Bridge Report:(8130)Sangetsu the first half of the Fiscal Year March 2020

![]()

Shosuke Yasuda, President | Sangetsu Corporation (8130) |

|

Company Information

Market | First Section, Tokyo and Nagoya Stock Exchanges |

Industry | Wholesale (Commerce) |

Executive Director and President・Executive officer | Shosuke Yasuda |

HQ Address | 1-4-1 Habashita, Nishi-ku, Nagoya-shi |

Year-end | March |

Homepage |

Stock Information

Share Price | Shares Outstanding | Total market cap | ROE Act. | Trading Unit | |

¥2,123 | 62,250,000 shares | ¥132,156 million | 3.5% | 100 shares | |

DPS Est. | Dividend yield Est. | EPS Est. | PER Est. | BPS Act. | PBR Act. |

¥57.00 | 2.7% | ¥92.72 | 22.9 x | ¥1,612.59 | 1.3 x |

*The share price is the closing price on December 4. The number of shares issued, DPS, EPS are taken from the financial report for the first half of FY March 2020. ROE and BPS are taken from the financial report for FY March 2019.

Earnings Trend

Fiscal Year | Sales | Operating Income | Ordinary Income | Net Income | EPS (¥) | DPS (¥) |

March 2016 Act. | 133,972 | 9,112 | 9,463 | 6,393 | 89.92 | 47.50 |

March 2017 Act. | 135,640 | 7,572 | 8,368 | 6,570 | 97.53 | 52.50 |

March 2018 Act. | 156,390 | 5,033 | 5,698 | 4,514 | 68.97 | 55.50 |

March 2019 Act. | 160,422 | 5,895 | 6,699 | 3,579 | 57.28 | 56.50 |

March 2020 Est. | 163,000 | 8,000 | 8,300 | 5,700 | 92.72 | 57.00 |

*Unit: million yen, yen. Estimates are those of the Company. Net income is profit attributable to owners of the parent. Hereinafter the same shall apply.

This Bridge Report provides a review of the first half of the fiscal year March 2020 earnings overview and more.

Table of Contents

Key Points

1. Company Overview

2. First Half of the Fiscal Year March 2020 Earnings Results

3. Fiscal Year March 2020 Earnings Forecasts

4. Situation of the Mid-term Management Plan “PLG2019” (2017-2019) and Problems with it

5. Conclusions

<Reference 1: Mid-term Management Plan “PLG 2019” (2017-2019) Overview>

<Reference 2: Regarding Corporate Governance>

Key Points

- The sales for the first half of the term ending March 2020 were 80 billion yen, up 5.4% year on year. Both the Interior and Exterior Businesses performed well. In the Interior Business, all the product categories saw the growth of sales. The sales of the overseas business declined. Operating income rose 107.7% to 4.5 billion yen. Gross profit rate increased 2 points, as the revision to the wholesale prices of products, which was started in October 2018 for coping with the skyrocketing costs for raw materials and distribution, progressed. Gross profit increased 12.2% year on year. The growth rate of SG&A was only 2.4%, and profit increased significantly. Both sales and profit exceeded the respective estimates.

- The financial results indicate that their efforts to improve the business in various ways, including the improvement in logistics and the installation of a new mission-critical system, paid off. In addition, the company was able to revise prices for the first time in 5 years since 2014, almost as planned, while gaining the understanding of surrounding people by utilizing its position in the industry centered around wallpaper.

- The earnings forecast has not been revised, because there are uncertainties over the overseas business, the domestic market trend, etc. The sales for the term ending March 2020 are expected to rise 1.6% year on year to ¥163 billion. Gross profit is projected to increase 3.5% year on year, exceeding the rate of sales growth and gross profit margin is estimated to increase by 0.6 points. In addition to the effect from the price increase, the company will improve profitability in overseas segments. Operating income is estimated to rise 35.7% year on year to ¥8 billion. The dividend is forecasted to be ¥57.00/share, up ¥0.5/share over the previous term. The estimated payout ratio is 61.5%.

- Thanks to the effects of business improvement measures the company has taken so far and the steady penetration of revised prices, sales and profit grew, while profit rate increased considerably. Progress rates seem to be healthy, but the full-year earnings forecast remains unchanged, because there are uncertainties over the effects of the rush demand before the consumption tax hike, the improvement in the overseas business, etc. We would like to keep an eye on how much the company can increase sales and profit in the second half of this term, which is the final fiscal year of the mid-term management plan.

- The points of the next mid-term management plan are how the company will enhance the earning capacity of the Interior Business, which is the mainstay, as the operation of the new Kansai LC will begin, and how the overseas business will increase revenue.

1. Company Overview

Sangetsu Corporation is the largest among all Japanese trading companies specializing in wallcoverings, flooring materials, curtains and other interior decorating products. Being a trading firm, the Company also operates as a “fabless company” that plans and develops interior decorating products. Sangetsu boasts of a business model that is able to produce stable earnings and top market share in its main product realms. The group is composed of seven companies including “Sangetsu Okinawa Corporation,” which sells interior materials in the Okinawa area, Sungreen Co., Ltd., a dedicated distributor of exterior products, Sangetsu (Shanghai) Corporation, the company responsible for business in China, “Koroseal Interior Products Holdings, Inc.,” the United States company conducting sales of wallcovering materials for non-residential applications, Fairtone Co., Ltd., which seeks to grow orders on the back of increases in installation capabilities, “Sangetsu Vosne Corporation,” specialized in curtain fabrics, and “Goodrich Global Holdings Pte. Ltd.,” the company selling interior materials in Southeast Asia.

1-1 Corporate History

Sangetsu was founded in 1849 under the original name of “Sangetsudo” to sell various traditional Japanese interior decorating products including scrolls, wall scrolls, folding screens, sliding doors, partitioning screens, and other products made of cloth and paper. Sangetsu Corporation was incorporated in 1953 by the founding family. From the latter half of the 1970s onwards, the business was expanded into Tokyo, Fukuoka, Osaka and other parts of Japan. In 1980, Sangetsu was listed on the Second Section of the Nagoya Stock Exchange, and later in 1996 its shares were also listed on the First Section of the Tokyo Stock Exchange. Currently, Sangetsu is expanding its operations into overseas markets and has established itself as a large total interior decorating product provider.

Shosuke Yasuda was appointed as the first President who is not from the founding family of Sangetsu in April 2014. He will direct the Company during its third stage of growth entitled “Our Third Founding Phase,” following on the heels of the original first phase of founding and the second phase when the company became a publicly listed corporation.

1-2 Corporate Philosophy

Sangetsu established a new corporate philosophy including a new brand philosophy in February 2016 that will enable it to take on the challenge of implementing reforms necessary to take it to its next stage of growth.

A new “brand philosophy” has been added to the “corporate creed,” “corporate mission,” and “Three Principles of Sangetsu” to create an expanded corporate philosophy.

<Corporate Creed>

Integrity

<Corporate Mission>

To contribute to society through interior design and strive to create daily culture of enrichment

<Three Principles of Sangetsu>

Creative Designs, High Reliable Quality, Fair Price

<Brand Philosophy>

・Brand statement: | “Joy of Design” |

・Brand purpose: | “We provide the joy of design to those who create new spaces.” |

Sangetsu endeavors to share the joy of creating new value through interior business with all of its stakeholders.

