Bridge Report:(6722)A&T the first half of Fiscal Year December 2019

![]()

Shigetaka Misaka President | A&T Corporation (6722) |

|

Company Information

Market | JASDAQ |

Industry | Electrical equipment (manufacturing industry) |

President | Shigetaka Misaka |

HQ Address | Yokohama Plaza Bldg. 2-6 Kinko-cho, Kanagawa-ku, Yokohama-shi |

Year-end | December |

Homepage |

Stock Information

Share Price | Shares Outstanding | Total market cap | ROE Act. | Trading Unit | |

¥937 | 6,257,900 shares | ¥5,863 million | 7.4% | 100 shares | |

DPS Est. | Dividend yield Est. | EPS Est. | PER Est. | BPS Act. | PBR Act. |

¥24.00 | 2.6% | ¥115.07 | 8.1 x | ¥1,175.60 | 0.8 x |

*The share price is the closing price on August 29, 2019.

The number of shares issued and BPS are as of the end of second quarter. ROE is from previous term.

Earnings Trend

Fiscal Year | Sales | Operating Income | Ordinary Income | Net Income | EPS | DPS |

December 2015 Act. | 10,138 | 1,202 | 1,183 | 839 | 134.18 | 20.00 |

December 2016 Act. | 10,234 | 1,015 | 1,004 | 651 | 104.14 | 20.00 |

December 2017 Act. | 10,371 | 773 | 757 | 678 | 108.41 | 20.00 |

December 2018 Act. | 10,430 | 774 | 768 | 518 | 82.80 | 24.00 |

December 2019 Est. | 11,200 | 1,010 | 1,000 | 720 | 115.07 | 24.00 |

* Estimates are those of the Company.Unit: million yen.

This report outlines A&T Corporation, briefly reports the results for the first half of Fiscal Year ending December 2019, and so on.

Table of Contents

Key Points

1.Company Overview

2.First Half of Fiscal Year ending December 2019 Earnings Results

3.Fiscal Year ending December 2019 Earnings Forecasts

4.Medium-Term Management Plan (FY Dec. 2018 to FY Dec. 2020) Progress

5.Interview with President Misaka

6.Conclusions

<Reference1: Outline of Medium-Term Management Plan>

<Reference2:Regarding Corporate Governance>

Key Points

- The sales for the first half of the term ending Dec. 2019 were 5,255 million yen, up 29.3% year on year. The sales of diagnostic reagents dropped, but the company’s original products, including clinical testing devices and systems and supplies, sold well, and the sales in the first half hit a record high. Operating income was 421 million yen, up 178.9% year on year. Due to the product mix, cost ratio rose 5 points, but outsourcing expenses decreased, so the augmentation of SG&A expenses was not significant. Both sales and profit exceeded the initial estimates.

- The ratios of direct and virtual overseas sales, on which the company puts importance for growth, were 5.8% and 23.8%, respectively. The sales to China, which grew considerably in the previous term, were as sluggish as 200 million yen (780 million yen in the previous term), due to the changes in the Chinese financial environment and the inventory adjustment of Runda, which is an OEM client, in China. This affected the results.

- There is no revision to the full-year earnings forecast. The sales for the term ending Dec. 2019 are estimated to be 11.2 billion yen, up 7.4% year on year. Some businesses in China are delayed, but this will be covered by the increase of domestic transactions in the IT and automation support business. The sales of original products, too, will increase. Gross profit is projected to rise 7.3% year on year, due to the settling-down in man-hours for new products of laboratory information system, the decrease of purchased products, etc. Operating income is forecasted to rise 30.4% year on year to 1,010 million yen. Due to the recruitment of personnel for sustainable growth and the development of new products for laboratory automation system, etc., SG&A expenses are estimated to increase 2.4% year on year, but it will be offset by the rise in gross profit. The dividend is estimated to be 24 yen/share, unchanged from the previous term. The estimated payout ratio is 20.9%.

- Sales and profit grew considerably year on year, exceeding the initial estimates. The OEM sale to Runda in China is still small-scale, so even if the OEM sales do not reach the initial estimate, it will be possible to cover it with domestic transactions, etc. In order for the company to grow further for commemorating the 50th anniversary in 2028, it is essential to cultivate overseas markets, including China, which is growing rapidly. How much the company will recover its performance in the second half while considering its business from the next term is noteworthy. In addition, the important step for achieving an ordinary income rate of over 10% is to increase ordinary income rate to 8.9% this term.

1.Company Overview

The core businesses of A&T Corporation are the “blood testing business,” in which the company develops, manufactures, and sells IVD devices, reagents, etc. mainly for electrolyte and glucose tests, and the “IT and automation support business,” which facilitates the streamlining of clinical tests.

The company excels at proposing an optimal one-stop solution for preparing necessary products in a laboratory, installing and operating equipment while proposing a layout, and possesses advanced technologies that are highly evaluated by leading overseas OEM clients.

1-1 Corporate History

In the 1980s, the general chemical manufacturer Tokuyama Corporation (4043, 1st section of Tokyo Stock Exchange) was expanding its business scope from materials to fine chemicals. While taking inventory of various technologies and items, Tokuyama Corporation decided to develop latex (rubber material; one of the chemical products) reagents for testing antigen-antibody reactions.

In the development process, Tokuyama Corporation formed a business tie-up with Analytical Instruments Inc., which develops, manufactures, and sells clinical test equipment and had been leading the industry by releasing such products as fully automatic blood sugar analyzer in 1978, and in Apr. 1988, they founded a joint venture for distributing their products, A&T Corporation. (“A” of Analytical Instruments and “T” of Tokuyama were combined.)

In November 1990, the company established Esashi Factory, which is now the primary production site, in Iwate Prefecture.

In 1994, A&T Corporation underwent an absorption-type merger, integrating the diagnosis system division of Tokuyama Corporation. The period from the 1980s to the 1990s was the growth period of the clinical testing industry, in which many core technologies were developed, and the company expanded its business steadily while taking advantage of that trend.

In Jul. 2003, the company issued over-the-counter shares. It is now listed in the JASDAQ market of Tokyo Stock Exchange.

1-2 Management Philosophy, etc.

A&T Corporation upholds its corporate ethos: “Support medical care and contribute to people’s health around the world,” and aims to improve the quality of medical care and reduce cost, under following three management policies.

