Bridge Report:(3538)WILLPLUS the Fiscal Year ended June 2025

![]()

President Takaaki Naruse | WILLPLUS Holdings Corporation (3538) |

|

Company Information

Market | TSE Standard |

Industry | Retail (Commercial) |

President | Takaaki Naruse |

HQ Address | 5-13-15, Shiba, Minato-ku, Tokyo, Shiba Mita Mori Building 8th Floor |

Year-end | June |

Homepage |

Stock Information

Share Price | Shares Outstanding (Term-end) | Total Market Cap | ROE Act. | Trading Unit | |

¥1,008 | 10,412,300 shares | ¥10,495 million | 14.0% | 100 shares | |

DPS Est. | Dividend Yield Est. | EPS Est. | PER Est. | BPS Act. | PBR Act. |

¥46.00 | 4.6% | ¥143.62 | 7.0 x | ¥1,187.23 | 0.8 x |

* The share price is the closing price on September 26. The numbers are based on financial results for the fiscal year ended June 2025.

Earnings Trend

Fiscal Year | Sales | Operating Income | Ordinary Income | Net Income | EPS | DPS |

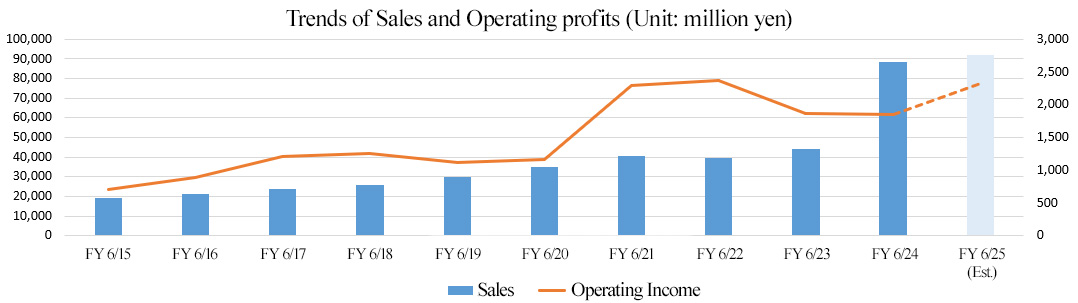

June 2022 Act. | 39,696 | 2,366 | 2,377 | 1,550 | 162.84 | 34.90 |

June 2023 Act. | 44,115 | 1,867 | 1,943 | 1,302 | 135.45 | 41.17 |

June 2024 Act. | 47,745 | 1,494 | 1,559 | 1,124 | 116.46 | 43.51 |

June 2025 Act. | 88,614 | 1,849 | 1,897 | 1,443 | 158.43 | 45.06 |

June 2026 Est. | 92,160 | 2,328 | 2,244 | 1,305 | 143.62 | 46.00 |

*Unit: million yen or yen. Estimates are those of the company.

This report includes Willplus Holdings Corporation's financial results for the fiscal year ended June 2025, earnings forecast for the fiscal year ending June 2026, and other information.

Table of Contents

Key Points

1. Company Overview

2. Mid- to Long-Term Strategy

3. Growth Strategy

4. Fiscal Year ended June 2025 Earnings Results

5. Fiscal Year ending June 2026 Earnings Forecasts

6. Conclusions

<Reference: Regarding Corporate Governance>

Key Points

- Willplus Holdings Corporation is a holding company with 6 dealers handling 17 brands of imported cars, including Jeep, BMW, Mini, and Volvo, and a consolidated subsidiary that operate used-car purchase, wholesale, and export. It is actively working to expand its business through an M&A strategy with an aim to acquire "new areas" and "new brand." At the same time, while continuing to "maximize business," the company is also committed to "maximizing GHG emissions reduction" by "greening its stores," seeing "solving climate change issues" as an "opportunity."

- In the fiscal year ended June 2025, sales increased 85.6% year on year to 88,614 million yen. The M&A of ENG INC., which was conducted in the previous fiscal year, made a significant contribution. Operating income increased 23.5% year on year to 1,849 million yen. Although gross profit increased only 32.8% year on year, it was able to offset increased SG&A expenses, including personnel expenses, investments in stores, and special expenses associated with the formation of a special investigation committee on the acquisition of treasury shares exceeding the distributable amount. While sales were mostly in line with the forecast, profit was significantly lower than expected. This was due to the impact of the yen's depreciation on the imported vehicle dealer business, resulting in higher prices of imported cars, leading to the number of new cars sold being lower than expected. In addition, the initial loss from the newly acquired business through M&A was higher than expected, and the Post Merger Integration (PMI) took time. In the used car export-related business, the supply of cars handled by our company to the used car market has expanded dramatically. In addition, the Malaysian currency, which had been on a strong trend against the yen, was on a weak trend against the yen, and demand from local importers shrank. As a result, sales fell below expectations in the second half of the fiscal year, when the export business to Malaysia is normally in a busy season.

- For the fiscal year ending June 2026, both sales and profit are expected to increase. Sales are projected to be 92,160 million yen, up 4.0% year on year, and operating income is forecast to be 2,328 million yen, up 25.9% year on year. Sales are expected to reach a record high. The imported car market in Japan is showing signs of bottoming out. Profit contributions from PMI attributable to M&A activities undertaken in the previous fiscal year are expected to become apparent this fiscal year. The dividend is expected to be 46.00 yen per share, up 0.94 yen per share from the previous fiscal year. The expected dividend payout ratio is 32.0%.

- The company recognizes its cost of equity as 5.3%. From the perspective of equity spread, ROE (14.0% for the fiscal year ended June 2025) is much higher than the cost of equity, but PBR is less than 1. Regarding this matter, in the updated “Measures for Achieving Management Focusing on Capital Costs and Stock Prices,” they noted that “PBR has not improved, reflecting the reality that the gain on negative goodwill through M&A boosted net profit,” and that “the outcome of M&A (= sales growth) has not been reflected in the stock price.” The company therefore believes that profit improvement through PMI is required to offset the impact of decline in the imported car market. For the fiscal year ending June 2026, they are expected to increase operating income by 26% despite a slight increase in sales. The company expects the profit contribution from PMI to become evident this fiscal year and to continue steadily.

1. Company Overview

Willplus Holdings Corporation is a holding company with 6 dealers handling 17 brands of imported cars, including Jeep, BMW, Mini, and Volvo, and a consolidated subsidiary that operate used-car purchase, wholesale, and export. It focuses on improving customer satisfaction and pursues growth through a multi-brand strategy, a dominant strategy, and an M&A strategy. It has a significant advantage in business revitalization capabilities in the M&A field. The company aims for further growth, taking the major environmental changes surrounding automobiles, including the shift to EVs, as an opportunity.

[1-1 Corporate History]

In January 1997, the father of President Takaaki Naruse established Sunflower CJ Co., Ltd., an imported car sales company, in Kitakyushu City, Fukuoka Prefecture. The company was the first official Chrysler dealer in western Japan.

In October 2004, President Naruse acquired all of the company's shares and started business activities as the Willplus Group.

Although it was a small dealer with a few staff members, including President Naruse, it achieved excellent results nationwide in sales of Chrysler cars and received high acclaim, which led him in 2005 to take over Chrysler's directly managed store in Ohta-ku, Tokyo, and advance to Tokyo. In 2006, the company opened a store in Kurume City, Fukuoka Prefecture. It also started a dominant strategy in Tokyo and Fukuoka.

Willplus Holdings Corporation was established in October 2007 to flexibly acquire dealers through optimal allocation of management resources and prompt management decision-making.

Under the holding company structure, the company actively expanded its business scope and was listed on the JASDAQ of the Tokyo Stock Exchange in March 2016. In September 2017, as the market changed, it shifted to the Second Section of the Tokyo Stock Exchange, and then it was listed on the First Section of the Tokyo Stock Exchange in February 2018. The company got listed on the Prime Market of Tokyo Stock Exchange in April 2022 in step with the market restructuring, and then listed on the Standard Market in October 2023.

[1-2 Corporate Philosophy]

In this section, we state the company's significance and core values.

Our Significance (MISSION STATEMENT) We propose a life with imported cars, share affluence, fun, and joy with more people, and continue to take on the challenge of drawing warm smiles on the face of everyone involved. |

Core Values ・Love our cars, love our colleagues, and work with pride. ・Always take on challenges and break through our limits. ・Achieve great results through teamwork. ・Make sure we reach our goal on time. ・Never give up until the end, and do our best. ・Provide richness, enjoyment, and joy. ・Never forget to be sincere and grateful. |

[1-3 Market Environment]

The business environment, which is essential in understanding the company, is as follows.

