Bridge Report:(9327)e-LogiT Fiscal Year ended March 2021

![]()

President Ryoichi Kakui | e-LogiT Co., Ltd. (9327) |

|

Company Information

Exchange | TSE JASDAQ |

Industry | Warehousing and transportation-related business |

President | Ryoichi Kakui |

HQ Address | Murataya Building 5th floor, 68 Kanda Neribeicho, Chiyoda-ku, Tokyo |

Year-end | March |

URL |

Stock Information

Share Price | Shares Outstanding (Term-end) | Market Cap. | ROE (Act.) | Trading Unit | |

¥1,619 | 3,400,000 shares | ¥5,504 million | 9.6% | 100 shares | |

DPS (Est.) | Dividend Yield (Est.) | EPS (Est.) | PER (Est.) | BPS (Act.) | PBR (Act.) |

TBD | - | ¥57.60 | 28.1x | ¥605.03 | 2.7x |

*Stock prices as of the close price on June 21, 2021. All figures are taken from the brief financial report for the term ended March 2021.

Earnings Trends

Fiscal Year | Net Sales | Operating income | Ordinary income | Net income | EPS | DPS |

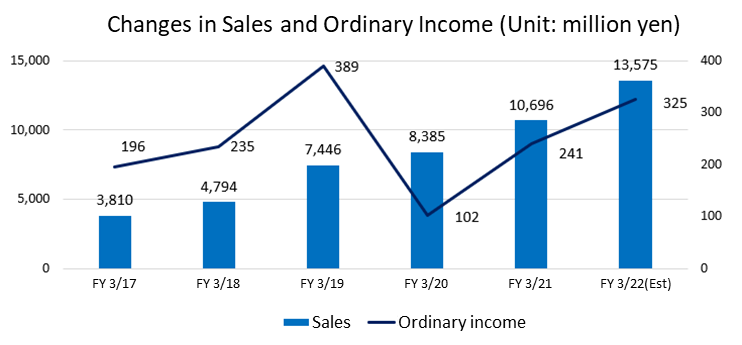

Mar. 2018 (Actual) | 4,794 | 234 | 235 | 158 | 58.68 | 5.25 |

Mar. 2019 (Actual) | 7,446 | 381 | 389 | 269 | 99.89 | 6.75 |

Mar. 2020 (Actual) | 8,385 | 84 | 102 | 76 | 28.35 | 2.00 |

Mar. 2021 (Actual) | 10,696 | 238 | 241 | 151 | 53.80 | 3.00 |

Mar. 2022 (Forecast) | 13,575 | 323 | 325 | 197 | 57.60 | TBD |

* Unit: million-yen, yen. Estimates calculated by the company.

This Bridge Report introduces e-LogiT Co., Ltd.’s profile, growth strategy, business performance trends, and an interview with President Kakui.

Table of Contents

Key Points

1.Company Overview

2. Fiscal Year ended March 2021 Earnings Results

3. Fiscal Year ending March 2022 Earnings Forecasts

4. Interview with President Kakui

5. Conclusions

<Reference: Regarding Corporate Governance>

Key Points

- The company offers all logistical services in one place as fulfillment service, mainly logistics agency service for mail-order companies, including product storage, picking, packing, and delivering. Their competitive advantage is their ability to flexibly respond to increases in shipment volume of shippers by utilizing Fulfillment Centers (FCs), which use a dominant marketing strategy. The company aims to make omni channel logistics, including physical stores in addition to mail-order logistics and e-commerce, as its business domain.

- For the term ended March 2021, sales increased 27.6% year on year to 10,696 million yen. In addition to acquiring new customers, the shipment volume of existing customers expanded. Gross profit was up 58.0% year on year, and gross profit margin augmented 1.5 points. Operating income rose 180.8% year on year to 238 million yen, absorbing the cost rise including upfront investment, such as an increase in packing freight charges due to the rise in shipment volume and the increases in labor and outsourcing costs for product movement due to the opening of the new FC. The company achieved significant growth in profits as planned. The dividend was set at 3.00 yen/share, an increase of 1.00 yen/share from the previous term. The payout ratio is 5.6%.

- For the term ending March 2022, sales are expected to increase 26.9% year on year to 13,575 million yen. The company will concentrate resources and strengthen sales capabilities to achieve high top-line growth. The number of partner companies will rise due to the acquisition of new customers, and the shipment volume of existing customers will expand. Operating income is forecasted to increase 35.6% year on year to 323 million yen. Growing sales will make up for the upfront investments, such as the opening of Saitama Soka FC in June 2021 and the hiring of 32 new graduates. The dividend is undecided currently.

- We asked President Kakui about the company’s competitive advantage, challenges, and message to investors. He has stated that, “With the spread of the COVID-19, consumer behavior has changed significantly, with people in their 70s, who we previously thought to be unlikely to use e-commerce, are actively using it. With this business environment as our tailwind, we would like to concentrate our management resources and expand sales and profits. So, by all means, we would like you to support our endeavor from a medium- to long-term perspective.”

- After the listing in March, the stock price has been sluggish recently. However, this is not limited to this company, but it can be seen among many EC-related stocks. This must be caused by the weakening trend to buy stocks related to housebound consumers amid the pandemic, since vaccination is progressing.

- However, it is certain that the EC market will continue to expand regardless of the demand of people staying at home due to the COVID-19 pandemic. The business environment surrounding the company will continue to be favorable. In addition, the opening of new FCs is a factor in cost increase in the short term. However, if the number of existing FCs increases, the negative impact of the cost increase due to the opening of new facilities will become smaller. On the contrary, its effect of increasing sales will contribute to business performance.