1. C.A.C.L. | Commit to research and development of unique products and technologies in all areas’ of “C.A.C.L.” in clinical laboratory testing. |

2.Consistent Framework | Increase market value and reduce the cost of products through an integrated system of development, manufacture, distribution and customer support. |

3.Alliance | Promote market expansion and quality improvement of products with business partners domestic and overseas. |

* C.A.C.L.: Acronym of “Chemicals (diagnostic reagents),” “Analyzers (Analyzers),” “Computers (laboratory information system),” and “Lab-Logistics (laboratory automation system)” in the field of products required for operating a clinical test room

1-3 Market Environment

Market scale

(Domestic and global markets)

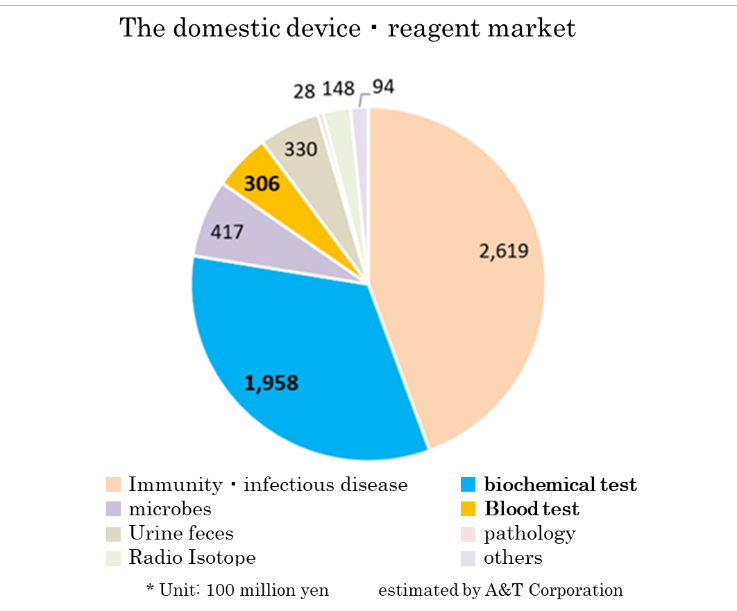

Based on the information in the website of the Japan Association of Clinical Reagents Industries, A&T Corporation estimated that the scale of the Japanese market of related devices and reagents is about 590 billion yen. The market scales of biochemical tests and hematology tests are 195.8 billion yen and 30.6 billion yen, respectively.

(Trend of IVD devices)

According to “Statistical Survey on Trends in Pharmaceutical Production” by the Ministry of Health, Labour and Welfare, the scale of the Japanese medical products market (domestic production amount) in 2015 was about 1.9 trillion yen. Products for medical treatment is dominant, and medical Analyzers, which is handled by A&T Corporation, has a market scale of about 180 billion yen.

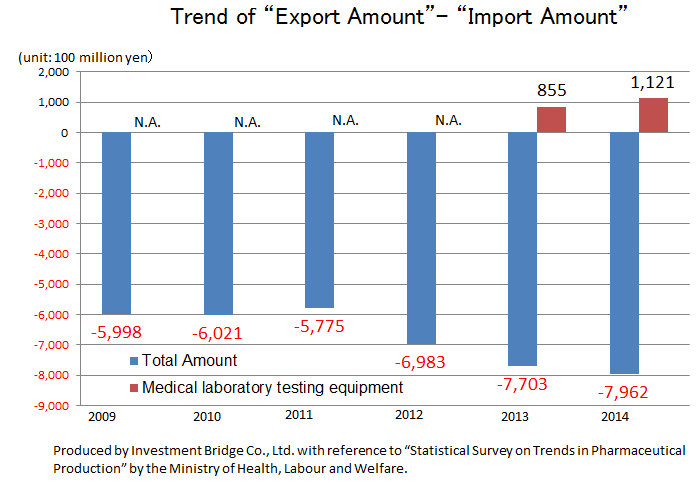

While there is a significant excess of imports of the overall medical product, there is an excess of exports of IVD devices. This indicates how competitive Japanese companies are. Hitachi and Canon Medical Systems (former Toshiba) supply testing equipment to Roche in Switzerland and Abbott in the U.S., respectively. Likewise, A&T Corporation supplies OEM products to Siemens. Namely, testing equipment made in Japan is now indispensable in the global clinical testing field.

| 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 |

Total amount |

|

|

|

|

|

|

|

Production | 15,760 | 17,130 | 18,080 | 18,950 | 19,050 | 19,890 | 19,450 |

Import | 10,740 | 10,550 | 10,580 | 11,880 | 13,000 | 13,680 | 14,240 |

Export | 4,750 | 4,530 | 4,800 | 4,900 | 5,300 | 5,720 | 6,220 |

Export - Import | -5,998 | -6,021 | -5,775 | -6,983 | -7,703 | -7,962 | -8,023 |

IVD devices |

|

|

|

|

|

|

|

Production | 1,100 | 1,030 | 1,450 | 1,580 | 1,470 | 1,690 | 1,800 |

Import | N.A. | N.A. | N.A. | N.A. | 210 | 200 | N.A. |

Export | 750 | 620 | 980 | 1,100 | 1,060 | 1,320 | 1,420 |

Export - Import | N.A. | N.A. | N.A. | N.A. | +855 | +1,121 | N.A. |

*Unit: 100 million yen. The import amounts of medical Analyzers from 2009 to 2012 and 2015 are N.A., because they were not in the top 10.

Companies in the same field

Code | Corporate name | Sales | Sales growth rate | Operating income | Profit growth rate | Operating income margin | ROE | Market cap | PER | PBR |

4549 | Eiken Chemical | 35,900 | +0.4 | 3,600 | -21.9 | 10.0% | 10.3 | 67,837 | 22.1 | 1.6 |

6678 | Techno Medica | 10,000 | +7.2 | 1,400 | -7.8 | 14.0% | 8.2 | 17,782 | 17.4 | 1.3 |

6722 | A&T | 11,200 | +7.4 | 1,010 | +30.4 | 9.0% | 7.4 | 5,863 | 8.1 | 0.8 |

6869 | Sysmex | 320,000 | +9.0 | 64,000 | +4.4 | 20.0% | 16.3 | 1,393,970 | 33.1 | 5.3 |

6951 | JEOL | 119,000 | +6.9 | 7,100 | +6.4 | 6.0% | 15.0 | 110,369 | 21.8 | 2.8 |

8036 | Hitachi High-Technologies | 710,000 | -2.9 | 56,000 | -16.0 | 7.9% | 11.9 | 783,733 | 19.1 | 1.8 |

*The results for this term were forecasted by the company. The units are million yen, %, and times. Share price-related indices are based on the closing prices on August 29,2019.

* Sysmex, Hitachi High-Technologies adopted IFRS. Hitachi High-Technologies' operating income is "adjusted operating income" which is calculated by subtracting the cost of sales and selling, general and administrative expenses from sales revenue.

We compared major listed clinical testing device manufacturers. A&T Corporation has the smallest business scale among them and the share price evaluation is the lowest as its price-to-book ratio is under one. It would be continuously necessary to manifest its strategies to enhance popularity and expand business as well as promoting understanding.

1-4 Business Description

In addition to the development, manufacturing, and sale of products, including testing devices and reagents used in the clinical testing rooms of hospitals, A&T Corporation offers customer support. The company also offers comprehensive consulting services, including the proposal for the layout of a laboratory, installation and operation.

(Source: the company)

What is clinical testing?

Clinical tests can be classified into “biopsies” for directly examining the body with medical equipment, such as X-ray equipment, CT, MRI, electrocardiographic and ultrasonic equipment, and “laboratory tests” for examining biological samples (specimens), such as blood, urine, stool, and cells, collected from patients.

A&T Corporation handles products used for laboratory testing, especially blood tests.

There are a variety of blood tests conducted at hospitals and in comprehensive medical checkups, including the tests of the hepatic system, the renal system, uric acid, the lipid system, glucose metabolism, blood cells, and infectious diseases. A&T Corporation mainly conducts business related to “electrolyte tests” and “glucose tests.”

