate for investment, there are also cases in which rental management work continues after a sale is made.

In addition, the company is engaged in a development business where it develops its own properties and a real estate specific joint enterprise business that aims to make real estate investment approachable to a wider range of individual investors through small-lot real estate investment.

1-5 Characteristics and strengths

①Management Leveraging Synergies

In addition to the above-mentioned real estate resale service, MUGEN ESTATE also performs real estate rental, real estate refurbishment, real estate distribution, and real estate management services. The knowhow developed in its various businesses based on the results of the many years of operation is leverage to be able to respond flexibly to changes in the market and derive various synergies between its various businesses.

②Diverse Product Lineup and Unique Positioning

With regards to the core real estate resale business, MUGEN ESTATE boasts of a strong information gathering capability based upon its network in the used real estate market in the Tokyo and the surrounding metropolitan region, which has enabled the Company to develop a diverse lineup including condominiums for sectional ownership, real estate for investment (whole rental condominium complexes, offices and apartment buildings) and detached housing, and to respond quickly and accurately to customers’ needs. In addition, MUGEN ESTATE has developed a strong reputation amongst real estate brokers for its ability to respond to all of the information gathered from them. Returning to those real estate brokers upon completion of rendering resale properties creates a benevolent cycle where the Company gains preferential treatment in the gathering of information on superior real estate.

MUGEN ESTATE has carved out a unique position within the real estate refurbishment industry through the creation of a diverse product lineup.

③Strength of High Levels of Professional Skill

The information gathering, investment decision making, property management, technological response and other capabilities are all part of MUGEN ESTATE’s high levels of professional skills and allow the Company to provide superior properties to the market.

Additionally, the stable constructing and management system, the business know-how that has been developed over many years and the strong financing ability based on contracts with about fifty financial institutions are MUGEN’s strengths.

2. Fiscal Year Ended December 2020 Earnings Results

(1)Business Results

| FY 12/19 | Ratio to s Sales | FY 12/20 | Ratio to Sales | YoY | Compared to initial forecasts | Compared to revised forecasts |

Sales | 39,677 | 100.0% | 34,858 | 100.0% | -12.1% | -22.8% | +13.7% |

Gross Profit | 6,475 | 16.3% | 5,864 | 16.8% | -9.4% | -20.7% | +11.9% |

SG&A | 3,317 | 8.4% | 3,398 | 9.8% | +2.5% | -18.6% | +1.3% |

Operating Profit | 3,157 | 8.0% | 2,465 | 7.1% | -21.9% | -23.4% | +30.5% |

Ordinary Profit | 2,493 | 6.3% | 1,785 | 5.1% | -28.4% | -26.9% | +47.4% |

Net Profit | 1,688 | 4.3% | 599 | 1.7% | -64.5% | -62.4% | +213.6% |

* Unit: Million yen. Comparison to the initial forecast and revised forecast are the ratios of actual results to the forecasts announced in February 2020 and November 2020, respectively.

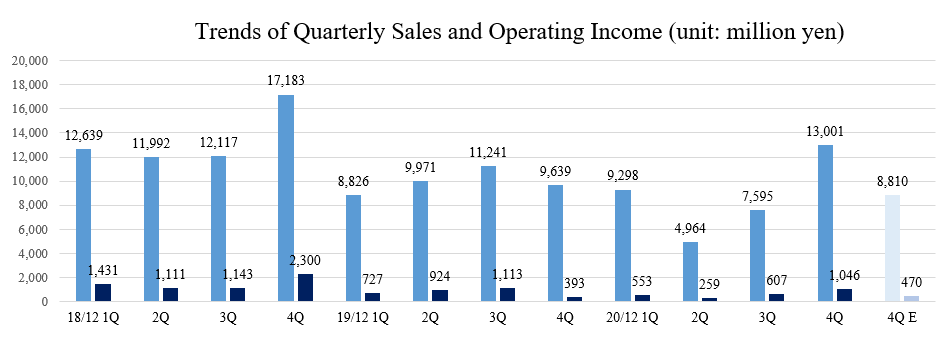

Decrease in sales and profit but a recovery in the fourth quarter. Exceeded revised estimates.