- A significant increases in sales and profits are expected in the current term, too. However, we will continue to pay attention to whether the company can significantly increase its business performance through its competitive advantages of its dominant strategy of using large FCs and capability to respond to surges.

1. Company Overview

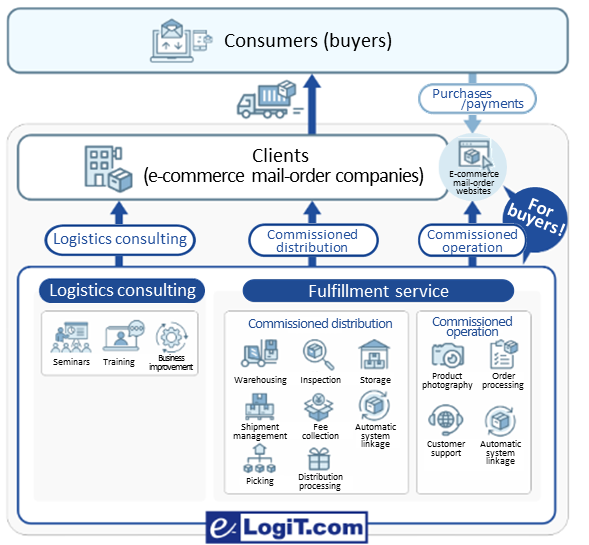

The company offers not only logistics agency service that store, pick, pack, and deliver products for mail-order companies, but also operation agency service as a one-stop fulfillment service that provides customer support to help companies by operating their websites, including product photography, order processing, and response to inquiries, in order to meet the needs of mail-order companies and mail-order users (end customers).

The company holds a strong competitive advantage with their ability, whitch is called “response to surges”, to flexibly respond to increases in shipment volume of shippers by utilizing its FCs (Fulfillment Center) that implement the dominant strategy.

It aims to make omnichannel logistics, including physical stores in addition to mail-order logistics and e-commerce, its business domain.

【1-1 Corporate History】

The company was founded in February 2000 by President Kakui, with the aim of acting as the logistics agency and offering consulting on logistics operations for the internet mail-order companies.

Under the concept of “Strategic Logistics” (improving sales through logistics), the company achieves “sales-earning logistics” that persuades the end-users who purchase products to become repeat customers through its operational efficiency, stemming from various aggressive schemes and its in-house-developed Warehouse Management System (WMS), rather than being contented with being a simple subcontractor. The company’s business has been growing steadily with the enthusiastic support from its clients (shippers), and it was listed on the JASDAQ Market of the Tokyo Stock Exchange in March 2021.

【1-2 Corporate Philosophy】

The company set the following vision, mission, and value.

Vision | Staying ahead of changes to keep innovating experiences that move a person’s heart |

Mission | Aim to be the No.1 company in “creating heart moving experiences” that realizes high added value through

-Having a bird’s-eye view of distribution from a global perspective -Exploring solutions that help individual customers above all -Aiming to become a group of mail-order and retail logistics professionals -Utilizing innovative technologies |

Value | -Always think and act ahead for customers and win their trust -Generate success with our massive proposal-making in collaboration with shippers -Keep learning and improving oneself with fresh eyes -Try it first and try it soon, then finish it with everyone’s effort -Enjoy your work with a humble and honest heart |

Although the company’s clients are shippers, the company keeps at the heart of its management to bring the heart moving experiences gained from goods and services to the mail-order users (end customers) who purchase products on mail-order websites by delivering products quickly and carefully, and it believes that increased sales through the end users’ greater satisfaction and repeated purchases will lead to the shippers’ own greater satisfaction.

【1-3 Market Environment】

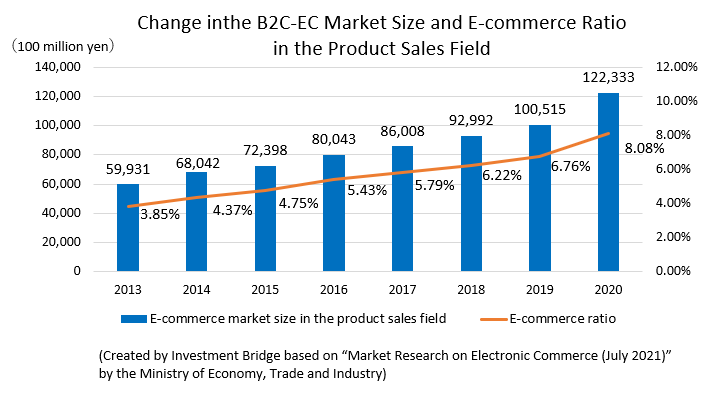

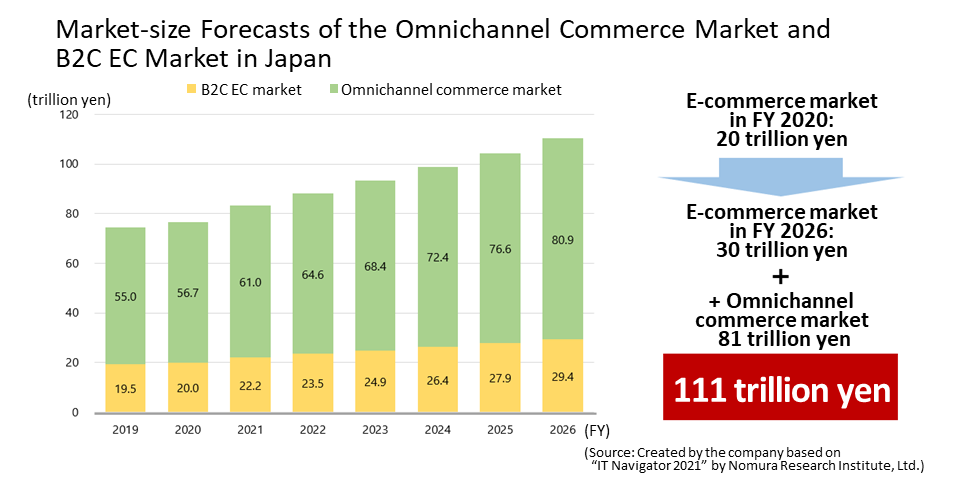

According to a report by the Ministry of Economy, Trade and Industry, the B2C-EC market size in the field of domestic goods sales was 12.2 trillion yen in 2020, representing the compound annual growth rate (CAGR) of 10.7% from 5,993 billion yen in 2013. In addition, the e-commerce ratio (the ratio of e-commerce market size against the entire commerce market size) continues to grow every year.

