Bridge Report:(3909)Showcase Second quarter of fiscal year ending December 2021

![]()

President Toyoshi Nagata | Showcase Inc. (3909) |

|

Company Information

Exchange | 1st section of Tokyo Stock Exchange |

Industry | Information and Communications |

President | Toyoshi Nagata |

Address | 14th Floor, Roppongi First Building, 1-9-9, Roppongi, Minato-ku, Tokyo |

Year-end | End of December |

Homepage |

Stock Information

Share Price | Number of Shares issued | Total Market Cap | ROE (Actual) | Trading Unit | |

¥633 | 8,561,900 shares | ¥5,419 million | 1.7% | 100 shares | |

DPS (Est.) | Dividend Yield (Est.) | EPS (Est.) | PER (Est.) | BPS (Actual) | PBR (Actual) |

¥6.50 | 1.0% | ¥4.20 | 150.7 x | ¥253.56 | 2.5 x |

*The share price is the closing price on August 20. Shares outstanding, DPS and EPS are taken from the brief financial report for the second quarter of FY ending December 2021. EPS is at the lower end of the forecast range. ROE and BPS are the results in the previous term.

Earnings Trends

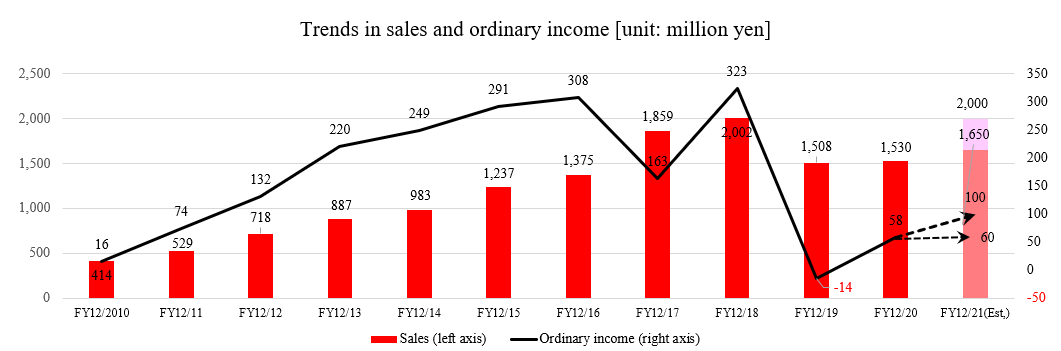

Fiscal Year | Net Sales | Operating Income | Ordinary Income | Net Income | EPS | DPS |

December 2017 Act. | 1,859 | 191 | 163 | 12 | 1.79 | 5.50 |

December 2018 Act. | 2,002 | 352 | 323 | 16 | 2.48 | 0.00 |

December 2019 Act. | 1,508 | 92 | -14 | -183 | -27.02 | 5.50 |

December 2020 Act. | 1,530 | 45 | 58 | 25 | 3.75 | 6.00 |

December 2021 Est. | 1,650~2,000 | 60~100 | 60~100 | 36~60 | 4.20~7.01 | 6.50 |

*Unit: million yen, yen. Net income is profit attributable to owners of the parent. Hereinafter the same shall apply.

This report outlines Showcase Inc.’s earnings results for the second quarter of fiscal year ending December 2021.

Table of Contents

Key Points

1. Company Overview

2. Second Quarter of Fiscal Year Ending December 2021 Earnings Results

3. Fiscal Year Ending December 2021 Earnings Forecasts

4. Conclusions

<Reference 1: Mid-term Growth Strategy>

<Reference 2: Regarding Corporate Governance>

Key Points

- Based on their core value, “Make People Happy with Our OMOTENASHI (Hospitality) Technology,” the company operates business, with a focus on development and provision of cloud-type SaaS systems from the viewpoint of users. The company has set up the term ended Dec. 2019 as the “Second Start-up” period. It upholds their new business concept, “DX cloud service that connects companies and customers,” and supports enterprises in promoting DX. Its strengths include an excellent customer base, plenty of SaaS development technologies with operation knowledge, and high customer satisfaction level.

- The sales in the cumulative second quarter of the term ending Dec. 2021 were 730 million yen, up 8.5% year on year. The sales of the SaaS Business, which is the mainstay, increased. The Cloud Integration Business contributed as well. The sales of the Advertising/Media Business decreased. An operating loss of 67 million yen was recorded. While gross profit also increased due to the growth in sales, SG&A augmented 16.6% year on year as active investment was made in development, advertising, personnel cost, etc.

- There is no change to the earnings forecasts for the term ending Dec. 2021, where the increase in sales and profit is projected. Considering the large impact of new businesses on revenues, the estimates are indicated with ranges, but sales are expected to grow, and operating income is estimated to rise by double digits even for the lowest values of the forecasted ranges. While a deficit is projected during the term, there will be business opportunities to recoup a portion of investments in the second half of the term, and full-year performance will be in the black. Significant increases in both sales and profit are anticipated due to intensive investments in commodities and services for markets with a substantial growth potential. However, the forecast for profit is conservative as investments in human resources and advertising will be enhanced. In addition to the release of Digital Input, the first joint development project with AI inside Inc. mentioned above, the release a new platform service to promote DX, and plans to form business alliances with leading sales partners,etc. are scheduled for the second half of the term. They are planning to pay a dividend of 6.50 yen/share, up 0.5 yen/share year on year. The estimated payout ratio is 92.7% to 154.8%.

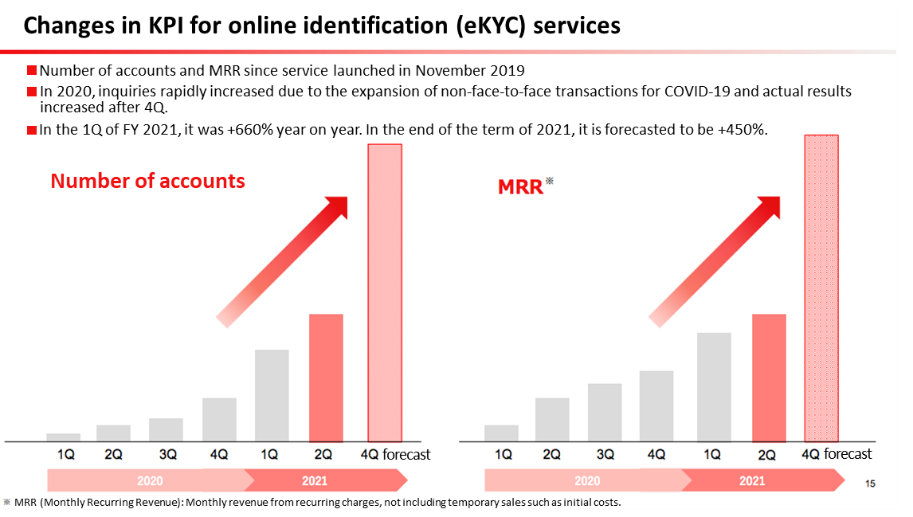

- The online identification (eKYC) service, which is the company’s growth engine, is growing favorably. The number of inquiries rapidly rose due to the increase of non-face-to-face transactions caused by the COVID-19 crisis in 2020, and the number of accounts and Monthly Recurring Revenue (MRR) set as KPIs show a rapid growth after the start of this year as well. The MRR at the end of the term ending Dec. 2021 is estimated to rise 450% year on year. The growth of MRR, which does not include temporary sales such as the initial costs, will lead to the stabilization of the revenue base as well as the improvement of profitability.

