Bridge Report:(3937)Ubicom the first half of the term ending Mar. 2021

![]()

President Masayuki Aoki | Ubicom Holdings, Inc. (3937) |

|

Company Information

Exchange | TSE 1st Section |

Industry | Information and communications |

CEO | Masayuki Aoki |

HQ Address | Joko Bldg., 9F, 2-23-11, Koishikawa, Bunkyo-Ku, Tokyo |

Year-end | End of March |

Homepage |

Stock Information

Share Price | Shares Outstanding | Market Cap. | ROE (Act.) | Trading Unit | |

¥3,040 | 11,743,600 shares | ¥35,700 million | 27.3% | 100 shares | |

DPS (Est.) | Dividend Yield (Est.) | EPS (Est.) | PER (Est.) | BPS (Act.) | PBR (Act.) |

TBD | - | ¥51.76 | 58.7x | ¥190.24 | 16.0x |

*The share price is the closing price on November 20. The number of Shares, DPS, and EPS are from the financial results for the first half of the fiscal year ending March 2021. ROE and BPS are the results of the previous fiscal year.

Earnings Trends

Fiscal Year | Net Sales | Operating Income | Ordinary Income | Net Income | EPS | DPS |

March 2017 (Act.) | 2,992 | 237 | 289 | 112 | 10.60 | 0.00 |

March 2018 (Act.) | 3,208 | 322 | 355 | 212 | 19.08 | 0.00 |

March 2019 (Act.) | 3,555 | 564 | 591 | 368 | 32.57 | 5.00 |

March 2020 (Act.) | 4,038 | 707 | 715 | 533 | 46.17 | 5.00 |

March 2021 (Est.) | 4,437 | 807 | 840 | 605 | 51.76 | TBD |

*Unit: million yen, yen.

*Forecasts are those of the company.

*The definition for net income means net income attributable to owners of parent.

This Bridge Report overviews the financial results of Ubicom Holdings, Inc. for the first half of the term ending Mar. 2021.

Table of Contents

Key Points

1. Company Overview

2. The First Half of Fiscal Year ending March 2021 Earnings Results

3. Fiscal Year ending March 2021 Earnings Forecasts

4. Future Growth Strategy

5. Conclusions

<Reference: Regarding Corporate Governance>

Key Points

- In the first half of the term ending March 2021, sales rose 8.8% year on year to 2,093 million yen. Orders and solutions projects mainly for major customers in the global business continued to increase. New product launches in the medical business also contributed to growth. Operating income increased 22.0% year on year to 393 million yen. Although the global business saw a profit decline by 3.6%, due to the COVID-19 pandemic, this was handily offset by contributions from the establishment of a highly profitable subscription model in the medical business. Although gross profit margin fell 1.9% year on year, operating income margin grew 2.0% as SG&A costs decreased 7.3%. Ordinary income rose 12.0% year on year to 377 million yen. When considering the impact from the COVID-19 pandemic (around 25 million yen in costs associated with providing employee transport and the shift to a telework-based development structure in the Philippines, etc.) and exchange rate effects (roughly 20 million yen), profit grew 20%. Both sales and profit reached a record high for the first half.

- The company’s full-year estimates for the term ending March 2021 are unchanged, calling for sales of 4,437 million yen (up 9.9% year on year), an operating income of 807 million yen (up 14.0% year on year), and an ordinary income of 840 million yen (up 17.4% year on year). Profit margins are improving and both businesses continue to perform well. From the third quarter, the company will implement strategic investments in employee training, but is aiming to offset drags on this front to achieve double-digit profit growth. Both operating income and ordinary income are expected to reach a record high for the seventh consecutive term. Dividends are currently undetermined, but the company plans to continue providing appropriate shareholder returns while maintaining a balance between earnings growth and strategic investments.

- In the first half of the term, sales growth remained in the single digits, due partly to the impact from the COVID-19 pandemic, but the company posted double-digit income growth thanks to significant margin improvement in the medical business. The operating income margin for the medical business reached almost 50% on a half-term basis, apparently owing to progress with new customers installing and existing customers switching to “MightyChecker® EX.” The company has not yet disclosed the situation of adoption of “SonaM,” which was launched in April 2020 and is more profitable than the Mighty series, but we look for it to contribute to full-year earnings.

- Our focus is on the speed at which the company taps into the huge market that the company is anticipating with its "Insurance Knowledge Platform,” the first step in its plans to launch new platform businesses over the medium term.

1. Company Overview

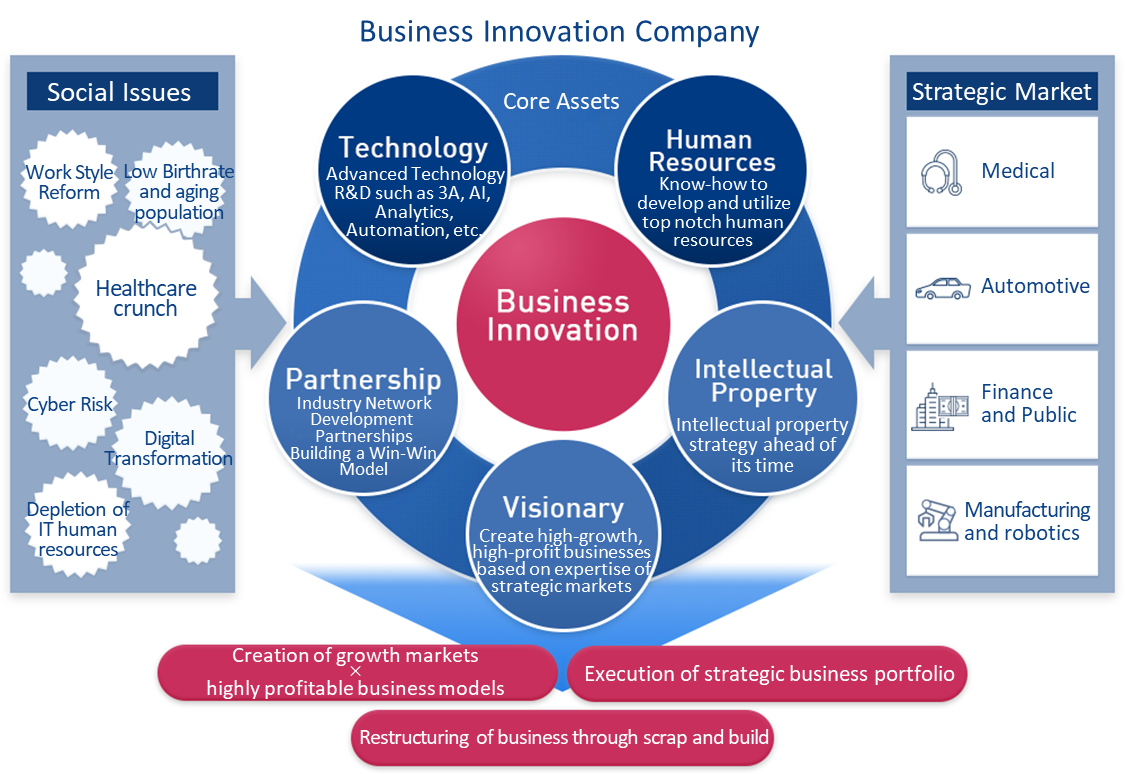

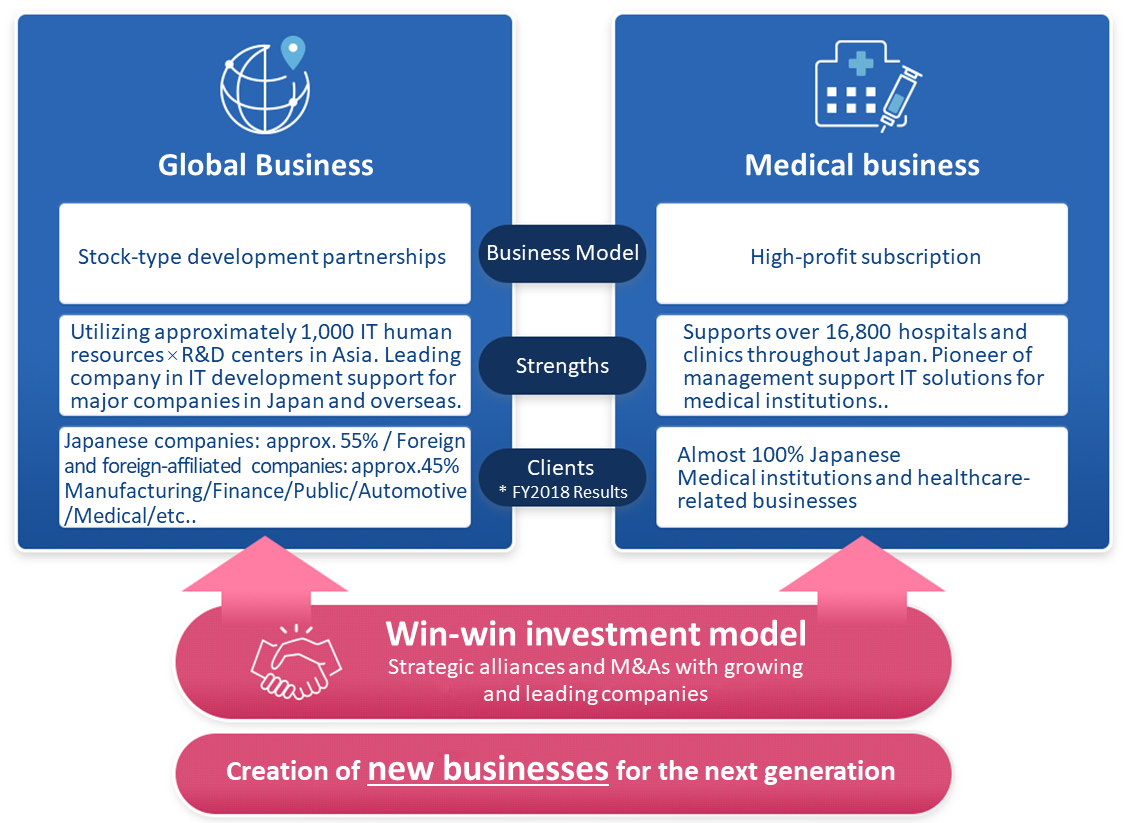

Ubicom Holdings is a one-of-a-kind business innovation company that creates IT solutions to social issues, such as the shortage of manpower and a medical crunch. It recognizes the financial/public, medical, automobile, and manufacturing/robotics markets as strategic markets, and offers a broad range of IT solutions and services.