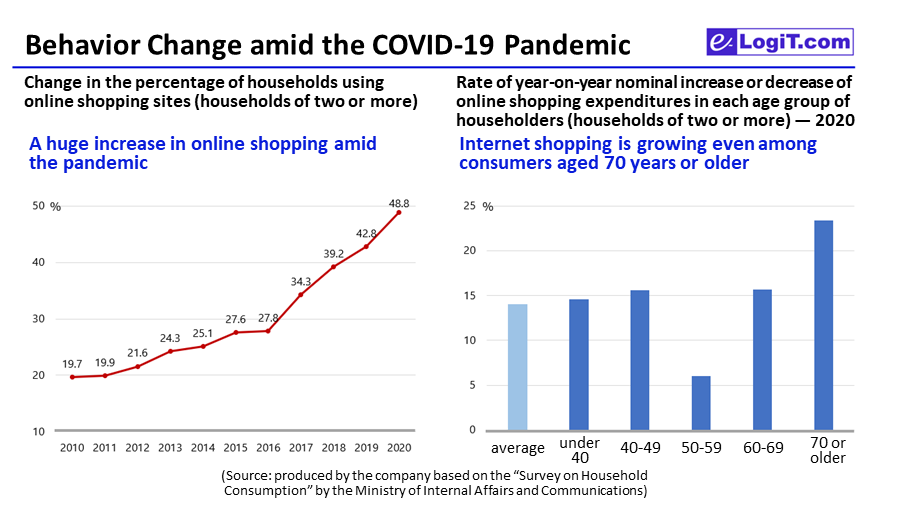

As this report and the company’s data show, the use of online shopping sites is growing significantly due to the demand from housebound consumers caused by the spread of the COVID-19.

(Taken from the reference material of the company)

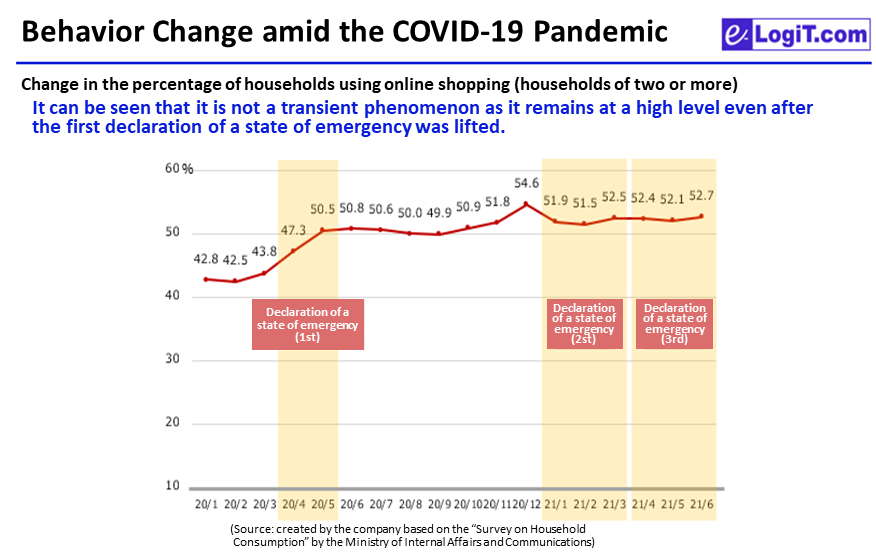

In addition, the percentage of the households (households of two or more) using online shopping has remained over 50% even after the first state of emergency in 2020 was lifted, and it can be seen that the increase in online shopping is not a transient consumption behavior.

(Taken from the reference material of the company)

The pace of expansion of the e-commerce market is expected to accelerate further due to the change of consumer behavior triggered by the COVID-19, the popularization and expansion of cashless payment, and the spread of D2C (Direct to Consumer) in which manufacturers sell their products directly to customers on e-commerce sites.

In an environment where the scale of the omnichannel commerce market is expected to reach 80 trillion yen, the company aims to make omnichannel logistics, including physical stores in addition to mail-order logistics and e-commerce, its business domain.

(Taken from the reference material of the company)

【1-4 Business Description】

(1) Outline of services

For mail-order companies that outsource logistics operations, the company mainly offers logistics agency service and operation agency service as one-stop fulfillment service that meets the needs of mail-order companies and mail-order users (end customers).

It also provides logistics consulting service to companies that operate logistics operations in-house.

The fulfillment service is a service that provides collective agency services related to the operation of mail-order websites, such as site construction, order processing, customer support, product management, logistics, delivery, and payment collection.

(Taken from the reference material of the company)

① Logistics Agency Service

At the request of mail-order companies, the company receives their products and undertakes a series of logistics operations such as product management, picking, distribution processing, packing, delivery, and payment collection.

