Bridge Report:(7199)Premium Group Second quarter of fiscal year ending March 2022

![]()

President and CEO Yohichi Shibata | Premium Group Co., Ltd. (7199) |

|

Company Information

Market | TSE 1st Section |

Industry | Other financial business (finance and insurance) |

President and CEO | Yohichi Shibata |

HQ Address | 19th Floor, The Okura Prestige Tower, 2-10-4, Toranomon, Minato-ku, Tokyo |

Year-end | March |

Homepage |

Stock Information

Share Price | Share Outstanding | Market Cap. | ROE (Act.) | Trading Unit | |

¥3,630 | 13,346,990 shares | ¥48,449 million | 38.3% | 100 shares | |

DPS (Est.) | Dividend Yield (Est.) | EPS (Est.) | PER (Est.) | BPS (Act.) | PBR (Act.) |

¥50.00 | 1.4% | ¥186.99 | 19.4x | ¥563.12 | 6.4x |

*The share price is the closing price on December 15, 2021. The number of shares outstanding, DPS and EPS are from the financial results for second quarter of fiscal year ending March 2022. ROE and EPS are from the previous results.

Consolidated Earnings Trends (IFRS)

Fiscal Year | Operating Income | Pretax profit | Net Income | Profit attributable to owners of parent | EPS (¥) | DPS (¥) |

March 2018 (Act.) | 9,065 | 1,979 | 1,293 | 1,293 | 107.44 | 85.00 |

March 2019 (Act.) | 10,759 | 2,097 | 1,391 | 1,388 | 113.08 | 85.00 |

March 2020 (Act.) | 14,016 | 2,604 | 1,452 | 1,466 | 112.33 | 44.00 |

March 2021 (Act.) | 17,825 | 3,463 | 2,393 | 2,383 | 186.74 | 46.00 |

March 2022 (Est.) | 21,446 | 3,500 | 2,422 | 2,409 | 186.99 | 50.00 |

*The forecast is from the company. Unit: million yen, yen. In August 2017, a 100-for-1 stock split was conducted. In April 2019, a 2-for-1 stock split was conducted. (EPS is revised retroactively.)

This Bridge Report reviews the overview of Premium’s earnings results of second quarter of fiscal year ending March 2022 and so on.

Table of Contents

Key Points

1.Company Overview

2.Second Quarter of Fiscal Year ending March 2022 Earnings Results

3.Fiscal Year ending March 2022 Earnings Forecasts

4. Conclusions

<Reference1: >

<Reference2: Corporate Governance>

Key Points

- The operating income for the second quarter of the term ending March 2022 was 10,104 million yen, up 20.5% year on year, and pretax quarterly profit was 1,915 million yen, down 4.3% year on year. Profit increased 31.5% year on year after adjustment for 545 million yen in one-time gains (negative goodwill, etc.) in the same period of the previous term. Due to the stagnant production of new cars, used cars are in short supply and their prices are skyrocketing, but both credit transactions and automobile warranty trading have exceeded the market averages.

- There is no change in the earnings forecasts. Operating income is expected to rise 20.3% year on year to 21,446 million yen, while pretax profit is projected to rise 1.1% year on year to 3.5 billion yen. Pretax profit excluding one-time profit or loss is forecast to increase 16.4% year on year. The progress of revenue and profit have been higher than the forecasts for the current term, but the full-year forecasts remain unchanged because of the uncertain future outlook due to the shortage of semiconductors in the automobile market and the resultant delay in new car production. Dividends will be 25 yen per share for both the interim period and the end of the term and the annual total is expected to be 50 yen per share, up 4 yen per share year on year. The projected payout ratio is 26.9%.

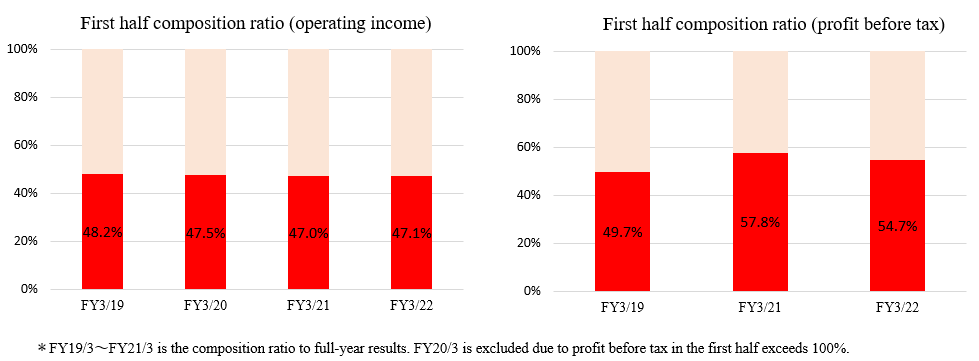

- The progress rate in the first half was 47.1% for operating income and 54.7% for pretax profit. However, regarding pretax profit, the ratio of the actual profit for the core business, excluding one-time profit in the term ended March 2021, was 42.1% and the progress rate for this term was significantly high compared to those in the past several years. The company's operating income is almost the same as that in a typical year and appears to be making good progress at this point. Although the full-year forecasts remain unchanged due to the uncertain impact of reduced production by automobile manufacturers on the used automobile market due to the shortage of semiconductors, we will closely monitor market trends and the company's business performance from the third quarter onward.

- Regarding the mid-term management plan VALUE UP 2023, the DX (Digital Transformation) strategy, one of the priority measures, appears to be making steady progress. We would like to expect their progress and outcomes.

1. Company Overview

Premium Co., Ltd., which is the core enterprise operating the Financial Business, Premium Warranty Services Co., Ltd., the core enterprise conducting the Automobile Warranty Business, Premium Mobility Services Co., Ltd., the core enterprise offering Auto Mobile Services Business, and over 15 group companies inside and outside Japan provide automobile-related services, including Credit Finance services and Automobile Warranty services for the purchase of used cars. Premium Group Co., Ltd. manages the corporate group and deals with accompanying and related tasks as a holding company.【1-1. Corporate history】

Mr. Yohichi Shibata used to handle auto loans in a leading financing company, and believed in the high affinity between automobiles and finance and its growth potential. He joined Gulliver International Corporation (current name: IDOM Inc.), which was his client company, following their request. In 2007, he established G-ONE Credit Services Co., Ltd., which is the predecessor of Premium Co., Ltd., a second-tier subsidiary of Gulliver International Cooperation, and started providing services. However, the business environment surrounding Gulliver International Cooperation changed, and the business was discontinued, and its shareholders shifted to the SBI Group and the Marubeni Group. In that situation, a desirable capital policy was actualized while maintaining the forte of “independence” from financial institutions, which is the greatest competitive advantage, based on the negotiation skill of President Shibata, and a holding company system was adopted with Premium Group Co., Ltd. being a holding company in 2016. Their business performance improved steadily with the rich product lineup as an independent corporate group and the advanced knowledge of auto finance, and the company was listed in the second section of Tokyo Stock Exchange (TSE) in 2017 and then in the first section of TSE in 2018.