It has about 1,000 engineers mainly at the development center in the Philippines, and operates two core businesses. One is the global business that solves the shortage of IT personnel and promotes digital transformation (DX) in Japan, by developing software and advanced solutions including AI. The other is the medical business that offers healthcare optimization solutions, such as medical claims inspection, support for medical safety, and cloud services, as a leading company that offers IT solutions for supporting the management of medical institutions. It established a highly profitable business model through business restructuring by implementing scrap and build. Furthermore, the company will promote a win-win investment model for accelerating its business through strategic alliances and M&A with leading companies and burgeoning enterprises, and quickly aims to establish new businesses with different approaches from the existing businesses, such as the platform business.

1-1 Corporate History

Mr. Masayuki Aoki, who had entrepreneurial ambition all along, took the position of President and CEO at WCL Co., which was a new business subsidiary of WORLD CO., LTD. in March 2005, and then found out that there are many young talented engineers who work vigorously in the Philippines when he visited there during his domestic and international search for seeds of various new businesses. As the adoption of IT on internal operations of companies progressed in Japanese companies, he thought that conducting the system development in the Philippines will open the possibilities to offer a wide array of system solutions globally at a low cost and capture the demand, and decided to commercialize the idea. In December 2005, He founded Advanced World Solutions, Ltd. (currently: Ubicom Holdings, Inc.)

Following the trend of ICT adoption, the increase of new customers progressed well, and the business expanded thanks to the competitive advantage of having a development center in the Philippines, which possesses many capable top-class engineers. In 2012, the company acquired AIS Co., Ltd., which is the largest company in the field of systems for medical claims, as a subsidiary. In June 2016, the company was listed on Mothers of Tokyo Stock Exchange. After it changed its name to Ubicom Holdings, Inc. In July 2017, it was listed on the First Section of the Tokyo Stock Exchange in December of the same year.

1-2 Corporate Ethos and Vision

The company advocates the following three management visions as the one and only business innovation company that creates innovative IT solutions combining people and technology.

1. Unique beyond comparison To remain a one-of-a-kind business innovation company that looks ahead to the future and creates IT solutions to social issues |

2. Go Global To use the business scheme of the Ubicom group globally mainly in the U.S. and Asian countries |

3. Win-Win To increase the “fellows” of the Ubicom group, by prospering together with customers, collaboration partners, and all other stakeholders |

Based on five core assets: technology, human resources, intellectual property (IP), foresight, and partnerships, the company creates business innovations aimed at solving issues such as Japan’s aging society, healthcare crunch, a lack of IT personnel, and digital transformation (DX), which it sees as its social responsibility and raison d’être.

(From the company’s website)

1-3 Business Description

1-3-1 Overview

With more than 20 years of experience in embedded software development, application development, testing, and quality assurance services, the company perceives social structure changes such as globalization and the decreasing birthrate and aging population, as well as technological advances in the field of Medical Life Sciences, Cybernetics, and Robotics, as an opportunity to develop new businesses. In the medical, financial/public, automotive, and manufacturing/robotics sectors, which are strategic markets, the company has developed its own core solutions in the field of mainly AI (Artificial intelligence), Analytics and Automation/RPA (Automation of software testing or inspection process of the production line), and is now working to develop and implement them, and provides services for many client companies.

1-3-2 The business environment surrounding the company

The business environment of Ubicom Holdings, which pursues the growth by offering IT solutions to social issues, such as the support for solving the shortage of manpower and the support for healthcare optimization, is as follows. The environment surrounding the global business and the medical business (which will be described in detail later) is favorable.

(From company documents)

1) Nationwide promotion of digitalization、Worsening labor shortage in the IT field

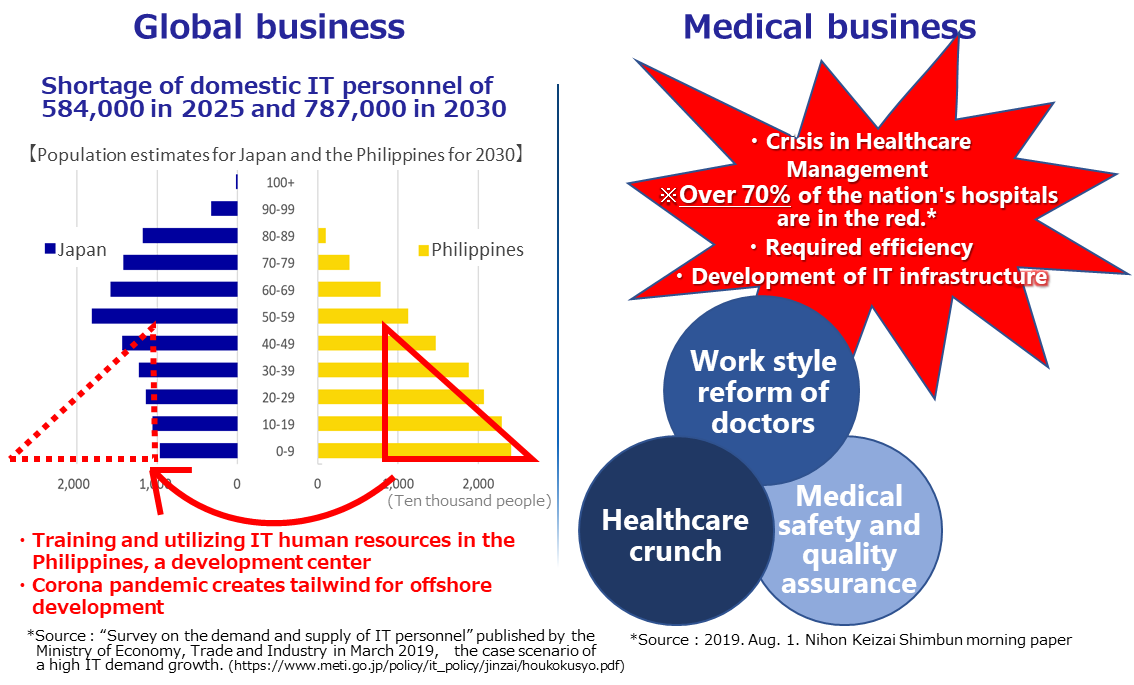

With the government's flag-waving for digitization in full swing, according to “Survey on the demand and supply of IT personnel” published by the Ministry of Economy, Trade and Industry in March 2019, it is important to secure IT personnel who can contribute to the improvement in productivity by creating added value and streamlining business operations in an innovative fashion, but it is difficult to secure them, due to the declining birthrate and the aging population. When the growth of IT demand is classified into “minor,” “medium,” and “significant” ones, it is estimated that Japan will be 584,000 engineers shortage in 2025 and 787,000 engineers shortage in 2030 in the case of “significant” growth.

2) Augmentation of national medical expenditure and tightening of examination of Medical Claims, Crunch in medical institution management, work-style reforms for healthcare providers

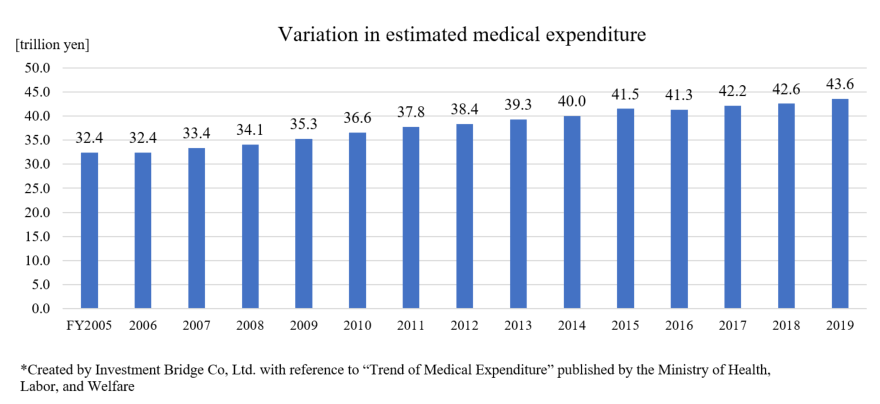

The estimated medical expenditure (excluding expenses such as workers’ accident compensation insurance and payments when the full payment is covered with own expenses. It accounts for about 98% of the national medical care expenditure, which is the overall estimate of all expenses required for treating injuries or diseases after examinations by doctors in medical institutions) has marked a record high in 2018 at 42.6 trillion yen. As medical expenses are in an increasing trend due to the progression of the aging population, the financial situation of medical insurances keeps getting worse. In order to reduce insurance costs, the national government is implementing a measure for rationalizing medical expenses by tightening the examination of Medical Claims,etc.