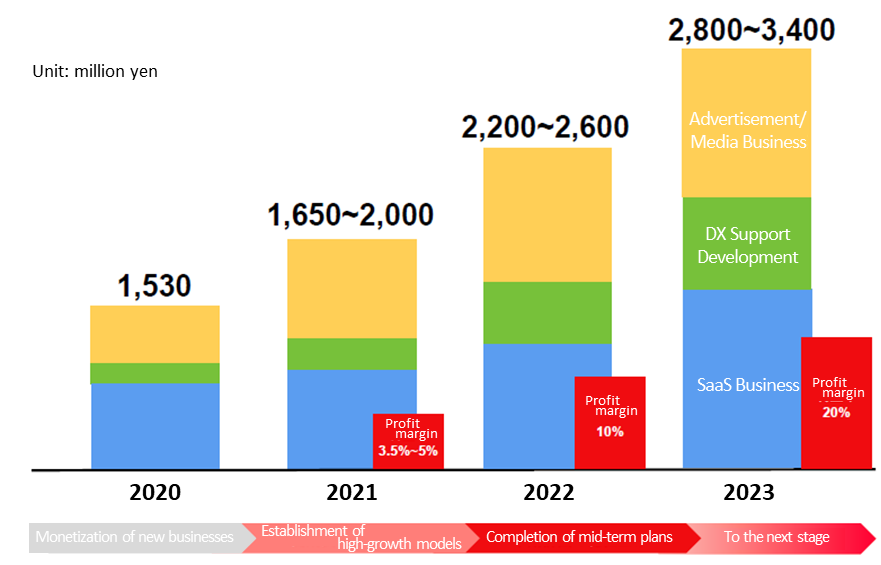

- While checking the quarterly trends toward achieving the forecast for the current fiscal year, we will also check whether the various measures will progress as expected toward the sales target of 2.8 to 3.4 billion yen and a profit margin of 20% in the term ending Dec. 2023 as set in the mid-term management strategy, and whether the products and services listed in the time schedule will be released as planned.

1. Company Overview

Based on the core value, “Make People Happy with Our OMOTENASHI (Hospitality) Technology,” Showcase Inc. operates business, with a focus on development and provision of cloud-type SaaS systems from the viewpoint of users. The company has set up the term ended Dec. 2019 as the Second Start-up period, it upholds the new business concept, “DX cloud service that connects companies and customers,” and supports enterprises in promoting DX. Its strengths include the excellent customer base, plenty of SaaS development technologies and operation knowledge, and high customer satisfaction level.

【1-1 Corporate History】

In 1996, Futureworks CORP was established for the purpose of supporting sales promotion and public relations activities. In 1998, it was reorganized into a joint stock company, and in 2005, it absorbed Smart Image Inc., which engaged in promotion utilizing the Internet, Web videos, etc. with Futureworks Co., Ltd. being the surviving company, for the purpose of expanding business and improving the efficiency of use of managerial resources, and the corporate name was renamed to Showcase-TV Inc. The company changed its business model from the commissioned production of sales promotion goods for marketing to the creation of original products and services.

Meanwhile, the Web Form Optimization service, Form Assist, which is the current core service developed with reference to the clients’ opinions, was highly evaluated. At first, it was adopted mainly by EC sites, real estate firms, etc., but the number of financial institutions that consider Showcase’s high-level system for maintenance and operation as attractive increased, and formed the current stable customer base. As a result, its business performance grew steadily, and it was listed in Mothers of Tokyo Stock Exchange in 2015, and then listed in the first section of TSE in 2016.

However, the policy for diversification of business through M&A, which was adopted in 2015, did not generate assumed synergetic effects, and sales dropped significantly, and impairment loss was posted in the first quarter of the term ended Dec. 2019. In this situation, that term was defined as the Second Start-up period, and Mr. Toyoshi Nagata, who had led business as vice-president since the inauguration of business, was appointed as representative director and president in March 2019. It was renamed to Showcase Inc., while conducting organizational reform to shift to a new business execution system in April 2019.

【1-2 Corporate Philosophy, etc.】

Its core value is “Make People Happy with Our OMOTENASHI (Hospitality) Technology.”

Since its business start-up, the company has been offering business services focused on users’ happiness by using easy-to-adopt, easy-to-use, hospitality-oriented technologies, with the aim of solving problems and creating value from the users’ viewpoint.

For the Second Start-up, the company started upholding “DX cloud service that connects companies and customers” as a new business concept in 2020, and clearly reports its business domains to investors.

【1-3 Market Environment】

(1) The DX market, which is expected to grow rapidly, and the 2025 Digital Cliff

According to “Digital Transformation: Overcoming of ‘2025 Digital Cliff’ Involving IT Systems and Full-fledged Development of Efforts for Digital Transformation” (Study Group for Digital Transformation) announced by the Ministry of Economy, Trade and Industry in September 2018,

“There have emerged new entrants with unprecedented business models based on new digital technologies in all kinds of industries, and drastic change is upcoming. In this situation, each enterprise is required to conduct digital transformation (DX) quickly, to maintain and enhance competitiveness.” Meanwhile, the following problems have been pointed out:

☆ | Since existing IT systems are closely linked to business processes, it is necessary to renew the business processes to solve the problems with the existing systems. Accordingly, on-site workers are reluctant. |

☆ | Unless the problems with existing IT systems are solved, it is impossible to create new businesses and reform business models swiftly. Namely, it is difficult to carry out DX on a full-scale basis. |

☆ | A lot of funds and human resources are allocated to the operation and maintenance of existing systems, so it is impossible to allocate resources to IT investments for utilizing new digital technologies. |

☆ | If this problem is left unaddressed, the costs for operation and maintenance will skyrocket further, the so-called technical debt will augment, the staff who can operate and maintain existing systems will become scarce, and security risk will increase. |

Especially, if existing systems that are complicated, decrepit, and obscure remain, the economic loss due to the rise in risk caused by the resignation of IT personnel, the termination of support, etc. by 2025 is estimated to reach up to 12 trillion yen/year (about 3 times today’s loss) in 2025 or later. This is called the problems with the existing IT systems, the 2025 Digital Cliff.

If many enterprises work on DX to survive, the DX market will grow rapidly, but the growth of service vendors depends on whether they can offer services and solutions for overcoming the 2025 Digital Cliff.