Sales for FY 12/20 were 34,858 million yen, down 12.1% year on year, and operating profit was 2,465 million yen, down 21.9% year on year.

The number of units sold of both real estate for investment and real estate for residence declined. Although sales of real estate for investment are gradually recovering, they were not able to make up for the decline in sales in the second and third quarters, which were affected by the spread of COVID-19. However, sales exceeded the earnings forecasts, which considered the conditions up to the third quarter.

Net profit declined 64.5% year on year to 599 million yen. After careful consideration of the recoverability of deferred tax assets, part of the deferred tax assets was reversed, and the amount of corporate tax adjustment was recorded at 535 million yen.

Sales and profits declined in the second quarter (April-June) and the third quarter (July-September), but in the fourth quarter (October-December), sales and profits increased and exceeded the forecasts (the cumulative third quarter was excluded from the revised forecasts announced in November). Sales exceeded 10 billion yen for the first time in five quarters.

(2)Segment Earnings Trends

| FY 12/19 | Ratio to Sales | FY 12/20 | Ratio to Sales | YoY |

Sales |

|

|

|

|

|

Real Estate Trading | 36,401 | 91.7% | 31,866 | 91.4% | -12.5% |

Real Estate Leasing and Other | 3,275 | 8.3% | 2,992 | 8.6% | -8.6% |

Total | 39,677 | 100.0% | 34,858 | 100.0% | -12.1% |

Segment Profit |

|

|

|

|

|

Real Estate Trading | 3,296 | 9.1% | 2,812 | 8.8% | -14.7% |

Real Estate Leasing and Other | 1,183 | 36.1% | 1,103 | 36.9% | -6.8% |

Adjustments | -1,322 | - | -1,450 | - | - |

Total | 3,157 | 8.0% | 2,465 | 7.1% | -21.9% |

* Unit: Million yen. Sales represent sales to external clients. Operating profit ratio represents sales operating profit margin.

Real estate rental revenues in the leasing and other business declined 9.5% from last term to 2,910 million yen.