【1-2. Corporate ethos】

(Missions)

Contribute to the construction of a prosperous society by providing top level financing and services to the world. |

By further improving our financing and services, and spreading them across the world, we will create a prosperous society. |

|

We will foster employees who are broadminded, have a positive outlook, and assiduously work their way towards creating results. |

We will not give up before we start by thinking we cannot do something, or something is not possible. We will promote innovation with creative ideas and great ambition, and forge ahead to the next step ourselves. |

The management policy is to improve corporate value in the medium/long term, by fulfilling the above missions and developing human resources who can take over these missions.

【1-3. Business description】

The corporate group provides clients, including used car dealers and car maintenance shops, with credit finance, automobile warranty, auto mobility services (such as the sale of auto parts, wholesale of vehicles, sales of software for task management at maintenance shops, maintenance, and sheet-metal work of automobiles), etc. Also, in Thailand, Indonesia, and the Philippines, they offer credit finance, automobile warranty, and so on via overseas affiliates. Since FY 3/22, the corporate group has classified the three business segments, which are Finance, Automobile Warranty, and Auto Mobility Business, and has disclosed the earnings results of each.

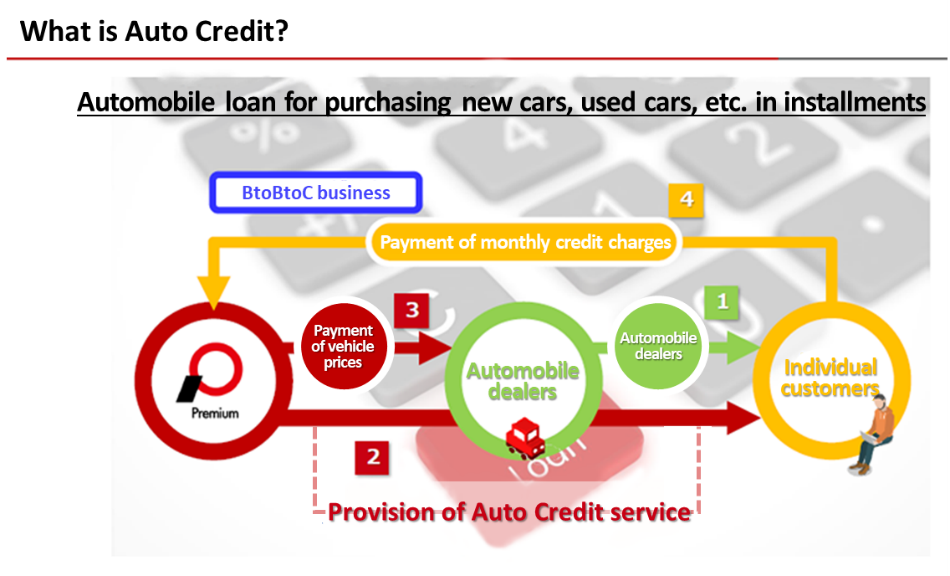

(1) Finance Business

As a business segment run by one of the company’s major subsidiaries, Premium Co., Ltd., the Finance Business provides services related not only to loans for purchasing automobiles (auto credit), but also to loans for purchasing photovoltaic power generation systems (ecology credit), shopping credit and such. The business also offers auto lease services targeting individual customers and debt recovery services on consignment.

(Taken from the reference material of the company)

Most of credit receivables are off-balance-sheet because they are affiliated loans with banks (which will be described below). For cases that do not satisfy the loan conditions of banks, such as the case in which the representatives of small and medium-sized enterprises purchase automobiles in corporate name and the case in which the total amount of credits exceeds a certain amount, the Premium Group’s own funds are used, and they are posted in balance sheets as receivables. Such receivables are from “out-of-pocket funds” differing from those from affiliated loans, but the commissions for installments paid by credit users and gross profit after deducting procurement costs are at almost the same level. The financial guarantee contract posted in the credit side of the balance sheet represents future (unrealized) revenues of the credit business, and when credits are repaid, they are posted as operating income. Its partner financial institutions are SBI Sumishin Net Bank, Ltd., ORIX Bank Corporation, Rakuten Bank, Ltd., and GMO Aozora Net Bank, Ltd. For affiliated loans, Premium Co., Ltd. screens credit users, pays credit charges and sales promotion expenses to affiliated dealers, and receives credit charges from partner banks about 10 days later. The company serves as a co-signer for each credit contract, undertakes the task of collecting credit charges, and receives them as well as installment fees from credit users. As for receivables, trade credit insurance is taken out for most receivables, so even if some receivables become irrecoverable, they will be covered by the insurance, so as not to cause any loss to the company. Accordingly, the company posts insurance premiums as operating costs every term. The insurance premiums vary according to the number of irrecoverable receivables.

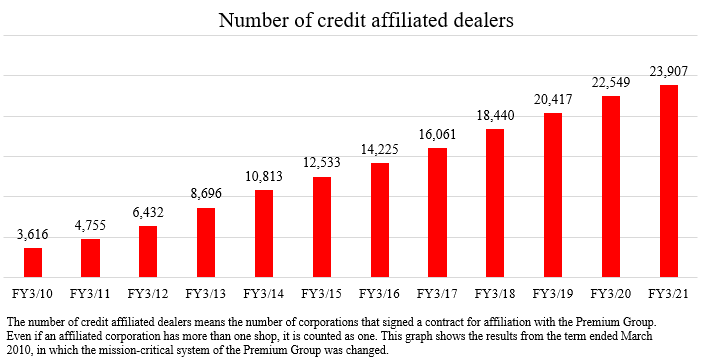

The sales of the term ended March 2021 was 166.4 billion yen, The balance of credit receivables as of the end of the same term was 361.4 billion yen. the ratio of delinquent receivables (over three months) as of the end of the term ended March 2021 was as low as 0.91%. As a characteristic, the average balance of credit receivables for individuals is as small as 1.173 million yen and its risk has been dispersed. For collecting receivables, the company approaches credit users early and utilizes SMS and Auto call system, etc. to minimize default cases and streamline the collection process. In April 2020, Central Servicer Corporation joined the Premium Group, boosting its capability of collecting receivables. The number of affiliated dealers has been increasing steadily, standing at 23,907 as of the end of the term ended March 2021, up 6.0% year on year. While seeking new affiliated dealers, the company is promoting other services, such as automobile warranty, targeting existing affiliated dealers, and concentrating on the improvement of utilization rate. In addition, the company is promoting dealers that are affiliated but not using their services to use its services by utilizing the contact center (outbound marketing).