(Taken from the reference material of the company)

(2) eKYC, which is expected to grow steeply

As the demand from housebound consumers grew amid the COVID-19 pandemic, we have entered the age of online cashless payment, and eKYC, which is a tool for online non-face-to-face identification, is rapidly distributed.

eKYC stands for electronic Know Your Customer, meaning online identification.

In order to prevent international money laundering and disrupt the provision of funds to criminal organizations, such as drug rings and terrorists, financial institutions, etc. are obligated to identify customers and check their purposes of transactions when their accounts are created, in accordance with the Act on Prevention of Transfer of Criminal Proceeds.

The damage due to illegal remittance amounted to about 2.5 billion yen in fiscal 2019, so financial institutions were requested to check transactions more strictly.

On the other hand, for non-face-to-face identification using conventional mails, the following problems have been pointed out:

* | Necessity to submit documents by mail for each financial institution is causing 1.7 million people per year to give up creating an account in the middle. |

* | The identification process at financial institutions is cumbersome, and its cost amounts to about 2 trillion yen per year. |

* | Japanese financial institutions bear the cost of about 4 billion yen per year for sending receiver-specified mails to identified customers. |

* | Even after creating accounts, customers need to log in to respective financial institution’s websites with different IDs when making transactions. |

The current identification process is not convenient for users, extremely costly for financial institutions, and many opportunities are lost. Accordingly, the identification process needs to be swifter and more efficient, thus, eKYC is rapidly distributed.

Through the amendment to the Act on Prevention of Transfer of Criminal Proceeds in November 2018, The Method for Checking Items for Identifying an Individual Online, in which each user sends identification documents and their images via the Internet, was added. Until 2023, both the conventional identification method using paper and the online one can be used, but from 2023, online identification will become mandatory.

It will become unnecessary to send identification documents by mail, so the identification process will become convenient for users and less costly for financial institutions. Accordingly, eKYC will become more common.

Since identification is not just for financial field, but also for other various fields, online identification is expected to become common in the fields of insurance, credit cards, communications carriers, trade of antiques (recycling), etc.

The unauthorized access incident at a leading communications carrier that occurred in 2020 could have been prevented with online identification, so it is likely that online identification will be popularized rapidly before 2023.

According to the company’s reference material, the market scale of the eKYC service will expand from 480 million yen in 2019 to 4.4 billion yen by 2024. Substantial growth with an average yearly growth rate of 55.8% is anticipated.

【1-4 Business Contents】

(1) Business form

Utilizing the SaaS development technology with high usability, the company offers high-value services to eliminate the insufficiencies in society.

In addition, under the new business concept, “DX cloud service that connects companies and customers,” the company develops SaaS and platforms around interfaces connecting enterprises and customers and supports DX for co-creation, to offer services for overcoming the 2025 Digital Cliff.

(2) Business segment

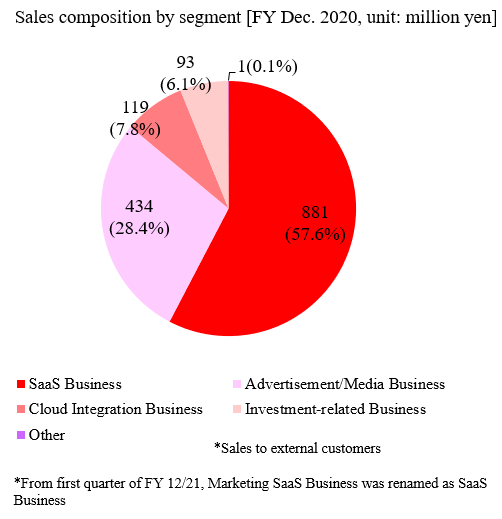

There are four segments to be reported: SaaS Business, Advertisement/Media Business, Cloud Integration Business, and Investment-related Business.

Cloud Integration Business is a new segment established in the term ended Dec. 2020, under the new business concept.

In the first quarter of the term ending Dec. 2021, the reported segment previously titled Marketing SaaS Business was renamed as SaaS Business in response to changes to organizational names.

① SaaS Business

It offers mainly Form Assist, which is a cloud service for increasing conversion rate based on the website optimization technology, and ProTech Series, which is a cloud service related to security.

◎ Form Assist

Administrators of websites for offering services, including EC sites, hope that visitors to their websites (potential customers) will not only browse their contents, but also input their personal information, send an inquiry, and purchase their products or services. They need to avoid a case in which a user accesses an Web form, but leaves the webpage because of the difficulty or cumbersomeness of inputting.

A measure for reducing such opportunity loss cases and increasing the ratio of customers who fill in forms for maximizing the results is called Web Form Optimization.

Form Assist is the first Web Form Optimization tool released by the company in Japan.

It has been adopted for over 5,000 forms, meeting various needs. The company offers original knowledge based on the accumulation of experience for over 10 years.

Among financial institutions, which are their major clients, leading megabanks, local banks, non-life insurance companies, etc. have installed it. It boasts the largest share in the financial Web Form Optimization market.

(Taken from the reference material of the company)

Introduction of more than 30 assisting functions to make form inputs more user-friendly. Plus other dedicated functions designed to change the look and feel of existing Web forms with absolutely no need of any major overhaul within the website. Pasting a single tag is the only thing needed. In addition to the ease of use, easy installation thanks to the fact that Showcase does not need access to personal information is a major benefit for financial institutions in particular.

Last but not least, our dedicated staff with extensive web marketing knowledge will analyze your website for better conversion, clarify issues, and provide you with measures to meet your customer's goals based on our accumulated successes and failures that no other company can offer.

The conversions rates of the companies that have implemented this service have improved steadily on average, and especially for companies that are not familiar with UI betterment, it has led to a 10% improvement and even more in some cases.

Many major financial institutions have their own development companies, and although these development companies may compete with each other in the adoption of Web form optimization, they lack the know-how in web marketing which gives a great competitive advantage to Showcase.

(Taken from the reference material of the company)

◎ Online identification/eKYC tool, ProTech ID Checker

ProTech Series is a cloud service for maximizing the benefits of orders from customers. It specializes in the prevention of unauthorized logins to websites, impersonations, losses of leads due to typing errors and such, fortification of security in general.

In addition to License Reader, which allows users to take a picture of their driver's license with their smartphone and automatically insert their personal information in form inputs using OCR technology, the company is focusing on expanding sales of ProTech ID Checker, an online identity verification/eKYC tool released in 2019, as a future growth driver.

As mentioned in the Market Environment section, eKYC is expected to be adopted not only by financial institutions but also by a wide range of industries and business categories.

The company's "ProTech ID Checker" also allows users to complete online identity verification by simply taking a photo of themselves and their identification documents.

Like the web form optimization service, it is easy to install, requiring only the embedding of a tag. The service is attracting attention as a solution to the rapidly growing need for non-face-to-face transactions due to the spread of the new Coronavirus infection and the social problem of identity fraud.

Although the full-scale introduction of this service has started in 2020, the number of companies introducing it is increasing in a wide range of industries as demand for non-face-to-face and online transactions increases.