Core services

Services | Outline |

Product management | Manages storing, quality, expiration date, quantity, etc. of products entrusted by mail-order companies. By cross-checking the data in the in-house developed e-LogiT WMS with the on-site surveys, it is possible to check the difference in expiration dates and quantities. Each mail-order company is given an account for the above system to continuously share data. |

Picking | Picks up the items stored in the FC and transport them to the packing location. By utilizing QR code inspection etc., the company prevents shipment errors in the work process, and improves inspection accuracy to pick up products in a timely and appropriate manner. |

Packing | Packs the products divided by delivery unit using packing materials such as cardboard. |

Delivery | Delivers packaged goods to buyers through couriers. |

Optional services

Services | Outline |

Distribution processing | Enhances the added value of products such as repackaging into smaller sizes, packaging of customized products*, and assembling of semi-finished products. |

Fee collection | Undertakes the COD payment (fee collected at the point of delivery of goods by couriers) on behalf of the mail-order company. The company signs contracts with couriers to provide this service to mail-order companies. |

*Customized products

Products that follow the unique packing instructions (message cards, campaign goods, appendix bundles, etc.) from mail-order companies, instead of being simply packaged and shipped.

② Operation Agency Service

At the request of mail-order companies, the company undertakes product photography, product data uploading, order processing, customer support, etc.

Optional services

Services | Outline |

Product photography | Takes photos and process images of products for mail-order sites. |

Uploading product data | Uploads the images and product information to mail-order sites. |

Order processing | Undertakes necessary processes for delivery, such as shipping instructions for orders from mail-order sites. |

Customer support | Responds to inquiries from purchasers, prospective buyers, etc. via email and phone calls. |

③ Logistics Consulting Service

By utilizing the knowledge accumulated through the experiences of the mail-order distribution business, the company offers year-long training programs for a flat rate, online training courses at the e-LogiT club, distribution insight and improvement seminars, and consulting for the mail-order distribution companies to improve the distribution forefront.

(2) Operation of FCs

As of June 2021, the company operates the following seven FCs as its bases for logistics agency service.

FC name | Area (tsubo) | Completion year and month |

Tokyo FC (Edogawa-ku, Tokyo) | 2,600 | October 2010 |

Saitama FC (Yashio City, Saitama) | 8,900 | October 2014 |

Misato FC (Misato City, Saitama) | 6,800 | November 2017 |

Osaka FC (Osaka City, Osaka) | 6,400 | April 2019 |

Adachi FC (Adachi-ku, Tokyo) | 8,400 | April 2019 |

Narashino FC (Narashino City, Chiba) | 4,700 | January 2021 |

Saitama Soka FC (Soka City, Saitama) | 7,400 | June 2021 |

The second Osaka FC is scheduled to open in the term ending March 2023.

In opening a new FC, upfront investments for rental fees and material purchases will occur, but sales will increase year by year with the operation of new customers, and operating income will usually turn positive from the third year after opening to contribute to earnings.

In addition, the negative impact of upfront investments on profits will be mitigated as the ratio of new FCs to existing FCs decreases.

【1-5 Characteristics and Strengths】

The company entrusted with outsourcing logistics operations boasts the following strengths and advantages.

(1) Domination with large distribution centers

When opening a FC, the company aims for a floor area of about 5,000 tsubo (1 tsubo = approximately 3.3 square meters). This is much larger than those of other companies’ mail-order distribution centers, which tends to be in the 1,000-2,000 tsubo range.

In the Kanto area, the company is going forward with its dominant strategy by keeping the FCs within 20 km of each other when opening a new one.

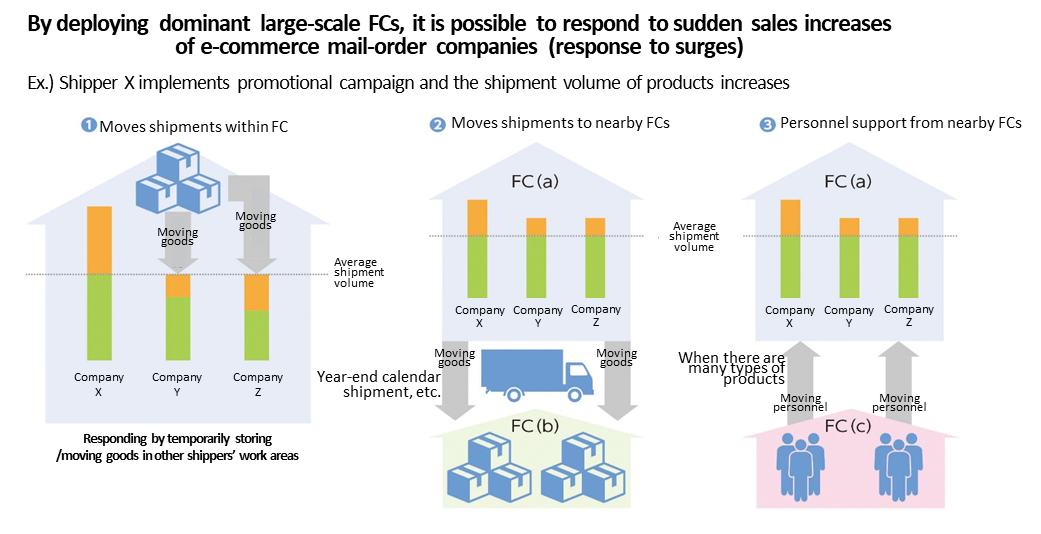

Dominant Strategy: the source of the company’s largest competitive advantage, the capability to respond to surges

Through the domination with large-scale FCs, it is possible to respond to the sudden surge in sales of e-commerce mail-order companies.

The company terms this as the “response to surges.”

For example, if the shipper X conducts promotional campaigns and product shipment volume increases rapidly, the company will mostly respond in the following three ways:

① Moves shipments within FC

Temporarily moves and stores shipper X’s goods to other shipper’s work area with enough room within the same FC.