“Electrolyte tests”

The water content constitutes about 60% of the human body, as body fluids, including intracellular fluid and blood plasma. Body fluids are classified into electrolytes, which are mineral ions that dissolve in water and conduct electricity (such as sodium, potassium, calcium, and chlorine), and non-electrolytes, which dissolve in water, but do not conduct electricity (such as glucose and urea).

Each electrolyte takes important roles for keeping human beings alive while maintaining a healthy balance - “sodium” adjusts the water content of the body, “potassium” controls muscles and nerves, “calcium” forms bones and teeth, conveys nervous stimuli, and coagulates blood, and “chlorine” supplies oxygen to the inside of the body. If the concentration of electrolytes in blood is abnormal, there is a possibility that the kidneys or hormones are malfunctioning.

The purpose of electrolyte tests is to measure the concentration of each electrolyte ion in body fluid, detect the disruption of a balance, and then diagnose a disorder in the body. Sampled blood and urine are examined with testing device.

*Major diseases

Sodium | Diabetic coma, dehydration, acute nephritis, chronic renal failure, nephrotic syndrome, heart failure, hypothyroidism, Addison disease, diabetic acidosis, etc. |

Potassium | Acute renal failure, chronic renal failure, respiratory insufficiency syndrome, etc. |

Calcium | Malignant tumor, multiple myeloma, hyperparathyroidism, renal failure, hypoparathyroidism, vitamin D deficiency, etc. |

Chlorine | Dehydration, renal failure, chronic nephritis, emphysema, etc. |

“Glucose tests”

The sugar in blood plasma (blood sugar) is composed mostly of glucose, which is the only energy source for the central nervous system, including the cerebrum. When the stomach is empty (over 5 hours after eating), the liver emits about 8 grams of glucose per hour, and the brain consumes about half of them, and muscles and red blood cells consume one fourth of them, respectively.

Blood sugar level in its normal condition is strictly controlled while keeping a balance between the increase through the absorption from the intestine and the generation in the liver and the decrease through the consumption in the muscles. If this control does not work properly, hyperglycemia or hypoglycemia will occur.

A glucose test is conducted for measuring the concentration of glucose in blood or urine.

*Major diseases

Hyperglycemia | Diabetes (insulin, which is a hormone secreted from the pancreas, does not work, and so cells cannot use glucose in blood), pancreatitis, thyroid disease, postgastrectomy dumping syndrome, etc. |

Hypoglycemia | Liver damage, hypopituitarism, adrenal hypofunction, etc. |

1.Business Field

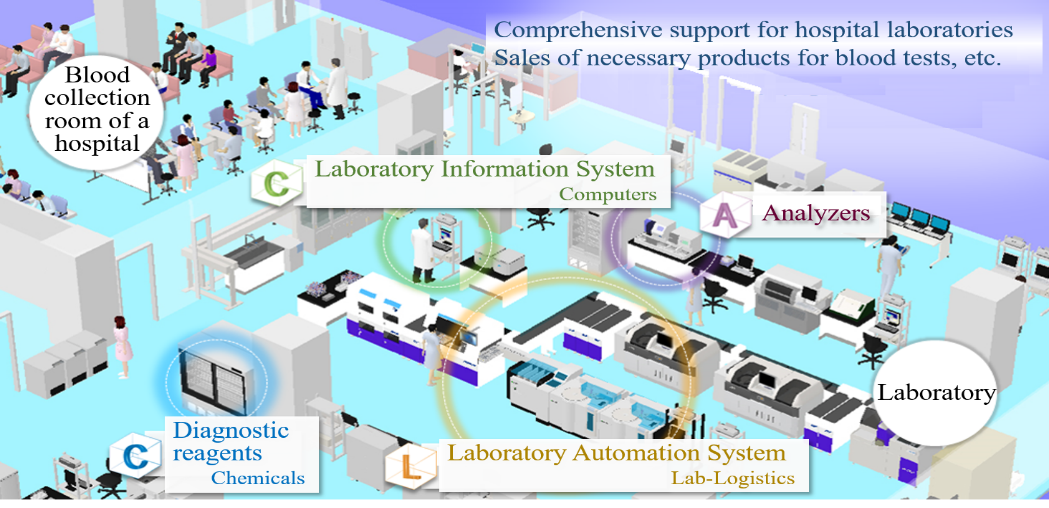

The business of A&T Corporation is composed of the “blood testing business,” in which the company develops, manufactures, and sells clinical testing devices, reagents, supplies, etc. for blood tests, and the “IT and automation support business,” which facilitates the streamlining of manual work in hospital laboratories with IT and automated systems. The company comprehensively supports hospital laboratories.

(Since this company conducts this business only, neither its brief financial reports nor securities reports contain segment information. It should be noted that the company discloses the sales of each product series in reference materials for briefing results, etc., but not the sales of each type of business.)