Regarding the business environment related to the M&A strategy, which is the company's growth driver, see

“”2. Mid- to Long-Term Strategy

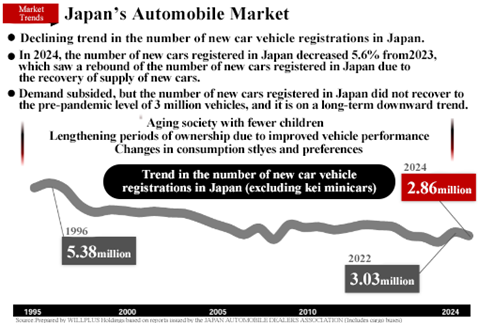

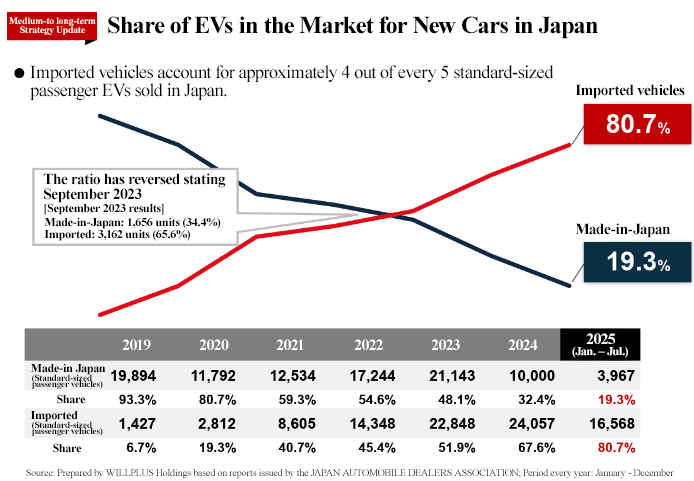

◎ The share of imported cars in the domestic passenger car market continues to increase, and the number of imported cars owned in Japan is growing steadily.

The number of new cars registered in Japan shows a decreasing trend due to the declining birth rates and aging population, the prolongation of the period of owning a car due to the elevation of functionality, changes in consumption styles and preferences (decrease of young people who own automobiles), etc.

(From the reference material of the company)

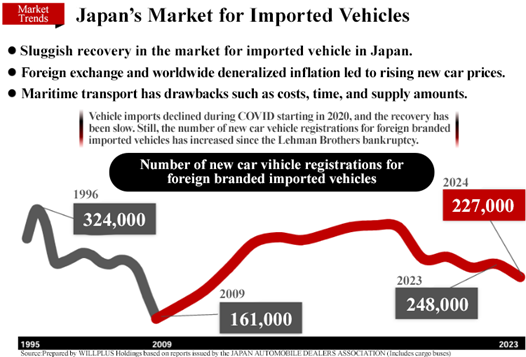

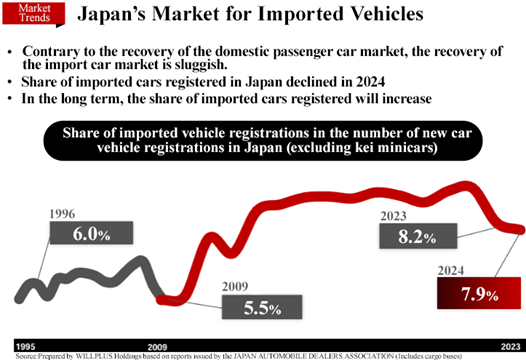

Amid such situation, although the number of new imported cars (made by overseas manufacturers) registered in Japan has been decreasing after 2020 due to the impact of COVID-19, and is recovering slowly, it has grown since the bankruptcy of Lehman Brothers. The recovery of the imported car market is sluggish, unlike the recovery of the domestic passenger car market, and the share of imported cars registered in Japan declined in 2024. However, in the long term, the share of imported cars registered in Japan shows a rising trend.

|

|

(From the reference material of the company)

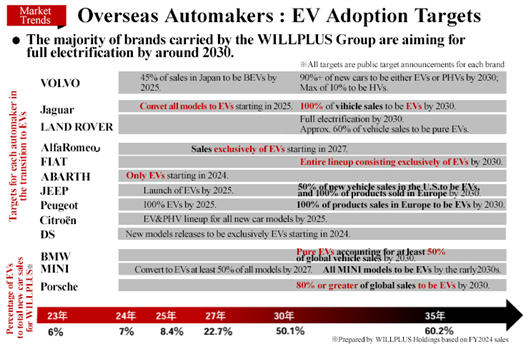

The imported car manufacturers are proactively addressing environmental issues and the majority of brands in which the company deals have announced plans aiming for complete electrification by 2030.

While the market share of EVs still accounts for just 1.5% of automobiles in Japan, there are more imported cars than cars manufactured in Japan among the EVs for personal use sold in Japan, which indicates that EVs are increasingly recognized as imported cars.

Moreover, active investment in Japan, such as establishing and expanding sales networks, has also increased the imported car manufacturers' market share.

|

|

(From the reference material of the company)

◎ Comparison with other companies in the same industry

Code | Company | Sales | Sales growth rate | Operating income | Profit growth rate | Operating income margin | ROE | Market Capitalization | PER | PBR |

3184 | ICDAHLD | 38,500 | +0.8 | 1,910 | +5.4 | 5.0% | 13.0 | 9,135 | 7.2 | 0.9 |

3538 | Willplus HLD | 92,160 | +4.0 | 2,328 | +25.9 | 2.5% | 14.0 | 10,516 | 7.0 | 0.9 |

7593 | VT HLD | 370,000 | +5.2 | 13,000 | +19.7 | 3.5% | 7.4 | 61,290 | 8.6 | 0.8 |

8291 | Nissan Tokyo Sales HLD | 145,000 | +2.4 | 7,000 | -5.6 | 4.8% | 7.6 | 34,983 | 7.8 | 0.6 |

9856 | KU HLD | 155,000 | -3.1 | 8,600 | -6.4 | 5.5% | 10.1 | 53,039 | 6.7 | 0.6 |

* Units: million yen and %. Sales and operating income are company forecasts for this term. ROE is the result of the previous fiscal year. Market capitalization is the number of shares at the end of the most recent quarter × the closing price on September 12, 2025. PER (forecasted figures) and PBR (actual figures) are based on the closing price on September 12, 2025.

Although ROE is the highest, PBR remains below 1 with PER being single-digit. The company expects to make steady progress with the measured mentioned in “2-5 Measures for Achieving Management Focusing on Capital Costs and Stock Prices” below.

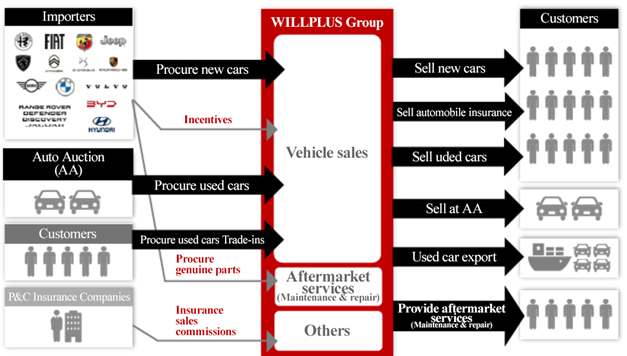

[1-4 Business Description]

(1) Overview

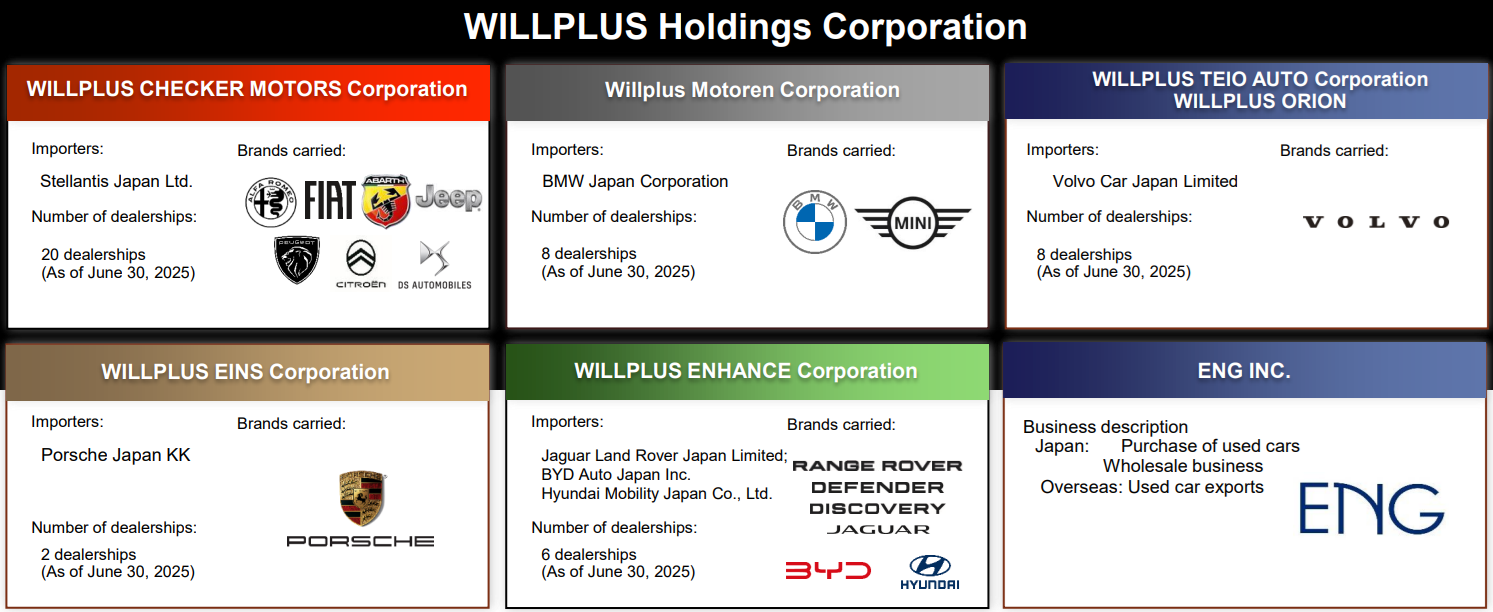

Under the holding company Willplus Holdings Corporation, seven consolidated subsidiaries engage in sales of imported new and used cars, vehicle maintenance, non-life insurance agency business, and used-car export. The company handles 17 brands. The company has an official dealer contract with an importer (a company that handles imported cars in Japan) for each brand it handles.