As of the beginning of 2021, the number of installations has already surpassed the number of installations for the entire year of 2020, and it is expected to contribute to both sales and profits from the term ending Dec. 2021.

(Taken from the reference material of the company)

Currently, the company provides two types of services: "ProTech ID Checker", which is compliant with the revised Act on Prevention of Transfer of Criminal Proceeds, and "ProTech ID Checker Type S", which is an ID-authentication-by-selfie type of service. In March 2021, the company released "ProTech AI Masking," which provides automatic masking of insurance cards during identity verification. And in May 2021, was released "ProTech MFA by SMS," a multi-factor authentication service using SMS. The company plans to increase its service lineup in the future.

(Taken from the reference material of the company)

② Advertisement/Media Business

The company operates its own media and offers advertisement-related services.

◎ Operation of its own media

This business is growing, with its major content being the smartphone-related media, bitWave. In addition, the company launched Finance Lab., a financial information media for providing simple-to-understand-information on money. It distributes useful tips regarding credit cards, stock investment, asset operation, insurance, loans, etc. As of August 2021, the number of subscribers to the video media channel has exceeded 30,000.

By utilizing the customer base composed of financial institutions, which was developed through the SaaS Business, the company is striving to increase the revenues from affiliate advertising, such as leading customers to credit-card companies. The company will actively invest in the media business, which is promising and profitable.

(Taken from the reference material of the company)

◎ Advertisement-related service

In addition to adjustable ad-related services, such as NaviCast Ad, which has been offered since before, the company offers a video platform, SHOWCASE Ad, which is compatible with SNS ads and smartphone apps, and so on.

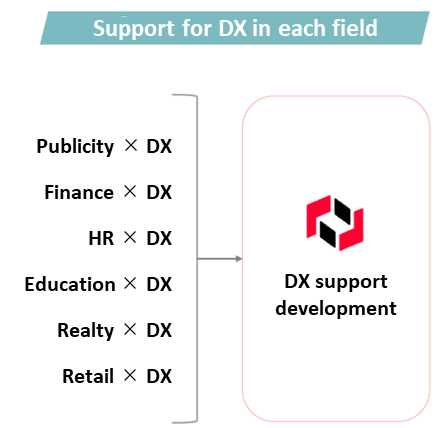

③ Cloud Integration Business

The company operates the DX support and development business by combining the accumulated knowledge to develop SaaS products and the business knowledge of leading companies.

It conducts the SaaS business actively in various fields, and supports enterprises in adopting cloud computing for information systems in the DX market, which is in the midst of a structural reform.

As mentioned in the Market Environment section, the DX market is expected to grow rapidly, as many companies will work on DX to survive. But the “2025 Digital Cliff “ still needs to be dealt with.

The company plans to use the technology and know-how it has cultivated to date to release a platform that will greatly reduce the time and efforts required by corporate system staff involved in DX, thereby contributing to the promotion of DX by corporations and local governments.

(Taken from the reference material of the company)

(Concrete measure (1): To support DX in the fields of publicity and PR)

PR Automation, a public relations automation system operated by PRAP node, Inc., a joint venture with PRAP Japan, Inc. (JASDAQ market of TSE: 2449), was adopted by more than 60 major companies within a month of its release in September 2020. The company is expanding its support for DX in the advertising/PR industry by developing additional functions.

(Concrete measure (2): To support DX in the financial field)

The Bank of Yokohama has developed a cloud-based system for confirming the contractual details of its loans, allowing customers to check the details online.

④ Investment-related Business

Consolidated subsidiary Showcase Capital Inc. operates SmartPitch, a matching platform service that matches startups with operating companies, venture capital firms, and corporate venture capital firms online. As of August 2021, there are more than 250 registered startups and more than 100 investors, including operating companies.

In addition, the company is a supporter of J Startup, a program promoted by the Ministry of Economy, Trade and Industry to support the development of start-up companies, and is collaborating with local governments to support regional development through entrepreneurship.

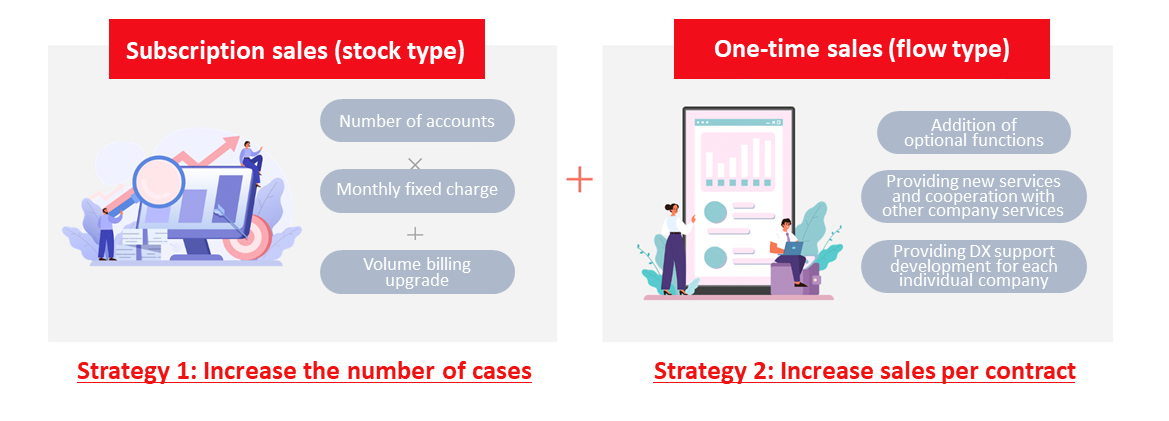

(3) Revenue model

The SaaS Business is based on a business model of earning revenues from the pay-as-you-go service in addition to monthly charges.

(Taken from the reference material of the company)

KPIs are sales per contract and the number of contracts. The following measures are taken for each KPI.

KPI | Measures |

To expand sales per contract | * To offer optional functions * To provide new services and services linked with other companies * To support DX * To expand the pay-as-you-go model |

To increase the number of contracts | * To enhance digital marketing * To increase sales via partners * To promote regional business operations * To sell products in other fields |

【1-5 Characteristics and Strengths】

(1) Excellent customer base

The excellent customer base composed of a total of over 8,000 customers, mainly financial institutions, which was developed through the SaaS Business, has high value as an intangible asset from the viewpoint of reliability. In addition, it led to the monetization of financial media in the Advertisement/Media Business.

(2) High customer satisfaction level thanks to plenty of SaaS development technologies, operation knowledge, and customer-oriented policy

The company has accumulated plenty of SaaS development technologies and operation knowledge. As the company develops products that meet customer needs speedily and offers high-quality products at low cost under the customer-oriented policy, the company is highly evaluated by customers and has a great competitive advantage.

Based on this advantage, it supports the DX in enterprises and governments through the newly launched Cloud Integration Business.