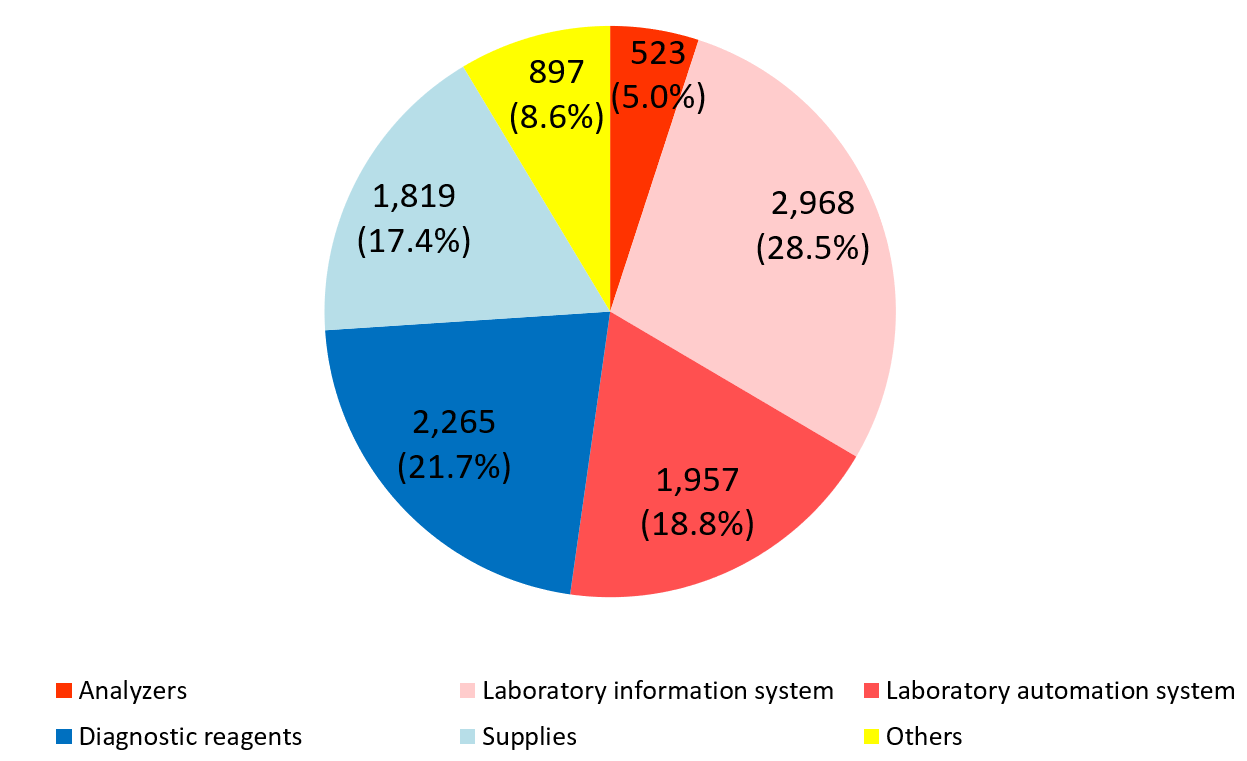

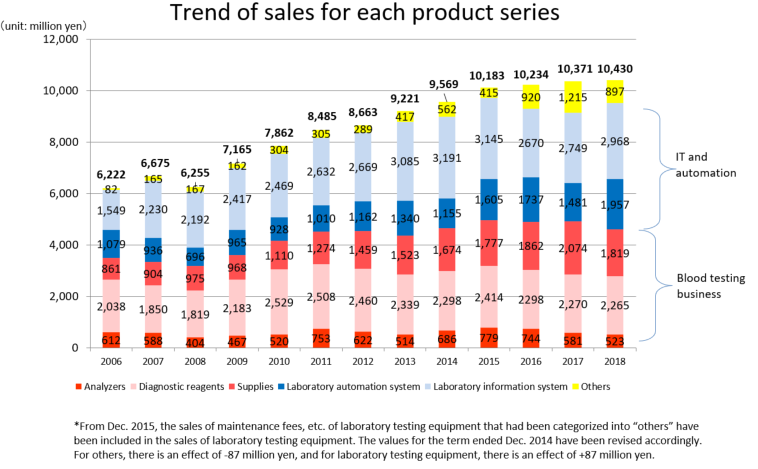

Product series | Results for FY Dec.18 | Ratio to total sales |

Clinical testing devices and systems | 5,448 | 52.2% |

Analyzers | 523 | 5.0% |

Laboratory information system | 2,968 | 28.5% |

Laboratory automation system | 1,957 | 18.8% |

Diagnostic reagents | 2,265 | 21.7% |

Supplies | 1,819 | 17.4% |

Others | 897 | 8.6% |

Total | 10,430 | 100.0% |

The red letters denote the “Blood testing business” (analyzers, diagnostic reagents, and supplies), while the blue letters denote the “IT and automation support business” (Laboratory Information System, Laboratory Automation System). The sales distribution ratio for the term ended December 2018 was 44.2% for the blood testing business, and 55.8% for the IT and automation support business.

1) Blood testing business

Outline

The company works on developing, manufacturing, and selling Analyzers for clinical tests such as “electrolyte tests” and “glucose tests,” reagents for clinical tests (for measuring the concentrations of electrolytes, blood sugar, etc.), and supplies (such as sensors installed in analyzer), and offers customer support.

Electrolyte analyzer | Glucose analyzer |

|

|

(Source: A&T’s website)

Commercial distribution

*Inside Japan

The company directly sells analyzers, reagents, and supplies to small and medium-sized hospitals via 8 branches nationwide. As of now, about 4,300 units of equipment are in operation.

*Outside Japan

The company sells analyzers as an OEM. It supplies electrolyte units, which are the specialty products of the company, to other Japanese manufacturers, including JEOL (6951, 1st section of TSE). The OEM clients combine the unit with large-size clinical chemistry analyzers and sell them. As an OEM, JEOL supplies products to Siemens, which is one of global enterprises handling large-size clinical chemistry analyzers.

Business model

Once Analyzers is newly installed, clinical reagents and supplies will be continuously delivered, and the maintenance service for the equipment will be offered.

Once adopted, it is rare for client hospitals to change manufacturers considering the continuity of test data and usability, and so it is difficult for new manufacturers to enter the market. 7 to 10 years later, upgraded models will replace them. This characterizes this business field.

Major enterprises in this field

Sysmex (6869, 1st section of TSE), Hitachi High-Technologies (8036, 1st section of TSE), JEOL (6951, 1st section of TSE), Fuji Film Wako Pure Chemical (unlisted), ARKRAY (unlisted)

2) IT and automation support business

Outline

In the case of blood tests, it is necessary to convey patient’s blood (specimen) sampled in a blood collection room to a clinical laboratory and manually set the specimen at testing equipment.

As several kinds of tests need to be conducted for many specimens at the same time, this work is extremely labor-intensive and inefficient, and the human error of taking a wrong specimen is difficult to avoid.

In these circumstances, A&T Corporation supports the streamlining of the testing process with the following 2 systems.

(Source: A&T’s website)

Laboratory Information System (LIS) | Software for a clinical laboratory, which receives requests for tests from medical doctors, sends a command for testing to Analyzers, and inputs test results in electronic medical charts, etc. accurately and swiftly. This also manages cost, etc. and serves as a core system of a laboratory. |

Laboratory Automation System (LAS) | The specimens delivered to a laboratory are automatically conveyed to Analyzers via a computer-controlled conveyor line, and then undergo measurement. Blood tests, which had been manually conducted, are fully automated, to streamline and speed up the testing process. |

It is expected that the installation of LAS will decrease the necessary number of workers from 7-8 to about 2, and the necessary time of testing from 90 min. to 30-40 min.

Through the introduction of LIS, it became possible to put together the data of test results, which had been printed out for each test item, and give feedback to medical doctors swiftly and accurately. In addition, the data mining function is helpful for reducing the number of times of abnormal value retesting and the duration of testing.

Commercial distribution

*Inside Japan

Targeting the laboratories of medium and large-sized hospitals, the sales division of A&T Corporation sells LIS in cooperation with hospital information system manufacturers, including Hitachi, IBM, and Fujitsu, and LAS in cooperation with large-size clinical chemistry and immunoassay analyzer manufacturers, including Hitachi, Toshiba, and JEOL, as comprehensive solutions *.

*For the details of comprehensive solutions, see the section “1-5 Characteristics and Strengths.”

*Outside Japan

Previously, the company has been selling LAS directly in Korea, China, etc., but in China it has started OEM supply. In the United States, OEM sales of blood aliquoting modules, which are the main components in LAS, are made to partner companies.

Business model

In addition to the maintenance service of LIS and LAS after their installation, the company can connect additional systems, customize the system, and so on for LIS, and can offer maintenance services, sell supplies, and so on for LAS. For both of the systems, stable sales can be expected.

Like Analyzers, clients are rarely motivated to shift to other manufacturer’s equipment, considering usability, data continuity, etc. The price range per transaction is 10 to 50 million yen for LIS, and 10 to 100 million yen for LAS.

Major enterprises in this field

LIS: Sysmex CNA (subsidiary of Sysmex), local vendors, etc.

LAS: IDS (unlisted), Hitachi-Aloka (unlisted), Siemens, etc.

2.Development systems

The company established development groups by product types in order to apply elementary technologies cultivated over many years to a wide range of product development. In addition, it places a chief technology officer for each field including electricity, machinery, and chemistry and promotes product development through management of a matrix organization structure.