(From the reference material of the company)

(2) Segments

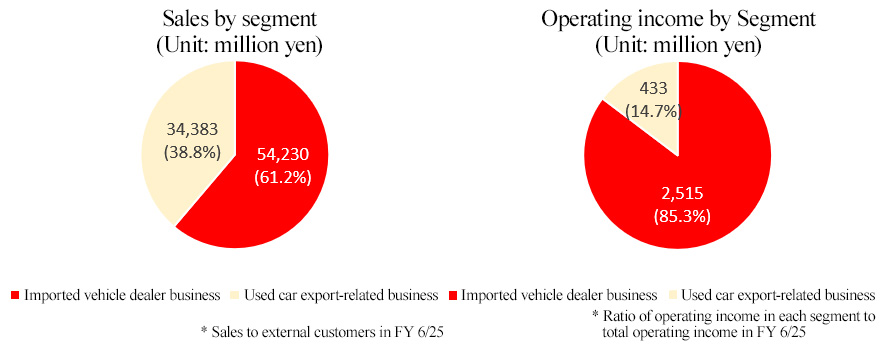

There are two segments to be reported: the imported vehicle dealer business and the used car export-related business.

(3) Products and services (business description)

The company discloses sales classified into the categories of new cars, used cars, auto auction sales, vehicle maintenance and other services in the summary of financial results. The company also discloses the domestic and overseas breakdowns of used car sales.

(From the reference material of the company)

Products and Services | Description |

|

New cars | As authorized dealers, the companies sell all new car brands procured from each importer. | |

Used cars | It mainly sells certified used cars of recent models of each brand with a short travel distance. Products are purchased through trade-ins at the time of selling new cars, purchases, and automobile auctions. ENG INC. exports used cars purchased in Japan mainly to Malaysia. | |

Sales | It sells trade-in used cars of other brands at automobile auctions. In addition, at the request of dealers of other companies, it may sell new and used vehicles owned by the corporate group. | |

Vehicle maintenance | The main services are maintenance, repair, and inspection of the sold vehicles. With the exception of some stores, service centers are set up alongside showrooms. | |

Others | It sells compulsory automobile liability insurance and voluntary insurance as an agent for non-life insurance companies. Incentive income related to new car sales from importers is also included. |

Although the sale of new cars is the main business. The company is focusing on the sale of used cars and strengthening customer relationships by providing services that customers need after purchasing a car, such as vehicle maintenance and car insurance sales.

Regarding vehicle maintenance, maintenance packages are provided to ensure maintenance after sale. As for insurance sales, the provision of detailed information on insurance products has been highly evaluated, and the enrollment and retention rates are higher than the industry average.

In addition to “the increase in the number of units sold = the increase in one-shot revenue,” an increase in the number of stores through M&A has led to an increase in recurring revenue in the form of “increase in the number of car maintenance and insurance contracts.”

Additionally, the inclusion of the "used car export-related business" in the business portfolio has enabled the company to enter a growing market and mitigate foreign exchange risk on a group-wide basis.

(4) Number of stores

As of the end of August 2025, the number of stores is 22 in Kyushu, 20 in Tokyo and Kanagawa, 1 in Yamaguchi, 2 in Miyagi, and 1 in Fukushima, for a total of 46 stores.

[1-5 Characteristics, Strengths, and Competitive Advantages]

(1) Advanced capability to revitalize business through M&A

From the perspective of "purchasing time," many companies currently use M&A strategies as a pillar of their growth strategies. It goes without saying that finding excellent deals and executing them at appropriate prices are essential for a successful M&A. However, the post-M&A process called PMI (Post Merger Integration) to create the expected synergy effect is seen as more important.

There are countless cases of M&A failing due to a lack of prior assessment of factors that impede integration and the inability to manage differences in corporate culture.

Under such circumstances, investors should pay attention to the company's business revitalization ability.

Since the establishment of Willplus Holdings in October 2007, the company has carried out 9 M&A deals to date. All deals have turned profitable. *Excluding those conducted less than last three fiscal years.

(From the reference material of the company)

The key to a successful M&A is sharing philosophies, such as pursuing the improvement of customer satisfaction and clarifying the evaluation criteria, which includes respecting challenges to the maximum extent possible. The company believes these key factors can drastically change companies and has great confidence in its ability to revitalize its business.

(2) The only listed company whose main business is being an authorized dealer of imported cars

While there are many companies that are authorized dealers of imported cars while mainly relying on selling used cars, the company is the only listed company that mainly sells new cars.

Believing that the share of imported cars in the domestic passenger car market (excluding mini cars) shows an increasing trend in the long term, the company intends to pursue further growth of revenues by expanding their market share based on an M&A strategy.

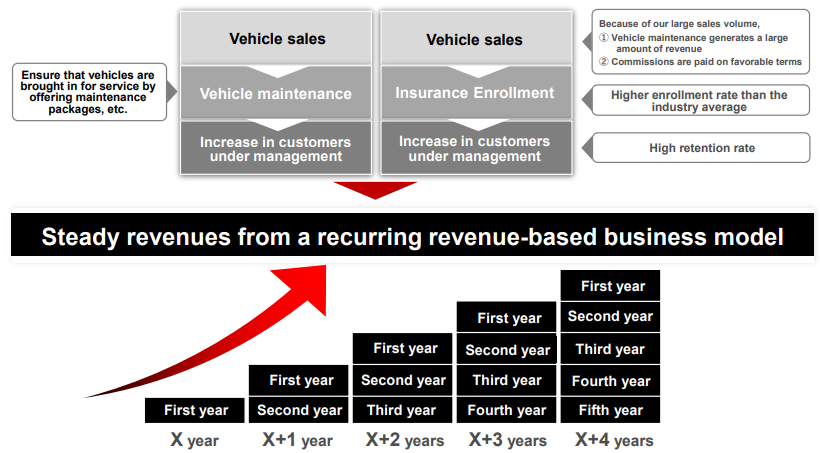

(3) Stable revenue structure based on the recurring revenue business

The stable revenue structure based on car maintenance and insurance sales, which are recognized as recurring revenue businesses, represents another significant characteristic and forte of the company.

The sum of car maintenance and insurance sales commissions has been growing for nine consecutive years since the company became publicly listed, reaching a new record high, partly due to M&A.

While a significant increase of owned cars in Japan can hardly be expected, a rising trend can be seen in the average number of years of using a car due to the changes in the economic situation, elevation of awareness concerning the environment, etc., inevitably making maintenance more important.

In addition, with the development of “CASE,” maintenance work is expected to become more complex, and maintenance work for imported vehicles is expected to be concentrated at authorized dealers.

Given these factors, the company believes that opportunities for earnings in the vehicle maintenance business will continue to increase, and it will seek to strengthen the foundation of this business by increasing the percentage of vehicles that come in for maintenance by adding maintenance packages and extended warranties for new vehicles.

In addition, the company will continue to brush up its staff's insurance knowledge to further improve customer satisfaction with regard to insurance commission income, which has been growing every fiscal year, and further strengthen the foundation for stable growth in the recurring revenue businesses of insurance sales and vehicle maintenance.

(From the reference material of the company)

2. Mid- to Long-Term Strategy

While today’s companies are required to improve their social significance and corporate value to solve social issues, the company formulated and implemented a mid- to long-term strategy based on its basic growth strategies (multi-brand strategy, dominant strategy, M&A strategy).

[2-1 Willplus Group Policy]

The company aims to enhance social value and corporate value. In other words, the company aspires to solve social issues and achieve corporate growth.

The company will strive to “contribute to the realization of a sustainable society” and “create social value” as a step toward the elevation of their social value.

Concretely, they will forge ahead with making their stores greener and decarbonizing the store areas, aiming for an enterprise that is needed by society.

They aim for “sustainable growth” and “elevation of corporate value in the medium term” as a step toward the elevation of their corporate value.

Concretely, they will promote their growth strategy, centered on M&A, and engage in solving issues through corporate revitalization in the car sales industry, where many small and medium-sized enterprises exist, by resolving the challenge of finding a successor, reusing assets (resources), improving profitability, and reeducating and stimulating human resources (human capital) while aiming for the maximization of sales and profit, as described below.

They view “the solving of issues concerning climate change” as an “opportunity,” aim for acquiring “new areas” and “new brands,” make proactive efforts to expand their business through “M&A” and work toward the “maximization of market capitalization” through the elevation of their social value and corporate value.

[2-2 Goal]

As the commitment to issues concerning climate change including the supply chain is sought, brand manufacturers are starting to demand the accurate grasping of GHG emissions from store operation, setting of goals for the reduction of GHG emissions and concrete initiatives to achieve these goals (ratio of EVs among demo cars, ratio of renewable energy use, ratio of recycled waste, etc.) from official dealers.

The company, which aims to be a leading company in solving climate change issues, has set the following GHG emission reduction targets.

To reduce Scope 1 + Scope 2 GHG emissions by 50% in FY 2030 compared to FY 2022 (6.25% reduction per year).