◎Real Estate Trading Business Conditions

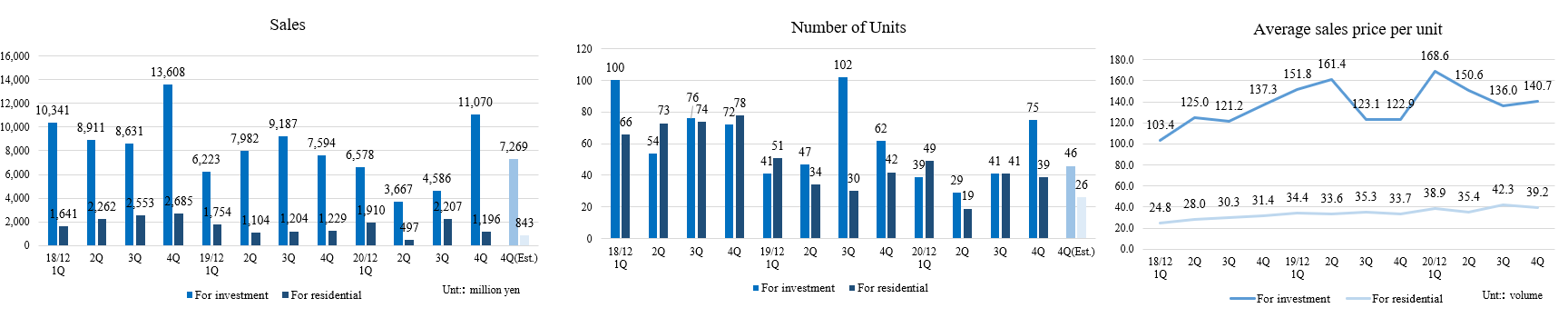

①Sales Value, Volume

| FY12/19 | FY12/20 | YoY |

Sales | 36,277 | 31,712 | -12.6% |

Investment-type | 30,986 | 25,901 | -16.4% |

Residential-type | 5,291 | 5,810 | +9.8% |

Number of Units | 409 | 332 | -18.8% |

Investment-type | 252 | 184 | -27.0% |

Residential-type | 157 | 148 | -5.7% |

Average Sales Price | 88.6 | 95.5 | +7.7% |

Investment-type | 122.9 | 140.7 | +14.5% |

Residential-type | 33.7 | 39.2 | +16.5% |

* Unit: Million yen, units

* Although the number of units sold of both real estate for investment and real estate for residence decreased, the average unit sales price of real estate for residence was high due to favorable sales from the third quarter onward and sales of high-priced properties such as properties in central Tokyo leading to an increase in sales.

* The average unit sales price of apartment buildings was 247.5 million yen, down 0.4% year on year. However, it has recovered in the fourth quarter.

* Sales volume of real estate for investment exceeding 300 million yen decreased by two units from the previous term to 27 units, and two units exceeding one billion yen were sold.

* By area, the number of units sold of real estate for investment declined except in Kanagawa prefecture, but the average unit price increased except in Saitama prefecture. As for real estate for residence, the number of units sold decreased in Tokyo and Chiba prefectures, but the average unit price rose in all areas.

* Sales to overseas investors declined 51.4% year on year due to the impact of strict restrictions on the entry to Japan. The number of units sold decreased 41.0% year on year. The average unit sales price also fell 17.7% year on year due to a decline in sales of high-priced investment properties.

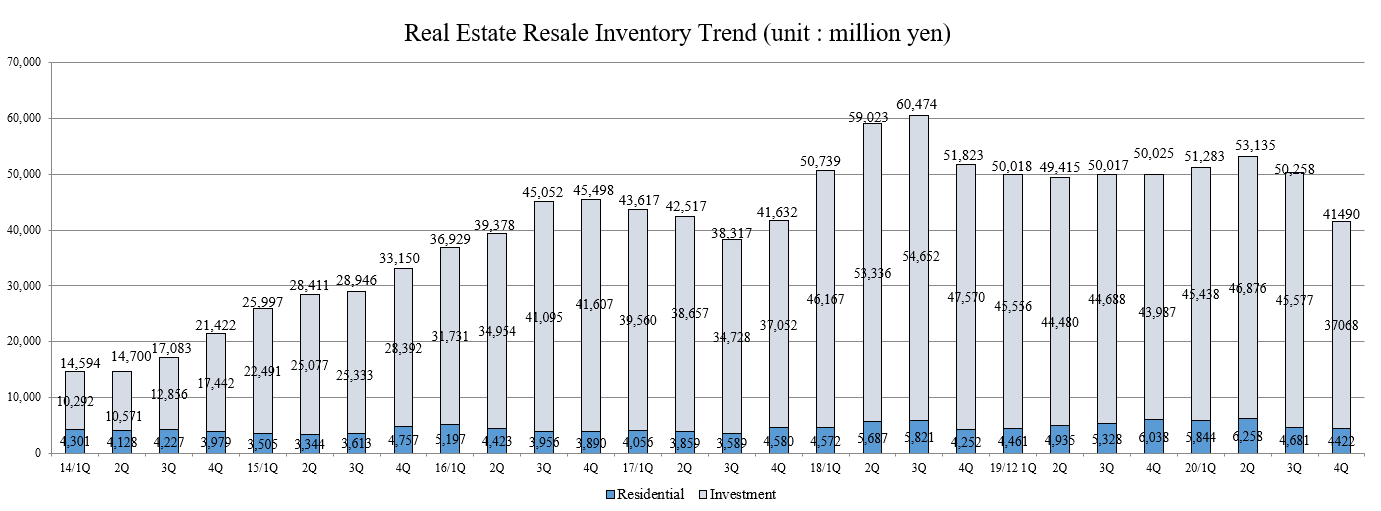

②Real Estate for Sale Inventory Conditions

Inventory of real estate for sale decreased 17.1% from the end of the previous term because the company was working on enhancing its financial position through measures such as increasing cash on hand. The inventory of real estate for investment declined 15.7% from the end of the previous term, and the inventory of real estate for residence decreased 26.8% from the end of the previous term.