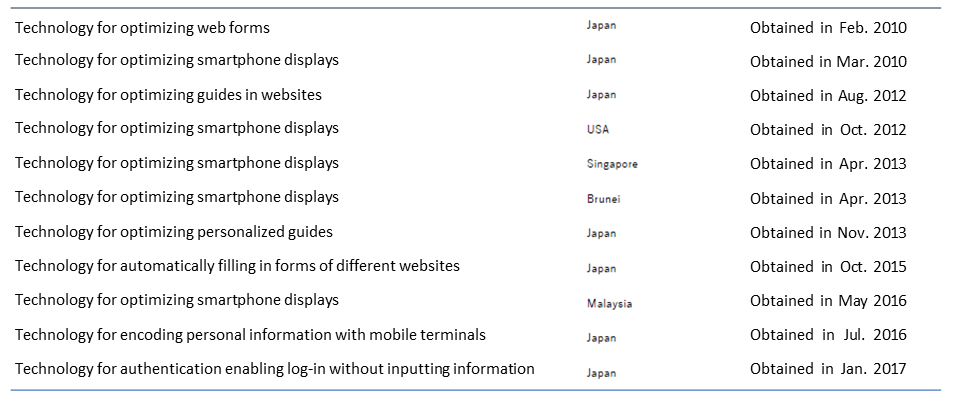

(3) Holding a lot of technological patents

Showcase holds a lot of patents in Japan, the U.S., Singapore, etc.

At present, patents for identification system programs, etc. of ProTech ID Checker are pending.

It will actively develop technologies with the aim of acquiring technological patents.

(Taken from the reference material of the company)

【1-6 Business Strategy】

With the above product lineup and competitive advantage, Showcase aims to increase sales and profit with the following three growth engines.

◎Growth engine I 【Identification (eKYC) service】

While the social situation is changing rapidly as mentioned above, the company aims to promote this service while advertising its simplicity of adoption.

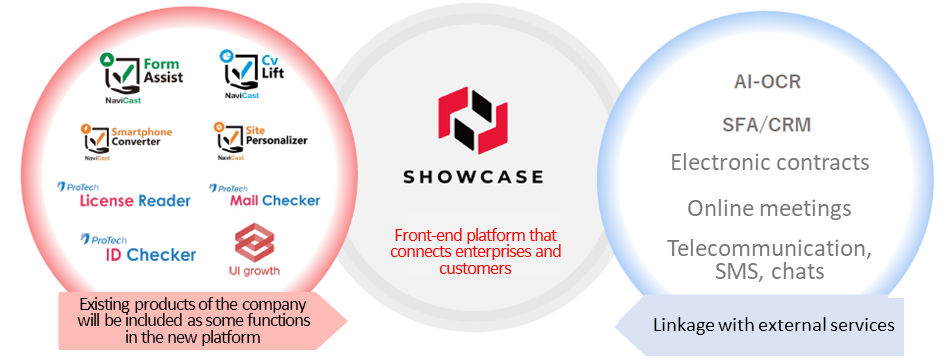

◎ Growth engine II 【New platform scheme】

The company will operate a new front-end platform for offering inlet of all kinds of data.

By linking its core technologies and patented technologies, SaaS development knowledge, and identification technologies with leading enterprises and services, the company will connect users and clients, and increase corporate users.

(Taken from the reference material of the company)

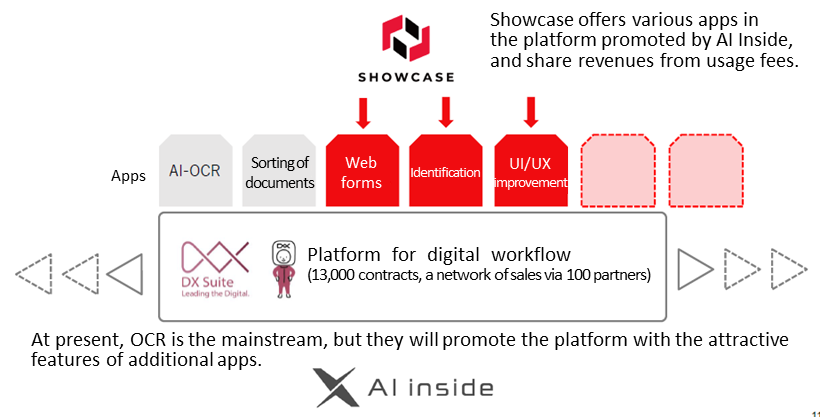

◎ Growth engine III 【Capital and business tie-ups with AI inside Inc.】

(For details, please refer to (4) Topics in Section 2. Fiscal Year December 2020 Earning Results)

By utilizing the strengths of the two companies, it aims to offer new value to society and improve the corporate value of both companies, through mutual use of technological knowledge, mutual sales of services, and collaborative product development.

(Taken from the reference material of the company)

In detail, Showcase offers various apps in the platform promoted by AI inside, and shares revenues from usage fees.

(Taken from the reference material of the company)

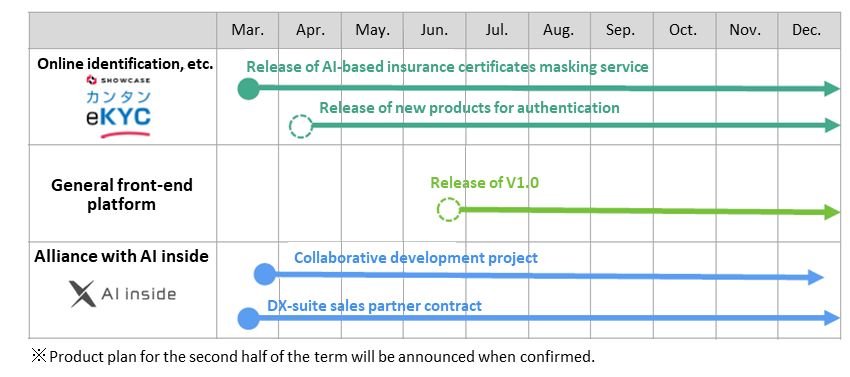

The release schedule of each growth engine is as follows:

(Taken from the reference material of the company)

【1-7 Return on Equity (ROE) Analysis】

| FY 12/16 | FY 12/17 | FY 12/18 | FY 12/19 | FY 12/20 |

ROE (%) | 14.8% | 1.0% | 1.4% | -17.2% | 1.7% |

Net income margin [%] | 12.86 | 0.65 | 0.84 | -12.14 | 1.69 |

Total asset turnover [times] | 1.02 | 0.92 | 0.78 | 0.63 | 0.59 |

Leverage [times] | 1.13 | 1.62 | 2.14 | 2.24 | 1.66 |

Although the company does not own a lot of assets, ROE has been low, because profitability and efficiency of assets are low.

In the mid-term management strategy, the company aims to achieve an operating income margin of 20% in 2023. The improvement in ROE depends on whether the company will be able to increase profitability by promoting eKYC tools and expanding the DX support business.