About 70 staff members are employed at the headquarters and Shonan Office.

The research and development cost for the term ended December 2018 was 958 million yen. It will continue to actively promoto reseach and development with a target sales of around 10%.

3.Production systems

There are two production sites: Shonan Factory, in Kanagawa Prefecture, for manufacturing some clinical reagents and supplies and Esashi Factory, in Iwate Prefecture, for producing equipment, Laboratory Automation System (LAS) and some clinical reagents.

The company manufactures high-quality, safe products with advanced equipment under rigorous management. In cooperation with the development section, the company is striving to improve quality and streamline operation.

In order to develop the foundation for expanding sales further, the company constructed a new building with a total floor area of 7,300 m2 at Esashi Factory by investing 1.7 billion yen in August 2017.The Company strengthens capabilities considerably through this construction.

4.Sales routes and methods

As mentioned above, A&T Corporation sells its products to client hospitals via 8 branches in Japan, by utilizing its capability of proposing comprehensive solutions.

Outside Japan, the company supplies products to overseas clients and dealers including Siemens through domestic OEM partners such as JEOL.

To expand its business scale by supplying products as an OEM like this is the basic strategy, and the company concentrates on the diversification of OEM clients.

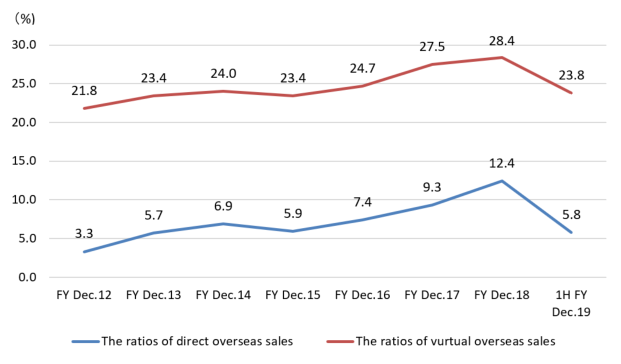

The direct overseas sales to overseas clients and dealers and its ratio for the term ended December 2018 were about 1.3 billion yen and 12.2%, respectively.

But, as the ratio of virtual overseas sales, including the (estimated) overseas sales via domestic OEM clients, for the term ended Dec. 2015, Dec. 2016, Dec. 2017, and Dec. 2018 were 23.4%, 24.7%, 27.5%, 28.2% respectively, the ratio of overseas sales is in upward momentum.

Especially in the term ended Dec. 2018, sales to China soared to 780 million yen, more than doubled from 351 million yen in the previous fiscal year. In the first half of the term ending Dec. 2019, the performance was sluggish due to the changes in the Chinese financial environment, but the company will keep cultivating the Chinese market, with the aim of achieving a ratio of virtual overseas sales of over 50% in the medium-term.

(The ratio of overseas sales, unit: %)

| FY Dec.12 | FY Dec.13 | FY Dec.14 | FY Dec.15 | FY Dec.16 | FY Dec.17 | FY Dec.18 |

Direct | 3.3 | 5.7 | 6.9 | 5.9 | 7.4 | 9.3 | 12.2 |

Virtual | 21.8 | 23.4 | 24.0 | 23.4 | 24.7 | 27.5 | 28.2 |

1-5 Characteristics and strengths

Capability of proposing comprehensive solutions

A&T Corporation handles products mainly for electrolyte and glucose tests, and does not handle large products for analyzing other tests. However, client hospitals need to install a variety of testing instruments in their clinical laboratories.

To meet their needs, the Laboratory Automation System (LAS) has an automatic conveyor line that is compatible with not only its own products, but also other manufacturers’ instruments.

There are few manufacturers that possess technologies for producing systems for connecting their own products and other manufacturers’ products freely and conveying them. Accordingly, the company occupies about 30% of the Japanese market.

The sales staff of the company not only delivers equipment, but also proposes a layout for the most efficient testing with 3D CAD or the like, while considering the area and shape of a laboratory.

All above, the company can offer optimal one-stop solutions for preparing necessary products in a laboratory, installing and operating equipment while proposing a layout. This is highly evaluated by client hospitals.

Advanced technologies in specific fields

A&T Corporation handles products mainly for “electrolyte tests” and “glucose tests.” Especially, its advanced technology for electrolyte analyzers can be verified by the fact that its products are supplied to JEOL, which is a leading manufacturer of measurement devices, including medical instruments, and Siemens, which is a large global company.

As mentioned in the section of the market environment, Japanese medical Analyzers is highly competent in the world, and A&T Corporation contributes to the competitiveness of Japanese products.

1-6 ROE analysis

| FY Dec.12 | FY Dec.13 | FY Dec.14 | FY Dec.15 | FY Dec.16 | FY Dec.17 | FY Dec.18 |

ROE (%) | 12.2 | 10.7 | 9.5 | 15.7 | 10.9 | 10.4 | 7.4 |

Ratio of net income to sales [%] | 5.60 | 5.11 | 4.76 | 8.28 | 6.37 | 6.54 | 4.97 |

Total asset turnover ratio [times] | 1.02 | 0.98 | 1.00 | 1.04 | 1.03 | 0.92 | 0.84 |

Leverage [times] | 2.14 | 2.13 | 1.99 | 1.83 | 1.67 | 1.73 | 1.79 |

ROE for the term ended December 2018 was below 8%, mainly due to the recording of relocation costs of manufacturing facilities and losses on cancellation of service contracts as extraordinary losses. The estimated ratio of net income to sales for the term ended December 2019 is 6.4%.

2.First Half of Fiscal Year ending December 2019 Earnings Results

(1)Consolidated Business Results

| 1H FY 12/ 18 | Ratio to sales | 1H FY 12/ 19 | Ratio to sales | YoY | Compared with the initial forecasts |

Sales | 4,065 | 100.0% | 5,255 | 100.0% | +29.3% | +5.1% |

Gross profit | 1,951 | 48.0% | 2,262 | 43.0% | +15.9% | - |

SG&A | 1,800 | 44.3% | 1,840 | 35.0% | +2.2% | - |

Operating Income | 151 | 3.7% | 421 | 8.0% | +178.9% | +18.8% |

Ordinary Income | 151 | 3.7% | 411 | 7.8% | +170.8% | +17.5% |

Net Income | 97 | 2.4% | 310 | 5.9% | +220.0% | +24.2% |

*Unit: million yen

Sales and profit grew, exceeding the estimates, with sales in the first half hitting a record high.

Sales were 5,255 million yen, up 29.3% year on year. The sales of diagnostic reagents dropped, but the sales of original products, including clinical testing devices and systems and supplies, were healthy, and the sales in the first half hit a record high.

Operating income was 421 million yen, up 178.9% year on year. Due to the product mix, cost ratio rose 5 points, but outsourcing expenses decreased, so the augmentation of SG&A expenses was not significant.

Current net profit was 310 million yen, up 220.0% year on year. The cost for relocating equipment from Shonan Factory to the new building at Esashi Factory decreased.

Both sales and profit exceeded the initial estimates.

The ratios of direct and virtual overseas sales, on which the company puts importance for growth, were 5.8% and 23.8%, respectively.