(What are the medical claims?)

Under the current system of health care services provided by health insurance, medical institutions receive up to 30% from patients and the other 70% or more from the health insurance association, mutual aid associations, city or ward offices, etc.

Medical institutions define the detailed statement of diagnosis and treatment, which is required to claim the amount covered by insurance from these public institutions, a Medical Claim; and the tasks performed to issue the Medical Claim are a very important procedure, which makes up most of the revenue of medical institutions.

The submitted Medical Claims are meticulously scrutinized by the Examination and Payment institutions. In case there is a mistake in its content, the Medical Claim may be sent back (returned) by the Examination and Payment institution, or the scores of medical fees may be reduced. In case the Medical Claim is returned, it must be carefully examined, revised, and resubmitted. Submitting appropriate Medical Claims is an extremely important task for the efficient management of medical institutions.

In 2009, medical institutions were obligated to make online requests for Medical Claims, as a general principle.

The crunch in medical care provision systems and deterioration of hospital management caused by the COVID-19 pandemic are becoming serious social issues. Against this backdrop, examination and payment institutions are moving to tighten the examination of medical claims, and work-style reforms are in progress for health care providers. Accordingly, it is now essential for the management of medical institutions to improve revenues through better operational efficiency for medical claim checks, etc., ensure the safety and quality of medical care, and deal with work-style reforms.

(3) Medical cloud market that is expected to grow rapidly

Thanks to the notice of the Ministry of Health, Labor and Welfare titled “Regarding places for storing medical records” partially revised in February 2010, it became possible to store medical information at data centers owned by private enterprises, which made it easier for private enterprises to offer medical cloud services.

It is expected that application platforms and cloud services in which servers exist in networks will be utlized in the medical field for electronic charts, medical image management systems, regional medical cooperation systems, and various services for home care support, remote image diagnosis, clinical trials, and dispensaries.

Especially, as the volume of data in today’s medical instiutions increased steeply and networks are used more widely, expectations toward medical cloud services are growing, as cloud services have merits, such as “It is easy to cooperate with other facilities,” “It is unnecessary to maintain and manage data by yourself,” and “They are inexpensive,” and they turned out to be useful for anti-disaster measures after many medical charts were lost in areas devastated by the Great East Japan Earthquake in March 2011. Furthermore, the medical crunch due to the spread of COVID-19 made us strongly aware of the necessity of online diagnosis and electronic charts.

Some point out the problem of safety from the viewpoint of protection of personal information, but the medical cloud market is expected to grow considerably for offering solutions to social issues while keeping a balance between the tightening and easing of regulations.

1-3-3 Strategic business domains

The company focuses its efforts to expand its business based on the strategic business domains of the “3As” fields, which will usher in the new age.

Field | Current situation and future plans |

AI | After finishing development for audio AI and chatbots (automatic conversation programs), the company is promoting cross-sectoral application. In the future, it will focus on developing solutions with in-vehicle AI devices by using voice AI with automobiles' SDL (The smart device link that connects car audio with smartphones). In addition, it also plans to support devices installed in self-driving cars and aims to build a recurring-revenue business that will sustainably generate significant profit by the time self-driving cars become popular. |

Analytics | The company finished the development phase of Japan’s number one Medical Claims Inspection Software, the Mighty series, and analysis tools, and will proceed to a phase of achieving a new monetization model by building an engine that analyzes big data of medical-related fields to improve the quantity and quality of the data. In addition, the company provides solutions for predictive maintenance for factories and shipping companies. |

Automation/RPA | The company has established an engine for software automation, and is pursuing robotics and RPA (automation of business operations with robots). It aims to expand its market reaching leading robotics and FA manufacturers. |

1-3-4 Segments

The company has 2 business segments; one is a global business that provides IT solution services to diverse markets such as Finance/Public, Medical, Automotive, Manufacturing and Robotics, and management improvement solutions etc for medical institutions such as the Medical Claims Inspection Software.

(From the company’s website)

1) Global business

- Overview

Its wholly-owned subsidiaries, Advanced World Systems, Inc. and Advanced World Solutions, Inc. are the major development centers in the Philippines, where it focuses on Finance, Public, Medical, Automotive, Manufacturing, and Robotics fields and delivers embedded software development, business application development, maintenance, and testing services.

The company defines “3As” (AI, Analytics and Automation/RPA) as a strategic business domain, and develops its own core solutions, utilizing these 3As technologies. The advanced capability of developing solutions is derived from its development centers in the Philippines, which has a top-class engineering group composed of about 1,000 engineers. This gives it a strong competitive advantage. (Refer to 【1-4 Characteristics and Strengths】 for more details.)

- Customers

Its client companies range broadly from finance, public, medical, automotive, manufacturing, to service industry-related ones. As mentioned above, in addition to the worsening IT personnel shortage, there have been strong needs for the reduction of costs for development and operation, but the company, which has 1,000 IT person who are proficient in Japanese and English, is steadily meeting such needs.

On top of that, the rich experience of development for numerous big domestic clients over many years has further earned their trust and built its reputation.

2) Medical business

- Overview

AIS Co., Ltd., which is a 100% subsidiary, engages in the development and sale of packaged solutions for medical institutions, cloud services, data analysis solutions, development support, and consulting services, contributing to the reform of workstyles of medical professionals and staff in medical institutions, the improvement of revenues at medical institutions, and the improvement in safety and quality of healthcare.

The “Mighty Series,” which improves the management quality and increases the work efficiency in medical fields, is well-received thanks to its user-oriented and cost-effective features. Sales were positively affected by work style reforms and over the past few years, it has gained more than 1,300 new users each year, as of the end of Mar 2020, the Mighty series occupied the top market share and was being used by approximately 38.8% of hospitals with a patient capacity of 20 or more (3,212 facilities), and 13.3% of clinics with a patient capacity of 19 or less (13,602 facilities), for a total of about 16,800 facilities.

- Mainstay products and services

(1) The Medical Claims Inspection Software (Mighty Checker®)

As improvement in efficiency and precision of Medical Claims Inspection were required, the company was ahead of competitors in releasing Medical Claims Inspection Software (Mighty Checker®) in 1999; it was well-received for its usability and it managed to establish its position as a leading maker of “Medical Claims Inspection Software.” In FY 2019, it released “Mighty Checker® EX,” an AI-based new-generation Medical Claim check system, and reaffirmed its market position.

Mainly, the company strongly supports the Medical Claim issuing process with the following features:

Product name | Features |

Mighty Checker® EX | - Top-end product in the Mighty Checker series released in the autumn of 2018 - Next-generation system for checking Medical Claims, which was developed by upgrading the highly-evaluated functions and usability of the conventional product “Mighty Checker PRO” and incorporating AI for Medical Claims Inspection |

Mighty Checker® PRO Analyze | - An advanced version of Medical Claims inspection software - Analyzes inspection results, and suggests an efficient inspection process. - In addition to the assessment and return measures, it can use inspection results more efficiently by utilizing the result of checking medical claims. - It makes it easier to modify the database by importing the assessment and return data; thus, it helps curb assessments and returns. |

Mighty Checker® PRO Advance | - A standard version of Medical Claims inspection software. - Validates the disease name, medicines, and medical care of the indication. - Inspects the measures for assessment and return (cross-check inspection, general inspection, calculation day check, etc.) - Validation by the claims support functions (checks items that can be calculated as consultation fees, etc.) |

Mighty Checker® Cloud | - A cloud service for inspecting medical claims, which can be linked with electronic charts in the cloud - Can be used for adopting the cloud for in-hospital systems, streamlining operations, realizing remote work, BYOD with any terminals, and BCPs, as it is easy to install and operate - Collaborations with cloud-type electronic medical record systems to be pursued |

(2) Medical Ordering check software, “Mighty QUBE® PRO”

This system utilizes the database of Mighty Checker® to check appropriateness of treatment and medication with disease, dosages and administration at the time of ordering prescriptions, and report errors when there is any inappropriate treatment or any disease name is missed. By preventing the erroneous input of medical instructions and misoperation, it can avoid medical accidents (near-miss accidents) and assessment (reduction of claimed amount), so that medical doctors can concentrate on their primary task, that is, healthcare. It is highly evaluated because it supports the financial and managerial improvement of hospitals through the pursuit of the safety and quality of medical treatment and the streamlining of business operation, and it also brings benefits to both hospital and patients, so many medical institutions have adopted it.

◎ Case study

In a case of installation in a hospital with 6 medical staff members, the hours for Medical Claims per month halved in a month after installation, and the claims support functions increased sales.

In the future, working hours will become even shorter as the staff gets used to operating the software. As more data accumulated, accuracy is also expected to improve further with the use of AI detection.

(3) SonaM, a medical cloud in preparation for disasters

This is a cloud service for supporting BCPs and preservation of medical data in medical institutions with one of the most advanced security bases in Japan.

Due to the spread of COVID-19, the necessity of online diagnosis and treatment attracted public attention, the diversification of diagnosis and treatment methods is progressing, and the demand for security in digital and cloud healthcare services is growing.

In addition, at medical institutions that take more important roles at the time of disasters, it is imperative to secure safe, reliable places and methods for storing in-hospital medical data.

“SonaM,” which was developed for the purpose of supporting healthcare systems suffering the lack of resources under these circumstances, is used for preserving medical data, including medical claims, medical charts, and examination images, with the security cloud.