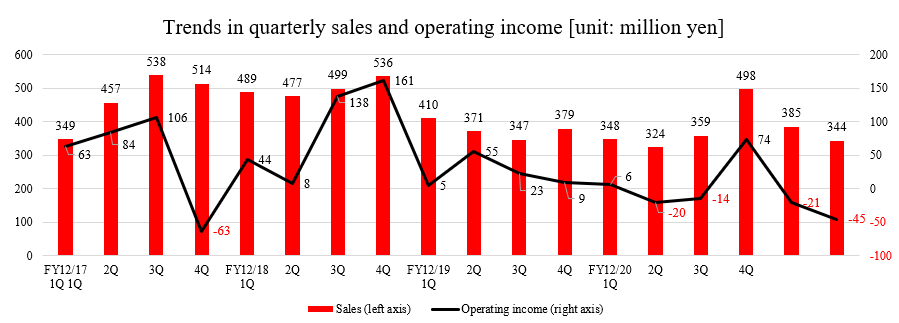

2. Second Quarter of Fiscal Year Ending December 2021 Earning Results

(1) Overview of consolidated business results

| FY 12/20 2Q (Accumulated) | Ratio to sales | FY 12/21 2Q (Accumulated) | Ratio to sales | YoY |

Sales | 672 | 100.0% | 730 | 100.0% | +8.5% |

Gross profit | 510 | 75.9% | 544 | 74.5% | +6.6% |

SG&A | 524 | 77.9% | 611 | 83.7% | +16.6% |

Operating Income | -14 | - | -67 | - | - |

Ordinary Income | -7 | - | -34 | - | - |

Quarterly Net Income | 17 | 2.7% | -36 | - | - |

*Unit: million yen. Quarterly net income means profit attributable to owners of parent.

Sales grew, while operating income declined

The sales in the cumulative second quarter of the term ending Dec. 2021 were 730 million yen, up 8.5% year on year. The sales of the SaaS Business, which is the mainstay, increased. The Cloud Integration Business contributed as well. The sales of the Advertising/Media Business decreased. An operating loss of 67 million yen was recorded. While gross profit also increased due to the growth in sales, SG&A augmented 16.6% year on year as active investment was made in development, advertising, personnel cost, etc.

(2) Trend in each segment

| FY 12/20 2Q | Composition ratio | FY 12/21 2Q | Composition ratio | YoY |

SaaS Business | 437 | 65.1% | 460 | 63.1% | +5.3% |

Advertisement/Media Business | 213 | 31.7% | 202 | 27.7% | -5.1% |

Cloud Integration Business | 21 | 3.1% | 60 | 8.3% | +186.9% |

Investment-related Business | - | - | 5 | 0.8% | - |

Other | 0 | 0.1% | 0 | 0.1% | -16.7% |

Total sales | 672 | 100.0% | 730 | 100.0% | +8.5% |

SaaS Business | 297 | 67.9% | 296 | 64.4% | -0.2% |

Advertisement/Media Business | 26 | 12.2% | 18 | 9.2% | -28.6% |

Cloud Integration Business | -8 | - | -15 | - | - |

Investment-related Business | -13 | - | -8 | - | - |

Other | -8 | - | 9 | - | - |

Adjustment | -307 | - | -368 | - | - |

Total profit | -14 | - | -67 | - | - |

*Unit: million yen. Sales mean those to external clients. The composition ratio of profit means the ratio of profit to sales. Cloud Integration Business was added as a new segment in the term ended Dec. 2020. In the second quarter of this term, a revision of management units was implemented in step with organizational changes, and some businesses previously included in the Cloud Integration Business have newly been included in the SaaS Business. Incidentally, the segment information in the second quarter of the previous term is also indicated according to the new classification.

⊚ SaaS Business

Sales grew, but profit decreased.

The sales of the core business grew steadily. The online identification (eKYC) service, which is the pillar of growth, continues to expand. The company continued active investments in development, advertising, etc.

⊚ Advertisement/Media Business

Sales and profit dropped.

While the media for smartphone comparison recorded large sales, operating income dropped significantly due to upfront investment in the new media for the comparison of financial instruments.

⊚ Cloud Integration Business

Sales grew and loss increased.

Operating costs augmented, leading to a drop in profit.

⊚ Investment-related Business

Regarding the Smart Pitch, platform for online matching of operating companies, VC, CVC, and start-up companies, the number of registered start-up companies exceeded 250 and the number of investors, such as operating companies, also reached over 100.

(3) Financial position and cash flows

⊚ Main Balance Sheet

| End of December 2020 | End of June 2021 | Increase/ decrease |

| End of December 2020 | End of June 2021 | Increase/ decrease |

Current Assets | 2,477 | 2,328 | -149 | Current Liabilities | 480 | 531 | +50 |

Cash and Deposits | 2,198 | 2,115 | -82 | Trade Payables | 25 | 17 | -7 |

Trade Receivables | 207 | 164 | -43 | ST Interest-bearing Liabilities | 328 | 395 | +66 |

Noncurrent Assets | 472 | 484 | +12 | Noncurrent Liabilities | 298 | 198 | -100 |

Tangible Assets | 85 | 84 | -0 | LT Interest-bearing Liabilities | 253 | 157 | -95 |

Intangible Assets | 125 | 133 | +7 | Total Liabilities | 779 | 729 | -49 |

Investment, Others | 260 | 265 | +4 | Net Assets | 2,170 | 2,082 | -87 |

Total assets | 2,949 | 2,812 | -137 | Total Liabilities and Net Assets | 2,949 | 2,812 | -137 |

|

|

|

| Balance of Interest-bearing Liabilities | 582 | 552 | -29 |

*Unit: million yen.

Cash and deposits and trade receivables decreased, and total assets stood at 2,812 million yen, down 137 million yen from the previous term. There was a drop in long-term interest-bearing liabilities and total liabilities are now 729 million yen, down 49 million yen from the previous term. Due to a decrease in retained earnings, net assets stood at 2,082 million yen, down 87 million yen from the previous term.

Capital-to-asset ratio rose 0.5 points from the end of the previous term to 74.1%.

⊚ Cash Flow

| FY 12/20 2Q | FY 12/21 2Q | Increase/decrease |

Operating Cash Flow | -4 | 14 | +18 |

Investing Cash Flow | -63 | -9 | +53 |

Free Cash Flow | -67 | 4 | +71 |

Financing Cash Flow | -230 | -87 | +143 |

Term End Cash and Equivalents | 1,131 | 2,115 | +984 |

*Unit: million yen

Cash position improved.

