Bridge Report:(7685)BuySell Technologies the second quarter of fiscal December 2023

![]()

President and CEO Kyohei Iwata | BuySell Technologies Co., Ltd (7685) |

|

Company Information

Market | TSE Growth Market |

Industry | Wholesale (trade) |

President and CEO | Kyohei Iwata |

HQ address | PALT Building, 28-8, Yotsuya 4-Chome, Shinjuku-ku, Tokyo |

Year-end | End of December |

Homepage |

Stock Information

Share Price | Shares Outstanding | Total Market Cap | ROE (Act.) | Trading unit | |

¥4,265 | 14,583,111 shares | ¥62,196 million | 35.8% | 100 shares | |

DPS (Est.) | Dividend yield (Est.) | EPS (Est.) | PER (Est.) | BPS (Act.) | PBR (Act.) |

¥25.00 | 0.59% | ¥191.80 | 22.2x | ¥560.38 | 7.61x |

* The share price is the closing price as of August 29. ROE and BPS were taken from the financial results for the previous term. Number of outstanding shares, DPS and EPS were taken from the financial statements for the second quarter of FY 12/23.

Earnings Trend

Fiscal Year | Net Sales | Operating Income | Ordinary Income | Net Income | EPS | DPS |

December 2019 | 12,828 | 846 | 817 | 505 | 41.94 | 7.50 |

December 2020 | 14,764 | 968 | 922 | 565 | 41.12 | 7.50 |

December 2021 | 24,789 | 2,315 | 2,295 | 1,314 | 93.26 | 14.00 |

December 2022 | 33,724 | 3,694 | 3,672 | 2,268 | 158.28 | 20.00 |

December 2023 Est. | 44,600 | 4,550 | 4,500 | 2,800 | 191.80 | 25.00 |

* The estimated values are based on the forecasts made by the Company. On January 1, 2021, a 2-for-1 stock split was conducted. EPS and DPS were adjusted retroactively.

This Bridge Report presents BuySell Technologies’ financial results for the second quarter of fiscal year ending December 2023 and so on.

Table of Contents

Key Points

1. Corporate Overview

2. The second quarter of Fiscal Year Ending December 2023 Earnings Results

3. Fiscal Year Ending December 2023 Earnings Forecasts

4. Conclusions

<Reference1: Medium-term Management Plan for 2024(announced in Feb. 2022)>

<Reference2: Regarding Corporate Governance>

Key Points

- In the cumulative second quarter of the term ending Dec. 2023, sales were 19,561 million yen, up 29.6% year on year, and ordinary income was 1,291 million yen, down 16.8% year on year. The impact of the inclusion of Four Nine in the scope of consolidation was also significant, and adjusted EBITDA increased to 1,887 million yen. Although sales were steady, ordinary income appears to have fallen short of the initial forecast (undisclosed) by approximately 200 million yen.

- Due to the serial robberies that occurred in January 2023, the number of inquiries regarding the at-home pickup was small in the first quarter. In order to make up for the delays in the second quarter, the company conducted additional advertising. Although the number of inquiries in the second quarter was at the internal plan level, it was not enough to make up for the shortfall in the first quarter. Since there is a certain lead time between receiving inquiries and actually conducting at-home visits, this impact is expected to continue until the third quarter.

- However, in the second half, the company plans to implement new measures, such as improving the media for attracting customers and priority marketing areas and balancing CPA and inquiry acquisition using performance-based media. Since mid-August, the company has been running a promotion with "Chibi Maruko-chan" as its new mascot. The company aims to recover the at-home pickup service through these efforts. In the first half, gross profit per at-home visit exceeded the forecast, so if the marketing measures work properly, it is quite possible to achieve the company's full-year forecast. With the exception of the inquiries about the at-home pickup service, all businesses, such as in-store ones of subsidiaries, are performing well, which should also be a tailwind for overall results.