Concretely, we set goals of “increasing the ratio of low-carbon vehicles to company vehicles (including test-vehicles) to 80% or higher by FY 2030” and “adopting renewable energy at all stores by FY 2025.”

In March 2025, we obtained a third-party assurance on their GHG emissions in FY 2024.

Regarding Scope 2, we have continued to achieve zero emissions by switching to renewable energy contracts and utilizing green certificates. In FY 2024, the company has achieved a 25.8% reduction in emission levels compared to FY 2023, when the group target was achieved ahead of schedule.

[2-3 Initiatives of the Willplus Group]

The company’s initiatives for realizing “the elevation of social value” and “elevation of corporate value” at the same time are outlined below.

(1) Social Value Enhancement

① Contribute to the realization of a decarbonized society by promoting green store operations

In addition to setting the above reduction targets, the company intends to make capital investments to promote the spread of EVs in its store areas as an imported car dealer striving to be one of the first to promote green store operations, thereby contributing to the decarbonization of the domestic automobile industry.

The achievements they have made so far are as follows.

(From the reference material of the company)

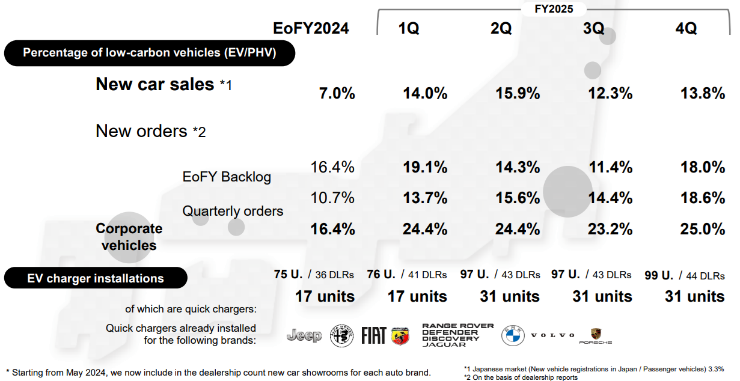

The number of EV chargers installed is increasing in parallel with the expansion of the EV lineup of the brands handled by the company. As of the end of June 2025, a total of 130 units have been installed, including 31 rapid chargers and 99 standard chargers.

The ratio of low-carbon vehicles to new car sales and company-owned cars also continues to increase. It increased by more than four times in the fiscal year ended June 2025 from the fiscal year ended June 2022.

② Other Initiatives and Responses

◎ Obtained the score B in the CDP “Climate Change” questionnaire for three consecutive years

In response to requests from institutional investors and purchasing companies around the world, the company answered the questionnaire regarding climate change conducted by the international organization Carbon Disclosure Project (CDP), which promotes companies to disclose environmental information, and obtained Score B for three consecutive years (2022, 2023, and 2024) in February 2025.

The CDP questionnaire is aimed at evaluating each organization’s disclosure of environmental information with the grades A to F as a global standard regarding “E” of ESG (environment, society, and governance). As of 2024, about 22,000 companies, which account for over two thirds of the global market cap, were scored by CDP, and institutional investors and purchasing companies around the world refer to such information when making decisions. In Japan, about 2,000 companies, including over 1,000 companies listed on the Prime Market, answered the questionnaire.

(2) Enhancement of corporate value through promotion of M&A

M&A is an important measure for quickly entering new areas, acquiring new brands, and expanding the market shares of existing brands. In the saturated domestic automobile market, the company believes that M&A is the most appropriate and priority strategy from the perspectives of customer acquisition, early return on investment, and securing profits.

Armed with the "advanced capability to revitalize business through M&A" mentioned in [1-5 Characteristics, Strengths, and Competitive Advantages,] they will strive to expand their sales and profit through M&A and steady PMI.

① Business Environment for M&A Promotion

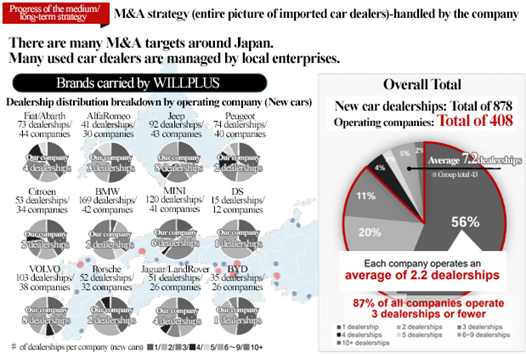

◎ Dealer Status

According to the company's assessment, there will be a total of 649 imported automobile dealers operating throughout Japan by the end of 2024, with a total of 1,525 new car sales offices. Each company had an average of 2.3 shops, while small and medium-sized businesses with three or fewer shops accounted for approx. 80% of the total number of dealers.

Store operation varies from brand to brand, and some brands are consolidating capital.

In addition, many dealers are struggling with the difficulty in finding successors, a common problem for small and medium-sized companies in Japan.

|

|

(From the reference material of the company)

For these imported car dealers, the "CASE" of automobiles, of which "Electric Vehicle" and "Connected" are the most important management issues for the future.

* "CASE" stands for Connected, Autonomous, Shared & Services (which may refer to car sharing and services/sharing only), and Electric. They are drastically changing the conventional concept of a "car" and creating new demand and markets in each of these areas.

◎ Enhanced Environmental Awareness and the Progress of the Shift to EVs

With heightened awareness of the global warming crisis, efforts to reduce greenhouse gas emissions and realize a decarbonized society are progressing rapidly.

One of the most significant concerns is reducing automotive emissions, and as governments try to attain carbon neutrality by 2050, automobile manufacturers are shifting from traditional gasoline and diesel engine cars to electric vehicles (EVs) in order to survive.

As mentioned in [1-3 Market Environment], manufacturers headquartered in Europe, which has long had a high degree of environmental awareness, have been particularly engaged in the transition to EVs.

On the other hand, while Japanese manufacturers set targets for the number and ratio of sold EVs, the expansion pace is sluggish in comparison with overseas competitors and there is a high possibility that the shares of imported cars will continue growing in regard to the sale of EVs in Japan.

At the same time, brand car manufacturers must commit to developing a firm understanding of emissions throughout their supply chains and to reducing them, so they are increasingly urging dealers to not only understand their current emissions, but also to make appropriate capital investments and responses to climate change issues, such as increasing EV purchases, installing quick chargers, and disclosing emission reduction targets.

Many dealers, however, face financial and human resource limits that make it difficult for them to respond adequately, and some analysts predict that brand car manufacturers may take the lead in further combining and restructuring vendors who can respond appropriately to such demand.

◎ Complication of car maintenance through the spread of connected systems and EVs

The term "connected" refers to the usage of communication equipment in automobiles to enable continuous external contact. Equipping vehicles with a SIM card will allow for grasping the state of a car and the situation on a road, exchange of information between cars and between a car and infrastructure, remote control, etc.

The connected automobile will evolve into smartphone-like devices, improving convenience while potentially complicating maintenance work in the case of a breakdown or vehicle inspection.

Furthermore, the previously noted shift to EVs will have a significant influence on car maintenance. Through the distribution of EVs, high-voltage battery and generator failures will increase, and vehicle maintenance will need to manage high-voltage systems, prompting substantial investment in high-voltage equipment and special training for safety reasons. Because the shift to connected systems and electric cars will need greater investment in both hardware and software, maintenance work for imported vehicles is likely to be concentrated in the hands of authorized dealers and large capital organizations with substantial investment capacity.

② The company's policy on M&A

◎ Actively addressing climate change issues

While responding to EVs and connected automobile is an urgent task for imported car dealers, the company intends to differentiate itself by building stores that are preferred by brand car manufacturers and by acquiring dealers who find it challenging to address these issues through M&A. By doing so, it hopes to expand into new areas and pick up new brands in order to grow and boost its corporate value. Additionally, the company wants to help with social issues by creating new brands and working to make its stores greener.

The company will not only decarbonize the neighboring area and turn the stores green, but it will also reinvigorate the social capital that already exists by repurposing resources and assets including stores, retraining personnel, and enhancing productivity by streamlining processes using DX.

◎ Favorable M&A Conditions after the subsiding of COVID-19

The company believes that the M&A strategy is beginning to receive a tailwind as COVID-19 is coming to an end.

*2020-2022: Business environment in which M&A (sale of business) is unlikely to be conducted

In the wake of the outbreak and spread of COVID-19, the demand for automobiles as a safe transportation means or for domestic travel as an alternative to overseas travel grew rapidly from 2020 to 2021.

In 2022, the prices of new automobiles skyrocketed due to the shortage of supply caused by the global shortage of semiconductors and the rise in material prices, and the shortage of new automobiles led to the growth of demand for used automobiles, and the prices of used automobiles rose significantly.

In such business environment, the sale and order receipt of automobile dealers were healthy. Inventory declined, working capital shrank, and order backlog increased steeply, so even dealers with weak marketing capabilities and small capital stock were able to operate business without trouble.

On the other hand, dealers thinking of selling their businesses decreased in that situation. It was unfavorable for the M&A strategy of the company, but the company’s growth and operating income margin exceeded the average in the industry, and the company concentrated managerial resources onto M&A in the next phase.

*2023-2025: Acceleration of M&A in parallel with the recovery of supply of new automobiles

The environment has been changing from 2023 to 2025.

The prices of new cars have been high since they were raised considerably in 2022. Meanwhile, the supply of new cars recovered due to the elimination of shortage of semiconductors, the prices of used cars are temporarily weakened.