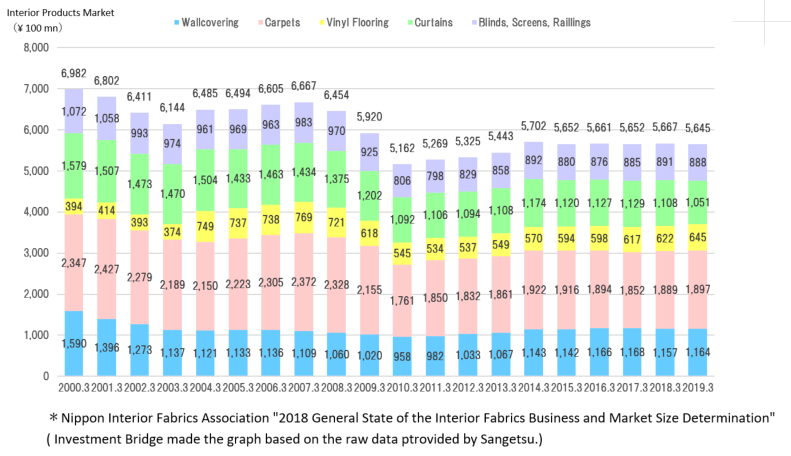

1-3 Market Environment

◎ Overview

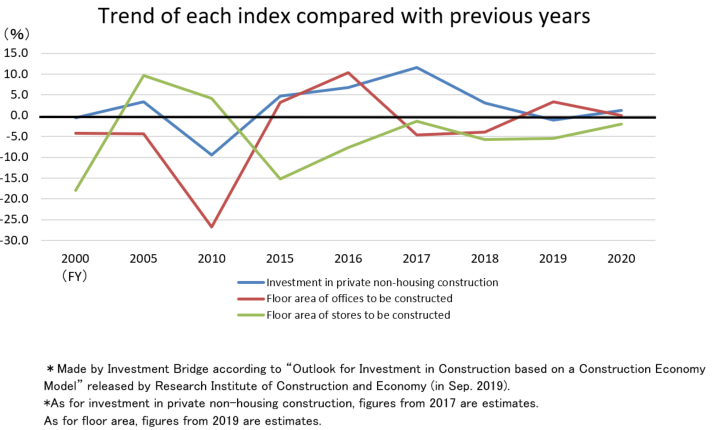

The market environment for the main wallcoverings and flooring materials is strongly influenced by trends in the Japanese construction market. Declines in new housing start arising from declining population and changing family structures within Japan, and deflationary trends have depressed sales of the interior products market as shown in the graph below.

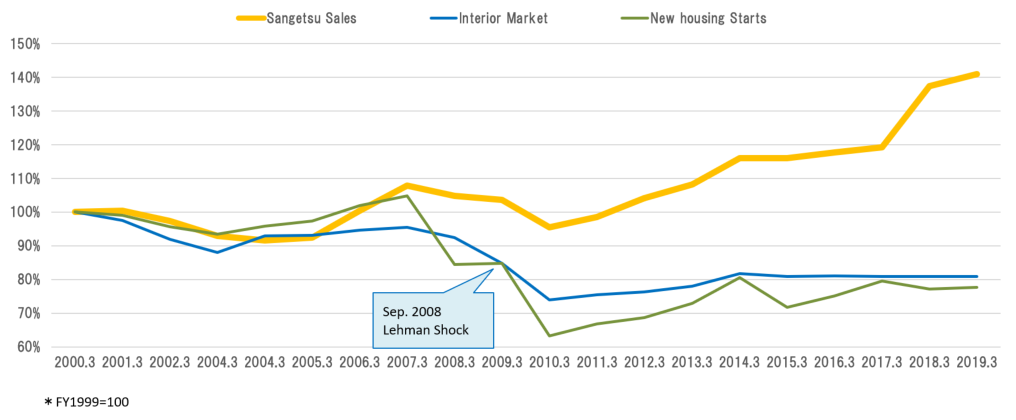

At the same time, the graph below shows the correlation between sales of Sangetsu relative to sales of the Japanese interior market and new housing starts (Ministry of Land, Infrastructure, Transport, and Tourism data).

The trends for both Sangetsu’s sales and the Japanese interior market have been closely linked to new housing starts. After the Lehman Brother’s Shock, however, this link has been overcome with Sangetsu’s sales reaching consecutive record highs despite the sluggish trends in new housing starts and the weak overall market.

Aside from private housing, this strong recovery can be attributed to M&A and Sangetsu’s efforts to cultivate business in the non-residential realm.

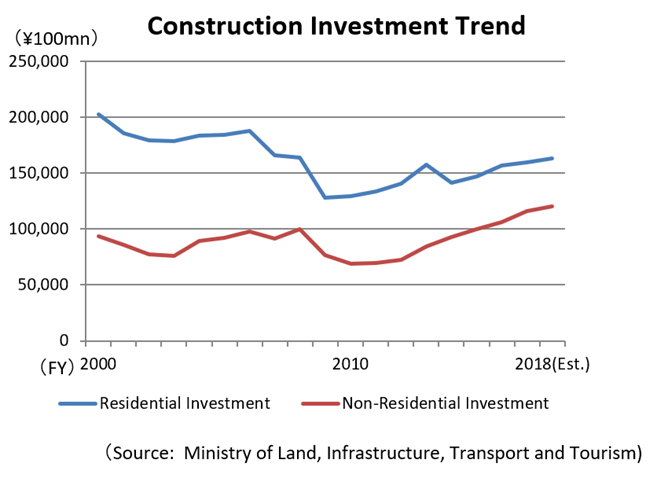

According to “Outlook for Investment in Construction” released by the Ministry of Land, Infrastructure, Transport and Tourism, the investments in private housing and non-housing constructions have been recovering since the bankruptcy of Lehman Brothers, but the estimated investment in private housing construction is still about 80% of the level in the year 2000, while the investment in private non-housing construction exceeds the level in the year 2000.

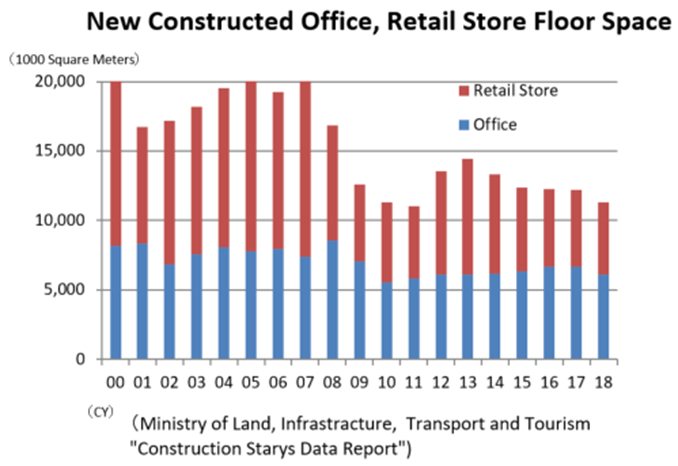

However, since the floor area of new offices and stores, which had been rising in past several years, shrank in 2018, it can’t really be said that it performed well.

According to “Outlook for Investment in Construction based on a Construction Economy Model” released by Research Institute of Construction and Economy (on September 26, 2019), The growth rate of investment in private, non-residential buildings increased 11.6% in FY 2017, and 3.0% in FY 2018 (estimate), but is expected to fall 1.0% in FY 2019 (estimate) and to increase 1.3% in FY2020 (estimate). Therefore, the growth is estimated to become sluggish.

While the growth rate of the floor area of offices to be constructed was 10.3% in fiscal year 2016, it turns out to minus 4.6%. The company estimates that the growth will continues to slow down such that the growth rate will be minus 4.6% in FY 2017 and minus 3.9% in FY 2018. Though it recovers to plus 3.3% in FY 2019, it is expected to hang low around 0.0%. Retail stores will continue to be lower than in the previous year as it has been since fiscal 2014. It is difficult to expect that the business environment will significantly get better.

For the above reasons, the residential and non-residential market environments are currently unfavorable, but there is steady demand for renovations in the non-residential market, so the company intends to meet the demand mainly through the contract sales department. They are also making efforts to develop overseas businesses, pursuing further growth by reinforcing the advantages they have over other companies.

◎Competitors

In addition to Sangetsu, there are eight publicly traded competitors that operate in the interior decorating market.