- In the company’s forecast for the term ending Dec. 2023, sales are projected to increase 32.2% year on year to 44,600 million yen, gross profit to rise 29.6% year on year to 25,750 million yen, operating income to grow 23.2% year on year to 4,550 million yen, and adjusted EBITDA to increase 30.2% year on year to 5,650 million yen. The projected dividend per share is 25.00 yen (payout rati 13.0%). The company will continue to strengthen hiring and invest in technologies for future growth. Despite the increased amortization/depreciation of goodwill and customer-related assets associated with the acquisition of FOUR-NINE, an increase in the number of at-home visits and variable profit per at-home visit, as well as an increase in gross profit margin due to the store network expansion in the Storefront Business, will support solid profit growth. The quarterly progress is expected to be more significant in the second half of the fiscal year. This is because the company intends to have a longer inventory turnover period in the first half of the fiscal year compared to previous years, in accordance with the company’s policy to re-accelerate its toC sales strategy to improve profitability from the beginning of the term ending Dec. 2023, which is caused by the impact of the shortening of the inventory turnover period by strategic toB sales in the second half of the previous fiscal year in response to market fluctuation.

- From the term ending Dec. 2023 onward, growth in the Storefront Business, in addition to the At-Home Pick up Purchase Business, will drive overall performance. The company plans to increase the number of stores, the core of its Storefront Business, from 10 BuySell stores at the end of December 2022 to 20 by the end of December 2023, then to 35 by the end of December 2024, from 19 to 25 to 35 for Timeless, and from 207 to 266 to 330 for FOUR-NINE (directly managed stores + franchised stores). Data-driven management will support this growth, and the development and installation of the “Cosmos” Reuse Platform are progressing steadily as the organization is expanding in the technology area through active hiring of engineers. In the short term, there are some concerns about the company's current marketing measures, but from a medium/long-term perspective, we consider these efforts, which are aimed at achieving growth, to be progressing smoothly.

1. Corporate Overview

BuySell Technologies operates reuse business that leverages the strengths of the "Internet" and "Real world".

The Company attracts sellers through a marketing strategy that makes full use of the Internet and mass media, and also provides the at-home pick up service throughout Japan. Its characteristics or strengths include the maximization of synergy with a variety of purchase and sales channels, the robust customer base centered around seniors, and the high-quality management. The Company is aiming for further growth by developing a huge potential reuse market and creating new businesses utilizing its customer base.

[1-1 History]

President Iwata, who was in charge of marketing at a major advertising company, questioned the situation where large and famous companies with abundant advertising expenses are favored to the disadvantage of small and medium-sized companies and start-ups with a small budget. He retired from the major advertising company and established a consulting company for his desire to help companies, including ones with weak capital, develop true marketing. He met BuySell Technologies (formerly Ace Co., Ltd.) while supporting many start-ups and small businesses.

The Company had long been providing the at-home pick up service, which is its current core business, but when President Iwata's consulting engagement started in May 2016, its marketing depended almost entirely on flyers. The homepage was not sophisticated, and the business performance was not good. The Company, which undertook a full-fledged reform under President Iwata, began to see the results when it registered a record number of applications in August of the same year, renewing the record in September.

In this process, President Iwata felt that while "the at-home pick up service" has a high added value and there are many customers who need it, the way in which the benefits of the service are communicated, the brand is constructed, marketing actions are taken, and others were extremely inadequate. He was convinced that with his marketing know-how, the Company could transform itself into a more attractive company.

In October of the same year, President Iwata assumed the role of Chief Sales and Marketing Officer (CSMO). In November, the Company name was changed to BuySell Technologies, and a new TV commercial was put on air and the reform sped up. He assumed the post of president in September 2017. The business expanded steadily thanks to the success of conducting the PDCA cycle of creative activities and the purchase of TV commercials utilizing his expertise. The Company also established a compliance system and was listed on the Tokyo Stock Exchange Mothers in December 2019.