The project period was 245 days in FY 12/20. It was prolonged by 28 days than the end of FY 12/19 and by 51 days than the end of the third quarter of FY 12/20.

(3)Financial standing and cash flows

◎Balance Sheet

| End of December 2019 | End of December 2020 | Increase/ Decrease |

| End of December 2019 | End of December 2020 | Increase/ Decrease |

Current Assets | 64,367 | 57,937 | -6,430 | Current liabilities | 12,185 | 11,137 | -1,048 |

Cash | 13,708 | 16,065 | +2,357 | Payables | 467 | 216 | -251 |

Real estate for sale | 49,887 | 41,337 | -8,549 | ST Interest-Bearing Liabilities | 10,340 | 9,102 | -1,238 |

Real estate for sale in process | 147 | 283 | +136 | Noncurrent liabilities | 33,486 | 28,744 | -4,742 |

Noncurrent Assets | 4,096 | 4,504 | +408 | LT Interest-Bearing Liabilities | 32,618 | 28,020 | -4,598 |

Tangible Assets | 3,068 | 3,838 | +769 | Total Liabilities | 45,671 | 39,882 | -5,789 |

Intangible Assets | 83 | 83 | 0 | Net Assets | 22,840 | 22,605 | -235 |

Investment, Others | 944 | 583 | -361 | Retained earnings | 17,914 | 17,790 | -124 |

Total assets | 68,512 | 62,487 | -6,025 | Total liabilities and net assets | 68,512 | 62,487 | -6,025 |

* Unit: Million yen

Sales of real estate for sale decreased 8.5 billion yen from the end of the previous term. Meanwhile, cash increased 2.3 billion yen from the end of the previous term, and total assets declined 6 billion yen from the end of the previous term to 62.4 billion yen. Total liabilities decreased 5.7 billion yen from the end of the previous term to 39.8 billion yen due to the repayment of interest-bearing liabilities for inventory reduction leading to their decline by 5.8 billion yen from the end of the previous term. Net assets dropped 200 million yen from the end of the previous term to 22.6 billion yen due to a decrease in retained earnings.

As a result, equity ratio rose 2.8 points from 33.2% at the end of the previous term to 36.0%.

Dependency on interest-bearing debts increased 3.3 points from the end of the previous term to 59.4%, and the net debt-to-equity ratio decreased 0.35 to 0.94 from the end of the previous term.

Inventory turnover rose 0.05 points from the end of the term to 0.84.

◎Cash Flow

| FY12/19 | FY12/20 | Increase/Decrease |

Operating Cash Flow | 3,276 | 10,981 | +7,705 |

Investing Cash Flow | -872 | -1,944 | -1,072 |

Free Cash Flow | 2,404 | 9,037 | +6,633 |

Financing Cash Flow | 712 | -6,656 | -7,368 |

Cash and Equivalents at Term End | 12,268 | 14,649 | +2,381 |

* Unit: Million yen

The surpluses of operating CF and free CF grew due to inventory reduction. The deficit of investing CF augmented due to the expansion of the acquisition of tangible assets. The financing CF turned negative due to the reduction of interest-bearing liabilities.

The cash position has improved.

3. Fiscal Year ending December 2021 Earnings Forecasts

(1) Impact of COVID-19

The company considers the impact of COVID-19 on the business environment in this term will be as follows.

(Impact on real estate for investment)

Although the state of emergency has been declared again, it is predicted that the recovery of domestic investors' attitude towards investing in real estate, which started at the end of last year, will continue. It should be noted that investors' movement is slowing down a little at the moment.

As for overseas investors, the company does not expect any improvement in investment demand due to continued strict restrictions on the entry to Japan. However, there still is a demand from overseas investment funds for large properties.