The company is also focusing on increasing members for its PFS Premium Club, a paid subscription service that provides services with higher added value to car dealers.

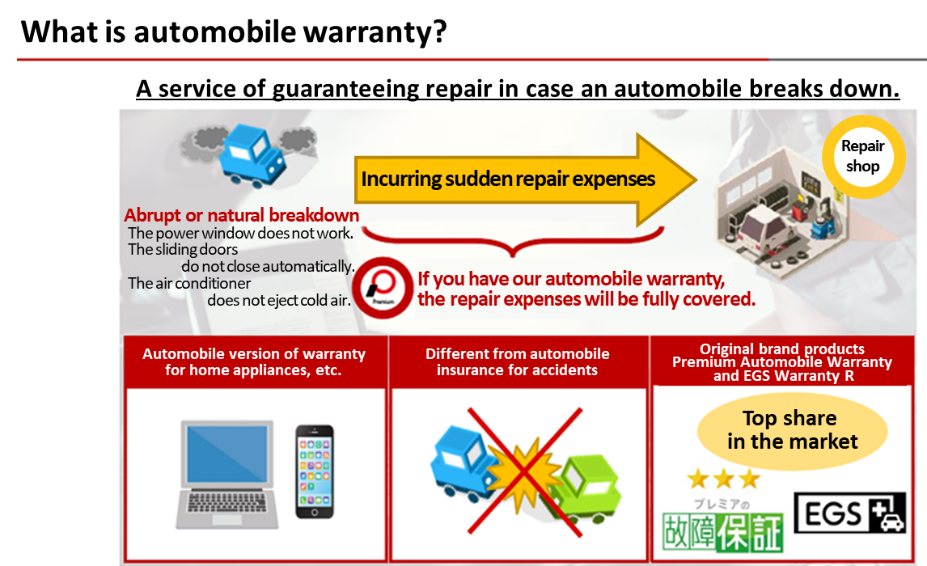

(2) Automobile Warranty Business

In a case where a credit user pays a warranty fee for this service when purchasing an automobile from an affiliated dealer (such as a used car dealer) of the Premium Group, he/she will be able to receive repair services free of charge within the predetermined coverage of the warranty if the purchased automobile breaks down.

(Taken from the reference material of the company)

Via affiliated dealers, the automobile warranty of Premium Warranty Services Co., Ltd. of the Premium Group is offered to those who have purchased an automobile. By accumulating and analyzing data on the broken-down cars’ travel distances, age, and detail of repairs, it is possible to design more appropriate warranties and prices. The Premium Group has designed products and set prices based on the accumulated big data on repairs, including about one million automobile warranty contracts held by Premium Warranty Services Co., Ltd.

The insurance provided by non-life insurance companies is designed to cover accidents, etc., but the automobile warranty only covers natural breakdowns, and these do not compete against each other. The automobile warranty covers a maximum of 397 parts, and the company offers about 1,000 different warranty products with different coverages and warranty periods. The automobile warranty dispels the anxiety over the purchase of a used car and is an indispensable product when purchasing a used car. In addition, the premiums (automobile warranty fee) based on the warranty period is received in a lump sum through advance payment, and the revenues are calculated by dividing it proportionally over the period.

Automobile warranties are classified into their original brands, Premium Automobile Warranty and EGS Warranty, and their customized version, OEM Warranty. The OEM Warranty is classified into Car Sensor After-sales Warranty, which is provided by the affiliates using the used car media, Car Sensor, published by Recruit Marketing Partners Co., Ltd., and covers the vehicles listed in Car Sensor, and other OEM Warranty in which target vehicles and coverages are customized for medium and large-sized used car dealers. To deal with repairs, the company assigns employees who are qualified as auto technicians to call centers for accepting orders for repair, and they directly communicate with warranty beneficiaries and maintenance shops. Accordingly, automobile warranty can be applied accurately and swiftly. Thus, this system brings a sense of reassurance to warranty beneficiaries.

In addition, regarding repairs corresponding to the cost of the warranty service, the company can reduce repair costs and prevent unnecessary repairs by such measures as procurement of recycled and rebuilt parts through subsidiaries, preferential warehousing of such parts through the company's network of repair shops, operation of directly managed repair shops in some areas, and the use of FAINES*.

*FAINES Information database on maintenance manuals, repair cases, etc. provided by Japan Automobile Service Promotion Association (JASPA) for car maintenance enterprises.

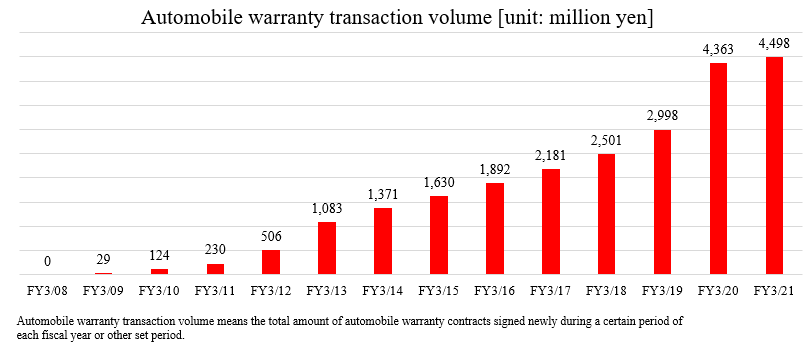

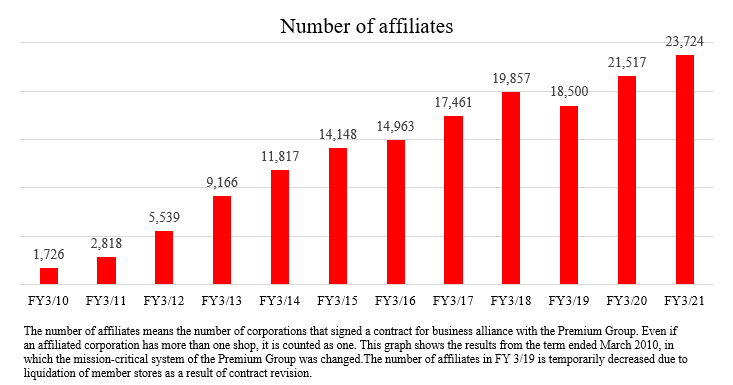

The volume of automobile warranty transactions in the term ended March 2021 stood at 4,498 million yen. The number of affiliated dealers and maintenance shops at the end of the term was 23,724. The company is taking measures to encourage automobile dealers, including used car dealers, to use the automobile warranty service as it does to the dealers affiliated with the auto credit service.

Until now, sales have been expanded mainly by focusing on the marketing of in-house brand products. From the second half of the term ending March 2022, in order to expand sales of OEM products and other OEM products, the sales structure is being changed by assigning sales personnel specializing in these products.