② Moves shipments to nearby FCs

If there are no room in other shippers’ work areas, move the shipper X’s goods to the nearby FC and continue working there.

A typical response to cases such as the year-end calendar shipments.

③ Personnel support from nearby FCs

When dealing with many types of products at once, it may not be efficient to move the products, so staff from nearby FCs would be called in to support them.

Since increase in shipment volume can manifest itself in many different ways, the company will take appropriate measures according to the situation each time, but response ① is able because of their large scale FC, and responses ② and ③ are able because of their domination which keeps the distances between FCs at 20 km or less.

While securing sales by shipping goods as requested by shippers, the company also achieves reductions in delivery costs and shortens lead times, and this “response to surges” is the company’s biggest competitive advantage and the company plans to further brush up this asset in the future.

(Taken from the reference material of the company)

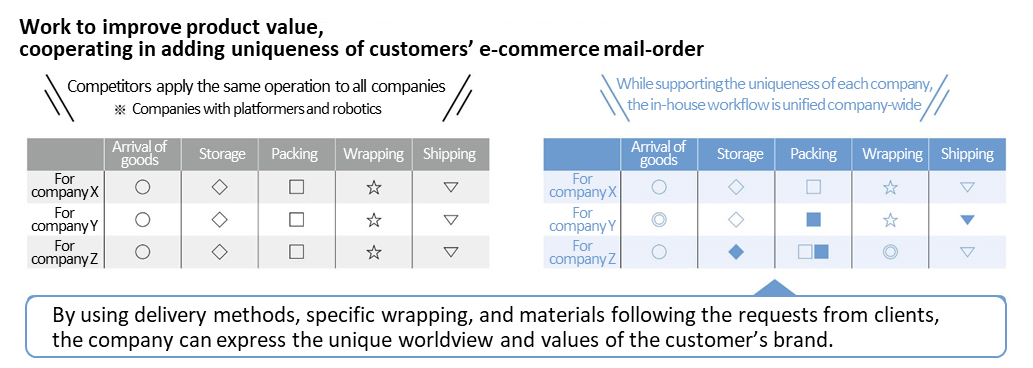

(2) Mass-customization

In each step of logistics — arrival of goods, storage, packing, wrapping, and shipping — other companies in the same industry, especially major operators that use platformers and robotics for efficiency improvement, tend to apply the same operation to all shippers.

In contrast, the company is supporting the uniqueness of each shipper, while the underlying workflow is unified company-wide.

This enables the company to help express the unique worldview and values of the clients’ brands by using delivery methods, specific wrapping, and materials according to the shipper’s request. Since the workflow is unified company-wide, efficiency is maintained.

This is the unique initiative of the company aiming to be No.1 in “creating heart moving experiences” as seen in its Mission.

(Taken from the reference material of the company)

(3) IT × Logistics

The company has developed its own WMS (Warehouse Management System) software that manages product information in the warehouse such as the storage location, expiration date, arrival and shipment of goods, and quantity.

By linking with the mail-order cart systems, that is aligned with the specifications of the mail-order sites of multiple e-commerce mail-order companies (shippers), the complicated inventory management is performed by the system.

In addition, since it is manufactured in-house by the company’s system department, it can be flexibly linked with the system environment of the e-commerce mail-order companies, and a smooth start-up is possible. The company is also active in introducing new services, and is rigorously pursuing improvements in logistics services as well as quality services by utilizing IT.

(4) Specializing in mail-order logistics to hone knowledge

In the 21 years since its establishment, the company gradually developed its services centered on mail-order logistics agency service, learnt how to deal with the high-mix low-volume logistics, which is considered difficult, and has been accumulating experiences and knowledge with diverse items such as car supplies, apparel, supplements, cosmetics, and wine. In addition, the company has honed its knowledge through on-site practice and logistics consulting.

The accumulation of such trust, credibility, and knowledge are highly valued, and the customer base continues to widen as the existing customers brings in many new customers.

Its accumulated knowledge and strong customer base should be evaluated as the company’s invisible assets.

(5) Emphasis on the front line

At every FC, all staff members are always aware of quality and improvement.

The company realizes and maintains high quality by thoroughly sticking with accomplishing each normal task perfectly. When a problem such as a shipment error occurs, the company thoroughly investigates the cause, makes improvements, and makes sure to share the findings with all staff members.

In addition, the company actively takes up the improvement proposals from on-site staff involved in various processes, and the number of improvement proposals exceeds 7,200 annually.

The company also trains and educates logistics personnel who offer their services both inside and outside the company. It also hosts courses to help its employees to pass the business and career certification exams sponsored by the Ministry of Health, Labor and Welfare, and for this reason, many of its employees hold these qualifications.

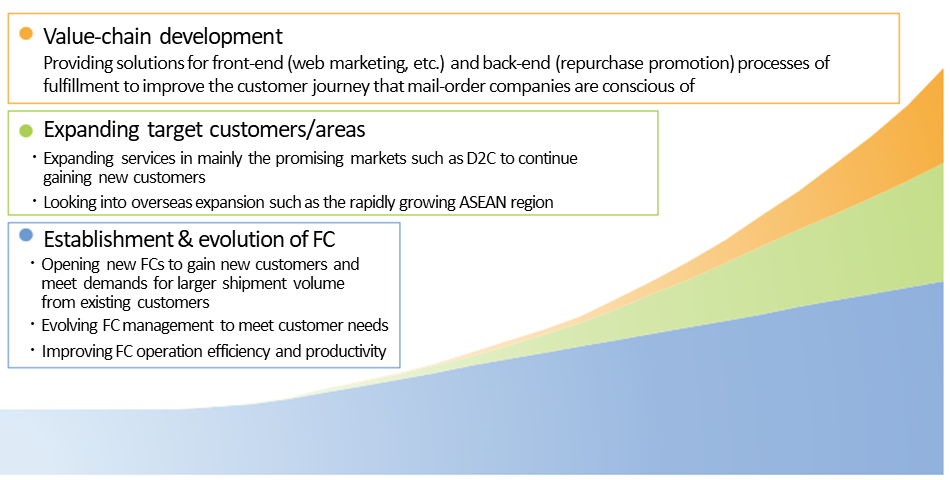

【1-6 Growth Strategy】

The company aims to increase sales and profits by strengthening the three pillars below for meeting customer needs.