In order to handle medical data in the cloud, it is necessary to comply with the three medical information security guidelines (the generic term is Three Guidelines from Three Ministries) suggested by the three ministries: the Ministry of Health, Labor and Welfare, the Ministry of Economy, Trade and Industry, and the Ministry of Internal Affairs and Communications, but the company covered all of them, by adopting the advanced cloud security base of NTT East.

Multiple step-by-step plans are prepared for meeting various needs from individual medical institutions with different scales.

This is a new profitable subscription model following the Mighty series, and the company aims to increase the average spending per user by cross-selling it with the Mighty series and increasing direct transactions.

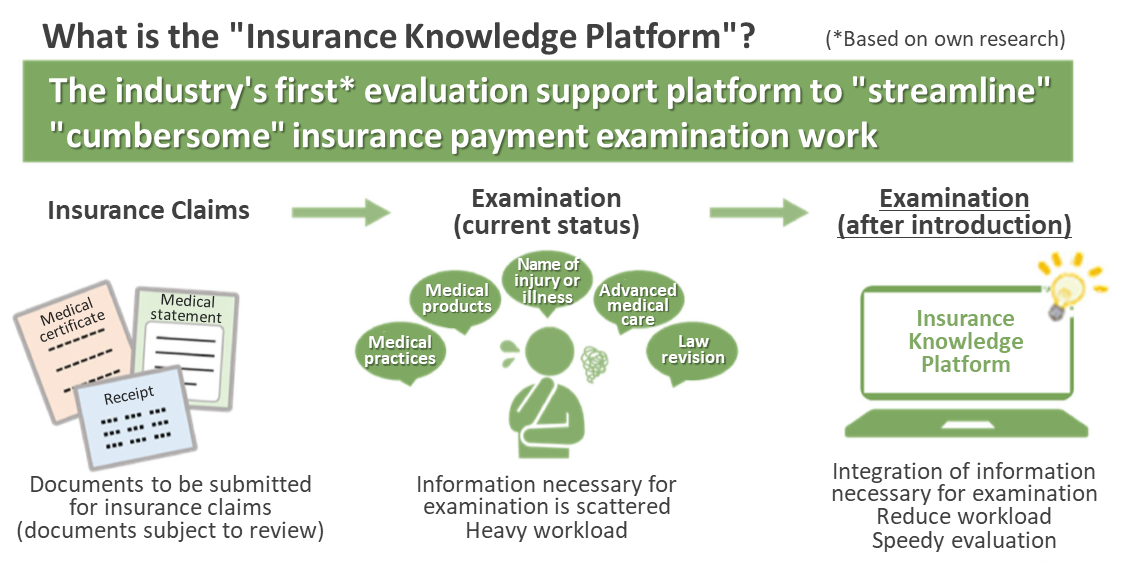

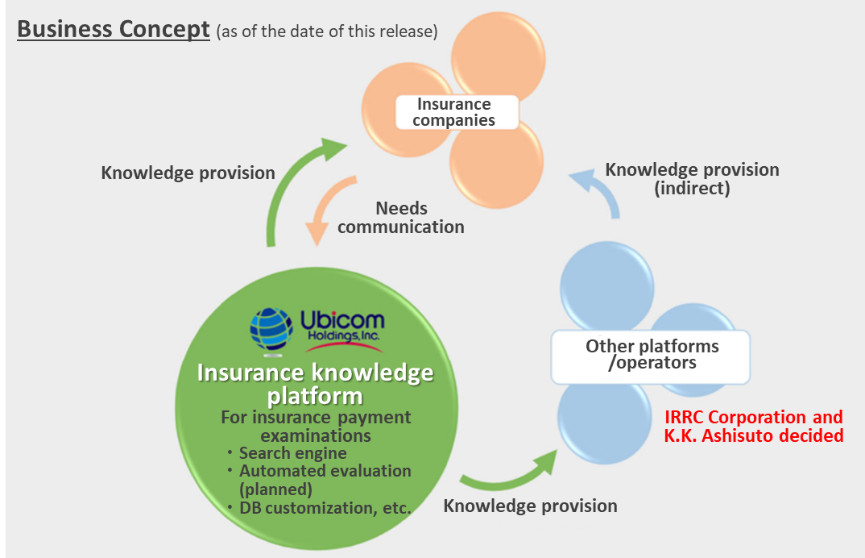

4) Insurance Knowledge Platform

“Insurance Knowledge Platform” is the industry’s first (based on Ubicom’s research) platform that supports improved evaluation efficiency by providing the information and knowledge necessary for insurance payment examinations carried out in the insurance industry on one, integrated system.

(Overview and features)

Until now, insurance companies have needed to exert a great deal of effort to cover the spectrum of information necessary to make an evaluation in examinations of insurance claims from customers, such as medical practices, medical products, names of injuries and illnesses, advanced medical care, and law revisions. However, utilizing the Insurance Knowledge Platform significantly improves the efficiency of the complicated examination processes.

After discharging the insured, it currently takes 2-4 weeks for insurance policy holders to receive benefits after completing paperwork with the insurance company and hospital, and it takes the insurance company about 2-3 weeks from examination to payment.

In Phase 1, the Insurance Knowledge Platform will shorten the above-mentioned period needed for the insurance company by at least one day.

In Phase 2, the claim process for the policy holder will be completed in minutes.

(Monetization concept)

The company is aiming to achieve a high-priced, high-profit subscription model that surpasses the Mighty series.

Revenue consists of basic initial costs, basic connection usage fees, optional initial costs, and optional connection usage. The company has developed more than 20 options to meet diverse needs, planning to secure high profits by offering a wide range of solutions.

(Strengths of the platform)

1. Intellectual Property (IP)

Utilizing the company’s own medical database backed by a track record of providing solutions to 16,800 medical institution users for over 20 years, the platform is equipped with medical treatment, drug codes, advanced medical information, etc., used for insurance examinations.

The platform also benefits from the knowledge of AI development.

2. Business model

The platform is operated via a cloud-based, next-generation service model with a high unit price and monthly subscription.

In addition, as the platform can be rolled out from the next year of development with only the burden of maintenance costs, its potential future value is enormous.

Also, the utilization of IT should reduce the burden of insurance claim procedures and shorten the number of days until insurance benefits are received. We also expect the company’s participation in the "Life Insurance Ecosystem Concept,” which aims to significantly reduce the administrative burden of insurance companies, to accelerate the platform’s market penetration.

3. Marketability

The company believes it is the first industry player to foray into an uncontested market space.

There is a potential customer base/market of over 100 companies, with an annual usage fee of several millions to tens of millions of yen per company.

(Future developments)

The company aims to expand the Insurance Knowledge Platform across the entire insurance industry in the form of a new subscription-type solution in the medical business, as well as develop and implement a payment examination search system equipped with AI and other advanced technologies geared toward further evolution of solutions for the insurance industry. Furthermore, it is focusing on capturing development demand associated with digital transformation and increased use of AI technology across financial services (including the insurance industry), boosted by the need to switch from "face-to-face services" to "non-face-to-face services" due to recent measures to prevent the spread of the coronavirus.

(From company documents)

1-4 Characteristics and Strengths

1-4-1 Training and utilizing approximately 1,000 engineers, mainly at its development sites in the Philippines

As was touched upon in the corporate history section, the president Aoki had inspected the site several times, and considered the Philippines as an optimum location for IT development. It not only is the source of the company's competitive advantage, but also plays an extremely important role for driving the future growth strategy.

The development center in the Philippines and its predecessor have over 25 years of development experience, and their main characteristics are as follows:

1) The optimum location for global IT development: the Philippines

The Philippines enjoys the demographic dividend period, where a long-term population growth, especially in young age groups, continues. It maintains an economic growth rate of roughly 6% on average. Moreover, young citizens are full of vigor and strive for upward mobility.

In addition, the fact that English is the official language plant the seeds for engagement in global activities, the high IT literacy, its easily accessible location at the center of ASEAN countries, etc. make it an optimum location as a global base for IT development.

2) Employing elite staff

As many as about 1,000 engineers enrolled mainly in development centers in the Philippines, but it does not only boast of the quantity (number of people), but also the quality (their aptitude), which is unrivaled.

Backed by a long track record, the engineers who seek employment at the company highly value the development center in the Philippines, and the group receives a few thousand applications for engineer positions almost every year. However, only top 4% of applicants are accepted.

3) Human resources development with original education and training

Building a top-class engineering group cannot be achieved just by hiring elite personnel.

One of the differentiating factors that make it hard for competitors to catch up with the company is, in fact, its educational system and training, which turn staff into capable top engineers.

In April 2003, 16 years ago, the corporate group established its own training center ACTION in the Philippines and started in-house developed training programs. It is constituted by 4 categories: basic concept for IT, advanced technologies, interpersonal skills, and the Japanese language. The training is conducted for 5 months and it aims employees will pass the PhilNITS (The Philippine National Information Technology Standards exam) and the Japanese Language Proficiency Test level 4.

After completing the training, the trainees present their achievements to the board members, and after going through interview assessments, they are finally assigned to projects. Even for elite students, the journey up to the point of being able to handle job assignments is not an easy one. The program graduates who overcome such hurdles acquire the skills needed for fulfilling their duties in an advanced technical field and a Japanese-speaking environment, hence they are overwhelmingly superior in the Japanese IT market, and they are the engine driving the company’s growth.

Furthermore, the company is always handling numerous challenging cutting-edge projects, giving highly motivated staff chances to shine. This is also one of the reasons why the corporate group is so popular as an employer in the Philippines.