The loss of demand from foreign visitors to Japan and lifestyle changes due to new work styles are changing the demand trend of properties for investment, and the purchasing environment is becoming challenging.

While the demand for investment in properties for commercial purposes and offices is uncertain, the demand is shifting to apartment buildings and condominiums for sectional ownership, so for the time being, the company will focus on residential property purchasing activities.

(Impact on real estate for residence)

Due to lifestyle changes such as the popularization of telework, the demand for residing in areas other than the city center is increasing. Thus, it is predicted that demand for properties in the area around the city center, which is the company's strength, will rise.

Since the competitive environment remains intense, the company will only purchase properties that can secure a gross profit margin. Thus, it forecasts sales more conservatively than in the previous term.

(Impact on renting trends)

Requests for rent reductions and postponements from tenants due to the spread of COVID-19 were limited.

It is necessary to pay close attention to demand trends by location and area. For example, there were decreases in demand in the university areas and in demand by foreigners due to strict restrictions on the entry to Japan. The company also must be cautious about purchasing units in areas where vacancy rates are rising.

(General impact)

The company will use IT to promote non-contact sales activities, such as increasing information on brokerage websites.

As the company has started telework in the wake of COVID-19 crisis, it will review the business flow and improve efficiency while utilizing RPA.

(2) Forecast of financial results and dividends

| FY 12/20 | Ratio to Sales | FY 12/21(Est) | Ratio to Sales | YoY |

Sales | 34,858 | 100.0% | 35,412 | 100.0% | +1.6% |

Gross profit | 5,864 | 16.8% | 5,773 | 16.3% | -1.5% |

SG&A | 3,398 | 9.7% | 3,857 | 10.9% | +13.5% |

Operating Profit | 2,465 | 7.1% | 1,916 | 5.4% | -22.3% |

Ordinary Profit | 1,785 | 5.1% | 1,315 | 3.7% | -26.3% |

Net Profit | 599 | 1.7% | 651 | 1.8% | +8.8% |

* Unit: Million yen

Increase in sales and decline in profit

Sales for FY 12/21 are expected to increase 1.6% year on year to 35,412 million yen, and operating profit is projected to decrease 22.3% year on year to 1,916 million yen, resulting in a slight rise in sales and a decline in profit.

Although there is uncertainty due to the impact of COVID-19, the demand recovery, which started in the second half of the previous term, is forecasted to continue this term.

Sales of real estate for investment will remain at the same level as the previous term, and sales of real estate for residence are planned to be slightly conservative due to the intensity of the competitive environment.

Sales related to development properties and real estate specified joint enterprise business are planned.

As we will continue to focus on inventory turnover in our sales activities this fiscal year, we expect inventory levels to decline, and real estate rental revenues are expected to decrease from the previous fiscal year.

We will expand the acquisition of properties as fixed assets depending on the area and location. The investment plan is 4 billion yen.

In other businesses, we plan to increase construction orders for external customers and the number of units under management.

Gross profit margin is estimated to decrease 0.5 points from the previous term due to the conservative plan for the gross profit margin of the purchase and resale business.

Also, due to the impact of the partial amendment to the Consumption Tax Act, taxes and dues will increase. Thus, operating profit margin is estimated to decrease 1.7 points.

The dividend is to be 10.00 yen/share, unchanged from the previous term. The expected payout ratio is 36.8%.

(3) Real Estate Trading Business Conditions

①Sales Value, Volume

| FY12/20 | FY12/21(Est) | YoY |

Sales | 31,712 | 30,100 | -5.1% |

Investment-type | 25,901 | 25,200 | -2.7% |

Residential-type | 5,810 | 4,900 | -15.7% |

Number of units | 332 | 280 | -15.7% |

Investment-type | 184 | 140 | -23.9% |

Residential-type | 148 | 140 | -5.4% |

Average Sales Price | 95.5 | 107.5 | +12.5% |

Investment-type | 140.7 | 180.0 | +27.9% |

Residential-type | 39.2 | 35.0 | -10.8% |

* Unit: Million yen, units

Real estate for residence, which had an increase in sales in the previous term, is expected to witness declines in both sales volume and average unit price. The average unit price of real estate for investment will increase significantly.