Due to the hovering prices of new cars, costs augmented through the increases in investment in company-owned cars and depreciation, decrease in the number of customers visiting the store, and inventory and working capital increased, making cash management difficult and squeezing small and medium-sized dealers.

In addition to these changes in the business environment, the profitability of automobile dealers is trending downward due to the augmentation of costs for enhancing corporate governance and tackling environmental issues.

As the importance of addressing climate change grows, coupled with challenges such as the shortage of successors for imported car dealers and deteriorating business environments, the company anticipates an increase in M&A, particularly among small and medium-sized dealers with weak financial foundations. The company believes that its M&A strategy will accelerate significantly as a result.

[2-4 Medium- to Long-term Shareholder Return Strategy]

The company, which has increased dividends consecutively since its listing, has established the following policy.

☆ | To target a medium- to long-term ROE of 15% or higher (14.0% in the fiscal year ended June 2025). |

☆ | The company will gradually raise its dividend payment ratio to 30% by fiscal year 2026 in order to "keep sufficient capital" and "further boost shareholder return" at the same time. |

☆ | From the fiscal year 2027 onward, the company will continue to pursue a dividend policy of pursuing a payout ratio of 30% while aiming for progressive dividends. |

☆ | The company will sustain and increase consistent and ongoing returns to shareholders, with a DOE of 4.5% or higher. |

In the fiscal year ended June 2025, the dividend remained 45.06 yen/share as forecast, while the company raised payout ratio from 21.4% in the fiscal year ended June 2022 to 28.4%.

They are forecasting a dividend of 46.00 yen/share and a payout ratio of 32.0% for this fiscal year ending in June 2026.

In order to demonstrate its extremely aggressive profit growth policy and shareholder return stance, the company aims to achieve ROE that significantly exceeds the cost of shareholders' equity, increase the dividend payout ratio gradually, and increase dividends in excess of profit growth.

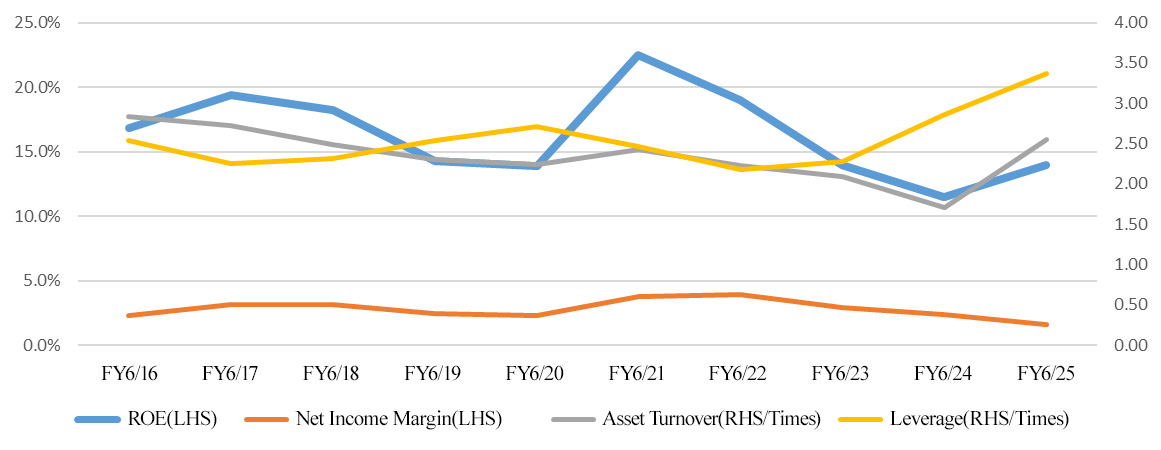

(ROE Analysis)

| FY 6/18 | FY 6/19 | FY 6/20 | FY 6/21 | FY 6/22 | FY 6/23 | FY 6/24 | FY 6/25 |

ROE (%) | 18.2 | 14.3 | 13.9 | 22.5 | 19.0 | 14.0 | 11.5 | 14.0 |

Net income margin (%) | 3.16 | 2.44 | 2.29 | 3.76 | 3.91 | 2.95 | 2.35 | 1.63 |

Total asset turnover (times) | 2.49 | 2.30 | 2.24 | 2.43 | 2.23 | 2.09 | 1.71 | 2.55 |

Leverage (x) | 2.31 | 2.54 | 2.71 | 2.46 | 2.18 | 2.28 | 2.85 | 3.37 |

Although it exceeds 8%, which is generally considered as a target for Japanese companies, it is declining. It was mainly due to an increase in leverage in the fiscal year ended June 2025. If profitability improves, ROE can be expected to rise further, and PBR can be expected to recover to the 1x level.

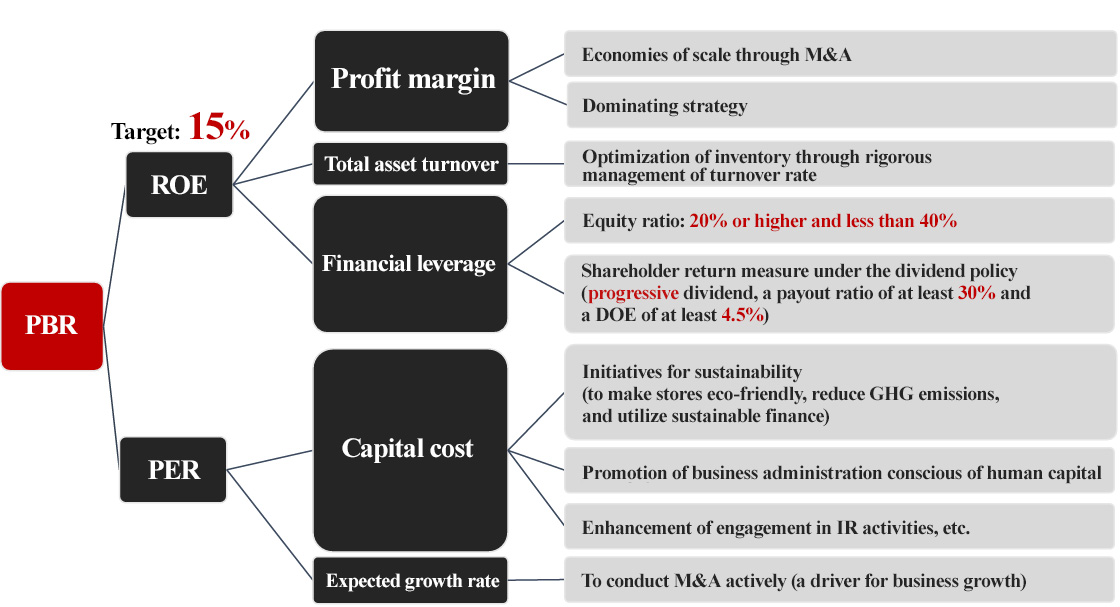

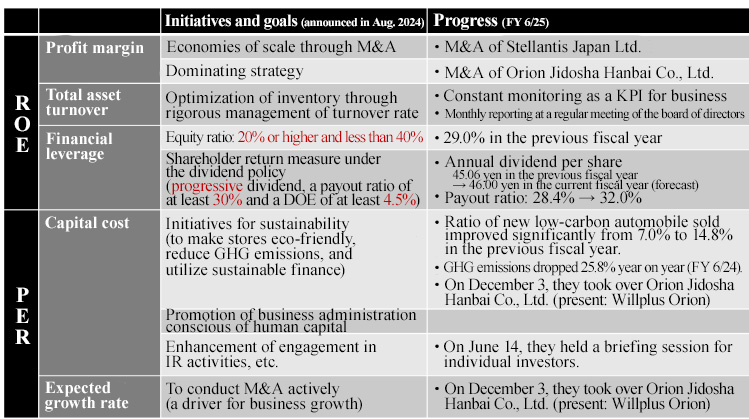

[2-5 Measures for Achieving Management Focusing on Capital Costs and Stock Prices]

Regarding the “Measures for Achieving Management Focusing on Capital Costs and Stock Prices” requested by the Tokyo Stock Exchange, the company has presented the following analysis and future initiatives.

(1) Analysis of the Current Situation

(Stock Price)

While the supply of new cars has recovered after the COVID-19 pandemic, car prices have remained high due to the weak yen. As the overall imported car market has been sluggish, ROE has declined due to deteriorating business performance. As a result, stock price has been low, with PBR less than 1x despite the support of dividend yield.

(Trends in Sales and New Store Openings)

During periods of strong business performance (FY 2021 and FY 2022), no M&A transactions were made. From FY 2023, business performance declined due to the deterioration of the imported car market, but M&A increased rapidly. However, stock price does not represent the outcome of M&A (sales growth). The company acknowledges that "profit improvement through PMI" is required to mitigate the effects of the declining imported car market.

(ROE and PBR)

The company acknowledges its cost of equity as 5.3% based on the CAPM, and ROE has been exceeding the capital cost since the company’s public listing. Although ROE improved to 14.0% in the fiscal year ended June 2025, PBR did not improve due to the gain on negative goodwill through M&A, which has increased net income. PBR ranged between 0.8x and 2.2x, with the current level considered to be near the bottom.