Stock Code | Company | Sales | YY Change of Sales | Operating Income | YY Change of Operating Income | Operating Income Margin | Total Market Cap | PER | PBR | ROE |

3501 | Suminoe Textile Co., Ltd. | 96,000 | -2.7% | 2,600 | -16.6% | 2.7% | 2,185 | 14.5 | 0.6 | 1.4% |

4206 | Aica Kogyo Co., Ltd. | 195,000 | +1.9% | 21,800 | +4.6% | 11.2% | 235,891 | 16.5 | 1.8 | 10.7% |

4215 | C.I. TAKIRON Corporation | 151,000 | +0.2% | 9,300 | +2.4% | 6.2% | 65,130 | 4.8 | 0.9 | 8.8% |

4224 | Lonseal Corporation | 20,500 | +1.0% | 1,600 | -17.0% | 7.8% | 8,510 | 7.4 | 0.5 | 9.0% |

5956 | TOSO COMPANY, LIMITED | 22,800 | +0.7% | 600 | -12.8% | 2.6% | 5,080 | 12.5 | 0.4 | 3.8% |

7971 | TOLI Corp. | 94,000 | +4.0% | 2,400 | +20.5% | 2.6% | 21,118 | 10.0 | 0.5 | 3.8% |

7989 | TACHIKAWA CORPORATION | 42,200 | +8.0% | 4,100 | +11.5% | 9.7% | 29,297 | 10.8 | 0.8 | 6.7% |

8130 | Sangetsu Corporation | 163,000 | +1.6% | 8,000 | +35.7% | 4.9% | 132,156 | 22.9 | 1.3 | 3.5% |

9827 | Lilycolor Co., Ltd. | 36,800 | +8.3% | 700 | +282.8% | 1.9% | 3,051 | 10.2 | 0.5 | 0.6% |

*Unit: million yen, times. Estimates are from those of the respective companies. Total market capitalization, PER and PBR are based upon the closing share price of each stock on December 4, 2019. ROE is based on the previous year.

1-4 Business Description

The main businesses include planning, development, and sales of wallcoverings, flooring materials, curtains, upholstery and other interior products. Sangetsu takes a “fabless operation,” which does not maintain any manufacturing facilities, and it is not a typical trading firm, but all the products it sells are planned, designed and developed in-house. Sangetsu also provides exterior products through its subsidiary. The overseas business is operated by three subsidiaries located in the U.S., China, and Singapore.

Yamada Shomei Lighting Co., Ltd., which became a subsidiary in 2008, had been operating the “Lighting Business” to sell general lighting fixtures inside and outside Japan, but the company concluded that the synergetic effects are limited, and transferred this business to Odelic Co., Ltd. on April 5, 2019.

① “Interior Business”

(FY3/19: Sales and Operating Income of ¥119,157 million and ¥6,174 million respectively)

◎Main Products

Wallcoverings | Sangetsu’s main product, used in a wide range of residential and non-residential applications. High functionality products have become popular in recent years that are resistant to staining, odor absorbing, and scratch resistant. Also, “Accent Wall” a wallcovering with colorful designs being used to decorate one full wall or a part of a wall in homes, adds an appeal to the living space, and is increasingly adopted in general residences and rental housing. |

Cushion Vinyl Sheet | Sheet formed flooring materials that are used in both residential and retail store applications, and commonly used in apartments and condominiums. They boast of wood grain, stone, and a wide range of other motif designs and have cushioning function for use in a wide range of applications. |

Vinyl Sheets | Sheet formed flooring materials used in commercial applications including medical and welfare institutions, and educational institutions. This product boasts of high levels of safety and hygiene, and is designed to reduce maintenance costs, thanks to the excellent maintenance properties, such as the unnecessity of waxing. It also has been designed with the environment in mind and helps to reduce the environmental burden. |

PVC Tiles | Tile formed PVC flooring which has a wide range of applications, is used in commercial facilities, educational institutions, detached houses and apartments. One feature is its high design, in which the materials used as motifs such as wood and stone are expressed through high-tech printing technology and precise embossing. |

Carpets | Textile flooring materials used in a wide range of applications including ryokans (i.e. Japanese inns), hotels, residential and commercial facilities. Manufactured with variety of designs and high functionality. It also proposes original designs to each property. |

Carpet Tiles | A square-shaped-tile-like carpet with a length of 50 cm, which is used mainly for offices, hotels, commercial facilities, and educational institutions It excels in its feature of easy installation and superior maintenance. |

Curtains | All of the curtains sold by Sangetsu are custom made and boast of the ability to create unique designs and custom sizes of curtains to match room decorations in which they are used. In addition to highly fashionable designs and heavy materials, mirror-like insulating characteristic lace curtains, which make it difficult to see inside from the outside and reduce the amount of heat transferred into the rooms, have also become popular. |

Sangetsu boasts a diverse product lineup with about 12,000 different products in total. There are about 4,300 different wallcovering products alone. Sample books are updated every two years (those for curtains are updated every three years), with an existing product replacement rate for wallcoverings of 30% to 40%.

Disposal of outdated products leads to producing wastes, but because keeping a sample book up-to-date is necessary to enhance customer satisfaction, the company has maintained a balance between efficiency and freshness through the company’s energetic engagement and long-cultivated know-how.