In April 2022, the company got listed on the Growth Market of TSE through the stock market restructuring.

[1-2 Corporate Philosophy and Management Philosophy]

The Company upholds the following missions and values.

Mission:Our Mission | Beyond people, beyond time, we aim to become a bridge connecting important things. |

Value :What We Aim to Be | 1. Hospitality We listen to others and provide them with joy and delight that exceeds their expectations. 2. Professional Maximize your performance by leveraging your professional knowledge and skills. 3. Creative Without being bound by existing concepts, we discover challenges ourselves and create new value. |

The Company believes that things have value that goes beyond their physical existence, and that properly connecting them is its mission and social existence value. In addition, the company is strongly aware of the need to address environmental issues and co-create with all stakeholders, and considers its group mission to be "contributing to the creation of a recycling-oriented society through the revitalization of the secondary distribution market to realize a sustainable society" and "pursuing sustainable growth and maximizing corporate value as a company that co-creates value with various stakeholders including customers, shareholders, employees and society.

Furthermore, the company intends to reflect the value in its human resources evaluation system and link them to the development of next-generation human resources.

[1-3 Market Environment]

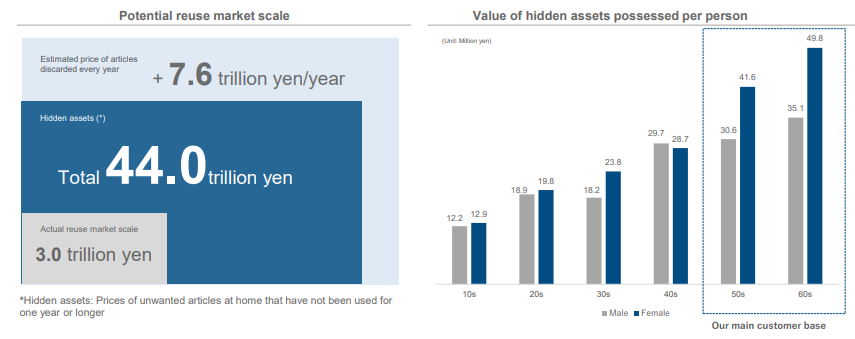

The scale of the reuse market is estimated to be about 3.0 trillion yen in 2022 and is expected to grow to 3.5 trillion yen by 2025.

However, this is only a figure for the actual reuse market, and the total potential size of the reuse market, including "hidden assets," which are unused items in houses that have not been used for more than one year, is estimated to be approximately 44 trillion yen. In addition, in Japan, where the population continues to shrink, disused articles are estimated to increase by 7.6 trillion yen each year, and the potential reuse market is expected to continue expanding. In terms of hidden asset holdings per capita in each age group, seniors in their 50s and older hold a significant portion.

(Source: the reference material of the Company)

The company intends to cultivate the reuse market, which has great potential for growth, by focusing on on-site purchase, which is one of the company's strengths, and by uncovering potential "hidden assets" in the home.

[1-4 Business Description]