The sales to China, which grew considerably in the previous term, were as sluggish as 200 million yen (780 million yen in the previous term), due to the changes in the Chinese financial environment and the inventory adjustment of Runda, which is an OEM client, in China. This affected the results.

(2)Sales of each product series

Product series | 1H FY Dec. 18 | Composition Ratio | 1H FY Dec. 19 | Composition Ratio | YoY |

Clinical Testing devices and Systems | 1,938 | 47.7% | 2,751 | 52.4% | +42.0% |

Analyzers | 241 | 6.0% | 330 | 6.3% | +36.9% |

Laboratory Information System (LIS) | 1,179 | 29.0% | 1,461 | 27.9% | +23.9% |

Laboratory Automation System (LAS) | 517 | 12.7% | 959 | 18.2% | +85.4% |

Diagnostic reagents | 1,180 | 29.0% | 1,074 | 20.4% | -9.0% |

Supplies | 846 | 20.8% | 1,060 | 20.2% | +25.3% |

Others | 99 | 2.5% | 369 | 7.0% | +269.4% |

Total | 4,065 | 100.0% | 5,255 | 100.0% | +29.3% |

*Unit: million yen

Clinical Testing devices and Systems

The sales of analyzers rose, due to the growth of overseas sales in the electrolyte business, direct sales in the glucose business, and OEM sales in the coagulation business.

The sales of laboratory information system increased thanks to the growth of demand for update of projects, etc.

The sales of laboratory automation system increased as the company made large-scale transactions in Japan, although sales were reduced by the changes in the Chinese financial environment, the inventory adjustment of Runda, which is an OEM client, in China, etc.

Diagnostic reagents

The sales to some OEM clients in the electrolyte business, the OEM sales in the immunity business, and direct sales in each business decreased.

Supplies

The sales volume of the managed pre-analysis module (MPAM+) increased in the laboratory automation system business, and the sales of sensors to existing OEM clients in the electrolyte business increased.

Others

The sales of purchased products increased, following large-scale transactions for laboratory information system and laboratory automation system.

(3)Financial standing and cash flows

Main Balance Sheet

| End of December 2018 | End of June 2019 |

| End of December 2018 | End of June 2019 |

Current Assets | 8,272 | 7,431 | Current liabilities | 4,656 | 3,727 |

Cash | 1,051 | 1,371 | Payables | 1,536 | 932 |

Receivables | 5,354 | 3,886 | ST Interest Bearing Liabilities | 2,100 | 1,900 |

Inventories | 1,795 | 2,069 | Noncurrent liabilities | 776 | 623 |

Noncurrent Assets | 4,339 | 4,275 | LT Interest Bearing Liabilities | 750 | 600 |

Tangible Assets | 3,794 | 3,716 | Total Liabilities | 5,432 | 4,351 |

Intangible Assets | 38 | 37 | Net Assets | 7,179 | 7,355 |

Investment, Others | 505 | 521 | Total liabilities and net assets | 12,611 | 11,706 |

Total assets | 12,611 | 11,706 | Total Interest-bearing Liabilities | 2,850 | 2,500 |

|

|

| Capital Adequacy Ratio | 56.9% | 62.8% |

*Unit: million yen

Current assets dropped 841 million yen from the end of the previous term, due to the decline in trade receivable, etc. Noncurrent assets decreased 63 million yen from the end of the previous term. Total assets decreased 905 million yen from the end of the previous term to 11,706 million yen.

Total liabilities dropped 1,081 million yen from the end of the previous term to 4,351 million yen, due to the repayment of debts, etc.

Net assets grew 176 million yen from the end of the previous term to 7,355 million yen, due to the increase in retained earnings, etc.

As a result, equity ratio rose 5.9% from 56.9% at the end of the previous term to 62.8%.

Cash Flow

| 1H FY 12/ 18 | 1H FY 12/ 19 | Increase/decrease |

Operating Cash Flow | 546 | 876 | +330 |

Investing Cash Flow | -93 | -56 | +37 |

Free Cash Flow | 452 | 819 | +367 |

Financing Cash Flow | -285 | -500 | -215 |

Term End Cash and Equivalents | 1,324 | 1,371 | +46 |

*Unit: million yen

The surpluses of operating CF and free CF increased, due to the growth of quarterly net profit before taxes, etc. The deficit of financing CF augmented due to the repayment of debts. The cash position was almost unchanged.

3.Fiscal Year ending December 2019 Earnings Forecasts

(1)Consolidated earnings forecasts

| FY 12/ 18 | Ratio to sales | FY 12/ 19 Est. | Ratio to sales | YoY | Progress rate |

Sales | 10,430 | 100.0% | 11,200 | 100.0% | +7.4% | 46.9% |

Gross profit | 4,446 | 42.6% | 4,770 | 42.6% | +7.3% | 47.4% |

SG&A | 3,671 | 35.2% | 3,760 | 33.6% | +2.4% | 48.9% |

Operating Income | 774 | 7.4% | 1,010 | 9.0% | +30.4% | 41.8% |

Ordinary Income | 768 | 7.4% | 1,000 | 8.9% | +30.1% | 41.1% |

Net Income | 518 | 5.0% | 720 | 6.4% | +39.0% | 43.1% |

*The forecasted values were provided by the company. Unit: ¥mn

No revision to the earnings forecast. Sales and profit are estimated to grow.

There is no revision to the earnings forecast. Sales are estimated to be 11.2 billion yen, up 7.4% year on year. Some businesses in China are delayed, but this will be covered by the increase of domestic transactions in the IT and automation support business. The sales of original products, too, will increase. Gross profit is projected to rise 7.3% year on year, due to the settling-down in man-hours for new products of laboratory information system, the decrease of purchased products, etc.

Operating income is forecasted to rise 30.4% year on year to 1,010 million yen. Due to the recruitment of personnel for sustainable growth and the development of new products for laboratory automation system, etc., SG&A expenses are estimated to increase 2.4% year on year, but it will be offset by the rise in gross profit.

The dividend is estimated to be 24 yen/share, unchanged from the previous term. The estimated payout ratio is 20.9%.

(2)Sales for each product series

Product series | FY Dec. 18 | Composition rate | FY Dec. 19 Est. | Composition rate | YoY | Compared with the revised forecasts | Progress rate |

Clinical Testing devices and Systems | 5,448 | 52.2% | 6,480 | 57.9% | +18.9% | +3.3% | 43.9% |

Analyzers | 523 | 5.0% | 700 | 6.3% | +33.8% | -5.4% | 44.6% |

Laboratory Information System (LIS) | 2,968 | 28.5% | 3,200 | 28.6% | +7.8% | +2.9% | 47.0% |

Laboratory Automation System (LAS) | 1,957 | 18.8% | 2,580 | 23.0% | +31.8% | +6.6% | 39.6% |

Diagnostic reagents | 2,265 | 21.7% | 2,200 | 19.6% | -2.9% | -4.3% | 46.7% |

Supplies | 1,819 | 17.4% | 2,020 | 18.0% | +11.1% | +4.7% | 54.9% |

Others | 897 | 8.6% | 500 | 4.5% | -44.3% | -28.6% | 52.7% |

Total | 10,430 | 100.0% | 11,200 | 100.0% | 7.4% | 0.0% | 46.9% |

*Unit: million yen

The estimate for total sales has not been revised, but the estimates for sales of respective product groups have been revised.