4) Further upgrading and reinforcing of solution development capabilities

The company is already outshining competitors with its advanced solution development capabilities, but as it aspires to make robust use of this advantage, the company established the “Advanced Technologies Development Center” in 2017.

About tens of the center’s advanced engineers specialize in AI and big data analysis. By taking advantage of their native English to connect with top-class researchers globally, the company established a system that gives access to the latest cutting-edge technologies.

With this, it became possible to produce a prototype with highly added value that matches customer needs in a short period of time at low cost and directly offer it to major clients in Japan. Accordingly, the company’s capability of giving a proposal is improving considerably.

5) Receiving external acclaim

The work of its top engineers, who had overcome high hurdles and managed to participate in projects, has received high external acclaim, which led to the winning of numerous awards.

* In 2020, its Philippine subsidiary was awarded the Export Excellence Award for Software Development Services by the country’s Department of Trade and Industry (DTI).

* In 2020, two engineers were selected as Asian top guns, who are outstanding among top passers of Asia’s common standardized version exam of the Japanese Information-Technology Engineers Examination.

* In 2017, its Philippine subsidiary, Inc. was awarded as the best software company across the Philippines in the “International ICT Award.”

* Its training program “ACTION” has been consecutively awarded the Outstanding Company Program award at the "e-Services Philippines Award” for 6 years.

1-4-2 A robust customer base

Armed with a strong competitive advantage of having both a global division and a medical division, the company has established a robust customer base.

The robust client assets are considered to play a big role for the expansion of the recurring-revenue business, which is based on subscriptions, and matching the win-win investment model partners (growing corporations) with client enterprises, etc.

1-4-3 Feeling of partnership inside and outside the Group, and a corporate culture with a sense of ownership

The president Aoki considers all the employees, including those who work overseas, and their family members as "fellows." He thinks that one of the Group's strengths is that it achieves leaping growth thanks to all the employees who positively work with a cheerful never-fading smile, yet are never satisfied with status quo; each and everyone has a sense of ownership and thus pioneer the new times.

This feeling of partnership that values harmonious relationships extends to even outside the Group.

“The win-win investment model,” which is one of important growth strategies of the company, promotes the collaboration and strategic alliances with leading companies and growing enterprises, to accelerate the growth of existing businesses and create new businesses. The mindset that investors and investees aim to grow together as “fellows” regardless of business scale and the relationship between shareholders and portfolio companies is expected to motivate alliance partners further. This is probably the big difference from general VC (venture capital) and CVC (corporate venture capital).

1-5 ROE analysis

| FY 3/2015 | FY 3/2016 | FY 3/2017 | FY 3/2018 | FY 3/2019 | FY 3/2020 |

ROE (%) | 4.9 | - | 12.2 | 17.7 | 24.7 | 27.3 |

Net Income to Sales Ratio (%) | 1.24 | -0.16 | 3.76 | 6.63 | 10.37 | 13.21 |

Asset Turnover Ratio (x) | 1.33 | 1.46 | 1.44 | 1.36 | 1.27 | 1.17 |

Leverage (x) | 2.97 | 2.62 | 2.25 | 1.96 | 1.87 | 1.76 |

*The asset turnover ratio and leverage are calculated with the average amount between the beginning and the end of the term. Calculated by Investment Bridge Co, Ltd. based on annual securities reports and brief financial statements.

ROE is rising, due to the improvement in margin.

The net income to sales ratio in the term ending 2021 is forecasted to 13.6% over the previous year's forecast, and ROE is expected to further rise.

1-6 Shareholder Return

While the company recognizes returning profits to shareholders as one of the management priorities, it has been prioritizing expansion of its internal reserves for future business development and reinforcing the management quality. However, in FY03/19, the company paid a dividend of 5.00 yen per share for the first time considering the recent increase of orders received, robust business performance, and the establishment of the foundation for a profitable recurring-revenue business model. In the previous fiscal year, the company also paid a dividend of ¥5.00 per share and the payout ratio was 10.8%.

From now on, the company will concentrate on the improvement of measures for returning profits to shareholders with the aim of achieving a payout ratio of 30% or higher, while considering the balance between the improvement in business performance and strategic investment, based on the creation of stable cash flows through the shift to the subscription business model.

2. The First Half of Fiscal Year ending March 2021 Earnings Results

2-1 Earnings Trends

| FY Mar. 20 1H | Ratio to sales | FY Mar. 21 1H | Ratio to sales | YoY |

Sales | 1,925 | 100.0% | 2,093 | 100.0% | +8.8% |

Gross profit | 840 | 43.7% | 874 | 41.8% | +4.0% |

SG&A | 518 | 26.9% | 480 | 22.9% | -7.3% |

Operating Income | 322 | 16.8% | 393 | 18.8% | +22.0% |

Ordinary Income | 336 | 17.5% | 377 | 18.0% | +12.0% |

Current Net Income | 236 | 12.3% | 254 | 12.2% | +7.7% |

*Unit: million yen

Sales and profit increased. Record high for the first half.

In the first half of the term ending March 2021, sales rose 8.8% year on year to 2,093 million yen. Orders and solutions projects mainly for major customers in the global business continued to increase. New product launches in the medical business also contributed to growth. Operating income increased 22.0% year on year to 393 million yen. Although the global business saw a profit decline by 3.6%, due to the COVID-19 pandemic, this was handily offset by contributions from the establishment of a highly profitable subscription model in the medical business. Although gross profit margin fell 1.9% year on year, operating income margin grew 2.0% as SG&A costs decreased 7.3%. Ordinary income rose 12.0% year on year to 377 million yen. When considering the impact from the COVID-19 pandemic (around 25 million yen in costs associated with providing employee transport and the shift to a telework-based development structure in the Philippines, etc.) and exchange rate effects (roughly 20 million yen), profit grew 20%. Both sales and profit reached a record high for the first half.

2-2 Trend of Segments

| FY Mar. 20 1H | Ratio to sales | FY Mar. 21 1H | Ratio to sales | YoY |

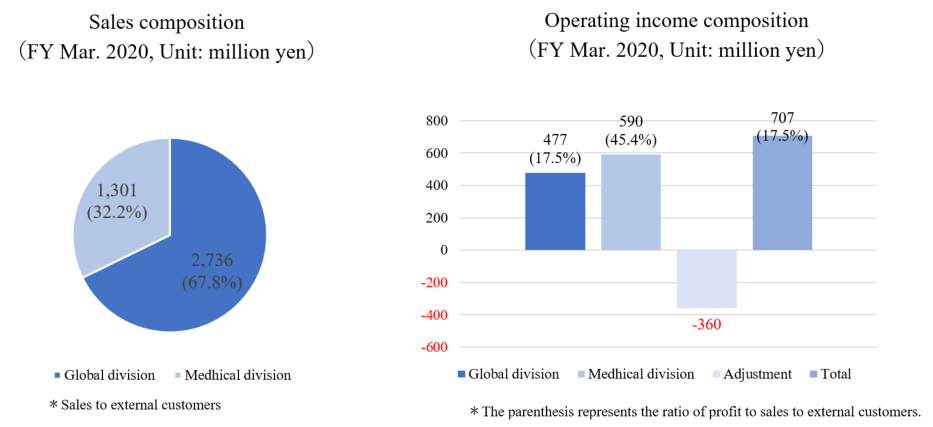

Global Business | 1,287 | 66.9% | 1,418 | 67.8% | +10.1% |

Medical Business | 637 | 33.1% | 675 | 32.2% | +6.0% |

Consolidated Sales | 1,925 | 100.0% | 2,093 | 100.0% | +8.8% |

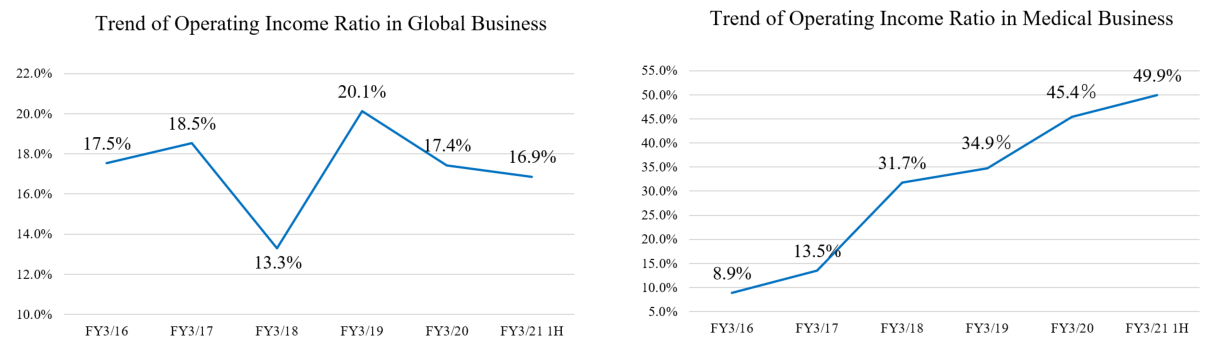

Global Business | 248 | 19.3% | 239 | 16.9% | -3.6% |

Medical Business | 267 | 42.0% | 337 | 49.9% | +25.9% |

Adjustment | -193 | - | -182 | - | - |

Consolidated Operating Income | 322 | 16.8% | 393 | 18.8% | +22.0% |

*Unit: million yen. Sales is the sales toward external customers. Ratio to sales in Operating Income is profit margin.

(Global business)

Sales increased but profit declined.