(4) Topics

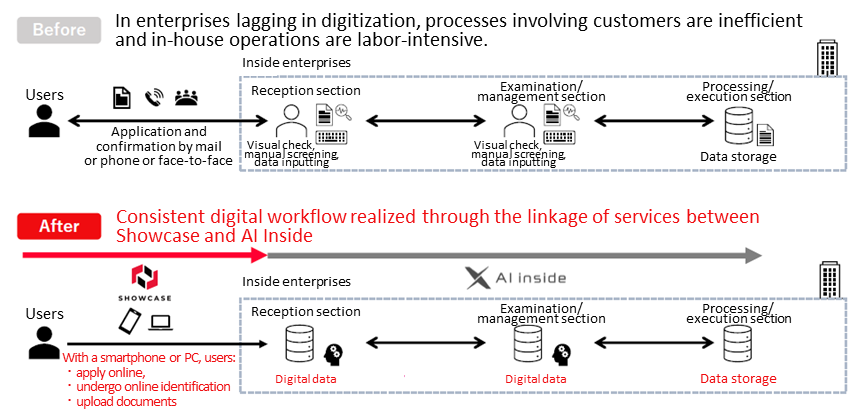

【First joint development project with AI inside Inc.】 Plan to launch the Digital Input service

The company announced the launch of the Digital Input service, which is the first project developed jointly with AI inside Inc. (Mothers of TSE; 4488), the company’s partner for capital and business tie-ups.

The actual release date remains to be determined.

(Outline of Digital Input)

Digital Input is a service that integrates the data entry workflow of web forms and paper forms and streamlines the flow of data.

It is available on Workflows, where AI and applications, such as DX Suite, an AI-OCR provided by AI inside, can be used.

Digital Input is provided as an application free of charge for a limited time period to users who have subscribed to the cloud version of DX Suite.

By utilizing Digital Input, users can integrate the two workflows of data entry read by AI-OCR from paper forms such as order forms, and from web forms as well, thus making it possible to improve work efficiency based on the unified management of information.

Furthermore, web forms are based on the development and operation knowledge of Form Assist, a web form optimization tool, which Showcase perfected over more than 10 years. The interface offers UI/UX allowing easy data input, preventing users from leaving the site.

(Background of joint development)

Japan is ranked 27th in the Global Digital Competitiveness Ranking 2020, and the shift to DX and digitalization of government and domestic companies is not progressing as expected.

Although digitalization has been progressing in recent years, paper-based procedures still remain, resulting in users having to deal with both digital and paper forms, thus creating inefficient data flows under complex workflows.

In order to resolve and reduce this situation, the company has developed "Digital Input" with AI inside, which acquires information from web forms and streamlines the data flow.

(Regarding future developments)

Showcase will continue the joint development with AI inside, with the perspective of the official release of Digital Input.

Moreover, through the business tie-up as well as joint development and sales with AI inside regarding various applications such as eKYC (online identification using face recognition), the company will aim for boosting user acquisition and business expansion, and expects to contribute to the popularization and promotion of a variety of online procedures, which show a rising trend due to the COVID-19 crisis.

3. Fiscal Year December 2021 Earnings Forecasts

Earnings forecasts

| FY 12/20 | Ratio to sales | FY 12/21 Est. | Ratio to sales | YoY | Progress rate |

Sales | 1,530 | 100.0% | 1,650 ~2,000 | 100.0% | +7.8% ~+30.7% | 36.5% ~44.3% |

Operating Income | 45 | 3.0% | 60 ~100 | 3.6% ~5.0% | +31.7% ~+119.6% | - |

Ordinary Income | 58 | 3.8% | 60 ~100 | 3.6% ~5.0% | +1.9% ~+69.9% | - |

Net Income | 25 | 1.7% | 36 ~60 | 2.2% ~3.0% | +38.8% ~+131.4% | - |

*Unit: million yen. The forecast was those released by the company.

There is no change to the earnings forecasts. Sales and profit are estimated to grow.

There is no change to the earnings forecasts for the term ending Dec. 2021. Considering the large impact of new businesses on revenues, the estimates are indicated with ranges, but sales are expected to grow, and operating income is estimated to rise by double digits even for the lowest values of the forecasted ranges. While a deficit is projected during the term, there will be business opportunities to recoup a portion of investments in the second half of the term, and full-year performance will be in the black. Significant increases in both sales and profit are anticipated due to intensive investments in commodities and services for markets with a substantial growth potential. However, the forecast for profit is conservative as investments in human resources and advertising will be enhanced.

In addition to the release of Digital Input, the first joint development project with AI inside Inc. mentioned above, the release of a new platform service to promote DX, and plans to form business alliances with leading sales partners, etc. are scheduled for the second half of the term. They are expected to pay a dividend of 6.50 yen/share, up 0.5 yen/share year on year. The estimated payout ratio is 92.7% to 154.8%.

With the following three growth strategies, the company will accelerate growth.

① Acceleration through the investment in the core business and its growth

The company will increase the investment in online identification and the development of a front platform for solving rapidly augmenting social issues.

The company will develop SaaS systems with leading companies in each field in the growing DX market.

② Acceleration through the active alliance with leading partner companies

The company will form business tie-ups and collaborate with leading enterprises related to DX, such as AI inside Inc.

In addition, it will try to expand the business scale by selling via partners, etc.

③ Acceleration through the M&A strategy for expanding business

M&A is planned to expand the scale of the core businesses, secure excellent engineers, etc.

4. Conclusions

The online identification (eKYC) service, which is the company’s growth engine, is growing favorably. The number of inquiries rapidly rose due to the increase of non-face-to-face transactions caused by the COVID-19 crisis in 2020, and the number of accounts and Monthly Recurring Revenue (MRR) set as KPIs show a rapid growth after the start of this year as well. The MRR at the end of the term ending Dec. 2021 is estimated to rise 450% year on year. The growth of MRR, which does not include temporary sales such as the initial costs, will lead to the stabilization of the revenue base as well as the improvement of profitability.

While checking the quarterly trends for achieving the forecasted performance in this term, we would like to see whether the company will proceed with various measures as expected to reach sales of 2.8 to 3.4 billion yen and a profit margin of 20% in the term ending Dec. 2023 as set in the mid-term management strategy, and whether they will release products and services mentioned in the time schedule as planned.

<Reference 1: Mid-term Growth Strategy>

As the company defined the term ended Dec. 2019 as the Second Start-up period, the term ended Dec. 2020 was the second year of the Second Start-up. From this term, the company set the following mid-term growth strategies for three years until the term ending Dec. 2023.

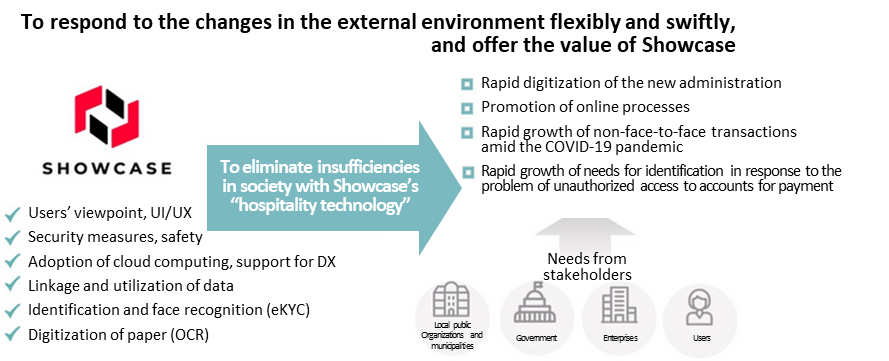

(1) Response to the changes in the external environment

The external environment has changed rapidly through the digitization led by the government, the significant increase of non-face-to-face transactions and online deals in various scenes amid the pandemic, the rapid growth of needs for identification in response to the problem of unauthorized access to accounts for payment, etc. Therefore, new needs emerged from stakeholders, including enterprises, users, governments, and municipalities.