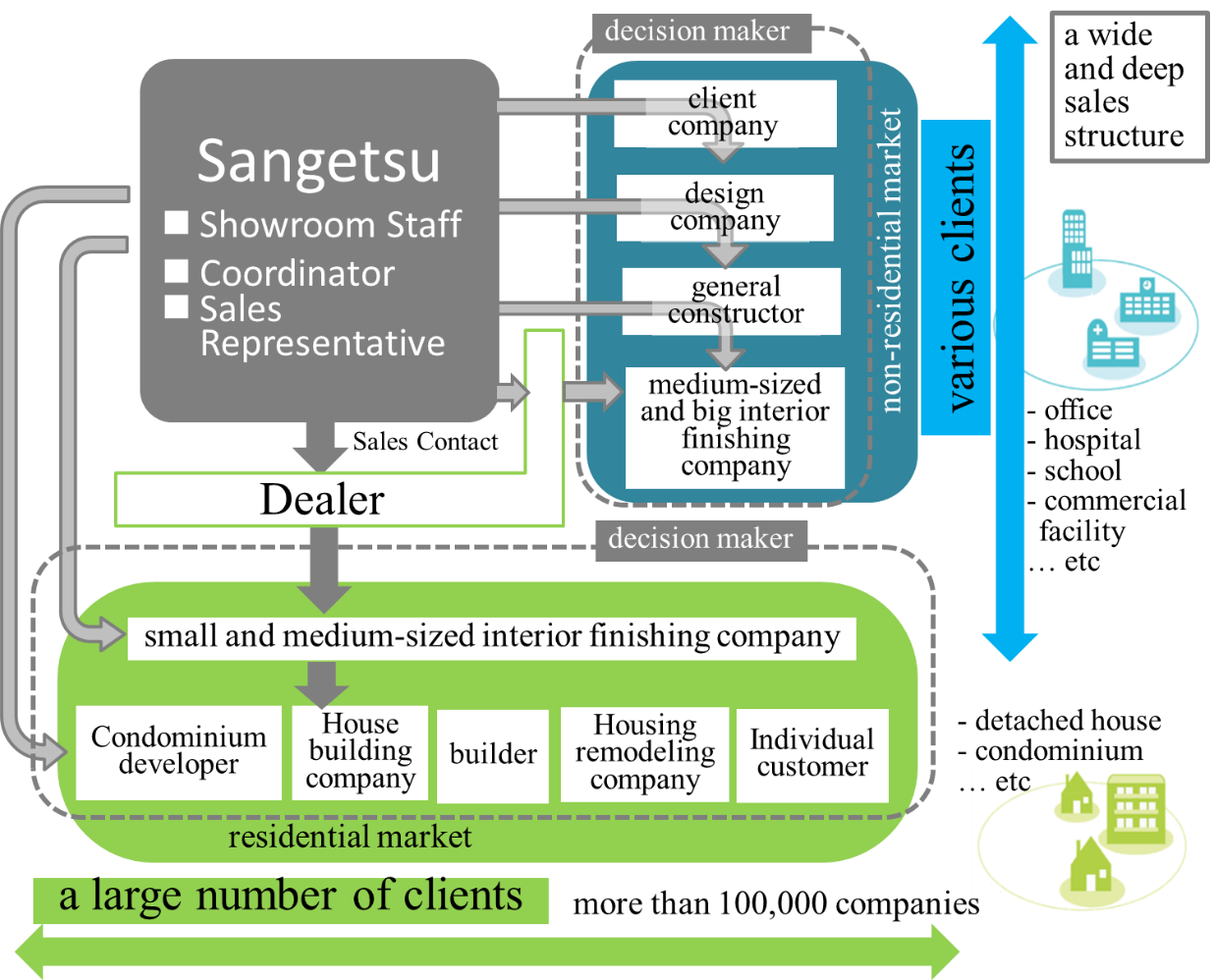

◎Marketing Structure

In addition to the headquarters located in Nagoya, Sangetsu maintains 8 regional offices and 50 marketing offices throughout Japan, with 8 of these marketing offices also hosting showrooms.

(Source: the company)

The downstream interior finishing process includes the final delivery of products, booking of sales, and receipt of cash. The main customers are interior construction companies and interior and building material shops that are serviced through dealers. Furthermore, public relations and advertising for products at the start of the process are also very important.

By the time the house or building is completed, a large number of players such as the client (owner), design office, design office, general contractor, subcontractor, house maker, etc. are involved, and the interior is finally selected from design and function. In many cases, decision making starts upstream.

Therefore, Sangetsu conducts public relations and advertising for its products through its sample books, showrooms, and others. In addition to these “passive” marketing activities, Sangetsu also conducts “proactive” marketing of its products through its Contract Sales Department and its 460 marketing staff to provide and gather information, and propose products to clients.

While the main marketing efforts are conducted through dealers, Sangetsu also conducts direct marketing to customers in the Nagoya and surrounding Chubu area, and the number of its directly accessed customer totals 6,000 in these regions alone. While the number of customers dealt with through dealers is not known, the total number of customers is estimated to amount to several tens of thousands nationwide.

◎Distribution Structure

Sangetsu maintains a network of 11 distribution centers nationwide. Most products are normally stocked at the Company’s distribution centers in Tokyo, Nagoya, Osaka and Fukuoka, with the number of products shipped from these centers surpassing 60,000 per day, and the out-of-stock ratio is 0.9% in average.

Sangetsu seldom asks their clients for backordering because the out-of-stocks are covered by surrounding distribution centers immediately.

Sangetsu’s nationwide distribution network makes “Just-in-Time” provision of products to match the interior construction schedules of its clients possible. Products are sourced from a wide range of over 100 supplier companies.

②“Exterior Business”

(FY3/19 Sales and Operating Income of ¥16,118 million and ¥594 million)

Sungreen Co., Ltd., which was turned into a subsidiary in 2005, sells doors, fences, terraces and other exterior products within Japan.

③Overseas business

(FY3/19 Sales and Operating Income of ¥20,920 million and ¥ -960 million)

This segment comprises 3 companies, i.e., Koroseal Interior Products Holdings, Inc. acquired in November 2016, Sangetsu (Shanghai) Textile Co., Ltd. established in April 2016, and Goodrich Global Holdings Pte. Ltd. acquired in December 2017.

1-5 ROE Analysis

| FY 3/12 | FY 3/13 | FY 3/14 | FY 3/15 | FY 3/16 | FY 3/17 | FY 3/18 | FY 3/19 |

ROE (%) | 3.5 | 4.1 | 4.6 | 3.7 | 5.6 | 6.0 | 4.2 | 3.5 |

Net income margin (%) | 3.50 | 3.90 | 4.14 | 3.33 | 4.77 | 4.84 | 2.89 | 2.23 |

Total asset turnover [times] | 0.84 | 0.88 | 0.93 | 0.91 | 0.95 | 0.88 | 0.91 | 0.94 |

Leverage [times] | 1.18 | 1.19 | 1.20 | 1.21 | 1.24 | 1.41 | 1.60 | 1.67 |

The new Medium-Term Business Plan calls for the quantitative target for return on equity of between 8% and 10% to be achieved by fiscal year ending March 2020.

In addition to reducing owned capital based on the capital policy, efforts to improve profitability are to be made.

1-6 Characteristics and strengths

①Business Model Capable of Yielding Stable Earnings

Sangetsu is a pioneer in the realm of “fabless operation” with no in-house manufacturing facilities and therefore has lower fixed expense burdens because they do not have to carry facilities for the manufacturing process. Besides, the Company boasts of over 12,000 products, sourced from over 100 suppliers, supplied to several tens of thousands of customers, which diversifies risk in many ways. Moreover, while Sangetsu may be considered as an economically sensitive company as its business and earnings performances are closely linked to trends in the construction market, the Company has never seen losses since its founding.

②“Creating,” “Proposing,” “Providing”

“Creating”

While the actual manufacturing of products is not conducted in-house, Sangetsu performs the planning, design and development process internally. The Company launched its original wallcoverings for the first time in 1965. Since the establishment of its fundamental values in 1973, Sangetsu has continuously made active investments for “creative designs,” one of the three principles of the Company. 25 in-house designers develop new and original versions of products based upon numerous basic designs. The cultivation of designers responsible for various products is done through participation in foreign exhibitions, communication with marketing staff, and discussions with outside design consultants as part of their on-the-job training. Furthermore, Sangetsu maintains a policy of actively taking the perceptions and opinions of younger designers and staff into consideration. Sangetsu also boasts of an overwhelming number of products of about 12,000 that far exceeds the number of products of its competitors. In addition, the Company conducts revisions of its products on a regular basis every 2 to 3 years with more than 30 types of sample books, which surpass by far those of its competitors.

(Source: the company)

“Proposing”

Nearly one third of all employees or about 460 staffs work in marketing functions at Sangetsu, the largest marketing function within the industry. These marketing staffs are assigned to 50 offices and 8 branches located throughout Japan and conduct proposal-based marketing to clients. Sangetsu also staffs its 8 showrooms with 80 employees. In addition, about 50 interior designers create design boards that combine samples of various products for customers to use when choosing interior products. This high level of proposal-based marketing capability is unmatched within the industry and sets Sangetsu apart from its competitors.

|

|

(Source: the company)

“Distribution system”

As mentioned earlier in this report, Sangetsu normally maintains inventories of all of its products so that they can be provided on a “Just-in-Time” basis using their nationwide distribution network. However, the Company is required to conduct speedy processing techniques as product orders are placed so that loss rates can be limited to avoid the maintenance of excess inventories and reduced efficiencies. Generally, wallcoverings are produced in rolls as long as 50 meters, and for example, Sangetsu cuts the rolls into a 30 meters and ships it when a 30 meters order is placed for shipment. The remaining segments of wallcoverings are then cut to match other orders to eliminate losses. This type of custom-made cutting technology has been cultivated over the long years of experience in the interior decorating business and is an important factor that differentiates Sangetsu from its competitors.

|

|

(Source: the company)

2. First Half of the Fiscal Year March 2020 Earnings Results

(1) Earnings Results

| 1H of FY 3/19 | Ratio to sales | 1H of FY 3/20 | Ratio to sales | YoY | Difference from the forecast |

Sales | 75,963 | 100.0% | 80,064 | 100.0% | +5.4% | +2.6% |

Gross profit | 23,538 | 31.0% | 26,403 | 33.0% | +12.2% | +4.4% |

SG&A | 21,350 | 28.1% | 21,858 | 27.3% | +2.4% | +1.2% |

Operating Income | 2,188 | 2.9% | 4,545 | 5.7% | +107.7% | +22.8% |

Ordinary Income | 2,658 | 3.5% | 4,895 | 6.1% | +84.1% | +25.5% |

Net Income | 1,839 | 2.4% | 3,635 | 4.5% | +97.7% | +34.6% |

*Unit: million yen

Sales grew, and profit rose considerably, exceeding the estimates.