Sales to existing pillar (major) customers and orders for solutions increased. Meanwhile, profit fell, owing partly to costs associated with various measures implemented to prevent the spread of the coronavirus (transport for employees in Philippines, etc.) and higher outlays stemming from the shift to a telework development structure. However, the company was able to minimize the impact from the COVID-19 pandemic.

◎ Global division

Orders from existing pillar customers in the Philippines and Japan increased in the fields of software testing, automation of the execution/management of said testing, and application development. In the PC/IT equipment field, the company is expanding business with major global PC makers, while also rolling out such measures to other major PC makers. In addition, it has stepped up its active efforts to make customers pillars and sub-pillars, centered on major customers that are industry leaders, such as expanding business with global consulting companies in the AI field.

As a new solution, the company is receiving orders from new customers in the Edge IoT/AI fields that utilize the intelligent video analysis (IVA) technology and expanding the opportunity to roll out their solutions with this and existing core technology.

◎ Enterprise division

New and existing projects centered on the financial/public sector market showed steady growth thanks to emerging benefits from investments in human resources, including mid-career recruitment.

(Medical business)

Both sales and profit increased.

Package sales of the Mighty series were strong, and profitability improved thanks to the establishment of a highly profitable subscription model.

The number of medical institutions that installed the medical claims inspection software “Mighty Checker®” and the medical ordering check software “Mighty QUBE®” continued to grow steadily. The number of installations of next-generation medical claims checking system “MightyChecker® EX,” which is a strategic product, also increased steadily due to numerous inquiries, including those from several hospitals belonging to the medical group which boasts top-class sales.

In addition to expanding the use of the MightyChecker® EX system within major medical groups, the company promoted the cross-selling of solutions in order to capture direct sales further and increase the unit price per customer by shifting sales and support operations online as part of measures to prevent the spread of the coronavirus.

The company aggressively started up a number of new businesses related to the digitalization of medical care, such as “SonaM,” a new cloud-based medical service announced in March 2020, development of new solutions for insurance companies, and other data analysis solutions for health insurance associations and academic societies.

Also, the company is aggressively investing in securing "new subscription-type revenue sources” for the future to follow on from the Mighty series.

In September 2020, SBI Life Insurance decided to install the Insurance Knowledge Platform, a solution that improves the efficiency of work processes for the insurance industry by utilizing Ubicom’s own medical database. The company plans to start introducing the new solution to the insurance industry in earnest going forward.

2-3 Financial position and cash flow

Main Balance Sheet

| Mar. 20 | Sep. 20 |

| Mar. 20 | Sep. 20 |

Current Assets | 3,128 | 3,409 | Current liabilities | 1,370 | 1,350 |

Cash and Deposits | 1,976 | 2,379 | ST Interest Bearing Liabilities | 115 | 105 |

Receivables | 667 | 652 | Advances received | 702 | 734 |

Noncurrent Assets | 668 | 709 | Noncurrent liabilities | 208 | 271 |

Tangible Assets | 65 | 63 | LT Interest Bearing Liabilities | - | - |

Intangible Assets | 132 | 132 | Liabilities | 1,579 | 1,621 |

Investment, Others | 470 | 513 | Net Assets | 2,217 | 2,497 |

Total assets | 3,797 | 4,119 | Total Liabilities and Net Assets | 3,797 | 4,119 |

*Unit: million yen

Due to the increase in cash & deposits, and investment & others, etc. total assets grew 321 million yen from the end of the previous year to 4,119 million yen.

Due to the rise in advances received, etc. total liabilities augmented 42 million yen from the end of the previous year to 1,621 million yen.

Due to the increase in retained earnings, net assets rose 279 million yen from the end of the previous year to 2,497 million yen.

As a result, capital adequacy ratio rose 2.2 points from the end of the previous term to 60.6%.

◎Cash flow

| FY 3/20 1H | FY 3/21 1H | Increase and Decrease |

Operating cash flow | 186 | 488 | +301 |

Investing cash flow | -19 | -42 | -23 |

Free cash flow | 167 | 445 | +278 |

Financing cash flow | -71 | -58 | +12 |

Cash, equivalents at term-end | 1,693 | 2,344 | +650 |

*Unit: million yen

Net cash provided by operating activities and free cash flow increased due to an increase in income before income taxes and a decrease in notes and accounts receivable-trade.

The cash position improved.

2-4 Topics

◎ To participate in the partner program of the edge AI platform provider Idein Inc.

In September 2020, Ubicom Holdings decided to participate in Idein’s Actcast Partner Program. Idein is a Tokyo-based startup aspiring to become a mega platformer that creates IoT systems utilizing edge computing, which is garnering focus amid the rapid development and spread of AI and IoT technologies. The program involves utilizing “Actcast,” its next-generation AI/IoT platform, to develop solutions and promote provider businesses.

(What is edge computing?)

Edge computing is technology that distributes data located close to the “edge” of an IoT network in smartphones, cameras, automobiles, and other devices.

In an era where huge amounts of data are accumulated in the tide of DX (digital transformation), the challenges of existing data-intensive cloud computing, such as load concentration on data centers and information security issues, are becoming apparent. Data-distribution edge computing is garnering attention as a new data processing technology to solve these problems.

Edge computing processes data with data terminal equipment or equipment near it to enable low-latency and high-speed processing of data by distributing the load on data centers and networks. In addition, it is expected that this technology will develop further, and the market will expand as it becomes an indispensable technology in the accelerating IoT and 5G era, ensuring security and privacy by only collecting and analyzing necessary data and such.

(Overview of Idein Inc.)

Idein is a tech startup with unparalleled technological capabilities that has achieved dramatic acceleration of deep learning inference that is striving to become a mega platform that supports the new software industry. In addition to being selected for the "J-Startup" program launched by the Ministry of Economy, Trade and Industry to support startups that are active on the global stage, it has received numerous awards.

(Reason for joining the program)

With an eye to expanding global operations, Ubicom decided to collaborate with UK-based Arm’s certified AI partner Idein Inc to make a full-scale entry into the IoT market, which is expected to exceed 4 trillion yen in Japan alone in 2023.

Through its partnership with Idein Inc, the company aims to accelerate the development of advanced solutions and of next-generation engineers using the edge AI platform Actcast, and expand its solutions provided in the financial/public, medical, automobile, and manufacturing/robotics fields, which the Ubicom group positions as strategic markets.

◎ Launch of a platform business for the insurance industry

In September 2020, the company began providing the Insurance Knowledge Platform, a solution that improves the efficiency of work processes for the insurance industry by utilizing Ubicom’s own medical database backed by a track record of providing solutions to 16,800 medical institution users. SBI Life Insurance has decided to use it.

◎ Insurance Knowledge Platform to participate in “Life Insurance Ecosystem Concept”

In November 2020, Ubicom began rolling out its Insurance Knowledge Platform, and joined the “Life Insurance Ecosystem Concept.”

(Overview of the Life Insurance Ecosystem Concept)

The concept aims to utilize IT to reduce the burden of insurance claim procedures, shorten the number of days it takes to receive insurance benefits, and significantly reduce the administrative load of insurance companies.

At the core of this concept is IRRC Corporation (TSE1: 7325), which has a unique AI-OCR technology and is engaged in the insurance sales, solution, and system businesses, and Assist, which handles software sales and technical support.

The technology that automates the insurance claim processes in the company’s Insurance Knowledge Platform was highly regarded in terms of developing and expanding this concept, leading to Ubicom being selected to participate as the first company to strengthen the concept.

Also, several insurance companies agreed with this concept, with their full cooperation, Ubicom started development with the aim of starting the service in the winter of 2021.

(Future developments)

The company has received many inquiries for its Insurance Knowledge Platform. Against this backdrop, it plans to launch the basic function “Evaluation Information Search Engine” for insurance payment examination procedures and provide an optional “Automated AI Evaluation” function in winter 2020 onward, with the aim of expanding the platform’s functions and enhancing its appeal from a user’s perspective.

In order to foster the provision of a subscription-type platform for the insurance industry, which is a new initiative for Ubicom, as a new core business, the company plans to create mutual benefits between insurance companies and their customers, generate synergies with partner companies, and innovate and establish a business model.

In addition, from the third quarter of the term ending March 2021, the Ubicom group will utilize approximately 1,000 of its global IT personnel to step up the development of advanced solutions for the insurance industry, including the Insurance Knowledge Platform, and the promotion of DX. It will also invest in human resource development in a bid to develop next-generation engineers specializing in cutting-edge areas such as AI, and work to further improve corporate value with an eye to future growth.

(From company documents)

3. Fiscal Year ending March 2021 Earnings Forecasts

(1) Earnings Forecasts

| FY Mar. 20 | Ratio to sales | FY Mar. 21 Est. | Ratio to sales | YoY |

Sales | 4,038 | 100.0% | 4,437 | 100.0% | +9.9% |

Operating Income | 707 | 17.5% | 807 | 18.2% | +14.0% |

Ordinary Income | 715 | 17.7% | 840 | 18.9% | +17.4% |

Net Income | 533 | 13.2% | 605 | 13.6% | +13.4% |

*Unit: million yen. The forecasted values were provided by the company.

No change in earnings forecast. Increase in sales and profit. Profit is expected to reach a record high.

The company’s full-year estimates for the term ending March 2021 are unchanged, calling for sales of 4,437 million yen (up 9.9% year on year), an operating income of 807 million yen (up 14.0% year on year), and an ordinary income of 840 million yen (up 17.4% year on year). Profit margins are improving and both businesses continue to perform well. From the third quarter, the company will implement strategic investments on employee training, but is aiming to offset drags on this front to achieve double-digit profit growth.