(1) Value-chain development

The value-chain covers the front-end (web marketing, etc.) and the back-end (repurchase promotion) processes of fulfillment, and improves the customer journey* that the mail-order companies are conscious of, which in turn offers solutions that lead prospective customers to their actual customers.

*Customer journey

A series of experiences that a customer follows — from the encounter with a product or service to actually purchasing/using it with the intention to purchase/use it — is perceived as a “journey.”

For a mail-order company to turn prospective customers into actual customers and fans of its products, it is necessary to manage the customer experience throughout the “journey” that the customer follows. To manage the customer experience efficiently and to take appropriate marketing measures, it is necessary to create a customer journey map that visualizes and captures its pathway.

(2) Expanding target customers/areas

The company will expand services in the promising markets such as D2C to continue increasing new customers.

It is also considering overseas expansion such as the rapidly growing ASEAN region.

(3) Establishment & evolution of FC

To gain new customers as well as coping with the increase in the existing customers’ shipment volume, the company will continue to open new FCs.

It also intends to keep improving the FC management to meet customer needs and aims to improve the efficiency and productivity of FC operation.

(Taken from the reference material of the company)

In addition to the conventional mail-order logistics and e-commerce, the company intends to make the omnichannel market including actual stores its business domain, and is working to secure management resources for that purpose.

【1-7 Shareholder Return】

The company recognizes that shareholder return is an important management issue. However, being currently in the process of growth and in need of making upfront investments such as leasing new FCs and purchasing equipment to expand its business scale, it also recognizes the necessity to keep enhancing its internal reserve.

Therefore, the company will take into consideration of the economic trends, business results, financial conditions, etc. comprehensively, and aims to continue with its shareholder return policy to pay stable dividends with a dividend payout ratio of 30%.

2. Fiscal Year ended March 2021 Earnings Results

(1) Overview of business results (Non-consolidated)

| FY 3/20 | Ratio to sales | FY 3/21 | Ratio to sales | YoY | Compared to forecasts |

Sales | 8,385 | 100.0% | 10,696 | 100.0% | +27.6% | +65 |

Gross profit | 530 | 6.3% | 838 | 7.8% | +58.0% | +33 |

SG&A | 446 | 5.3% | 600 | 5.6% | +34.6% | +6 |

Operating Income | 84 | 1.0% | 238 | 2.2% | +180.8% | +26 |

Ordinary Income | 102 | 1.2% | 241 | 2.3% | +134.8% | +24 |

Net Income | 76 | 0.9% | 151 | 1.4% | +98.0% | +19 |

* Unit: million-yen

Significant increase in sales and profit. Sales hit a record high.

Sales increased 27.6% year on year to 10,696 million yen. In addition to acquiring new customers, the shipment volume of existing customers expanded.

Gross profit increased 58.0% year on year, and gross profit margin rose 1.5 points. Operating income grew 180.8% year on year to 238 million yen, absorbing the cost rise including upfront investment, such as an increase in packing freight charges due to the rise in shipment volume and the increases in labor and outsourcing costs for product movement due to the opening of the new FC. The company achieved significant growth in profits as planned.

The dividend was set at 3.00 yen/share, an increase of 1.00 yen/share from the previous term. The payout ratio is 5.6%.

(2) Financial position and cash flows

Main Balance Sheet

| End of Mar. 2020 | End of Mar. 2021 | Increase/ decrease |

| End of Mar. 2020 | End of Mar. 2021 | Increase/ decrease |

Current Assets | 1,874 | 3,459 | +1,584 | Current Liabilities | 1,624 | 2,314 | +690 |

Cash and Deposits | 877 | 2,249 | +1,372 | Trade Payables | 505 | 726 | +221 |

Trade Receivables | 755 | 981 | +226 | ST Interest-Bearing Debts | 100 | 93 | -7 |

Prepaid Expenses | 182 | 207 | +24 | Other Payables | 825 | 1,073 | +247 |

Noncurrent Assets | 1,404 | 1,557 | +152 | Noncurrent Liabilities | 569 | 645 | +75 |

Tangible Assets | 534 | 470 | -63 | LT Interest-Bearing Debts | 467 | 471 | +3 |

Facilities Attached to Buildings | 307 | 288 | -18 | Total Liabilities | 2,193 | 2,959 | +765 |

Investment, Other Assets | 851 | 1,074 | +223 | Net Assets | 1,085 | 2,057 | +971 |

Total Assets | 3,279 | 5,016 | +1,737 | Total Liabilities and Net Assets | 3,279 | 5,016 | +1,737 |

* Unit: million-yen.

Total assets rose 1,737 million yen from the end of the previous term to 5,016 million yen due to an increase in cash and deposits caused by a public offering accompanying the listing of shares.

Total liabilities increased 765 million yen from the end of the previous term to 2,959 million yen due to the increases in trade payables and other payables because of sales growth.

Net assets increased 971 million yen from the end of the previous term to 2,057 million yen because of the rises in capital and capital surplus due to the public offering.

Equity ratio increased 7.9 points from the end of the previous term to 41.0%.