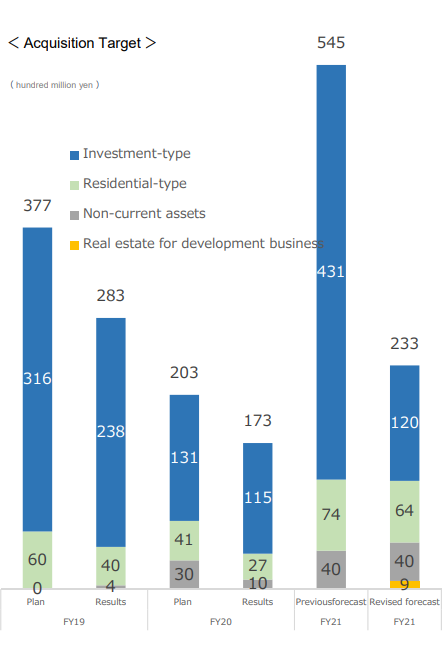

4. Three-year Mid-term Management Plan

The company was proceeding with a three-year medium-term management plan which started from FY 12/19. However, the business environment has changed significantly, including further tightening of the financing environment, the spread of COVID-19, and the amendment of the Consumption Tax Act leading to uncertainty about demand trends for the current term. Thus, the company saw that a significant recovery would be difficult and revised the numerical plan for FY 12/21, the final year of the medium-term management plan.

<Quantitative goal>

| FY 12/18 | FY 12/19 | FY 12/20 | FY 12/21 (Est.) | FY 12/21(Revised Plan) |

Consolidated Sales | 539 | 396 | 348 | 630 | 354 |

Consolidated Ordinary Profit | 52 | 24 | 17 | 55 | 13 |

Consolidated Equity Ratio | 32.9% | 33.2% | 36.0% | Above 30% | |

* Unit:100 Million yen

The company still maintains a capital adequacy ratio of 30% or more as a financial security measure to achieve stable growth over the medium to long term.

(1) Overview

<Management policy>

The company strives to establish a solid management base to ensure continued growth with three business policies, i.e., “Making products that support the business base,” “Building networks that support the revenue base” and “Creating human resources and systems that support the management base.”

<Positioning>

The company considers this mid-term management plan as the first mid-term management plan and views this as the period to restructure its management base into a strong one so that the company can grow further through the implementation of the second and third mid-term management plans, which will be formulated later.

The company aims to establish a solid management base to ensure continued growth, as it is mentioned in its management policy, by reviewing the existing business from zero, carefully learning the obstacles and improving on them.

The whole company strives to achieve the target by fixing a clear deadline.

<Business policy>

The company will carry out its business initiatives following the six business policies given below, under the management policies mentioned above.

Business Policies |

| Business Measures |

(1) Providing products that respond to environmental changes, meet social needs and please customers | ◇ | Providing accumulated Group know-how as products for outside customers. Deeply cultivating a new customer base with the development of real estate-related products that meet current needs. |

(2) Refurbishing properties held | ◇ | Maximizing added value by changing the application (conversion) according to the area and the architectural structure and by implementing large-scale repairs. |

(3) Mastering products and services | ◇ | Improving inventory turnover by accelerating the commercialization of vacant buildings and properties with a high vacancy rate by soon raising the occupancy rate. |

◇ | Providing safe, secure and comfortable properties by checking inspection items in detail after completion. | |

◇ | Developing high value-added properties for foreigners in Japan. | |

(4) Mastering the selling and buying of properties | ◇ | Increasing profitability by reviewing and fully enforcing the profit management of each property. |

◇ | Fully enforcing risk management by strengthening compliance. | |

◇ | Expanding sales channels for foreign investors by holding seminars for them. | |

(5) Responding to diverse work styles (6) Further strengthening Group power | ◇ | Securing and cultivating human resources by promoting diversity; managing human resources by optimizing staff assignments in the Group and implementing stratified trainings; and visualizing work by improving the working environment and reviewing the workflow. |

(2) Concrete Initiatives for the fiscal year 2021

The concrete initiatives following each management policy are as follows.