In addition, cost ratio is being reduced by procuring recycled and rebuilt parts through the above subsidiaries and by utilizing the network of repair shops.

(3) Auto Mobility Business

In addition to credit finance and automobile warranty, the company operates a broad range of businesses related to the distribution of used cars. Currently, the company operates recycled parts business which distributes parts of used cars, reuse business which distributes repossessed vehicles and uses them inside the Premium Group, and repair business which offers maintenance services for inspecting and repairing automobiles and sheet-metal services for repairing scratches, dents, etc. on automobiles. All of them are environmentally friendly, and the company focuses on these businesses as “new 3Rs.”

In addition, a network for repair shops and a paid subscription system are being developed. The initial target for the network of repair shops was achieved ahead of schedule, increasing the number of companies to 3,160 and the number of paid subscription members to 104. By leveraging its auto mobility business, network of repair shops, and paid subscription system, the company is displaying the synergy between its finance and automobile warranty businesses to enhance its competitive advantage in each business. In the finance business, it is a cross-selling of finance services and auto mobility services. In the case of the automobile warranty business, as described above, automobile warranty repair is outsourced to a network of repair shops and a group of paid subscription members, and repair costs are reduced by procuring parts from group companies at low prices. The company will also create new businesses in the auto mobility business by combining big data and expertise obtained in the automobile warranty business.

The auto mobility business is the newest business among the three major businesses, but it is the fastest-growing field. Although it is still in an expansion phase, it moved into the black in the second quarter of the term ending March 2022.

(4) Regarding overseas business operation

The Premium Group applies the knowledge for credits, automobile warranty, maintenance, and sheet-metal work related to the sale of automobiles in Thailand, Indonesia, and the Philippines.

In Thailand, the company gives management and business consulting services to Eastern Commercial Leasing p.l.c., an equity-method affiliate conducting auto finance, and carries out automobile warranty and car maintenance businesses in Premium Services (Thailand) Co., Ltd., which is a joint venture with Eastern Commercial Leasing p.l.c. In Indonesia, PT Premium Garansi Indonesia, which is a joint venture with Sumitomo Corporation and the SinarMas Group, a local industrial conglomerate, offers consulting services about the development and design of automobile warranties. In the Philippines, Premium Warranty Services Philippines, Inc., which is a joint venture with Mitsui & Co., Ltd. and the GT Capital Group, a local industrial conglomerate, offers automobile warranties.

Additionally, used parts are exported to Tanzania and Russia etc. through subsidiaries.

【1-4. Characteristics and strengths】

The competitiveness of the company is attributable to the following three points.

(1) Mixed product lineup achieved by their independency from banks

The services which the competitors under the umbrella of banks can offer are limited to auto credit, auto lease, etc. due to the restrictions of law. Meanwhile, the Premium Group, which is independent from banks, can provide various products and services, including automobile warranty, to meet a broad range of needs from dealers and users.

As a result, the company has established a competitive advantage through convenience and mutual usage discount.

(2) Expertise in auto finance

By providing deep expertise in automobiles and finance fields, as well as products that combine automobiles and finance, the company can provide enhanced services that are unrivaled and create a competitive advantage.

(3) Firm marketing network covering the entire area of Japan

A nationwide network of sales offices in major cities and original contact centers (outbound sales) forms a strong network with member stores reaching almost 25,000 companies nationwide, thus forming a solid customer base.

【1-5. ROE analysis】

| FY 3/2019 | FY 3/2020 | FY 3/2021 |

ROE (%) | 24.8 | 27.4 | 38.3 |

Net Income to Sales Ratio (%) | 12.90 | 10.46 | 13.37 |

Asset Turnover Ratio (x) | 0.27 | 0.28 | 0.28 |

Leverage (x) | 7.11 | 9.50 | 10.15 |

In the medium-term management plan, VALUE UP 2023, the target return on equity (ROE) is 31.7% for the term ending March 2023.

The company intends to maintain a ROE of 20% or higher while pursuing an optimum business portfolio and streamlined business operations through the promotion of DX.

2. Second quarter of Fiscal Year ending March 2022 Earnings Results

【2-1. Consolidated Earnings (IFRS)】

| 2Q of FY 3/21 | Ratio to Operating Income | 2Q of FY 3/22 | Ratio to Operating Income | YoY |

Operating Income | 8,386 | 100.0% | 10,104 | 100.0% | +20.5% |

Other Income | 625 | 7.5% | 16 | 0.2% | -97.5% |

Operating expenses | 6,944 | 82.8% | 8,216 | 81.3% | +18.3% |

Quarterly pretax profit | 2,001 | 23.9% | 1,915 | 19.0% | -4.3% |

Quarterly net Income | 1,321 | 15.8% | 1,365 | 13.5% | +3.3% |

Quarterly profit attributable to owners of parent | 1,313 | 15.7% | 1,358 | 13.4% | +3.4% |

*Unit: million yen.

Income increased, pretax profit excluding transient factors increased

Operating income was 10,104 million yen, up 20.5% year-on-year. Pretax profit decreased 4.3% year-on-year to 1,915 million yen. Adjusting for one-time profit (negative goodwill, etc.) of 545 million yen in the same period of the previous year, profit increased by 31.5% year-on-year. Due to the stagnation of new car production, inventory shortages and soaring prices of used cars have become noticeable, but the transaction volume has exceeded the market in terms of both credit and failure guarantee.

Classification of operating expenses

| 2Q of FY 3/21 | 2Q of FY 3/22 | YoY | Factors driving change |

Guarantee Commission | 981 | 1,105 | +12.6% | The credit transaction volume increased (the balance of credit receivables grew). |

Warranty Cost | 1,359 | 1,384 | +1.8% | The Automobile Warranty Business was expanded. |

Auto mobility related cost | 209 | 799 | +283.0% | Increased due to expansion of parts sales and wholesale vehicle sales |

Personnel Expenses | 2,010 | 2,163 | +7.6% | The number of employees at the end of the term was 644 (up 48 from the end of the previous term). |

Asset Depreciation, Payment fee | 616 | 618 | +0.3% |

|

System Operation Cost, Outsourcing Expenses | 941 | 1,171 | +24.4% | Increased due to DX promotion, recruitment, and outsourcing of credit business. |

Other Expenses | 827 | 977 | +18.1% | Reduction in cost due to outsourcing credit business |

Total Operating Expenses | 6,944 | 8,216 | +18.3% | - |

*Unit: million yen.