Cash Flow

| FY 3/20 | FY 3/21 | Increase/decrease |

Operating CF | 242 | 830 | +588 |

Investing CF | -265 | -265 | +0 |

Free CF | -23 | 565 | +588 |

Financing CF | 35 | 806 | +771 |

Cash and equivalents | 877 | 2,249 | +1,372 |

* Unit: million-yen.

The rise in pre-tax net income increased the surplus of operating CF, and free CF turned positive.

The income from the issuance of shares at the time of the initial public offering expanded the surplus of financing CF.

The cash position has risen.

3. Fiscal Year ending March 2022 Earnings Forecasts

【3-1 Earnings Forecasts】

| FY 3/21 | Ratio to sales | FY 3/22 Est. | Ratio to sales | YoY |

Sales | 10,696 | 100.0% | 13,575 | 100.0% | +26.9% |

Operating Income | 238 | 2.2% | 323 | 2.4% | +35.6% |

Ordinary Income | 241 | 2.3% | 325 | 2.4% | +34.9% |

Net Income | 151 | 1.4% | 197 | 1.5% | +30.4% |

* Unit: million-yen. Estimates calculated by the company.

| FY 3/21 1H | 2H | FY 3/22 1H Est. | YoY | 2H Est. | YoY |

Sales | 5,302 | 5,394 | 6,311 | +19.0% | 7,264 | +34.6% |

Operating Income | 192 | 46 | -19 | - | 342 | +637.3% |

* Unit: million-yen. Estimates calculated by the company.

Sales and profit expected to grow significantly.

Sales are expected to increase 26.9% year on year to 13,575 million yen.

The company will concentrate resources and strengthen sales capabilities to achieve high top-line growth. The number of partner companies will rise due to the acquisition of new customers, and the shipment volume of existing customers will expand.

Operating income is estimated to grow 35.6% year on year to 323 million yen.

Sales growth will make up for the upfront investment, such as the opening of Saitama Soka FC in June 2021 and the hiring of 32 new graduates.

In the first half, an operating loss of 19 million yen will be recorded due to an increase in rent and material handling costs as a result of the new opening of Saitama Soka FC, and a rise in personnel costs due to the hiring of 32 new graduates. However, operating income is projected to increase significantly to 342 million yen in the second half, seven times more than that of the same period of the previous term due to the increase in sales and new graduates playing an active role in the company.

The dividend is still to be determined.

【3-2 Main Measures】

As the B2C-EC market is expected to expand further, the company regards this term as an investment phase for sustainable growth. Thus, it will flexibly implement upfront investments such as opening new FCs and developing and hiring human resources.

The main measures are as follows.

Strengthening on-site capabilities | -Improving the management capabilities of leaders -Recruitment of new graduates centered on university graduates and formulation of educational programs |

Strengthening marketing capabilities | -Opening of new FCs: Opening Saitama Soka FC in June 2021 -Further improvement of push marketing as well as pull marketing -Further expansion of sales per tsubo of FC (Currently, monthly sales per tsubo are 23,000 yen, but based on the experience so far, there is room to increase it to 33,000 yen) |

Increasing sales from existing customers | -Further strengthening the capability to respond to surges through the dominant marketing strategy of using FCs -Improving customer satisfaction by expanding operating agency service -Fine-tuning the customer journey |

4. Interview with President Kakui

We asked President Kakui about the company’s competitive advantage, challenges, and message to investors.

Q: “First of all, could you give us a more concrete image of your company’s concept of ‘strategic logistics?’”

For example, a customer orders by mail-order and receives a product. When you receive the item you ordered, you are usually excited to open it, and you may be pleased as the item is as expected or you may be disappointed.

Even if the same product is packed with the same cardboard and the same cushioning material, the impression when receiving the package differs depending on the packaging method.

If you are pleased, you will order again and use the same mail-order for different products, but you may not order from that company anymore if you are disappointed.

In addition, part of the strategic logistics is proposing to pack the products in a way that is in line with the mail-order companies’ strategy and product concept.

For example, if you are a company focusing on SDGs, we recommend using environmentally friendly cushioning materials.

In this way, our strategic logistics is to handle the logistics by paying attention to the smallest details so that customers will want to place an order again.

Logistics is generally a cost center, so the main idea is to increase productivity and efficiency, but we believe that the role of logistics is to increase sales and the added value of products.

Q: “I think that these meticulous efforts are of course shared throughout your company, but please explain the vision and mission that will be the basis for that.”

The company vision was set by executives, and the mission and value were determined while involving employees. Therefore, my ideas and the ideas of the employees are in agreement.

Our vision is to aim to predict changes and continue to enrich people’s heart moving experiences, and the mission is to aim to be the No.1 company in creating heart moving experiences. By doing so, we think the customers who purchase the product will be impressed. This is a significant pillar of our company.

Generally speaking, a vision or a mission of a company usually describes the attitude and feelings toward clients. However, in our case, we aim to satisfy the end customers of our clients.

As I mentioned earlier, if you are pleased when the product arrives, it will result in more orders as you would want to order it again or use the same mail-order for different products. This will lead to the satisfaction of our direct clients ,that are shippers.

In addition, to create a heart moving experience, we emphasize high quality and improvement activities at FCs, which are the work sites.

When a problem such as a shipment error occurs, we investigate the cause, make improvements, and thoroughly share it with all staff.

Also, the number of improvement proposals from field staff exceeds 7,200 annually. This is because all employees and staff, including part-time workers, share the company’s vision, mission, and value as their own.

The scale of our company will continue to grow, and even in that case, we will make sure that we can share these company culture through the training of executives.

Q: “Next, please tell us about your company’s competitive advantage.”

Our greatest strength or feature is our ability to respond to surges.