(2) Initiatives to Improve PBR

The company is implementing the following measures from the perspective of profit margin, total asset turnover, financial leverage, capital cost, and expected growth rate.

|

|

As a financial strategy, they have set the optimal capital structure at “an equity ratio of 20% or higher, but less than 40%.” The company will constantly monitor the inventory level and turnover rate in the imported vehicle dealer business along with the receivable level of accounts, collection period, and default rate in the used car export-related business. In addition, they will aim to maintain an ROE of 15% or higher while maintaining appropriate capital by pursuing management that “does not hold” fixed assets as much as possible.

As a result, the company will be able to maintain ROE well above the cost of shareholders' equity of 5.3% over the long term. Going forward, they will continue to maintain a system in which ROE consistently and stably exceeds the capital cost, regardless of β value fluctuations, in order to maximize corporate value (market capitalization).

Regarding shareholder returns, as stated in “2-4 Medium- to Long-term Shareholder Return Strategy,” they will strive to maintain and improve stable and consistent profit returns through progressive dividends with a target dividend payout ratio of 30% and a minimum DOE of 4.5%.

In addition, they will strengthen shareholder returns through the flexible acquisition of treasury shares and commit to improving corporate value through the introduction of various equity-based initiatives.

In terms of IR, the company intends to hold the general meeting of shareholders, build a forum for interaction with shareholders, both individual shareholders and institutional investors, with the goal of promoting two-way communication by the management.

3. Growth Strategy

Three strategies promote the company's growth: "multi-brand strategy," "dominant strategy," and "M&A strategy."

(From the reference material of the company)

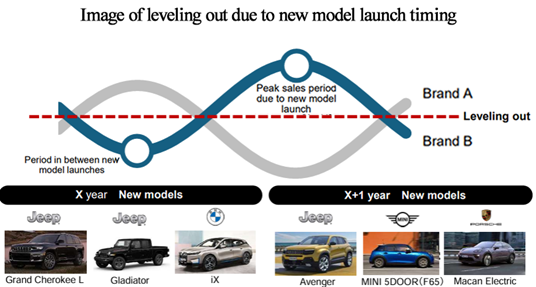

[3-1 Multi-brand strategy: Expansion of earnings and leveling of the sales cycle]

By handling multiple brands without relying on a specific brand, the company aims to even out the impact of the sales cycle caused by differences in the timing of new model launches among brands.

The company currently handles 17 brands and aims to expand the number of brands through M&A strategies.

(From the reference material of the company)

[3-2 Dominant strategy: Increase the market share and maximize profit in the same trade area]

The company is opening new stores in cities with a population of 1 million and surrounding cities as specified areas in order to increase its market share by attracting customers in the same trade area, improve productivity through efficient personnel allocation among stores, and maximize profit.

Currently, the company focuses on Tokyo, Kanagawa, and Fukuoka, which are Japan's top markets in terms of new car registrations and ownership of imported cars (passenger cars), but it is also aiming to expand into other areas through the M&A strategy.

[3-3 M&A Strategy: Speed Up]

M&A is an important measure for quickly entering new areas, acquiring new brands (multi-brand strategy), and expanding the market share of existing brands. Following the acquisition of a huge number of stores, trade areas, and new brands via M&A, the company has been extending its business by building additional stores in neighboring regions to complement its trade areas.

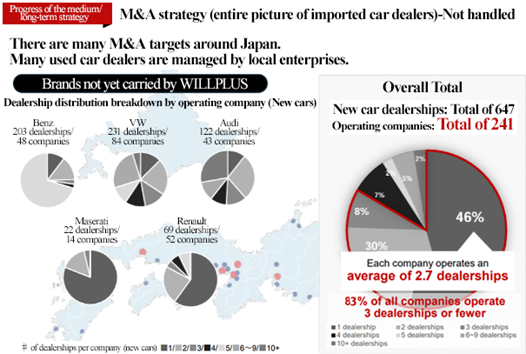

There are many brands that the company targets but does not handle, such as Mercedes-Benz, Volkswagen, and Audi, and there is a tremendous opportunity for growth through the M&A acquisition of additional brands.

Aside from direct approaches from the company to the target companies and direct contact from the target companies back to the company, the company searches out deals through introductions from importers, financial institutions, and M&A brokerage firms.

The company will carry out due diligence and only engage in negotiations with those agreements that satisfy the company's investment recovery requirements following internal discussions that focus on prospects for future development and synergies.

Since their founding in October 2007, WILLPLUS Holdings has implemented 9 projects of M&A (*Excluding projects implemented within the last 3 fiscal years). They have achieved profitability in all these projects by injecting their know-how, etc. in addition to opening new stores and making investments in stores, including relocation and renovation, and the high level of their PMI capability is attracting attention.

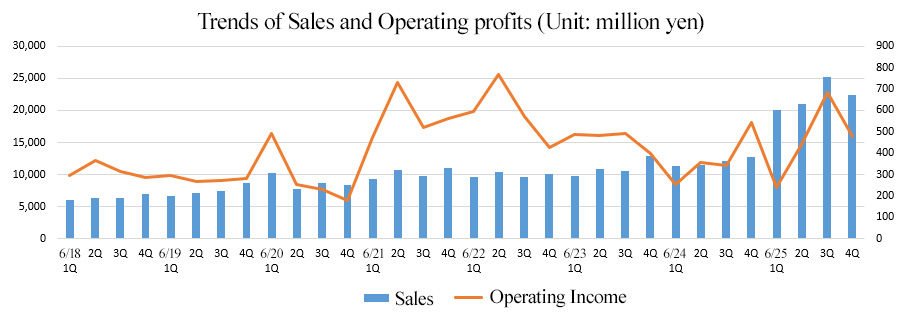

4. Fiscal Year ended June 2025 Earnings Results

[4-1 Overview of Financial Results]

| FY 6/24 | Ratio to sales | FY 6/25 | Ratio to sales | YoY | Ratio to forecast |

Sales | 47,745 | 100.0% | 88,614 | 100.0% | +85.6% | +0.3% |

Gross Profit | 9,364 | 19.6% | 12,432 | 14.0% | +32.8% | - |

SG&A | 7,866 | 16.5% | 10,582 | 11.9% | +34.5% | - |

Operating Income | 1,497 | 3.1% | 1,849 | 2.1% | +23.5% | -26.8% |

Ordinary Income | 1,562 | 3.3% | 1,897 | 2.1% | +21.5% | -23.8% |

Net Income | 1,120 | 2.3% | 1,443 | 1.6% | +28.8% | +0.4% |

*Unit: million yen. Net income is net income attributable to owners of the parent.

Sales and profit increased, but profit was lower than expected.

Sales increased 85.6% year on year to 88,614 million yen. The M&A of ENG INC., which was conducted in the previous fiscal year, made a significant contribution.

Operating income increased 23.5% year on year to 1,849 million yen. Although gross profit increased only 32.8% year on year, it was able to offset increased SG&A expenses, including personnel expenses, investments in stores, and special expenses associated with the formation of a special investigation committee on the acquisition of treasury shares exceeding the distributable amount.

Net income rose 28.8% year on year to 1,443 million yen. The company recorded a gain on negative goodwill of 308 million yen as an extraordinary profit, and an impairment loss of 249 million yen as an extraordinary loss.

While sales were mostly in line with the forecast, profit was significantly lower than expected. This was due to the impact of the yen's depreciation on the imported vehicle dealer business, resulting in higher prices of imported cars, leading to the number of new cars sold being lower than expected. In addition, the initial loss from the newly acquired business through M&A was higher than expected, and the Post Merger Integration (PMI) took time. In the used car export-related business, the supply of cars handled by our company to the used car market has expanded dramatically. In addition, the Malaysian currency, which had been on a strong trend against the yen, was on a weak trend against the yen, and demand from local importers shrank. As a result, sales fell below expectations in the second half of the fiscal year, when the export business to Malaysia is normally in a busy season.

[4-2 Market Environment]

The Japanese market of passenger cars (in units) expanded steadily by 3.9% year on year. The cars manufactured by the foreign manufacturers faced a challenging environment as a result of global inflation and price hikes caused by the yen depreciation. However, since January 2025, it has recovered moderately. In April-June 2025, the imported car market in Japan grew rapidly by 9.8% year on year. From April to July, it outperformed the growth of Japanese passenger cars for four consecutive months.

In the period from April to June 2025, the brands (in units) handled by the company also increased significantly by 13.3%. On a monthly basis, it has been higher than the previous year for seven consecutive months since January 2025. The full model change of MINI, which has continued since 2024, has contributed significantly. While the sales for Jeep have been stagnant since March 2025, the sales increased year on year in July for the first time in a while, showing signs of recovery.

[4-3 Trend of each business and sales by product category]

◎ Trend of each business

| FY 6/24 | Composition ratio | FY 6/25 | Composition ratio | YoY |

Sales |

|

|

|

|

|

Imported vehicle dealer business | 47,745 | 100.0% | 54,230 | 61.2% | +13.6% |

Used car export-related business | - | - | 34,383 | 38.8% | - |

Total | 47,745 | 100.0% | 88,614 | 100.0% | +85.6% |

Segment profit |

|

|

|

|

|

Imported vehicle dealer business | 2,369 | 5.0% | 2,515 | 4.6% | +6.2% |

Used car export-related business | - | - | 433 | 1.3% | - |

Adjustment | -872 | - | -1,100 | - | - |

Total | 1,497 | 3.1% | 1,849 | 2.1% | +23.5% |

*Unit: million yen. The composition ratio of profit is the profit margin on sales.