Both operating income and ordinary income are expected to reach a record high for the seventh consecutive term. Dividends are currently undetermined, but the company plans to continue providing appropriate shareholder returns while maintaining a balance between earnings growth and strategic investments.

The company plans to strategically invest over 35 million yen in personnel development while maintaining a balance between full-year targets and profit.

(2) Initiatives to be implemented from the third quarter

Performance in strategic markets in the first half of the current term and initiatives to be carried out in the second half onward are outlined below.

Market | Outline of 1H | Third quarter and beyond |

Finance/public sector | The need for business reforms and DX acceleration in the financial and public sphere continued even in the COVID-19 pandemic. Orders grew steadily, particularly for existing projects. | Focus on strengthening offshore utilization proposals, capturing development demand in line with national policies, acquiring technologies essential for the development of next-generation financial and public sector services. |

AI | The development scale/scope of existing projects, such as AI chatbots for major consulting firms, expanded. | Promote further investment in human resources and establish a business model with an eye to developing unique AI solutions. |

Automotive | For some projects, customers held off making decisions and the outlook is uncertain, but performance remained solid. | Assuming slightly sluggish performance overall, the company will focus on capturing demand and improving skills related to model-based development (MBD), which is expected to expand going forward. |

Manufacturing/ robotics | While performance in the MFP (multifunction device) area was slightly weak, that in the PC field was strong due to the demand stemming from the COVID-19 pandemic. | Pursuing the acquisition of new projects, advanced technology development, and a co-creation model in the PC, IT, IoT, and ARVR* areas with an eye to device suppliers, content owners, and trading companies. |

Medical | Although chances to acquire new orders decreased due to refrained visits, the average spending of existing customers rose on benefits from price hikes and cross-selling. | Utilize the Internet to promote direct sales and increase average spending that exceed the negative impact from refrained visits, and expand the utilization of Filipino personnel in development operations. |

4. Future Growth Strategy

◎ Growth vision

As outlined above, the company will make growth investments from the third quarter of the current term to promote its “Strategy to Become the No. 1 Niche Platformer" on the premise of achieving full-year targets.

In the term ending March 2022, the company is targeting ordinary income growth of 840 million (target for current term) plus at least 300 million yen or so.

◎ Investment targets

The company will develop advanced IT human resources that take national policies and national interests into consideration, and promote solution and platform development.

The following three areas are its main target areas:

Medical | The development of packages and platforms that meet diversifying medical care needs, such as remote/online medical care and cloud computing. |

DX | The development of solutions and platforms equipped with core technologies that will become mainstream, such as AI, IoT, edge computing, and AR/VR. |

Finance | Develop next-generation applications that are faster and more flexible with cloud-native technology through containerization, microservices, etc. |

◎ Investment details

The company will develop advanced IT personnel in the AI, IoT, and DX fields from its pool of human resources.

From the third quarter onward, the company will start investing in employee training, and also expand the utilization of Filipino personnel in the medical business.

From the next term onward, the company will strive to swiftly reap the benefits of above-mentioned investments, and aim for a structure of 100 advanced IT personnel.

◎ Medical business

*Initiatives

Steady progress is being made with efforts to achieve a highly profitable business model and marketing-style reforms.

The following three factors are contributing factors behind the business’ recent double-digit sales and profit growth.

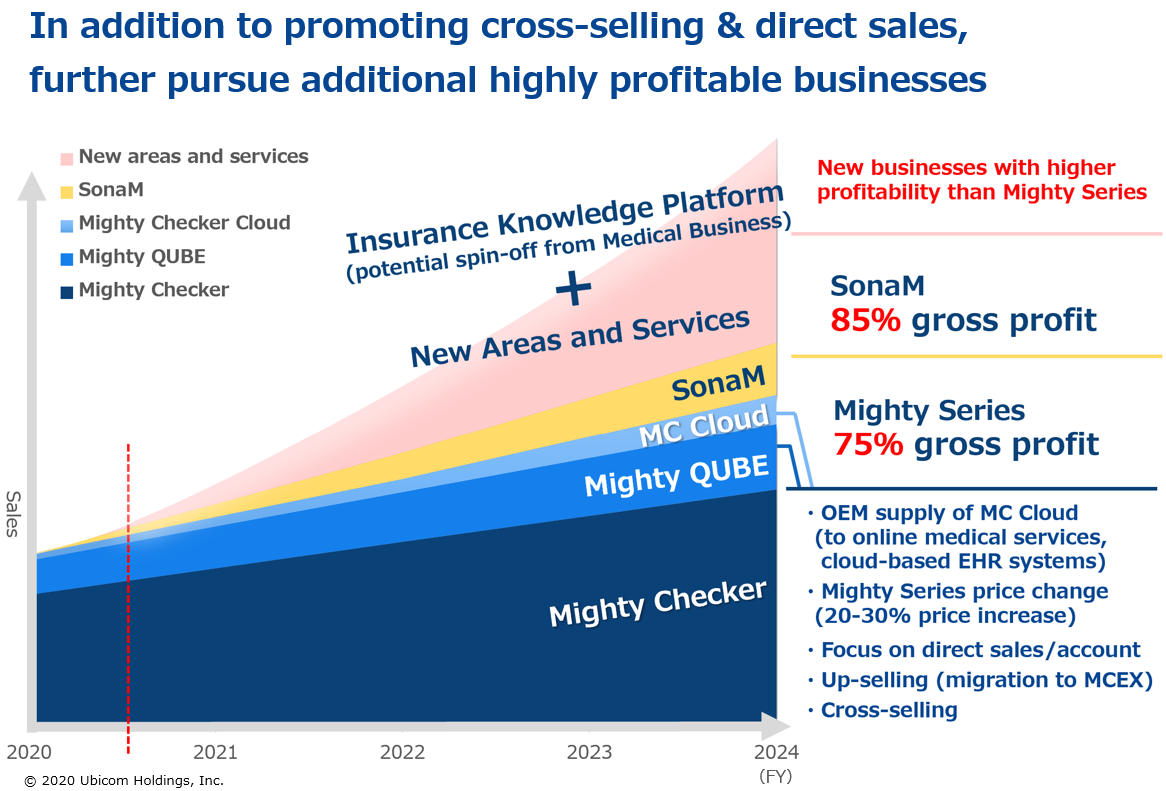

1. The high-margin subscription model is seeing steady growth.

Looking at the weighting of sales, development support, which posts low profit margins for all projects except strategic development projects, accounted for a lower portion of total sales, while subscription-based solutions, such as the Mighty series, accounted for over 85% of the business’ overall sales.

2. Higher average spending of customers thanks to price hikes and cross-selling for the Mighty series.

3. The company is promoting marketing-style reforms through online seminars and the enhancement of customer support.

It held a total of three free management improvement seminars for medical institutions online, due partly to the COVID-19 pandemic. Of the roughly 3,500 institutions invited, 219 attended. Among these, the company made proposals to the 69 medical institutions (roughly 30%) that expressed interest in switching to Mighty Checker® EX, the top-end product in the Mighty Checker series.

*Growth vision

As mentioned in the “1. Company Overview” section, the company sees this platform becoming a highly profitable subscription model that surpasses the Mighty series.

In addition to the Mighty series, which has a gross margin of 75%, and SonaM, which has a gross margin of 85%, the company will continue to accumulate new, high-margin services such as the Insurance Knowledge Platform going forward.

(From company documents)

◎ Global business

*Growth vision

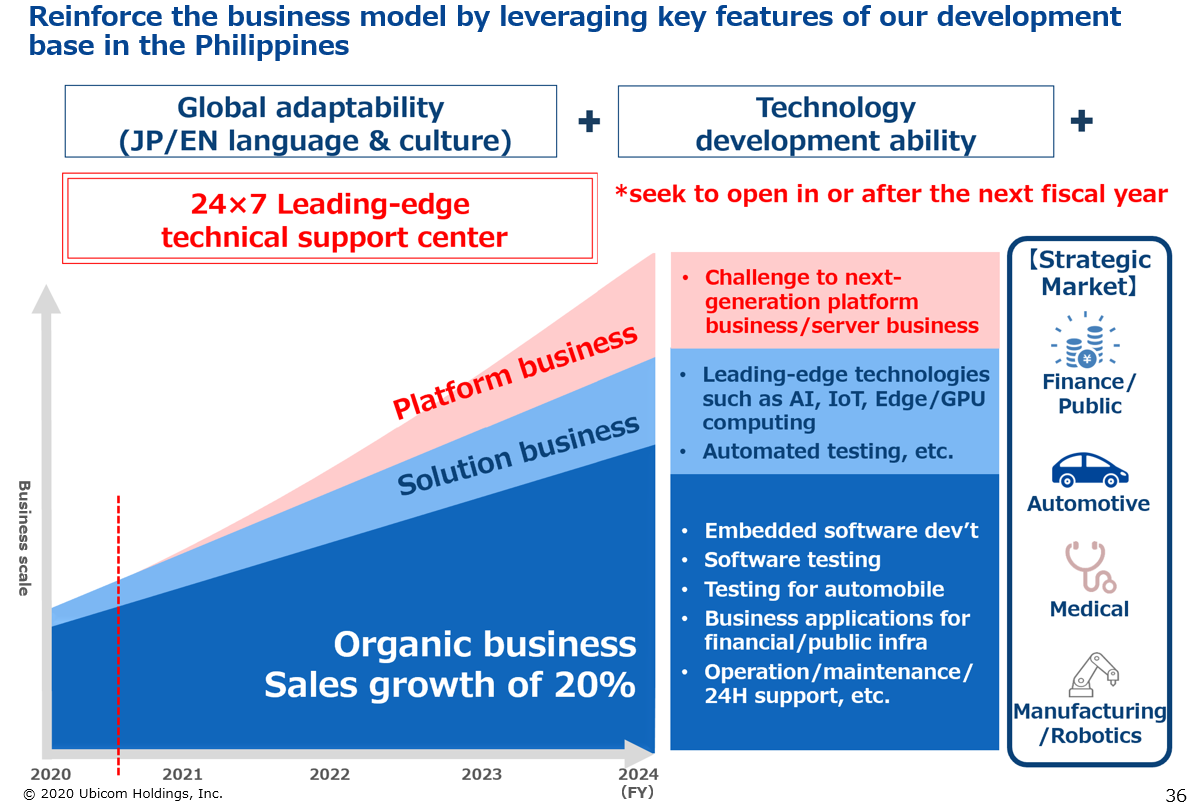

The company will continue to strengthen its business model by utilizing its canter in the Philippines, targeting the strategic financial/public sector, automobile, medical, and manufacturing/robotics markets.