Sales were 80 billion yen, up 5.4% year on year. Both the Interior and Exterior Businesses performed well. In the Interior Business, all product categories saw the growth of sales. The sales of the overseas business declined.

Operating income rose 107.7% to 4.5 billion yen. Gross profit rate increased 2 points, as the revision to the wholesale prices of products, which was started in October 2018 for coping with the increasing costs for raw materials and distribution, progressed. Gross profit increased 12.2% year on year. The growth rate of SG&A was only 2.4%, and profit increased significantly. Both sales and profit exceeded the respective estimates.

The financial results indicate that their efforts to improve business in various ways, including the improvement in logistics and the installation of a new mission-critical system, paid off. In addition, the company was able to revise prices for the first time in 5 years since 2014, almost as planned, while gaining the understanding of surrounding people by utilizing its position in the industry centered around wallpaper.

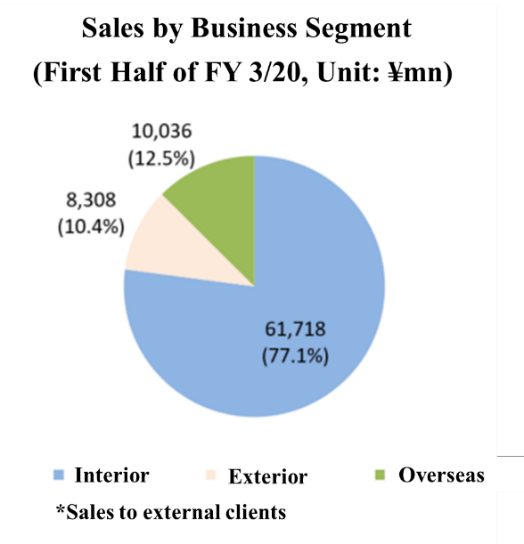

(2) Business Segment Trends

| 1H of FY 3/19 | Ratio to sales | 1H of FY 3/20 | Ratio to sales | YoY | Difference from the forecast |

Sales |

|

|

|

|

|

|

Interior segment | 56,621 | 74.5% | 61,898 | 77.3% | +9.3% | +2.3% |

Wallcoverings business | 27,278 | 35.9% | 29,880 | 37.3% | +9.5% | - |

Flooring Materials business | 20,131 | 26.5% | 21,907 | 27.4% | +8.8% | - |

Fabric Materials business | 3,929 | 5.2% | 4,126 | 5.2% | +5.0% | - |

Others | 5,281 | 7.0% | 5,984 | 7.5% | +13.3% | - |

Exterior segment | 7,307 | 9.6% | 8,308 | 10.4% | +13.7% | +10.0% |

Lighting segment | 1,902 | 2.5% | - | - | - | - |

Overseas segment | 10,342 | 13.6% | 10,036 | 12.5% | -3.0% | -1.6% |

Adjustments | -211 | - | -179 | - | - | - |

Total | 75,963 | 100.0% | 80,064 | 100.0% | +5.4% | +2.6% |

Operating Income |

|

|

|

|

|

|

Interior segment | 2,372 | 4.2% | 4,570 | 7.4% | +92.6% | +12.8% |

Exterior segment | 180 | 2.5% | 382 | 4.6% | +111.8% | +91.1% |

Lighting segment | 2 | 0.1% | - | - | - | - |

Overseas segment | -378 | - | -404 | - | - | - |

Adjustments | 11 | - | -2 | - | - | - |

Total | 2,188 | 2.9% | 4,545 | 5.7% | +107.7% | +22.8% |

*Unit: million yen. Ratio to sales of operating income represents the operating income margin. The fabric materials category of sales includes both curtains and upholstery.

➀Interior segment

Sales and profit grew.

The company strived to distribute the new sample books of wallpapers and curtains released in May to June 2019 in the market.

In order to cope with the skyrocketing costs for raw materials and distribution, the company revised the wholesale prices of products from October 2018, and revenue improved.

<Wallcovering Materials>

Sales grew. Sales volume declined slightly. As prices were broadly raised, profitability recovered. The company released “Fine 1000” as a sample book for housing in May, and released the mass-produced wallpaper “SP” while enriching the product lineup in June. Then, the company held exhibitions nationwide, to popularize it in the market as soon as possible and promote sales. The sales of FAITH, a certified fire-proof wallpaper, increased steadily in the non-residential field, because of the urban redevelopment and the firm demand from foreign people mainly in the Tokyo Metropolitan Area. The sales volume of middle-grade products recovered, but the sales of low-price mass-produced products are still on a recovery track.

<Flooring Materials>

Sales increased, and sales volume rose slightly. The sales of “the carpet tile DT/NT,” a fabric flooring material, drove the sales as the urban redevelopment in the Tokyo Metropolitan Area and the new construction and renewal of offices for reforming the ways of working were active. The sales of vinyl chloride floor tiles for the housing market and commercial facilities were healthy. Also, the efforts for enhancing marketing in the upstream market paid off.

<Fabrics>

Sales grew, and sales volume increased a little. The company released “AC” as a sample book for curtains for housing in May, and implemented a campaign linked with “Fine 1000,” a sample book for wallpapers released at the same timing as “AC,” for sales promotion taking advantage of the strengths of its comprehensive interior business. “Simple Order,” which was developed while setting a single low price so that customers can easily choose a product, contributed to sales.

<Others>

Sales increased. The performance of Fairtone Co., Ltd., which operates the installation system, and the fees for installation work are included.

②Exterior Business

Sales and profits increased.

The repair and restoration work after the natural disaster, which occurred in the previous term, continued, and the refurbishment for disaster prevention and construction of new buildings, which had been delayed, progressed. “Fences” and “carports” contributed to sales. In addition, the company acquired a large-scale order, and increased orders for works. Accordingly, the Exterior Business performed well. As for the renovation of houses, there was rush demand before the consumption tax hike.

➂Overseas Business

Sales dropped, and loss augmented. The overseas business was affected by the decline of the non-residential market, especially the U.S. hotel renewal market, and the intensification of competition with other companies in China and Southeast Asia.

As for Koroseal, which targets the North American market, the sales of products of the European wallpaper VESCOM, whose distributorship was acquired by Koroseal in September 2018, contributed. In addition, as a measure for promoting business in the thriving digital printing field in the U.S., the company installed new equipment and started operating it in May 2019, and established a new manufacturing line for wallpaper in July, to prepare for full-scale operation and boost its productivity and earning capacity. As for Sangetsu (Shanghai), which targets the Chinese market, wallcovering and flooring materials contributed to sales, thanks to the shift to infill of condominiums (housing with interiors) and the increase of medical facilities in the aging society.

Goodrich, which targets the Southeast Asian market, proceeded with the establishment of a cooperative system with Sangetsu (Shanghai) for exerting synergy in the corporate group in marketing in the Chinese market and product development.