【2-2. Business Segment Trends】

Classification of operating income

| 2Q of FY 3/21 | Ratio to operating income | 2Q of FY 3/22 | Ratio to operating income | YoY |

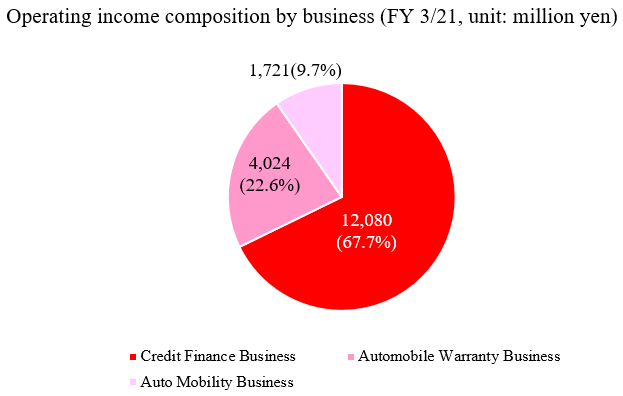

Finance Business | 5,865 | 69.9% | 6,626 | 65.6% | +13.0% |

Automobile Warranty Business | 1,961 | 23.4% | 2,169 | 21.5% | +10.6% |

Auto mobility Business | 560 | 6.7% | 1,309 | 13.0% | +133.8% |

Total operating income | 8,386 | 100.0% | 10,104 | 100.0% | +20.5% |

*Unit: million yen.

(1)Finance Business

*Credit transaction volume

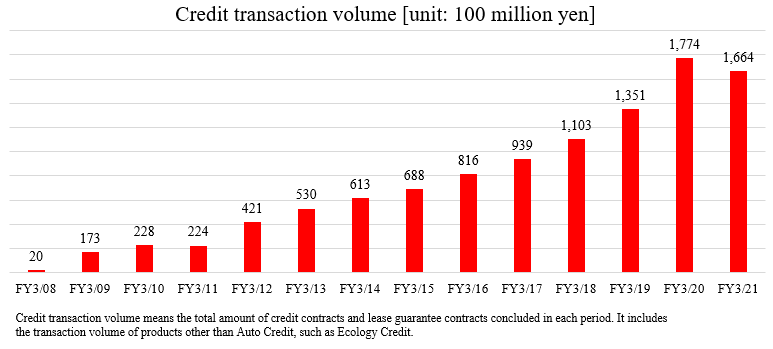

The amount of credit transactions in the second quarter of the term ending March 2022 was 100.4 billion yen, up 29.2% year on year.

DX measures and reorganization of the sales organization enabled the company to develop efficient sales activities. As of the end of the first half of the term, 79% of all transactions were paperless. The number of sales offices increased 9 year on year to 24.

The number of sales personnel at the end of the first half of the term was 94, up 10 from the end of the first quarter, and the goal of having 100 sales staff members was almost accomplished.

The average monthly transaction volume per auto sales staff member (in the second quarte from July to September) was also favorable at 178 million yen, up 16.7% year on year.

*Loan receivables

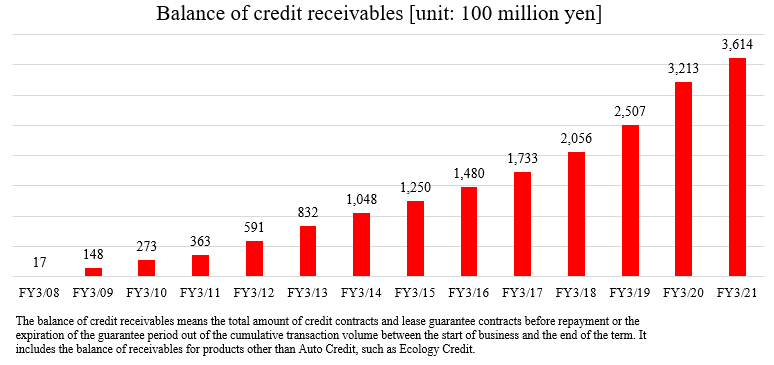

At the end of the second quarter of the term ending March 2022, the balance of credit receivables steadily rose 16.3% from the end of the same period of the previous term to 393.1 billion yen. The ratio of overdue receivables fell to 0.82% from 0.91% at the end of the same period of the previous term. The company implemented business innovations through DX measures, such as the efficient resolution of initial arrears through the adoption of IVR (Automated Calling System). In addition, the continuous collection of medium- to long-term arrears in cooperation with Central Servicer Corporation contributed to the decline in the delinquency rate.

*Number of network stores

At the end of September 2021, the number of affiliated companies increased 6.1% from the end of the same period of the previous term to 24,739, and new affiliated stores have increased almost as planned. In addition, the accumulated number of paid members (PFS Premium Club) has reached 757 as a result of preferentially facilitating the subscription of existing member stores. The targets for the end of the term ending March 2025 are 30,000 member companies and 3,000 paid subscription members.

(2)Automobile Warranty Business

*Transaction Volume

The number of transactions for the second quarter of the term ending March 2022 was 2,520 million yen, up 12.3% year on year. The number of transactions from in-house products rose 29.0% year on year.

The sales of in-house products grew as planned after focusing on their sales expansion, but sales growth of affiliated products slowed down due to sluggish markets.

(3)Auto mobility Business

The operating income for the second quarter of the term ended March 2021 was 1,309 million yen, up 133.8% year on year. With the expansion of the paid subscription system, the handling of each service increased. In particular, sales of parts and wholesale of vehicles were the driving force behind the growth in earnings and helped the company make a profit. The accumulated total number of companies in the repair network rose 63.3% year on year to 3,160, exceeding the target of 3,000 ahead of schedule. There are 104 paid members (FIXMAN Club), and the company will focus on expanding its FIXMAN Club membership in the future.

【2-3. Financial Condition and Cash Flow】

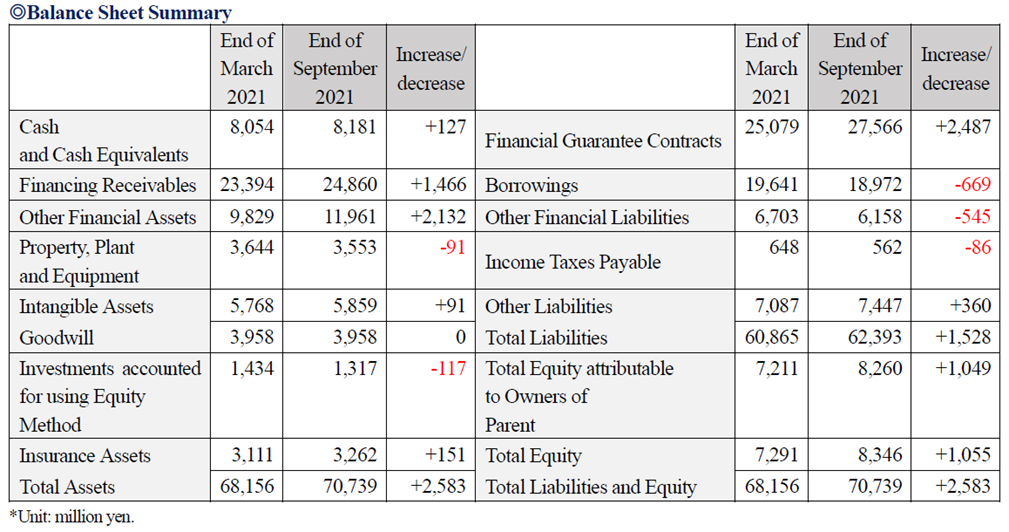

Total assets increased 2,583 million yen from the end of the previous term to 70,739 million yen, as finance receivables and other financial assets expanded due to business expansion. Total liabilities rose 1,528 million yen from the end of the previous term to 62,393 million yen, as the number of financial guarantee contracts increased in parallel with the increase of credit transactions.