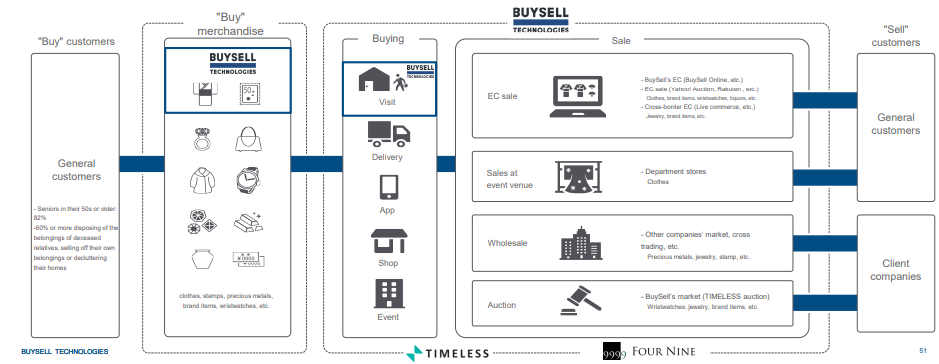

(1) Business Model

The company and its 4 subsidiary, TIMELESS, BuySell Link Inc., and FOUR-NINE, Inc. operate the reuse business by utilizing respective strengths in the Internet and in real transactions. (BuySell Link Inc. is a special subsidiary for the purpose of promoting the employment of people with disabilities.) It attracts sellers through a marketing strategy that makes full use of the internet and mass media, and also provides a shipping purchase service and a store purchase service as well as the at-home pick up service delivered by its assessors who can travel throughout Japan.The Company sells purchased products to general customers (toC sales) though EC sales at EC malls such as the Company's own EC site “BuySell Online and BuySell brandchée” and Yahoo! Auctions, and at cross-border EC sites such as eBay, and special event sales at department stores. In addition, it sells to external vendors through the “Timeless Auction", which is held by TIMELESS Corporation, which was acquired as a subsidiary, and wholesale using other companies' markets.

(Source: the reference material of the Company)

The Company has built a system to consistently manage and execute the entire flow from marketing to attracting customers, purchase appraisal, inventory management, and sales on its own. At the same time as expanding its mainstay reuse business, the Company is also focusing on launching and developing new business adjacent to the reuse business and other services utilizing customer data.

(2) Overview of Each Service

The Company's reuse business consists of the following business flo "Attracting sellers" → "Conducting purchase" → "Selling purchased products". The outline and features of each step of "customer attraction", "purchase" and "sales" are described in detail below.

(Source: the reference material of the Company)

1) Attracting Customers: Developing cross-media marketing aimed at high-net-worth seniors

◎Marketing

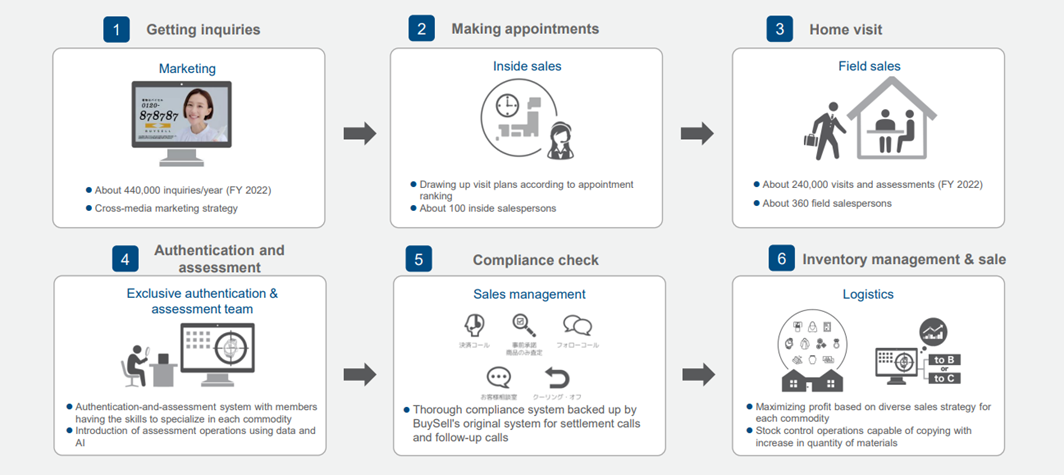

Marketing activities for receiving appraisal requests from customers are the starting point of the business strategy and execution, and maximizing the number of customers is the first key to the success of the Company's business. The marketing skills and expertise of the management team, including President Iwata, play a major role.