Our ability to flexibly respond to sudden increases in shipment volume by shippers has been highly evaluated. Many shippers used to be partners with other companies, but they switched to our company as a result of using us as a trial. This is our great strength.

The source of this is our dominant strategy of using FCs. In the future, as we open one or two new FCs a year, the volume will increase steadily. So, we are working to improve the management capabilities of our major leaders to enhance our ability to respond to surges.

Another competitive advantage of our company is our consulting ability.

In addition to dealing with high-mix low-volume logistics, which is considered most challenging in logistics, we have built up credits and knowledge for products of various genres, and we have further deepened our knowledge through on-site practice and logistics consulting.

We have received high praise for the knowledge we have accumulated in this way, and our existing customers have introduced us to many new customers. For this reason, we have rarely conducted the so-called push marketing so far, and we have been able to acquire customers very efficiently.

Q: “What are your perceptions of the challenges and issues you must tackle in pursuing growth?”

It is the evolution of WMS, Warehouse Management System.

We will expand our business domain to handle not only mail-order and e-commerce but also the omni channel including physical stores. Thus, we will manage inventory in an integrated manner not only in FCs, but also in physical stores. Nonetheless, we must continue to offer an inspiring experience to customers who receive products and respond to the surge in demand by shippers as we did before.

For that purpose, it is necessary to develop an unprecedented WMS. Therefore, we will work on system development investment, including creativity and human resources.

In addition, to develop new customers, we believe that it is necessary to hire human resources not only in the logistics industry, but also in other industries.

By hiring people who are familiar with each industry, we can understand how to approach that industry.

In addition, FC is a distribution center and a factory that creates added value, so specialized human resources in fields such as production control and labor management are also required.

Q: “Please give a message to shareholders and investors.”

With the spread of the COVID-19, online shopping and EC demands are expanding. However, these are not something that will decrease when the COVID-19 pandemic is over. Consumer behavior has changed dramatically, with people in their 70s, who we previously thought to be unlikely to use e-commerce, are actively using it.

With this business environment as a tailwind, we would like to concentrate our management resources and expand sales and profits.

Thus, by all means, we would like you to support our challenge from a medium- to long-term perspective.

5. Conclusions

After the listing in March, the stock price has been sluggish recently. However, this is not limited to the company, but it is seen in many EC-related stocks. This must be caused by the weakening trend to buy stocks related to housebound consumers amid the pandemic, since although the future is still uncertain, vaccination is progressing.

However, it is certain that the EC market will continue to expand regardless of the demand of people staying at home due to the COVID-19 pandemic. The business environment surrounding the company will also continue to be favorable.

In addition, the opening of new FCs is a factor of cost increase in the short term. However, if the number of existing FCs increases, the negative impact of the cost increase due to the new facilities will become smaller. On the contrary, its effect of increasing sales will contribute to business performance.

A significant increase in sales and profits is also expected in the current term. However, we will continue to pay attention to whether the company can significantly increase its business performance through the competitive advantages of its dominant strategy of using large FCs and capability to respond to surges.

<Reference: Regarding Corporate Governance>

Organization Type and the Composition of Directors and Auditors

Organization type | Company with corporate auditor(s) |

Directors | 5 directors, including 2 outside ones |

Auditors | 3 auditors, including 3 outside ones |

Corporate Governance Report

Last updated on Jun. 29, 2021.

<Basic policy>

Our goal is to maximize corporate value by achieving sustainable business growth. In order to build a highly transparent corporate governance system, including rigorous compliance and appropriate information disclosure, and to fulfill corporate social responsibility, we will promptly respond to changes in the business environment and select the optimal business management system and will make efforts to improve and enhance it.

By implementing the above, we will earn the trust of all stakeholders such as shareholders, business partners, officers, and employees and build good relationships.

<Reasons for Non-compliance with the Principles of the Corporate Governance Code >

Principles | Reasons for not implementing the principles |

[Principle 4-8 Effective utilization of outside directors] | We have appointed two independent outside directors. In addition, all three auditors are independent outside officers, and five independent outside officers have been appointed in total. At the Board of Directors, we have determined that five independent outside officers are fully fulfilling their roles and responsibilities according to their attributes and that a system in which appropriate supervision of business execution is maintained. We will consider the necessity of increasing the number of independent outside directors and selecting candidates, considering changes in the environment surrounding the company. |

<Disclosure Based on the Principles of the Corporate Governance Code >

Principles | Disclosure contents |

[Principle 1-4 Strategically held shares] | At this time, we do not hold any strategically held shares. |

[Principle 5-1 Policy on constructive dialogue with shareholders] | We are committed to promoting constructive dialogue with our shareholders and investors. (i) The Corporate Planning Division of the Management Department has been designated as the IR center, and the officers in charge of the Management Department are the officers in charge of IR. (ii) The Corporate Planning Division of the Management Department collects information in cooperation with each department. (iii) In addition to the general meeting of shareholders and the financial results briefing, we will provide information through our website. (iv) We have a system in which opinions from shareholders and investors obtained through dialogue are reported to management each time. (v) IR activities will be restricted to prevent dialogue with shareholders and investors for a certain period before announcing financial results. Regarding the management of insider information, we will thoroughly manage insider information based on the Insider Trading Prevention Regulations. |

This report is intended solely for information purposes, and is not intended as a solicitation for investment. The information and opinions contained within this report are provided by our company based on data made publicly available, and the information within this report comes from sources that we judge to be reliable. However, we cannot wholly guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness, or validity of said information and opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration. Copyright(C) Investment Bridge Co.,Ltd. All Rights Reserved. |

You can see back numbers of Bridge Reports on e-LogiT Co., Ltd. (9327) and IR related seminars of Bridge Salon, etc. at www.bridge-salon.jp/.