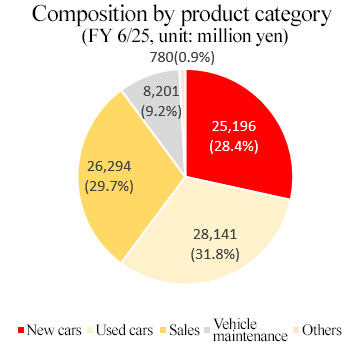

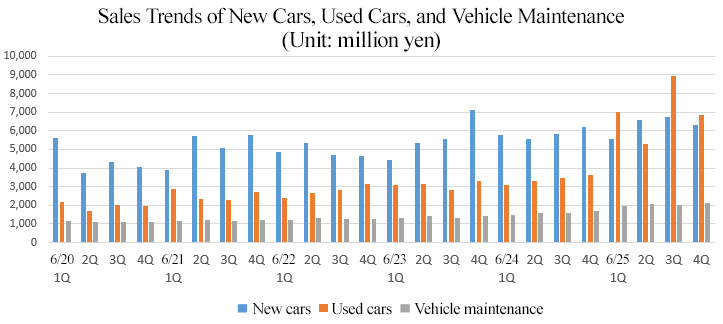

◎ Sales by product category

(FY6/25)

| Import (*1) | YoY | Export (*2) | YoY | Total (*3) | YoY |

New cars | 25,196 | +7.9% | - | - | 25,196 | +7.9% |

Used cars (Japan) | 14,852 | +10.3% | 214 | - | 15,067 | +11.9% |

(Overseas) | - | - | 13,074 | - | 13,074 | - |

Used car total | 14,852 | +10.3% | 13,288 | - | 28,141 | +108.9% |

Auto auction sales | 5,221 | +31.9% | 21,072 | - | 26,294 | +564.3% |

Subtotal of sales of cars | 45,270 | +11.0% | 34,361 | - | 79,632 | +95.2% |

Car maintenance | 8,201 | +29.0% | - | - | 8,201 | +29.0% |

Other | 758 | +26.7% | 22 | - | 780 | +30.4% |

Total | 54,230 | +13.6% | 34,383 | - | 88,614 | +85.6% |

*Unit: million yen. Import (*1) represents imported vehicle dealer business, Export (*2) represents used car export-related business, Total (*3) represents Group total.

<Imported vehicle dealer business>

*New Car Sales

In addition to an increase in the number of stores, sales remained strong, particularly for brands with strong demand for new models and popular cars. The number of new cars sold increased 10.1% year on year, and the sales of new cars increased 7.9% year on year, offsetting declines in brands whose deliveries were concentrated in the same period of the previous year and brands where the effect of new models had diminished.

*Used Car Sales

The company focused on used car sales, particularly for brands experiencing a decline in new car sales. As a result, sales revenue increased 10.3% year on year.

We focused on reducing inventory, which had been relatively overstocked.

*Recurring-revenue business

The business has shown steady growth, thanks to an increase in the number of stores through the M&A strategy and a steady increase in the number of repeat customers.

The sales of car maintenance increased 29.0% year on year, reaching a record high. It also reached a record high in the fourth quarter (April to June 2025). The effects of PMI through securing personnel and customer management following M&A became apparent.

Insurance commission income also grew significantly, up 22.4% year on year.

<Used car export-related business>

Although the growth rate of the domestic economy of Malaysia, a major export destination, decreased due to concerns over the impact of U.S. trade policies, it continued to expand, supported by strong domestic demand. As a result, demand for imported cars remained strong. In the first half of the year, the strong demand for used cars in Malaysia and the ongoing weak yen trend provided tailwinds, leading to a favorable number of exported cars. The company had a successful start in January 2025, which is usually the month with the highest export increase in the year. However, in addition to a sharp increase in the supply of used cars, particularly for models exported by the company to the used car market beginning in February 2025, the Malaysian currency, which had previously been weak against the yen, became strong, and demand from local importers weakened.

Sale by distributors stepped up their sales while focusing on stock turnover ratio. In preparation for the busy season, the company intensified the procurement of cars, focusing on models for overseas export. Simultaneously, they promoted procurement based on the assumption that the used car market in the Japanese market would also remain strong. However, due to bad market conditions caused by the increased domestic supply, demand in the Malaysian market also dropped, and the market was weak in both domestic and overseas areas. As a result, the company promoted sales with an emphasis on stock turnover ratio, resulting in a decline in profit margin.

[4-4 Financial Standing and Cash Flow]

◎ Main Balance Sheet

| End of June 2024 | End of June 2025 | Increase/ Decrease |

| End of June 2024 | End of June 2025 | Increase/ Decrease |

Current Assets | 22,920 | 26,675 | +3,755 | Current Liabilities | 13,968 | 18,051 | +4,082 |

Cash and Deposits | 7,508 | 8,245 | +737 | Payables | 3,534 | 4,182 | +647 |

Inventories | 10,779 | 13,276 | +2,496 | ST Borrowings | 6,760 | 10,362 | +3,602 |

Noncurrent Assets | 9,231 | 10,555 | +1,324 | Noncurrent Liabilities | 7,109 | 6,975 | -133 |

Tangible Assets | 7,997 | 8,865 | +867 | LT Borrowings | 6,415 | 6,171 | -243 |

Buildings and Structures | 4,645 | 4,325 | -319 | Total Liabilities | 21,077 | 25,026 | +3,948 |

Intangible Assets | 312 | 266 | -46 | Net Assets | 11,073 | 12,204 | +1,131 |

Investment, Others | 921 | 1,424 | +503 | Retained Earnings | 9,140 | 10,167 | +1,026 |

Total Assets | 32,151 | 37,231 | +5,079 | Total Liabilities and Net Assets | 32,151 | 37,231 | +5,079 |

*Unit: million yen.

Both assets and liabilities increased through M&A. In the imported vehicle dealer business, new car inventory is at a healthy level; however, used car inventory is relatively overstocked, and they will continue to focus on reducing it. Capital-to-asset ratio declined 1.5 points from the end of the previous fiscal year to 29.0%, but it is considered to be within the range of appropriate capital.

◎ CF

| FY 6/24 | FY 6/25 | Increase/ Decrease |

Operating CF | 2,505 | -1,303 | -3,808 |

Investing CF | -3,857 | -545 | +3,312 |

Free CF | -1,352 | -1,848 | -495 |

Financing CF | 4,566 | 2,578 | -1,987 |

Cash and Equivalents | 7,503 | 8,234 | +730 |

*Unit: million yen.

Operating cash flow turned negative and the deficit of free cash flow augmented due to an increase in inventory assets and a gain on negative goodwill.

The cash position improved.

[4-5 Topics]

(1) Stock repurchase

In May 2025, the company resolved and executed the repurchase of its own shares.

The company adopted a stock compensation program for employees in September 2023 with the aim of increasing their awareness of participation in management, playing an active role over the long term, and contributing to the enhancement of corporate value through their ownership of the company's stock. The treasury shares acquired this time will be used for future stock compensation program to promote human capital management and further enhance corporate value.

The company acquired 50,000 shares (approximately 53 million yen) on May 15, 2025, through Tokyo Stock Exchange’s system for purchasing treasury shares through off-floor trading (ToSTNET-3).

(2) Adoption of a Performance-based Stock Compensation Program (BIP Trust for Executives’ Compensation)

In August 2025, the company resolved to adopt the “BIP (Board Incentive Plan) Trust for Executives’ Compensation” as a new performance-based stock compensation program for the company's directors (excluding outside directors and directors who are audit & supervisory committee members), replacing the previous performance-based stock compensation program, the “Stock Grant Trust (BBT [Board Benefit Trust]).” The adoption of the program is subject to approval at the 18th Ordinary General Meeting of Shareholders scheduled for September 25, 2025.

(BIP [Board Incentive Plan] Trust for Executives’ Compensation)

A stock compensation program under which a trust acquires the company's shares using funds equivalent to the amount of remuneration paid to directors by the company, and then the trust distributes the company's shares to directors based on their position and the achievement of performance targets, etc. The plan covers five consecutive fiscal years, initially from the fiscal year ending June 2026 to the fiscal year ending June 2030.

(Purpose of Introducing the BIP Trust for Executives’ Compensation)

The company will adopt the BIP Trust for Executives’ Compensation to further improve efficiency and optimize the operation of the performance-based stock compensation program, clarify the link between the remuneration of directors and the company's performance and stock value, and increase the incentive for directors to continuously achieve management goals while taking appropriate risks.

Under this system, the company's shares and cash equivalent to the converted value of the shares are distributed to directors based on their positions, etc. The company has established a Compensation Advisory Committee, a majority of whose members are outside directors, as an advisory body to the board of directors for the purpose of strengthening the independence, objectivity, and accountability of the functions of the board of directors related to remuneration for directors. The adoption of the BIP Trust for Executives’ Compensation has been deliberated by this committee.

(3) Status of store openings

Based on the comprehensive agreement for “Kyushu (Fukuoka City, Fukuoka Prefecture)” and “Tohoku (Sendai City, Miyagi Prefecture)” concluded with Hyundai Mobility Japan Co., Ltd. in January 2025 and the basic agreement regarding opening a store in “Fukuoka City, Fukuoka Prefecture,” the first store under the new brand “Hyundai” was opened under the name “Hyundai Citystore Sendai” in Sendai City on June 28, 2025.