Showcase considers that growth can be achieved by responding flexibly and swiftly to such changes in the external environment and emerging needs and solving social issues by offering its value.

(Taken from the reference material of the company)

(2) Priority strategies

The company puts importance on the following three strategies:

* Improvement in mid-term corporate value and return to shareholders

* Intensive investment in profitable, promising domains

* Active dissemination of information for popularizing the corporate brand

For the core business, the company will reform its business model and aim to expand the business in markets with a high growth rate.

For new businesses, the company will grasp changes in the business environment and establish a revenue structure that can take advantage of its forte.

(3) Envisioned mid-term growth

While the performances of existing services are on plateau, sales declined in the term ended Dec. 2020, due to the COVID-19, but from this term and beyond, the trend will change, thanks to the next growth engines, including eKYC, which was released in 2019. The ARR* of the new service is expected to rise 63% year on year.

The company aims to earn record-high sales and profit in 2022, and achieve sales of 2.8 to 3.4 billion yen in 2023, which is the final fiscal year of the plan, to proceed to the next stage.

The measures and goals for each business are as follows:

Business | Measures and goals |

SaaS Business | To expand the business of new front-end platforms, including eKYC Target operating income margin (2023): 65% |

DX Support Development | To expand development scale and apply the SaaS development knowledge multilaterally. Target operating income margin (2023): 10% |

Advertisement/Media Business | To enhance the investment in financial media, and expand business. Target operating income margin (2023): 30% |

(Taken from the reference material of the company)

*ARR (Annual Recurring Revenue)

It means stable sales earned every year and does not include initial costs, additional purchase expenses, consulting fees, or the like. It is often used in recurring, subscription, and SaaS businesses based on annual contracts. By grasping the variation in ARR, it is possible to check the outlook for the increase, retention, and loss of customers for each business.

<Reference 2: Regarding Corporate Governance>

⊚ Organization type and the composition of directors and auditors

Organization type | Company with company auditor(s) |

Directors | 6 directors, including 3 outside ones |

Auditors | 3 auditors, including 3 outside ones |

⊚ Corporate Governance Report

Last update date: April 9, 2021

<Basic Policy>

Our company considers that establishing corporate governance is one of the important managerial issues to maximize the profits of many stakeholders, including shareholders, and to improve corporate value while enhancing the efficiency and transparency of management.

In this situation, we will observe related laws and regulations and operate a management organization system while responding to the changes in the business environment swiftly and flexibly.

<Reasons for Non-compliance with the Principles of the Corporate Governance Code>

Principle | Reasons |

(Supplementary Principle 3-1-2) | Our company opened the English version of our website to disclose the details of our business around the world. (English website: ) As for material for briefing financial results, convocation notices for general meetings of shareholders, overviews of quarterly results, etc., we will see the trend of ratio of foreign shareholders and consider cost-effectiveness, and if the ratio of foreign shareholders exceeds a certain value, we will consider translating documents and disclosing information in English.https://www.showcase-tv.com/en/corporate/ |

(Supplementary Principle 4-1-3) | Our company recognizes that a plan for appointing successors to CEO, et al. is important for realizing sustainable growth and improving mid/long-term corporate value. As of now, there are no concrete plans, but considering that it is indispensable to train executives and managers who will support the management in order to achieve sustainable growth and improve mid/long-term corporate value, we will comprehensively discuss requirements for becoming a chief executive and other executives, the policy for training them, etc. while taking into account our business environment and climate, and if necessary, we will discuss how the board of directors should supervise business operations. |

(Principle 4-11) | We think that the board of directors should be composed of directors who possess knowledge, experience, and skills for fulfilling their roles and duties with good balance for realizing diversity and appropriate scale. Our board of directors is composed of personnel who possess technical knowledge and plenty of experience in the fields of business administration, financial affairs, marketing, systems, etc., being well-balanced. In addition, our auditors include certified public accountants and tax accountants who possess appropriate knowledge of financial accounting. However, we recognize that there are problems regarding gender diversity and internationality. From now on, we will have discussions for securing female and foreign personnel to be appointed as directors. |

<Disclosure Based on the Principles of the Corporate Governance Code (Excerpts)>

Principle | Description of disclosure |

【Principle 1-4 Strategically Held Shares】 (Supplementary Principle 1-4-1) (Supplementary Principle 1-4-2) | Our company may hold some shares of listed companies, if such shareholding is expected to improve our corporate value in the medium/long term, from the viewpoints of fostering stable, long-term transactions and concreate cooperation in business activities with business partners and alliance partners. We have the basic policy of disposing of or reducing the strategically held shares that are considered to be not worth holding as soon as possible, by considering the situation as of the end of the latest fiscal year. Hence, we will discuss the effects of shareholding from the viewpoints of mid/long-term economic rationality and the maintenance/strengthening of comprehensive relationships with business alliance partners, and the board of directors will pass a resolution. We will exercise the voting rights of the listed shares appropriately after examining the contents of bills at general meetings of shareholders and checking whether the exercise will contribute to the improvement in corporate value and benefits for shareholders. Our company does not have the so-called cross-held shares. |

(Supplementary Principle 4-11-3) | The internal audit division conducts a questionnaire survey every year to directors and auditors, on the composition and operation status of the board of directors, to evaluate the effectiveness of the operation, deliberation, etc. of the board of directors. The evaluation results indicate that the board of directors can exert its supervision function with the current composition, operation, and deliberation systems, and participants in meetings of the board of directors is able to express their opinions actively and to have unfettered discussions. On the other hand, in order to improve the effectiveness of the board of directors further, it is important to enrich information to be offered to directors and auditors. With this recognition, our company will make continuous efforts to increase the effectiveness of the board of directors. |

【Principle 5-1 Policy for Constructive Dialogue with Shareholders】 | The management planning department is in charge of IR, and promotes constructive dialogue with shareholders.The section in charge of IR is developing a system for collecting necessary information for giving explanations to shareholders on a daily basis in cooperation with the corporate headquarters, which manages general affairs, financial affairs, accounting, and legal affairs, to support the dialogue with shareholders.We will strive to enrich the contents of sessions for briefing financial results and giving explanations to investors.The information obtained through the dialogue with shareholders will be reported at the meetings of the management council, the board of directors, etc. and we will give feedback to executives, directors, and auditors.We set the regulations for preventing insider trading, and manage information appropriately and thoroughly. |

This report is intended solely for information purposes and is not intended as a solicitation to invest in the shares of this company. The information and opinions contained within this report are based on data made publicly available by the company and comes from sources that we judge to be reliable. However, we cannot guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness, or validity of said information and or opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration. Copyright(C) Investment Bridge Co.,Ltd. All Rights Reserved. |