(3) Financial standing and cash flows

◎Main BS

| End of Mar.19 | End of Sep.19 |

| End of Mar.19 | End of Sep.19 |

Current Assets | 97,674 | 95,869 | Current Liabilities | 39,389 | 36,863 |

Cash, Equivalents | 27,220 | 28,373 | Payables | 26,522 | 25,196 |

Receivables | 50,504 | 44,878 | Noncurrent Liabilities | 31,342 | 30,732 |

Marketable Securities | 300 | 3,378 | Long-Term Debt | 18,925 | 18,301 |

Inventories | 17,331 | 17,791 | Total Liabilities | 70,732 | 67,595 |

Noncurrent Assets | 73,200 | 71,641 | Net Assets | 100,143 | 99,915 |

Tangible Assets | 35,688 | 36,123 | Shareholders’ Equity | 97,897 | 98,251 |

Intangible Assets | 16,686 | 15,677 | Treasury Stock | -2,889 | -3,187 |

Investments, Others | 20,825 | 19,841 | Total Liabilities, Net Assets | 170,875 | 167,511 |

Total Assets | 170,875 | 167,511 | Capital Adequacy Ratio | 58.0% | 59.1% |

*Unit: million yen.

Current assets decreased 1.8 billion yen from the end of the previous term, due to the decline in receivables, etc. Noncurrent assets dropped 1.5 billion yen from the end of the previous term, due to the intangible assets, goodwill amortization, etc. related to Koroseal and mission-critical systems. As a result, total assets decreased 3.3 billion yen to 167.5 billion yen.

Total liabilities dropped 3.1 billion yen from the end of the previous term to 67.5 billion yen, due to the decrease in payables. Net assets decreased 200 million yen to 99.9 billion yen, due to the drop in valuation difference on available-for-sale securities, the increase in treasury shares, etc. Capital-to-asset ratio rose 1.1 points from 58.0% as of the end of the previous term to 59.1%.

◎Cash Flow

| 1H of FY 3/19 | 1H of FY 3/20 | Increase/decrease |

Operating Cash Flow | 4,371 | 8,022 | +3,651 |

Investing Cash Flow | 5,269 | -3,247 | -8,516 |

Free Cash Flow | 9,640 | 4,775 | -4,865 |

Financing Cash Flow | -3,944 | -3,533 | +411 |

Cash and Equivalents | 25,406 | 27,868 | +2,462 |

*Unit: million yen.

The surplus of operating CF expanded due to the increase in net income before taxes and other adjustments, etc., but investing CF turned negative due to the purchase of securities, etc. Then, the surplus of free CF shrank.

The cash position improved.

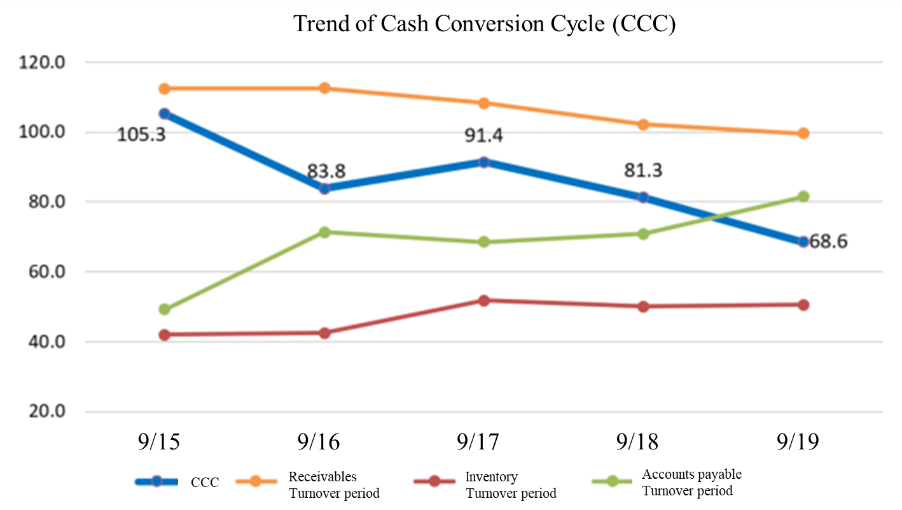

CCC (cash conversion cycle: the number of days between procurement and cash collection through sale), on which the company puts importance, is now 60 to 75, achieving its target level.

3. Fiscal Year March 2020 Earnings Forecasts

(1) Earnings Forecasts

| FY 3/19 | Ratio to sales | FY 3/20 Est. | Ratio to sales | YoY | Progress rate |

Sales | 1604.2 | 100.0% | 1630.0 | 100.0% | +1.6% | 49.1% |

Gross profit | 507.2 | 31.6% | 525.0 | 32.2% | +3.5% | 50.3% |

SG&A | 448.2 | 27.9% | 445.0 | 27.3% | -0.7% | 49.1% |

Operating Income | 58.9 | 3.7% | 80.0 | 4.9% | +35.7% | 56.8% |

Ordinary Income | 66.9 | 4.2% | 83.0 | 5.1% | +23.9% | 59.0% |

Net Income | 35.7 | 2.2% | 57.0 | 3.5% | +59.2% | 63.8% |

*Unit: 100 million yen. Estimates are those of the Company

There is no revision to the earnings forecast. Sales, profit, and profit rate will increase.

The earnings forecast has not been revised, because there are uncertainties over the overseas business, the domestic market trend, etc.

Sales are expected to rise 1.6% year on year to ¥163 billion. Gross profit is projected to increase 3.5% year on year, exceeding the rate of sales growth, and gross profit rate is estimated to rise 0.6 points. In addition to the effect from the price increase, the company will improve profitability in overseas segments.

Operating income is estimated to rise 35.7% year on year to ¥8 billion.

The dividend is forecasted to be ¥57.00/share, up ¥0.5/share over the previous term. The estimated payout ratio is 61.5%.

(2) Business Segment Trends

| FY 3/19 | Ratio to sales | FY 3/20 Est. | Ratio to sales | YoY | Progress rate |

Sales |

|

|

|

|

|

|

Interior | 1195.0 | 74.5% | 1,265.0 | 77.6% | +5.9% | 48.9% |

Exterior | 161.2 | 10.0% | 155.0 | 9.5% | -3.9% | 53.6% |

Lighting | 42.2 | 2.6% | - | - | - | - |

Overseas | 209.2 | 13.0% | 215.0 | 13.2% | +2.8% | 46.7% |

Adjustment | -3.5 | - | -5.0 | - | - | - |

Total | 1604.2 | 100.0% | 1,630.0 | 100.0% | +1.6% | 49.1% |

*Unit: 100million yen.

| FY 3/19 | Ratio to sales | FY 3/20 Est. | Ratio to sales | YoY | Progress rate |

Operating Income |

|

|

|

|

|

|

Interior | 61.7 | 5.2% | 85.0 | 6.7% | +37.7% | 53.8% |

Exterior | 5.9 | 3.7% | 4.0 | 2.6% | -32.7% | 95.6% |

Lighting | 0.6 | 1.5% | - | - | - | - |

Overseas | -9.6 | - | -7.2 | - | - | - |

Adjustment | 0.2 | - | -1.8 | - | - | - |

Total | 58.9 | 3.7% | 80.0 | 4.9% | +35.7% | 56.8% |

* Unit: 100 million yen. Ratio to sales of operating income represents the operating income margin. The operating income of the overseas business is after amortization of goodwill.

◎Interior Business

As the company was able to offset part of SG&A by raising prices, they aim to maintain these prices and recover sales volume and market share for further improvement from now on. They also plan to recover the market share by revising the sample books for mass-produced wallcovering materials, where the company is struggling against other competitive companies.

◎Overseas Business

The company is expected to incur an operating loss of ¥30 million even before posting amortization of goodwill, and they acknowledge that improving sales and profits is the main goal this term as well.

They aim to fortify their management structure and cost competitiveness by installing new equipment.

4. Situation of the Mid-term Management Plan “PLG2019” (2017-2019) and Problems with it

The progress of the medium-term management plan so far is as follows.

(1) Functional enhancement

①Streamlining of business operation and marketing structure

Streamlining of business operation

Thanks to the operation of the new mission-critical system and the adoption of BPO, the streamlining of the order-receiving process is progressing rapidly.