① Purchases and Resale Business

*Management Policy: Development of products to support the business foundation and network building to support the revenue base.

Source : MUGEN ESTATE

(Main measures)

(1) The company will consider and implement initiatives using IT to enable contactless sales.

In addition to enhancing brokerage websites (increasing the amount of information, browsing of properties using VR, and video streaming), the company will also strengthen its efforts in IT investments.

(2) The company will convert rental condominiums into condominiums for sale.

Based on the current trends of residential condominiums and the marketing situation in the surrounding areas, the company will convert rental condominiums into condominiums for sale.

The company will continue to thoroughly investigate the locations and areas of properties and reinforce its measures.

(3) Since the competitive environment is intense, the company will purchase properties that can secure enough profits.

The company will conduct thorough profit management due to the intense competitive environment for real estate for residence.

Regarding real estate for investment, the company will focus on purchasing residential products.

The purchase plan was revised downward from 54.5 billion yen to 23.3 billion yen.

② Development and Real Estate Specific Enterprise Business

* Management policy: Creating products that support the business foundation and networks that support the earnings base

(Completion and sales of development projects)

The company has planned projects to develop four properties.

It has developed a profitable property (mainly rental condominiums and offices) and plans to sell it in the second half of this term.

It will also focus on purchasing land from next term onward.

(Real estate specific joint enterprise business, first product association composition)

The Yoyogi Project, the first product of the real estate-specific joint enterprise business, formed an association in December 2020 and started operation.

5. Conclusions

The recovery in the fourth quarter was much higher than expected at the end of the third quarter for the sales of both real estate for investment and real estate for residence.

It is projected that demand recovery, which started at the end of the second half of the previous term, will continue in this term, too. However, it is difficult to anticipate the recovery of the demand from overseas investors, and the movement of investors seems to be slowing down, so a rapid recovery is challenging. If we simply divide the forecasted sales of 35.4 billion yen for this term by four, it will be about 8.8 billion yen in each quarter. For the time being, we would like to confirm whether sales will reach that level after the first quarter (January-March).

A demand from the popularization of remote working is emerging, and this is a tailwind for MUGEN ESTATE, which specializes in areas around the city center. Nevertheless, recovery of real estate for investment is essential in the current business structure. We would like to see how the various initiatives, such as converting rental condominiums to condominiums for sale, will contribute to profits.

We are also looking forward to the progress of development projects which entail the construction of four buildings.

<Reference:Regarding Corporate Governance>

◎Organization type and the composition of directors and auditors

Organization type | Company with auditors |

Directors | 7 directors, including 2 outside ones |

Auditors | 3 auditors, including 2 outside ones |

◎Corporate Governance Report

Updated on March 24, 2020

<Basic policy>

Our company, as mentioned in its policy, strives to realize “MUGEN” (make dreams come true and pursue the ideal), which is the root of our management policy and also the origin of the company’s name, and upholds the following three corporate philosophies in order to achieve a sustainable improvement of corporate value.

・We will help society to achieve prosperity and will continue to grow

・We will ensure compliance in our management

・We will strive to enhance stakeholder satisfaction

We believe that securement of transparency and soundness in management and strengthening of the management system to respond to environmental changes promptly and accurately are the most needed measures to realize these corporate philosophies, and consider the establishment of corporate governance as the most important task. Therefore, we promote (1) strengthening of check-and-balance and oversight of the person in charge of execution of work, (2) securement of transparency through information disclosure and (3) establishment of a management system for business execution.

Also, the company's Board of Directors has established "Guidelines for Corporate Governance" (hereinafter referred to as "Company Guidelines") to show an effective governance framework and contribute to its realization.