*As for analyzers and diagnostic reagents, the overseas sales in the electrolyte business and the direct sales in the glucose business will be healthy like in the first half, but the pace of sales will decline gradually.

*As for laboratory information system, the demand for renewal and new installation will be strong. We will concentrate on the establishment of an engineer system for coping with the growth of demand.

As for laboratory automation system, the OEM sales to Runda in China are stagnant, but it is expected that the demand inside Japan will grow and the company will make large-scale transactions in South Korea.

*As for supplies, the sales of supplies for laboratory automation system outside Japan and sensors to each OEM client are estimated to grow.

*In the first half, the sales of purchased products increased, but the company will reduce the sales of purchased products and concentrate on the sale of its original products in accordance with the policy of medium-term management plan.

4.Medium-Term Management Plan (FY Dec. 2018 to FY Dec. 2020) Progress

(1) Recognition of the business environment

There is no significant change from the time when the current medium-term management plan was formulated.

<Business environment analysis>

| Blood testing business | IT and automation support business |

Business environment | *Due to the change in the sales environment, the sales to some OEM clients may decline. *The domestic testing markets for electrolytes, glucose, etc. will reach a plateau. *The growth of the overseas market, especially China, is remarkable. | *The scale and competition of the domestic market have not changed significantly, and are on a plateau. Overseas demand is high. *The amount per order is large, but the period until the next update is as long as 5 to 10 years. *Once a product is installed, it tends to be adopted again at the time of the next update (relatively easy to defend). On the other hand, it is relatively difficult to reel in customers from competitors (difficult to attack). *Recently, the overseas demand for LAS has been strong. |

*The domestic test markets for electrolytes, glucose, etc. have reached a plateau, but in September 2018, the company signed a contract for business alliance in the field of the clinical test field with ARKRAY, Inc. (Kyoto City), which is a pioneer in diabetes testing, to pursue new business chances.

*While the Japanese market is estimated to grow by about 1%, the overseas market is projected to grow by 5-6%.

(2) Progress toward important objectives

1 | To deal with the fact that sales are concentrated on specific OEM clients |

2 | To compensate for the decline in sales to some OEM clients, and find new clients |

3 | To increase gross profit (increasing the sales of original products) |

4 | To reduce the cost for securing product quality |

5 | To put the business in the Chinese market, which is growing rapidly, on track as soon as possible |

6 | To reform ways of working and train personnel |

The company got closer to the objectives 1 and 2 steadily.

As for the objective 3, the sales of original products are growing as planned.

As for the objective 4, the company will establish the quality assurance division, to improve product quality at Esashi Factory, while reducing costs.

As for the objective 5, business performance was behind schedule in the first half of this term, due to the changes in the Chinese financial environment.

(3) Progress of Basic Policy

Basic Policy | Situation |

To increase the ratio of sales of original products, and improve profitability | The sales of original products are increasing as planned, and are estimated to grow about 1 billion yen year on year. Thus, gross profit is projected to rise 300 million yen year on year to 47.7 million yen. |

To enhance business operation in China, and boost the ratio of overseas sales | The business performance is behind schedule, due to the changes in the Chinese financial environment, but the business direction has not been changed. |

To cement the cooperation between development and manufacturing sections, and establish systems for developing and producing high-quality products stably | The company continues efforts to improve yield ratio and reduce fraction defective. |

To reform ways of working and train personnel thoroughly | The company started a company-wide training program. |

(4)Numerical goals and progress status

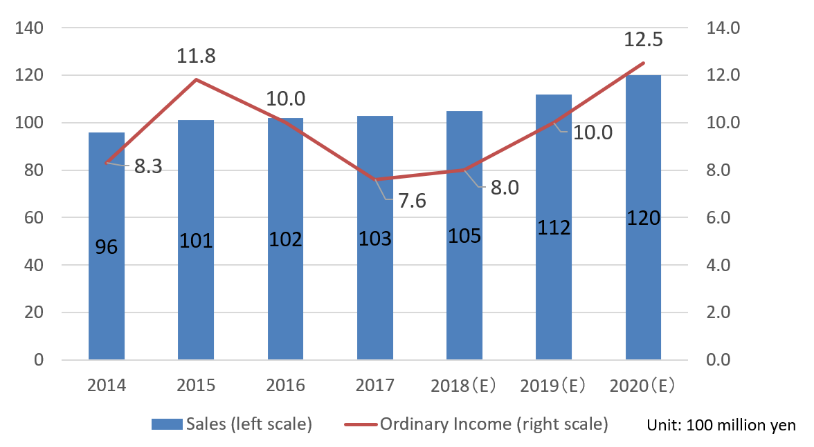

| FY 12/ 18 | FY 12/ 19 | FY 12/ 20 | |

Plan | Act. | Plan | Plan | |

Sales | 10,500 | 10,430 | 11,200 | 12,000 |

Ordinary Income | 800 | 768 | 1,000 | 1,250 |

Ordinary margin to sales | 7.6% | 7.4% | 8.9% | 10.4% |

Direct sales rate in overseas | - | 12.2% | Over 10% | Over 10% |

*Unit: million yen

*FY December 2018

Although the number of clinical testing devices and systems increased, OEM sales of sensors remained sluggish due to the response to overseas regulations and holding-off buying from price revision. Ordinary income did not reach the target due to a decrease in sales of sensors and initial costs for new products exceeding the plan. However, the ratio of overseas sales exceeded 10% for the first time with strong Chinese OEMs sales for the laboratory automation system. As a result, it reached the target a year ahead of the plan.

*FY December 2019

The compositions of products and sales differ from the initial plan, but the overall goals are unchanged. In addition to the decrease of man-hours for dealing with new products and the full-scale production at the new building of Esashi Factory, the company will continue activities for sustainable growth, including the establishment of a system for coping with the growth of demand for clinical testing devices and systems.

*FY December 2020

Using the actions for the first and second years of the medium-term management plan as steps, it will maintain the plan to achieve the largest sales and profit. It is planning to establish the next medium-term management plan.

5.Interview with President Misaka

“The sales of original products will increase as planned.”

*In the first half of this term, the sales of purchased products increased thanks to the large-scale transactions for the laboratory information system and laboratory automation system. In the full term, it is expected that the sales of original products will increase as planned, to improve profitability.

“The business in China, which was sluggish in the first half, will recover in the second half.”

*The OEM sales to Runda in China, which grew significantly in the previous term, decreased, as the activities of Runda were stagnant in the first half of this term due to the changes in the Chinese financial environment, etc. In China, it is difficult to avoid the changes in the business environment due to governmental policies, but it was decided that Runda would be publicly funded, and it is expected that its management system will become more stable.

The company will continue the strategy of selling V4 as a packaged product by utilizing the customer base and service system of Runda.

Business performance is expected to recover in the second half of this term or later.

*The company mainly offers a packaged service providing the basic pattern of establishment, but it is also necessary to meet customer needs accurately for business growth. Accordingly, the improvement of the basic pattern is somewhat necessary, and the company will enrich its lineup while considering the balance with profitability.