The company had been receiving orders online, but its employees were involved with inputting, confirmation, etc. and the rate of involvement of employees as of April 2016 was as high as 60.9%. It did not streamline the order-receiving process to a sufficient degree.

In order to improve that situation, the company started BPO (Business Process Outsourcing) on a full-scale basis in January 2017, and started the operation of the new mission-critical system in October 2018. As a result, the rate of involvement of employees decreased to 2.5% in October 2019.

The company became able to allocate human resources to the strengthening of the practical business, including marketing and back-office tasks.

Marketing structure

As the function to promote marketing has been improved, the marketing structure has changed from the individual-based to the team-based, to brush up its marketing capability.

Enhancement of marketing activities in local areas

The company concentrates on the cultivation of local areas where its market share has been relatively small.

In addition to the establishment of Sangetsu Okinawa, Chugoku-Shikoku Branch relocated the office and showroom from Okayama to the downtown of Hiroshima City in July 2019.

② Logistics

Improvement of logistics centers

When selecting locations for bases, the company will consider sustainability, efficiency, and scalability.

While establishing or integrating Tokyo Metropolitan Area LC (logistics center), Hokkaido LC, and Chubu LC, the company established Okinawa LC.

The equipment in Tohoku LC, Chugoku-Shikoku LC, and Kyushu LC has been renewed.

The company will put energy into the new Kansai logistics center.

The old Kansai LC had two sites, deterioration progressed, and its area was small. Meanwhile, the warehouse area of the new Kansai LC is 13,000 tsubo ( 42,900 m2), so that the total floor area of warehouses in Japan is 71,400 tsubo ( 235,600 m2). The company is planning to mechanize the conveyance of products inside distribution facilities, processing, such as cutting, and so on, and aims to start the operation of the core distribution center in western Japan in January 2021.

After the start of operation, the company will automate equipment and develop systems for maintaining and improving long-term services install them as a model case in other LCs in Tokyo, etc., even though it causes a deficit.

Redevelopment of its own delivery network

In order to cope with the distribution cost, which is estimated to keep rising, the company is striving to redevelop its own delivery network that does not rely on the service of sharing trucks that run the same routes regularly.

In addition to the development of systems and joint delivery according to the characteristics of each region and the establishment of depots that store products temporarily, the company is reconsidering transportation vehicles.

(2) Geographical expansion: activities in the overseas segment

The U.S.

KOROSEAL is taking measures for drastic reform and improvement.

In July, Mr. Victor Paul, who had been serving as president of a Canadian subsidiary, was appointed as new CEO. He is expected to grasp situations and take action appropriately.

As for equipment, the operation of two new lines with the cutting-edge wallpaper production equipment is to be started in November 2019 and January 2020, respectively.

With the new equipment, it will be possible to print, glue films to backing paper, and emboss products in an integrated manner, reducing loss considerably. In addition, it will be possible to realize more sophisticated designs with seven-coloring and increase the speed of production.

Furthermore, the company will enhance product competitiveness by increasing and training designers and reviewing all products based on the short-term and mid/long-term plans, and increase the number of sales staff members, which is currently slightly over 100. Especially, it is considered necessary to improve the capability of developing products from the viewpoint of customers.

The company will also improve its brand while promoting the Koroseal brand.

China and Southeast Asia

The company will review its business structure in China and Southeast Asia.

Goodrich mainly handles U.S. and European products, and possess competitive designs and designers, but had a problem that the marketing efficiency per staff was low.

On the other hand, Sangetsu (Shanghai) mainly handles the products of Sangetsu and has a high marketing efficiency per staff member.

Considering this situation, the company will develop a structure that can exert synergy through the collaboration between the two companies.

Some employees of Sangetsu (Shanghai) will be transferred to Goodrich China or take another post in Goodrich China, while Goodrich will employ younger executives, including those in charge of product development, and enrich stocks for expanding sales in small lots.

As for product strategies, the company will release new sample books, develop its brand by unifying manners, and review the product composition while utilizing suppliers of Sangetsu according to regional characteristics, including designs and tariffs.

(3) ESG/CSR

Tightening of governance

In order to maintain and improve the transparency of corporate governance, the company has appointed 2 executive directors and 5 directors who serve as members of the audit committee.

In addition, the company held a session for introducing the company to individual shareholders in Tokyo and a guide tour for institutional investors in Tokyo Logistics Center, to deepen their understanding of the company.

(4) Capital policy

This term, the company acquired 811,000 treasury shares worth 1.63 billion yen by the end of September, and retired 600,000 treasury shares on July 31.

For interim dividends, the company paid a total of 1.73 billion yen, so that the total amount of shareholder return is 3.36 billion yen.

Total return ratio falls below those in the previous term and the term before that, but the company recognizes that it is still above the market average.

5. Conclusions

Thanks to the effects of business improvement measures the company has taken so far and the steady penetration of revised prices, sales and profit grew, while profit rate increased considerably. Progress rates seem to be healthy, but the full-year earnings forecast remains unchanged, because there are uncertainties over the effects of the rush demand before the consumption tax hike, the improvement in the overseas business, etc. We would like to keep an eye on how much the company can increase sales and profit in the second half of this term, which is the final fiscal year of the mid-term management plan.

The points of the next mid-term management plan are how the company will enhance the earning capacity of the Interior Business, which is the mainstay, as the operation of the new Kansai LC will begin, and how the overseas business will increase revenue.

<Reference 1: Mid-term Management Plan “PLG 2019” (2017-2019) Overview>

◎Vision

Based upon the “Corporate Creed: Integrity” and “Brand Philosophy: Joy of Design”, Sangetsu has created its Medium-Term Business Plan “PLG 2019” with the goal of establishing strong roots within both the Japanese and overseas markets by leveraging the Group’s “diversified product lineup and highly specialized knowledge.”

“P” stands for personal and reflects the highly professional employees that helps it to link to people outside of the Company.

“L” stands for local and refers to the strong positioning in local markets.

“G” stands for global and represents Sangetsu’s global lineup of products and designs.

◎Targets for the Final Year 2019

Target | ROE: 8~10% |

Associated Targets | ・Sales: ¥165.0~¥175.0 billion ・Net Income: ¥8.0~¥10.0 billion ・Capital: ¥105.0~¥100.0 billion ・CCC: 75~60 days |

In line with the previous Medium-Term Business Plan, Sangetsu will focus upon raising its capital efficiency as a common goal shared with all of its stakeholders. The details of its sales targets are outlined below.

Interior Business | ¥122.0~¥126.0 billion |

Exterior Business | ¥15.5~¥16.0 billion |

Lighting Business | ¥5.0 billion |

Overseas Business (NA, China, SE Asia) | ¥22.5~¥28.0 billion |

Total Sales | ¥165.0~¥175.0 billion |

* The lighting business was transferred in April 2019.

◎Themes

As a basic policy, Sangetsu has identified the following measures as part of its strategy of “strengthening the function and expanding geographic sales of the interior materials business (planning, procurement, logistics, sales).”

(1) Business Strategy for Growth

① Realizing Stable Growth in Earnings through Expansion and Strengthening of the Value Chain Activities Realm in Japan as a Fundamental and Stable Source of Revenues

Sangetsu will promote “development and procurement of materials and raw materials through alliances with superior suppliers within and outside of Japan”, “strengthen interior coordinator proposal and installation capability”, “fortify alliances and cooperation with dealers” and “conduct reviews of internal sales structure”.

② Strengthen Activities in Overseas Markets with High Growth Potential, Fortify Product Lineup and Functionality to Promote Geographic Expansion

Local logistic and sales structures will be strengthened in important markets including North America, Asia and others.

③ Create a Global Product Planning, Procurement Structure to Promote Global Designs, Cultivate Global Product

Sangetsu will strengthen cooperation with local facilities in Japan, United States and China for the implementation of “cooperation between Sangetsu globally and superior overseas product manufacturers” and “efforts to promote joint marketing of products and deployment of European and Japanese designs”.