Please refer to the company's website for the full text of the Company Guidelines.

→https://www.mugen-estate.co.jp/en/ir/management/governance/pdf/Corporate-Governance-Guidelines_20200324.pdf

<Reasons for Non-compliance with the Principles of the Corporate Governance Code (Excerpts)>

Principles | Reasons for not implementing the principles |

[Supplementary Principle 4-2-1 Remuneration of management for sustainable growth] | Remuneration for management consists of fixed remuneration (money) and stock option compensation (stock acquisition rights) granted to executive directors. The Board of Directors has resolved to appoint to the President the specific distribution of fixed remuneration to the seven Directors within the limit of the total remuneration of the Board of Directors which is decided by the General Meeting of Shareholders. The President decides the specific distribution of remuneration to each director, taking into consideration the company's business performance, business content, economic conditions, and the evaluation of each director. Regarding the granting of stock option compensation (stock acquisition rights) to five Executive Directors, the Board of Directors decides the allocation in accordance with internal regulations. The current remuneration system for management is not linked to the company's management plan. Thus, the ratio of fixed remuneration and stock option compensation is not stipulated. Based on the belief that "achieving the business plan" is the foundation that leads to "sustainable growth," we will continue to consider establishing voluntary advisory committees, etc. to enhance objectivity and transparency and performance-based compensation system that will contribute to the achievement of our business plan. |

【Supplementary Principle 4-10-1 Discretionary use of functions and the involvement and recommendations of independent outside directors】 | The Company has a Board of Corporate Auditors, of which two out of seven directors are appointed as independent outside directors. Currently, independent outside directors account for less than half of the Board of Directors, but we see that the system allows these individuals to make use of their unique skills, knowledge, and experience in order to stay involved and offer appropriate advice. At this time, we have not established an advisory committee, but we intend to further enhance governance in the future, and will use our discretion to make arrangements as needed so as to better interact with and receive advice from independent outside directors. |

<Disclosure Based on the Principles of the Corporate Governance Code (Excerpts)>

Principles | Disclosure contents |

【Principle 1-4 So-called strategically held shares】 | The company does not hold any shares of other listed companies as strategically held shares. However, if there was a need to acquire them to strengthen relationships or form tie-ups with other partner companies, the company will hold the shares upon verifying medium/long-term economic reasonability and disclosing its results. |

[Supplementary Principle 4-11-3 Analysis and evaluation of the effectiveness of the Board of Directors as a whole] | The company's Board of Directors conducted an evaluation of the effectiveness of the Board of Directors for FY 2019 in March 2020. A survey of all directors and corporate auditors was conducted regarding the size, composition, and role division of the Board of Directors, information provision and support system for the Board of Directors, the quantity and quality of the agenda and discussions at the Board of Directors. The evaluation was conducted in the form of discussions at the Board of Directors based on the results of the survey. As a result of the evaluation, the Board of Directors determined that the effectiveness of the Board of Directors is generally at a high level. Moreover, we will steadily implement measures to reform the points that we recognized that have room for improvement in terms of operation such as the quantity and quality of the agenda for the Board of Directors and the way information should be provided. |

【Principle 5-1 Policy for constructive dialogues with shareholders】 | The Management Planning Section is in charge of IR, and the directors of said Section manage IR in collaboration with relevant sections. The Section regularly holds sessions to introduce the company to individual investors and financial settlement briefings to analysts and institutional investors. The Section also makes efforts to enrich mutual communications through constructive dialogues with shareholders and reports the results of analysis and evaluation concerning management to the executives. The basic policy concerning “dialogues with shareholders” is compiled in the company’s “Guidelines” and disclosed on the web-page. |

This report is intended solely for information purposes, and is not intended as a solicitation to invest in the shares of this company. The information and opinions contained within this report are based on data made publicly available by the Company, and comes from sources that we judge to be reliable. However, we cannot guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness or validity of said information and or opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration. Copyright(C) Investment Bridge Co., Ltd. All Rights Reserved. |