Total equity attributable to the owners of parent increased 1,049 million yen from the end of the previous term to 8,260 million yen. Equity ratio (the ratio of total equity attributable to the owners of parent) increased 1.1 points from the end of the previous term to 11.7%.

◎CF

| 2Q of FY3/21 | 2Q of FY3/22 | YoY |

Operating CF(A) | 1,771 | 1,800 | +29 |

Investing CF(B) | -749 | -325 | +424 |

Free CF(A+B) | 1,022 | 1,475 | +453 |

Financing CF | 2,160 | -1,344 | -3,504 |

Cash and Cash Equivalents | 9,468 | 8,181 | -1,287 |

*Unit: million yen.

Operating and free CFs increased. The cash position declined.

【2-4 Topics】

(1) Progress of the DX strategy

The transaction volumes of finance, automobile warranty, and auto mobility services realized through DX have been set as KGIs.

The finance business manages the volumes of auto credit transactions and auto lease transactions; the automobile warranty business manages the volume of automobile warranty transactions; and the auto mobility business manages the volume of transactions through the platform as DX strategy indicators. The system is under development except for paperless credit contracts.

The adoption rate of paperless credit contracts, which started in the previous term, has been increasing.

The number of paperless applications in the second quarter was 36.9 billion yen, a significant increase from 1.3 billion yen in the same period of the previous term. Paperless adoption rate also jumped to 79% from 7% in the same period of the previous term.

The DX Strategy positions this term and the next as development phases, and the development of business DX and in-house DX are progressing smoothly.

(2) Other topics

Year / Month | Description | |

2021 | July | The back-office division of the automobile warranty business was newly established in Kawaguchi City, Saitama Prefecture. |

The company held its first IR Day (Investor Relations Day) to explain its business and growth strategy. | ||

August | The company was selected as a constituent of the JPX-Nikkei Mid and Small Cap Index. | |

In response to the notification from Tokyo Stock Exchange that the company complies with the Prime Market listing maintenance criteria, the company decided to be listed on the new Prime Market category. | ||

The company was ranked in the Toyo Keizai Online's "High Ratio of Female Managers" company ranking for the second consecutive year. | ||

The Osaka Contact Center was established to strengthen outbound sales. It has become a system which further promotes the expansion of a nationwide network of member stores and the promotion of the operation of various services. | ||

October | The company started handling Loading Vehicle Lease for mobility service providers. It is one of the FIXMAN Club's services and is available at the lowest price in the industry. | |

The corporate website was renewed. It has been redesigned to make it easy to use for all stakeholders. The company will continue to share information to promote understanding and popularize various services. | ||

3. Fiscal Year ending March 2022 Earnings Forecasts

【3-1 Full-year consolidated earnings 】

| FY3/21 | Ratio to operating income | FY3/22(Est.) | Ratio to operating income | YoY | Progress rate |

Operating Income | 17,825 | 100.0% | 21,446 | 100.0% | +20.3% | 47.1% |

Pretax profit | 3,463 | 19.4% | 3,500 | 16.3% | +1.1% | 54.7% |

Net Income | 2,393 | 13.4% | 2,422 | 11.3% | +1.2% | 56.4% |

Profit attributable to owners of parent | 2,383 | 13.4% | 2,409 | 11.2% | +1.1% | 56.4% |

There is no change in the earnings forecasts, operating income and pretax profit are estimated to be increased. There is no change in the earnings forecasts. Operating income and pretax profit are estimated at 21,446 million yen and 3,500 million yen, up 20.3% and 1.1% year on year, respectively. Pretax profit excluding temporary profit and loss is projected to increase 16.4% year on year. The progress of revenue and profit have been higher than the forecasts for the current term, but the full-year forecasts remain unchanged because of the uncertain future outlook due to the shortage of semiconductors in the automobile market and the resultant delay in new car production. An interim dividend and a term-end dividend are both to be 25 yen per share, and an annual dividend will be 50 yen per share, up 4 yen per share year on year. The payout ratio will be 26.9%.

【3-2 Major strategies 】

(1) Finance Business

*Increase of credit transactions

In addition to promoting the increase of members for the PFS Premium Club membership service, the company aims to increase royalties and transactions.

*Increase of credit receivables

The company will thoroughly reduce initial arrears and reduce medium to long-term arrears through the synergy with Central Servicer Corporation.

Further introduction of DX measures is planned for more efficient collection of receivables.

*Increase of credit card affiliated stores

While continuing to increase affiliated stores, the company will focus on promoting operations and increasing members for its PFS Premium Club subscription service.

There were 85 diamond members, up 15 from the first quarter, and 672 gold members, up 135 from the first quarter.

As described in Topics, the company opened a new contact center (outbound sales) in Osaka in August 2021. It will also promote the operation of non-operating facilities at three locations nationwide.

(2)Automobile Warranty Business

The company will increase the number of sales staff members specializing in affiliated products.

It will strengthen handling of new products (extended warranties and warranties incidental to inspection and maintenance).

To further reduce costs, the company will promote warehousing in repair networks and in-house procurement of used parts.

A new system following DX measures is scheduled to be released this term.

(3)Auto mobility Business

FIXMAN Club has added a new membership category.

The company aims to attract new members by expanding content for members such as (i) Automobile leasing (started in October 2021) and (ii) Support for driving customer traffic "Premium—the place for cars and financing": (scheduled to start next term).

4. Conclusions

The progress rate in the first half was 47.1% for operating income and 54.7% for pretax profit. However, regarding pretax profit, the ratio of the actual profit for the core business, excluding one-time profit in the term ended March 2021, was 42.1% and the progress rate for this term was significantly high compared to those in the past several years. The company's operating income is almost the same as that in a typical year and appears to be making good progress at this point. Although the full-year forecasts remain unchanged due to the uncertain impact of reduced production by automobile manufacturers on the used automobile market due to the shortage of semiconductors, we will closely monitor market trends and the company's business performance from the third quarter onward. Regarding the medium-term management plan “VALUE UP 2023”, it seems that the DX strategy, which is a priority measure, is steadily progressing. We would like to look forward to the future progress and results.