In July 2025, they opened both “BYD Auto Fukuoka” and “Hyundai Citystore Fukuoka” in Fukuoka City, Fukuoka Prefecture. Since both the showrooms are nearby in LaLaport Fukuoka, customers can test drive and compare cars from both brands.

(4) Getting a Sustainability Linked Loan

In June 2025, the company secured funding from Chiba Bank through “Chiba Bank Leaders Loan NEXT (target-linked),” a sustainability linked loan.

(Overview of the Sustainability Linked Loan)

It aims to promote and support environmentally and socially sustainable economic activities and economic growth by establishing sustainability targets in conjunction with borrowers' sustainability policies and strategies, as well as by linking borrowing conditions such as interest rates to the achievement of sustainability targets, thereby incentivizing borrowers to achieve the targets.

(Overview of Chiba Bank Leaders Loan NEXT (target-linked))

It refers to important elements from international principles such as the Sustainability Linked Loan Principles, the Green Loan Principles, and the Ministry of the Environment Guidelines, and it composes a Sustainability Linked Loan based on a framework independently designed by Chiba Bank. Chibagin Research Institute Corporation, a third-party evaluation organization inside the Chiba Bank Group, evaluates the framework developed in-house by Chiba Bank.

In the framework of this loan, WILLPLUS Holdings Corporation has set “the reduction of GHG emissions (per unit basis) within the Wilplus Group” as a KPI and believes that it will contribute to the decarbonization of the automobile industry by addressing climate change issues. The measurement scope is defined as “Scope 1 (direct emissions of greenhouse gases by business operators themselves).”

The contract period is five years and the loan amount is one billion yen.

5. Fiscal Year ending June 2026 Earnings Forecasts

[Earnings Forecast]

| FY 6/25 | Ratio to Sales | FY6/26 (Est) | Ratio to Sales | YoY |

Sales | 88,614 | 100.0% | 92,160 | 100.0% | +4.0% |

Operating Income | 1,849 | 2.1% | 2,328 | 2.5% | +25.9% |

Ordinary Income | 1,897 | 2.1% | 2,244 | 2.4% | +18.3% |

Net Income | 1,443 | 1.6% | 1,305 | 1.4% | -9.6% |

*Unit: million yen. Estimates are those of the company.

Sales and profits are expected to increase. Sales are forecast to hit a record high.

Sales are projected to be 92,160 million yen, up 4.0% year on year, and operating income is forecast to be 2,328 million yen, up 25.9% year on year. Sales are expected to reach a record high. The imported car market in Japan is showing signs of bottoming out. Profit contributions from PMI attributable to M&A activities undertaken in the previous fiscal year are expected to become apparent this fiscal year.

The dividend is expected to be 46.00 yen per share, up 0.94 yen per share from the previous fiscal year. The expected dividend payout ratio is 32.0%.

6. Conclusions

The company recognizes its cost of equity as 5.3%. From the perspective of equity spread, ROE (14.0% for the fiscal year ended June 2025) is much higher than the cost of equity, but PBR is less than 1. Regarding this matter, in the updated “Measures for Achieving Management Focusing on Capital Costs and Stock Prices,” they noted that “PBR has not improved, reflecting the reality that the gain on negative goodwill through M&A boosted net profit,” and that “the outcome of M&A (= sales growth) has not been reflected in the stock price.” The company therefore believes that profit improvement through PMI is required to offset the impact of decline in the imported car market.

For the fiscal year ending June 2026, they are expected to increase operating income by 26% despite a slight increase in sales. The company expects the profit contribution from PMI to become evident this fiscal year and to continue steadily.

<Reference: Regarding Corporate Governance>

◎ Organization type, and the composition of directors and auditors

Organization type | Company with audit and supervisory committee |

Directors | 8 directors, including 5 outside directors (5 of which are independent executives) |

Audit committee members | 5 members, including 5 outside directors (5 of which are independent executives) |

◎ Corporate Governance Report

Last update date: September 25, 2025

<Basic Policy>

Our company’s basic approach on corporate governance is to establish a sound management system that can respond to rapid changes in society and is efficient and compliant with laws and regulations, for maximizing our corporate value. To achieve this, we continue to strive to ensure transparent management and appropriate and prompt disclosure, by strengthening our relationships with stakeholders and further enhancing management governance functions.

<Reasons for Non-compliance with the Principles of the Corporate Governance Code (Excerpts)>

Our company follows all principles of the Corporate Governance Code.

<Disclosure Based on the Principles of the Corporate Governance Code (Excerpts)>

■Principle 1-3: Fundamental Capital Policy

Our fundamental capital policy is to maintain an appropriate capital base, consistently achieve an ROE that exceeds our cost of capital, and enhance corporate value.

Detailed information regarding our efforts to manage the company with a focus on our cost of capital and share price is disclosed on our company website.

https://contents.xj-storage.jp/xcontents/AS01236/c344ad3a/f422/40ec/9afb/9d116046c9e6/140120250814541929.pdf

■ Principle 1-4 [Strategic Shareholding]

(1) Policies concerning strategic shareholding

Our company does not hold shares strategically. Unless such shareholding is necessary to maintain and strengthen relationships for capital tie-ups and collaboration with our business partners and it is determined that their business benefits are worth the risk and cost of capital from the medium/long-term perspective, we shall adhere to our company’s policy of not holding shares strategically.

(2) Review process concerning strategic shareholding, and criteria for exercising voting rights related to strategically held shares

If it is considered appropriate to hold shares strategically, we will establish a method to review the reasonableness of continued holding of such shares as well as specific criteria for the exercise of voting rights on such shareholding.

■ Supplementary Principle 2-4 ① [Ensuring Diversity in Appointment of Core Personnel, etc.]

< Our view on ensuring diversity >

Our company aims to provide an environment where every and each staff member can utilize their ability to the maximum extent, and our basic policy is to promote human resources based on individual ability, aptitude, achievements and motivation, regardless of gender, nationality and attributes.

<Voluntary and measurable targets for ensuring diversity>

Regarding ensuring the diversity of core human resources, we have set targets for the ratio of female directors and managers and the ratio of male employees who have taken childcare leave, which serve as indices for ensuring diversity. The targets and results for each category are shown in the chart below.

| Result in FY 6/25 | FY 6/30 (target) |

Ratio of female directors | 12.5% | 30.0% |

Ratio of female managers | 7.1% | 10.0% |

Ratio of male employees who have taken childcare leave | 41.7% | 50.0% |

*As of the date on which this report was submitted, the ratio of female directors was 12.5%.

We have not set concrete numerical targets for the promotion of foreigners to managerial positions as there are few employees of foreign nationality at our company, but we shall keep discussing the necessity of setting such targets for ensuring further diversity.

Furthermore, as the proportion of highly specialized and experienced mid-career recruits is high in our corporate group, mid-career recruits account for 96.1% of managers (as of the end of June 2025). We have therefore not set any targets for the ratio of mid-career recruits in managerial positions.

■ Supplementary Principle 3-1 ③ and Supplementary Principle 4-2 ② [Issues related to Sustainability]

Our company has formulated basic sustainability policies, and established a Sustainability Committee and a Risk Management Committee to strengthen our corporate group’s sustainability initiatives and proactive risk management platform, and to focus on expanding our business scope by promoting growth strategies, responding to technological innovations including EVs in the automotive industry, and promoting DX, in order to achieve a sustainable society and enhance corporate value through our corporate activities. Details concerning concrete activities centered on these committees and investments in human capital, etc. for elevating the corporate value in the medium/long term are disclosed in our financial results presentation materials, annual security reports, etc.

https://contents.xj-storage.jp/xcontents/AS01236/73a1773f/f10e/4676/be8e/00e6a0e3b739/140120250827548317.pdf

In addition, our efforts to address climate change issues are disclosed through CDP.

For details, please refer to the “Sustainability” section on our company website.

https://www.willplus.co.jp/sustainability/

■ Principle 5-1 [Policies concerning the establishment of a system to promote constructive dialogue with shareholders and the initiatives for it]

Our company believes that clearly explaining our management policies and growth strategies to shareholders and institutional investors and deepening their understanding through active and constructive dialogue (interviews) with them will contribute to enhancing our company’s medium/long-term corporate value.

Dialogue with shareholders and institutional investors is conducted reasonably through visits, office visits, telephone calls, etc. by representative directors and IR staff, with the IR Office of the Corporate Strategy Division as a point of contact. In addition to individual interviews, in order to provide opportunities for direct dialogue with many investors, our company holds financial results briefings for investors and analysts as well as briefings for individual investors at which representatives themselves give explanations, and uses such opportunities to promote mutual understanding between our company and investors. Furthermore, we broadly disseminate information by video streaming of the meetings or posting material on our website.

When engaging in dialogue, we take all necessary precautions to ensure that there is no leakage of unpublished important information.

This report is not intended for soliciting or promoting investment activities or offering any advice on investment or the like, but for providing information only. The information included in this report was taken from sources considered reliable by our company. Our company will not guarantee the accuracy, integrity, or appropriateness of information or opinions in this report. Our company will not assume any responsibility for expenses, damages or the like arising out of the use of this report or information obtained from this report. All kinds of rights related to this report belong to Investment Bridge Co., Ltd. The contents, etc. of this report may be revised without notice. Please make an investment decision on your own judgment. Copyright(C) Investment Bridge Co., Ltd. All Rights Reserved. |