It plans to start up a 24-hour advanced technical support center in the next term or later.

(From company documents)

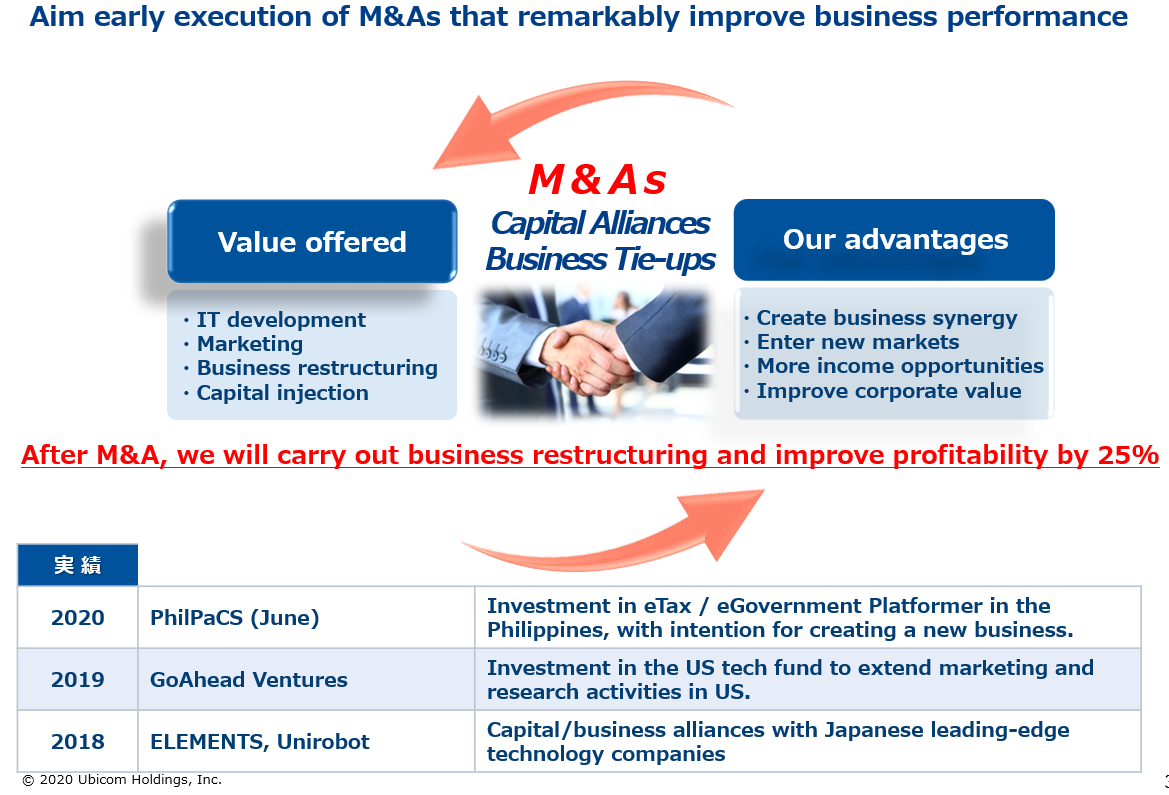

◎ The promotion of M&A, a win-win investment model

The company is pursuing the early implementation of M&A that will continue to accelerate growth. It will also actively form various alliances.

It will implement post-merger integration and business restructuring within one year after executing M&A, aiming to improve profit margin by 25%.

(From company documents)

5. Conclusions

In the first half of the term, the global business saw profit decline, due partly to the impact from the COVID-19 pandemic, but performance apparently beat the company’s projections by a wide margin. Also, the medical business posted significant margin improvement, resulting in double-digit profit growth overall, with the company having established a highly profitable business model.

The operating income margin for the medical business reached almost 50% on a half-term basis, apparently owing to progress with new customers installing and existing customers switching to “Mighty Checker® EX.” We look for the company to benefit from cross-selling and price hikes, including for “SonaM,” which was launched in April 2020 and is more profitable than the Mighty series.

Also, for the global business, we will be monitoring the effects of strategic investments in personnel, to be made from the third quarter of the current term, in terms of expansion of solution businesses and the speed of such growth.

Our focus is also on how the company utilizes the Insurance Knowledge Platform, the first step in its plans to launch new platform businesses over the medium term, will tap into the huge market it is anticipating.

(Prepared by Investment Bridge based on company documents)

<Reference: Regarding Corporate Governance>

◎ Organizational structure and composition of directors and corporate auditors

Organizational structure | Company with corporate auditor |

Directors | 5, out of which 2 are outside directors. |

Corporate auditors | 3, out of which 2 are outside auditors. |

◎ Corporate Governance Report

Last updated: July 1, 2020

*Basic Policy

The corporate ethos of our company is “to remain a one-of-a-kind business innovation company,” “global business operation,” and “co-prosperity based on a win-win model.” We recognize that it is essential to enrich and tighten our corporate governance, in order to improve our corporate value and maintain our global competitiveness under this ethos. In detail, our basic policy is “to aim to enhance our profitability and maximize the profits for shareholders by conducting more efficient, sound business activities” and put importance on compliance. Under this policy, we strive to strengthen our corporate governance, while considering that it is essential to fulfill our social responsibilities toward all kinds of stakeholders, including shareholders, employees, business partners, and local communities, and achieve sustainable growth and expansion.

<Reasons for Non-compliance with the Principles of the Corporate Governance Code (Excerpts)>

Principles | Reasons for not implementing the principles |

【Supplementary principle 1-2-(4) Electronic exercise of voting rights, and translation of convocation notices into English】 | Considering the current composition of our shareholders, we have not adopted the electronic exercise of voting rights and the translation of convocation notices for general meetings of shareholders into English. Seeing the ratio of exercised voting rights so far, we think that the exercise of voting rights in Japanese has not caused any significant troubles. From now on, we will discuss their necessity, while taking into account the situation of exercise of voting rights by overseas investors, the trend of the ratio of foreign shareholders, etc. |

【Supplementary principle 4-2-(1) Remunerations and incentives for executives】 | Since the term of each director of our company is one year, their remunerations are revised every year according to the performance in the previous fiscal year, but we have not adopted remunerations that vary with mid/long-term performance or remunerations paid with treasury shares. As for the remunerations for executives, we recognize the necessity to reflect mid/long-term corporate performance and potential risks in them and give incentives for stirring entrepreneurship soundly, and will keep discussing appropriate methods. |

<Disclosure Based on the Principles of the Corporate Governance Code (Excerpts)>

Principles | Disclosure contents |

Principle 1-4 【The so-called strategically held shares】 | Our company may hold shares strategically, if they are considered to contribute to the enhancement of the value of our corporate group from the mid/long-term viewpoint. Our policy is to hold such shares, as long as we can secure the rationality of shareholding purposes, such as the maintenance and cementing of transaction relations through business alliance, collaboration, etc. For exercising the voting rights of the shares, we discuss whether or not a bill is consistent with our shareholding policy. |

[Supplementary Principle 4-11-(2) Status of concurrent outside directors] | Concurrent positions held by outside directors and outside corporate auditors at other companies are disclosed on an annual basis along with notifications for the general meeting of shareholders, securities reports, and reports on corporate governance. Two outside directors concurrently serve as outside directors of companies other than the Company, but executive directors are to focus solely on the Company, and they do not hold concurrent positions as officers of companies other than the Company and its subsidiaries. One of the two outside corporate auditors concurrently serve as an external corporate auditor of a company other than the Company, but it does not hinder their duties as a corporate auditor. |

Principle 5-1 【Policy for constructive dialogue with shareholders】 | We positively respond to shareholders’ application for dialogue. The finance and accounting department and the strategic planning department are in charge of our IR activities, and have developed an IR system based on their daily close cooperation, so that they can accept the phone interviews from investors, small meetings, etc. In addition, we hold a result briefing session involving the representative director and distribute a result briefing video twice or more times every year. |

This report is intended solely for information purposes, and is not intended as a solicitation to invest in the shares of this company. The information and opinions contained within this report are based on data made publicly available by the Company, and comes from sources that we judge to be reliable. However, we cannot guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness or validity of said information and or opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration. Copyright (C) 2020 Investment Bridge Co., Ltd. All Rights Reserved |

To view back numbers of Bridge Reports on Ubicom HD. (3937) and other companies and to see IR related seminars of Bridge Salon, please go to our website at the following url: www.bridge-salon.jp/