<Reference 1:Overview of Medium-term Management plan “VALUE UP 2023” >

The 3-year mid-term management plan, VALUE UP 2023, which started the term ended March 2021 and will end in the term ending March 2023, is ongoing. On May 13, 2021, the company revised and re-announced the plan due to a change in business environment caused by the spread of COVID-19.

(1) Progress so far

Since the start of the business in 2007, the company has expanded the credit and automobile warranty businesses as the mainstays, and got listed in the first section of Tokyo Stock Exchange in 2018, showing steady growth. As for business performance, sales and profit grew significantly, and ROE and ROA rose steadily.(2) Regarding the mid-term vision

(Recognition of the business environment) Considering the impact of the novel coronavirus, the company recognizes the business environment as follows.

Target | Situation | Recognition | Necessary measure |

Individual customers | Used cars sold increased in number in the second half of the term although fewer people purchased used cars when a state of emergency was issued in April 2020 | Constant demand for used cars, which is a daily necessity, is recognized again | To further grow the Finance Business and the Automobile Warranty Business |

Used car market (dealers/maintenance shops) | A decline in the quantity of new cars distributed resulted in a drop of the quantity of used cars distributed, which increased the cost price | -Dealers and maintenance shops with less financial power are struggling -The quantity sold and the number of opportunities for contacting customers decreased | To support small- and medium-sized dealers and maintenance shops in running business |

Social trend | An era of the new normal in which conventional thoughts and methods do not work began | It is necessary to establish competitive superiority for sustainable growth | To make shifts to a new business model and promote business innovation based on DX |

(Mid-term vision: ideal state)

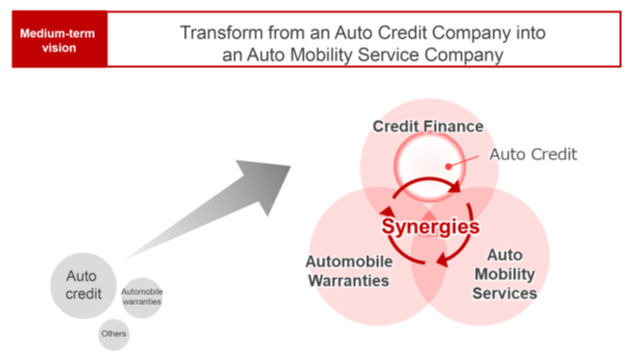

Recognizing the business environment as mentioned above, the company considers that it is necessary to grow the existing businesses and vitalize the used car market by supporting the management of used car dealers and maintenance shops, which are their direct customers. For this, the company upholds the mid-term vision of evolving from an auto credit company, offering mainly auto credits and warranties, to an auto mobility company that develops networks with automobile dealers, maintenance shops, and customers and creating the synergy among credit finance, automobile warranty, and auto mobility.

(Taken from the reference material of the company)

(Materiality based on the mid-term vision) Based on the recognition of the business environment, the company defined the following four as materiality items.

Business environment recognition | Materiality |

It is important to expand the existing Credit Finance and Automobile Warranty Businesses to grow the company. | ① To improve the Credit Finance Business, which is its forte ② To expand the market of automobile warranty |

It is necessary to support the management of small and medium-sized dealers and maintenance shops. | ③ To enrich the Auto Mobility Business |

It is important to establish new business models and promote industrial innovation through DX. | ④ To become a provider of platforms in the used car and car maintenance markets |

The company announced digital transformation (DX) strategies, recognizing that it is essential to promote DX to realize sustainable growth and enhance competitiveness.

(3) Initiatives in each business

To realize an ideal state, it is necessary to develop a system to offer the best finance and the best service.

Based on the mid-term vision, VALUE UP 2023, the company will implement the following measures in each field.

① Credit Finance Business

Auto credit and auto lease for individuals

The priority measures are to enhance marketing and to proceed with industrial innovation.

For enhancing marketing, the company will expand the target area with the BIZ site method* and increase the number of marketing staff members to 130.

In addition, the company will upgrade outbound contact centers, start operating affiliates that are still not in operation, cultivate uncultivated areas, promote the development of a members-only organization for affiliates, and grow the top line steeply.

For promoting industrial innovation, the company will develop an automatic screening system based on AI, make back-office operations unmanned, and do away with paper to increase business efficiency and profit margin.

* BIZ site method means the marketing method of establishing footholds in major cities rather than establishing branches in respective regions and visiting the target area when necessary.

Servicer

The priority measures are to collect receivables jointly with other group companies and sell repossessed cars*.

For collecting receivables with other group companies, the company will collect receivables in cooperation with Central Servicer Corporation, which was acquired as a subsidiary in April 2020, and exert synergy to grow revenues further.

For selling repossessed cars*, the company will sell the vehicles repossessed at the time of collection of receivables to affiliates of the members-only organization, to create new earning opportunities.

*Repossessed cars: Vehicles repossessed when the company collects receivables for auto credits.

② Automobile Warranty Business

The company considers that it is indispensable to expand the market itself.

To do so, the company will implement the following measures and reduce the scrapping of cars by maintaining used cars.

Measure | Outline |

Development of extended warranties | To increase business opportunities by increasing the contact points with customers through extended warranties. |

Improvement in profitability | To curtail repair costs and discount selling prices by putting cars in the maintenance shops of the members-only organization and using recycled auto parts procured within the corporate group. |

Advertisement for increasing popularity | To popularize automobile warranty and disseminate its effectiveness through advertisement via TV, the Internet, etc. |

③ Auto Mobility Business

The company will concentrate on the expansion of the “new 3Rs” businesses, which are environmentally friendly. The new 3Rs are Recycle (recycled parts) business, which distributes the parts of used cars, Reuse business, which distributes repossessed vehicles within the corporate group, and Repair business, which offers maintenance services for inspecting and repairing automobiles, sheet-metal services for repairing scratches, dents, etc. on automobiles, and so on. At present, the company offers a broad range of services, including the sale of recycled parts, repossessed vehicles, and task management software for maintenance shops, etc., via subsidiaries acquired through M&A.

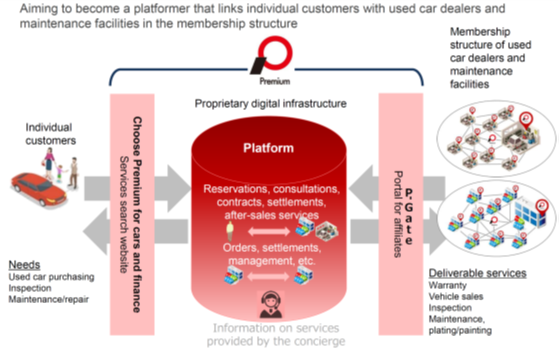

The priority measures are to enrich the service lineup, to develop members-only organizations for affiliated used car dealers and maintenance shops, and to proceed with the platform scheme. The company aims to actualize the sustainable growth of the corporate group, by diversifying revenue sources.