④ Strengthen Consolidated Management Structure to Pursue Comprehensive Synergies, Integrated Management of Affiliates Responsible for Special Markets, Functions and Geographic Regions

A management structure system will be introduced to maximize business synergies and conduct clearly controlled earnings management, and to act as a surveillance support structure for the overall Group.

A consolidated management division will be newly established with authority to oversee the entire Group.

In addition, regularly scheduled monitoring and communications will be introduced to increase the overall effectiveness of the Group.

⑤ Business Format Conversion Trials to be Conducted with a View to the New Medium Term Business Plan

In order to pursue synergies and leverage business resources and the characteristics of each Group company, Sangetsu will conduct trials and promote business format conversion.

(2) Strengthen Human Resources

In order to cultivate real professionals, all of the Sangetsu Group companies will implement measures to 1) cultivate professional human resources, 2) conduct strict adherence to performance, 3) promote diversity, 4) reform work styles and 5) maintain a healthy management structure.

(3) Strengthen the Earnings Management Structure

① Strict Control, Reduction of Sales, General and Administrative Expenses

A chief cost controller will be appointed, and sales, general and administrative expense control methodologies will be facilitated. Also, the total number of staff of the parent company Sangetsu will be reduced.

② CCC Management Will be Introduced for All Group Companies

Targets for return on equity and CCC management through Dupont analysis on a consolidated basis will be promoted.

③ Sangetsu to Clearly Define and Promote Management Benchmarks for Each Business, Company

Targets for sales and gross income by employee will be established for each of the Group companies.

(4) ESG/CSR Policies

① E: Environment

The Sangetsu Group will assess the environmental burden of its overall businesses to create a structure that seeks to achieve sustainability and prevent global warming.

・A plan to achieve CO2 zero emissions will be created.

② S: Society

☆Provide support to workers including those who are socially vulnerable to foster diversity of each Group company.

・Retain women in 15% of all management positions (Actual 12.0% as of Apr. 2019).

・Retain workers with disabilities as 3% of the total workforce (2.7% as of the end of Mar. 2019).

☆Promote Corporate Social Responsibility in Supply Chain Function

☆Expand Societal Contribution Activities of Employees

・Provide support for interiors of childcare welfare facilities (Target: Over 20 facilities per year)

➂ G: Governance

☆Strict implementation of compliance, maintain and improve transparency of corporate governance activities

・Improve communications with shareholders, investors, employees, business partners and all other stakeholders

(5) Capital Policy

① Financial Policy for Improvement of Capital Efficiency

Sangetsu will continue to conduct share buybacks and stable increases in dividend payments with a goal of reducing its net worth to between ¥100.0 and ¥105.0 billion (¥110.3billion as of FY3/17) with a view to conditions within the capital markets.

② Shareholder Return Policy of the Medium Term Business Plan

・Achieve over 100% total consolidated shareholder return ratio over a three year period

・Conduct stable increases in dividends over the long term

・Conduct share buybacks flexibly and in response to stock market conditions

We provide details of our capital procurement and capital allocation below.

Capital Creation, Sourcing |

| Capital Allocation | ||

Cash, Equivalents as of End FY3/17 | ¥30.0 billion |

| LT Investments | ¥10.0~¥25.0 billion |

Operating CF (Medium Term Plan) | ¥31.0~¥38.0 billion | = | Shareholder Returns | ¥25.0~¥33.0 billion |

Debt (Medium Term Plan) | ¥0~¥22.0 billion |

| Term End Cash, Equivalents | ¥25.0~¥30.0 billion |

Total | ¥61.0~¥90.0 billion |

| Total | ¥60.0~¥88.0 billion |

<Reference 2:Regarding Corporate Governance>

◎ Organization type and the composition of directors

Organization type | Company with audit and supervisory committee |

Directors | 7 directors, including 4 outside ones |

◎Corporate Governance Report

Last update date: :July 2, 2019

<Basic Concept>

Our corporate creed is “Integrity,” and we aim to foster good relationships with all stakeholders to improve our corporate value and grow stably on a long-term basis.

To attain these goals, we consider that it is essential to improve our corporate governance based on the transparency, swiftness, and efficiency of business administration.

Our company has been reorganizing to a company with an audit committee, with the aim of strengthening the auditing and supervising functions of the board of directors, by having outside directors join the management.

Under this governance system, we will make efforts to further improve our corporate value.

<Reasons for Non-compliance with the Principles of the Corporate Governance Code (Excerpts)>

The company implements each principle of the Corporate Governance Code.

<Disclosure Based on the Principles of the Corporate Governance Code (Excerpts)>

Principles | Disclosure contents |

Principle 1-4 So-called strategically held shares | 1. Policy on strategically held shares We make decisions on shares to strategically hold for the medium- to long-term by comprehensively judging from various perspectives, considering companies with which we should newly forge relationships and companies with which we should continue to strengthen relationships as our clients for business strategies. With regard to holding shares, each year we will check the associated cost and returns, and if it is determined that holding the shares has no strategic value in the medium-and long-term, we will sell the shares, and conduct operations based on that decision. The Board of Directors’ decision and a disclosure of the shares we decide to continue holding will appear in the “Shareholding status” column of the securities report. 2. Attitude toward exercise of voting rights We will keep an open dialogue and communicate through various channels, while respecting the management policies of companies that we invest in. We will make a comprehensive judgment based on company’s stance on shareholder returns and improving corporate value in the medium-to long-term, their corporate governance policies, and CSR activities. We will also separately examine whether holding the shares of the company is constructive to our goals and whether it will lead to improving the corporate value of the company we invest in. |

Principle 5-1 Policy on constructive communication with shareholders | Aiming to establish good relationships with shareholders by encouraging constructive communication with them and striving for information disclosure and interaction with high transparency, our company proactively performs IR activities as follows: ・In our company, the Chief Executive Officer manages the implementation of IR activities. ・Our company has established the Public Relations and IR Department for rational communication with our shareholders and swift IR activities. ・The Chief Executive Officer, the executive in charge, and the Public Relations and IR Department carry out interviews with both Japanese and overseas institutional investors, and analysts, upon their request. ・Although the IR department specializes in handling IR activities, other departments such as the headquarters of each business, the Finance and Accounting Department, and the Office of the President’s Corporate Planning Division cooperate with the IR department to provide information with higher effectiveness. ・Our company announces our financial statements, arranges financial results briefings for investors, and participates in IR events for individual investors hosted by stock exchanges and the like to hold explanatory meetings. ・Since 2017, we have held company briefings for shareholders at our Shinagawa showroom in mid-July, after the general meeting of shareholders. This has created opportunities to introduce our company to mainly individual shareholders in the Kanto region. All directors attend this briefing session, and the president and executive officers describe the company. In September 2018 and March 2019, we held IR meetings related mostly to governance, led by directors (who are also audit and supervisory committee members) and institutional investors. ・Our company publishes on our website explanatory material we used at the above-mentioned events (the English-version of such material is also published as needed). ・Our company creates an integrated report for every fiscal year and publishes such reports both in Japanese and in English through our website. ・Our company conducts activities which contribute to enhancement of our shareholders’ understanding about various items, including our management strategy, business environment, business progress, and financial information, through direct communication and material published on our website. ・Our company responsibly utilizes opinions obtained from interaction with our shareholders and investors for administrative improvement through The Public Relations and IR Department. ・Our company properly deals with the management of insider information in accordance with the regulations for the management of insider trading (regulations for the prevention of insider trading), by assiduously managing unpublished material facts. |

This report is intended solely for information purposes, and is not intended as a solicitation for investment. The information and opinions contained within this report are made by our company based on data made publicly available, and the information within this report comes from sources that we judge to be reliable. However, we cannot wholly guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness or validity of said information and opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration. Copyright(C) 2019 Investment Bridge Co., Ltd. All Rights Reserved. |