*In order to increase sales, it is necessary to enhance marketing and educational support for service engineers, so the company started the training of Chinese staff at Esashi Factory.

The level of staff of Runda is higher than imagined, and we can expect that their sales will grow from now on.

“The business alliance with ARKRAY is progressing steadily.”

*The business alliance with ARKRAY, which is a pioneer in diabetes testing, in the clinical testing field is progressing steadily.

*As for the collaboration in the glucose testing field, the company offered the glucose analyzer “GA09II” to ARKRAY and released a collaborative product in February of this year.

As for the cooperation for laboratory information system, they started discussions about concrete systems.

In addition, the company is thinking of supplying products in a broad range of fields and selling products outside Japan, but it plans to first cooperate in the business of coagulation analyzers for animals.

*It is expected to contribute to actual revenue next term or later. The company considers it as a chance to expand its share in the domestic glucose testing market, which is forecasted to reach a plateau, and will conduct collaborative business in a broad range of fields.

“Cultivation of the Chinese market with open strategies”

*The scale of the Japanese market of clinical testing systems is 10 billion yen, while that of the overseas market is as huge as 770 billion yen. Especially, the scale of the Chinese market is expected to grow significantly with an annual rate of 20%.

*In the Chinese market, major European and American companies, including Beckman Coulter, Roche, and Abbott, had a lead with “the closed strategy,” in which they produce equipment, conveying systems, and reagents to be delivered to laboratories all by themselves.

*However, as the market is rapidly growing, the conventional closed strategy is no longer satisfactory, and a system that has a higher degree of freedom is demanded, and “the open strategy,” in which a product lineup is not limited to original devices, but also includes other companies’ devices, is now highly evaluated.

*In the Chinese market of clinical testing systems, the two strategies are competing with each other.

Due to the rapid changes in the external environment, the OEM sales to Runda were sluggish in the first half of this term, but the company plans to actively cultivate the Chinese market by taking advantage of the stable business of Runda and the service of offering optimal solutions, including installation, operation, and layout design, to meet the needs from hospitals and laboratories on a one-stop basis.

*It is indispensable to expand the business in China, in order to achieve a ratio of virtual overseas sales of over 50%, which is a mid-term goal.

As its achievements are highly evaluated, some would-be partners have approached the company, and the company will expand the business for Runda, and also the business in other fields.

6.Conclusions

Sales and profit grew considerably year on year, exceeding the initial estimates. The OEM sale to Runda in China is still small-scale, so even if the OEM sales do not reach the initial estimate, it will be possible to cover it with domestic transactions, etc. In order for the company to grow further for commemorating the 50th anniversary in 2028, it is essential to cultivate overseas markets, including China, which is growing rapidly. How much the company will recover its performance in the second half while considering its business from the next term is noteworthy. In addition, the important step for achieving an ordinary income rate of over 10% is to increase ordinary income rate to 8.9% this term.

<Reference1: Outline of Medium-Term Management Plan>

In May 2018, as a celebration of the 40th anniversary of its founding, and in anticipation of its 50th anniversary in 2028, the company has formulated a three-year medium-term management plan starting this term.

Sales in the last three terms have been mostly unchanged, and ordinary income has declined after reaching a peak in FY Dec. 2015, but with the theme of “building a framework for sustainable growth,” the company aims to “shift toward an increasing trend in sales and profits, and quickly recover ordinary income.”

<Target Figures>

For the term ending Dec. 2020, the company mentioned “sales of 12 billion yen or greater, an ordinary income rate of over 10%, and an overseas direct sales ratio of 10% or more.”

<Analysis of the business environment, etc. at the time of formulation of the medium-term management plan and status of each business>

| Blood testing business | IT and automation support business |

Sales | *OEM sales were sluggish due to price revision, etc. *Sales of supplies and sensors increased as the number of customers increased. *Domestic clinical markets, such as the electrolyte and glucose markets, leveled off. | *LIS started full-scale introduction of new products, and grew due to focus on sales. *Large-scale LAS transactions are decreasing (lower average unit price per transaction). *Sales increased for purchased products accompanying large transactions. |

Profit (Main reason for a decreasing trend in profit) | *OEM sales were sluggish due to price revision, etc. | *In FY2017, carried out intensive investment for development of the LIS subsystem. *There was strong price competition for large transactions both domestically and overseas. *Outsourcing expenses (outsourcing of system engineers) increased. *Sales increased for purchased products accompanying large transactions. |

Business Environment | *Due to changes in the sales environment, sales to some OEM clients may decrease. *Domestic clinical markets, such as the electrolyte and glucose markets, leveled off. *The overseas market (especially China) is growing rapidly. | *There is no major change in the domestic market both in size and competitive situation, and it is in a state of equilibrium. Overseas demand is high. *While the value of each order is large, the time until the next renewal can be as long as 5 to 10 years. *Once the product is introduced, it is easy to sell subsequent renewals of the product (relatively easy to secure repeat business). On the other hand, it is relatively difficult to persuade new customers to switch to the company’s products. *In recent years, overseas demand for LAS is particularly high. |

Intensive measures | *To increase OEM clients for electrolytes, and develop stable commercial distribution to existing OEM clients. *To promote technological development for reducing costs. *To utilize the new building of Esashi Factory. | *LIS started full-scale introduction of new products, and grew due to focus on sales. *Large-scale LAS transactions are decreasing (lower average unit price per transaction). *Sales increased for purchased products accompanying large transactions. |

Progress of each business | *Start of supply of electrolyte units to a new OEM client in Japan *The commercial channels of the electrolyte unit with two new OEM clients inside and outside Japan are under development. *Development of technologies for improving the quality and yield rate of sensors *Completion of transfer of some clinical reagents from Shonan Factory to Esashi Factory | (LIS) *Introduction of new subsystems (blood transfusion, bacteria tests, infectious diseases.) to the first user *Transactions for both installation and renewal increased. (LAS) *In Japan, a large-scale module to refrigerate samples, which will be added to the product lineup, is completed and introduced to first users. *The company signed a distributorship contract with a Chinese company (Runda), and started OEM sale. |

The company believes that overseas expansion is crucial for both businesses in order to achieve the objective.

<Reference2:Regarding Corporate Governance>

Organization type and the composition of directors and auditors

Organization type | Company with audit and supervisory committee |

Directors | 11 directors, including 2 external ones |

Corporate Governance Report

Last update date: March 29 2019

<Basic policy>

As a top priority, our company aims to secure the effectiveness of corporate governance and actualize fair business administration by putting importance on the transparency, fairness, and speed of decision making and business execution. In addition, we adopted the system of audit and supervisory committee in order to separate the supervision and execution of business administration, actualize highly transparent management, and streamline the decision-making process of the board of directors.

<Reasons for Non-compliance with the Principles of the Corporate Governance Code (Excerpts)>

The company fully follows the 5 items of basic principles of the corporate governance code.

This report is intended solely for information purposes, and is not intended as a solicitation for investment. The information and opinions contained within this report are made by our company based on data made publicly available, and the information within this report comes from sources that we judge to be reliable. However, we cannot wholly guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness or validity of said information and opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration. Copyright (C) 2019 Investment Bridge Co., Ltd. All Rights Reserved. |