Among the network which the company has developed so far (including over 30,000 automobile dealers and over 3,000 maintenance shops), the company will establish members-only organizations with affiliates with an increasing number of transactions: PFS Premium Club for automobile dealers and FIXMAN Club for maintenance shops.

By connecting these members-only organizations and customers, the company aims to become a platform provider for offering a wide array of services.

(Taken from the reference material of the company)

④ Overseas strategy

As indicated in the mission, the company will target to the world and expand our know-how cultivated in Japan to overseas.

While keeping an eye on the situation of the pandemic, etc., the company will strive to exhibit its products and services in more countries, while recognizing Phase I of the mid-term vision as a planting season. The company will make inroads into foreign markets by establishing joint ventures with local capital, etc. instead of establishing a company with its own funds.

Phase II of the mid-term vision will be recognized as the reaping period, and the company will engage in overseas businesses on a full-scale basis while considering the reorganization of joint ventures into consolidated subsidiaries.

(4) Numerical goals

In VALUE UP 2023, they aim to achieve an operating revenue of 25.8 billion yen and a net profit of 3.3 billion yen, in the term ending March 2023. In the term ending March 2025, which is the final fiscal year of the next mid-term vision, they aim to achieve an operating revenue of 41.9 billion yen, a net profit of 6.5 billion yen, and a market cap of 175 to 200 billion yen.

| FY 3/21 Results | FY 3/22 Est. | FY 3/23 Est. | FY 3/24 Est. | FY 3/25 Est. | CAGR |

Operating income | 178 | 214 | 258 | 329 | 419 | +23.9% |

Pretax profit | 35 | 35 | 49 | 65 | 100 | +30.0% |

Net profit | 24 | 24 | 33 | 43 | 65 | +28.3% |

ROE | 38.3% | - | 31.7% | - | 37.0% | - |

Market cap | 322 | - | 900-1,000 | - | 1,750-2,000 | - |

*Unit: 100 million yen. Net profit means the profit attributable to owners of parent. Market cap means the closing value on March 31, 2021. CAGR is the average annual growth rate in the four years from FY 3/21 to FY 3/25. Calculated by Investment Bridge Co., Ltd. with reference to the plan of Premium Group.

(5) Initiatives toward ESG and SDGs

Being deeply conscious of its social significance and responsibility, Premium Group published an Environment, Society, and Governance (ESG) report from an ESG perspective covering its business and corporate activities. It will move ahead with efforts by identifying nine materiality items regarding the environment, social capital, human capital, business models and innovation, and risk management and governance.

<Reference 2: Corporate Governance>

◎Organization type, and the composition of directors and auditors

Organization type | Company with an audit and supervisory board |

Directors | 8 directors, including 3 outside ones |

Auditors | 3 auditors, including 2 outside ones |

◎Corporate governance report (updated on June 29, 2021)

<Reasons for Non-compliance with the Principles of the Corporate Governance Code (Excerpts)>

[Supplementary Principle 1-2 (3) Appropriate scheduling of general meetings of shareholders]

The company will ensure adequate audit periods for appropriate financial reporting and effective audits by auditors and comptrollers, and appropriately set schedules related to general meetings of shareholders so that more shareholders can participate based on its belief that general meetings of shareholders provide opportunities to have a dialogue with shareholders.

In addition, the company will secure opportunities for shareholders to participate through online distribution using the web conferencing system.

[Principle 1-4: Strategically held shares]

As a principle, the company does not hold listed shares strategically and does not currently hold such shares. In the event that strategic shareholding is required, the Board of Directors will examine the details of the proposal, including whether the purpose of holding the shares is appropriate and whether the benefits and risks associated with holding the shares are commensurate with the cost of capital and so on, and make a rational decision on the appropriateness of holding such shares and properly disclose the decision.

<Disclosure based on the principles of the Corporate Governance Code> [Principle 5-1. Policy on constructive dialogue with shareholders] Our company has adopted a positive attitude toward constructive dialogue with our shareholders as much as is reasonably possible. With the president assuming the primary responsibility for our company’s dialogue with the shareholders in general, the president and the directors mainly have dialogue with the shareholders according to such matters as the number of our company’s shares held by and the scale of the shareholder to interview with. The public relations and IR department supervised by the director in charge conducts business operations for effective IR activities. We have established a structure that encourages various departments including the management department, department supervising corporate governance, the general affairs department, the accounting department, and the legal compliance department, to cooperate with the public relations and IR department, in order to assist in the dialogue with the shareholders. Our efforts at dialogue with the shareholders include disclosure of information through financial results briefings and our website, and proactive IR activities that help the shareholders broaden their understanding of our corporate group’s present condition and other relevant matters. Specifically, we hold individual meetings with institutional investors and analysts’ meetings for dialogue with such stakeholders, in which mainly the president and the directors have direct dialogue with them, depending on the situation. Regarding dialogue with individual investors, our company proactively participates in company information sessions and online seminars hosted for individual investors by financial securities firms and other similar organizations so that our president and directors can explain our corporate group’s present condition and other relevant matters with their own words. The schedule of IR events for individual investors is disclosed on the company’s website. (https://ir.premium-group.co.jp/ja/calendar.html). In addition, for overseas investors with a certain volume of transactions in the Japanese stock market, the company is taking steps such as individual meetings held by telephone, preparation of English translated documents, and conveying information through the English version of the website.

In addition, the Public Relations and Investor Relations Department of the company collect and organize opinions obtained through dialogue with shareholders and report them to the Board of Directors as necessary to share information and improve management.

Further, regarding the management of insider information during dialogue, the company strictly controls undisclosed information in accordance with the regulations on the prevention of insider trading.

| This report is not intended for soliciting or promoting investment activities or offering any advice on investment or the like, but for providing information only. The information included in this report was taken from sources considered reliable by our company. Our company will not guarantee the accuracy, integrity, or appropriateness of information or opinions in this report. Our company will not assume any responsibility for expenses, damages or the like arising out of the use of this report or information obtained from this report. All kinds of rights related to this report belong to Investment Bridge Co., Ltd. The contents, etc. of this report may be revised without notice. Please make an investment decision on your own judgment Copyright (C) Investment Bridge Co., Ltd. All Rights Reserved |

The back number of Bridge Report (Premium Group Co., Ltd.: 7199) and the contents of Bridge Salon (IR Seminar) can be viewed here: www.bridge-salon.jp/