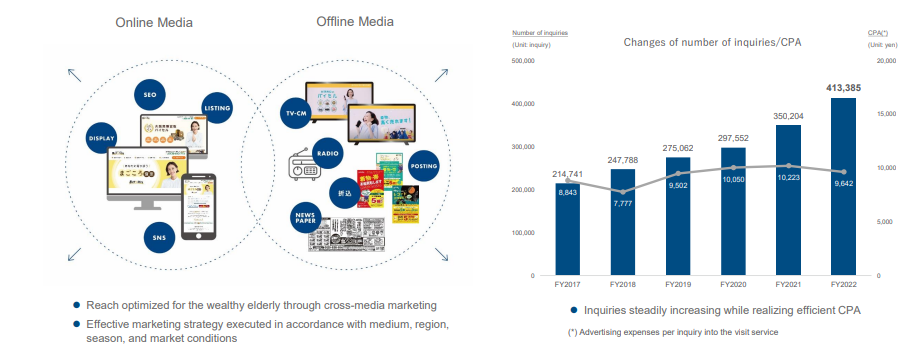

The Company develops cross-media marketing that leverages "the Internet", such as SEO (Search Engine Optimization), listing ads, and SNS, as well as "the mass media" centered on TV commercials, foldouts, flyers, etc..

In addition to advertising operation from a macro perspective based on market conditions and seasonality, the company conducts detailed analysis for each kind of daily media, area, etc., to realize efficient CPA (cost per action) and maximize cost-effectiveness in its marketing activities.

Due to such detailed marketing activities, the number of inquiries and customers are increasing year by year.

(Source: the reference material of the Company)

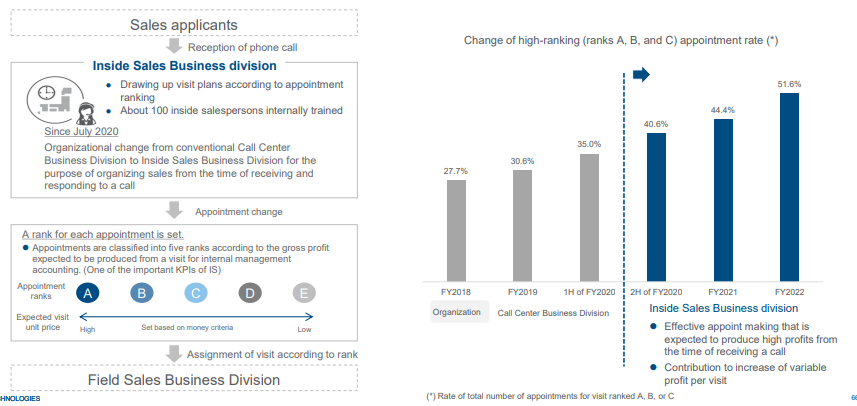

◎Inside Sales: Providing services that meet customer needs and maximizing the efficiency of assessor operations In response to incoming calls from potential buyers, the company approached through marketing, approximately 100 operators listen directly to customers’ requests and cooperate with assessors to provide services in line with customer needs.

In July 2020, the organization was changed from the previous "Call Center Business Division" to the "Inside Sales Division" for the purpose of organizing sales from the time of answering the first inquiry call.

Moreover, the call center not only performs administrative tasks such as receiving inquiries about products to be sold and arranging the date and time of visits, but also provides the customer with an explanation that will be given when they are visited by an assessor, as well as an overview of the Company's services, information regarding the range of products that can be assessed, and a guidance for preventing uninvited solicitations so that customers can use the Company's services with greater confidence.

In addition, the Inside Sales Division, along with these customer-oriented services, generates highly profitable and effective appointments by classifying them into five ranks based on the expected gross profit per business visit (expected cost per visit) when the call is received.

This organizational change has resulted in a steady increase in the ratio of highly ranked appointments over the years, contributing to an increase in variable profit per at-home visit.

The company receives 410,000 calls (The Fiscal Year Ended December 2022 Results) for asking about purchase per year, and records all of them, to trace the subsequent appointments and home visits. With this, they extract common items and essential points from highly ranked appointments, and educate operators about them. By repeating this cycle, they increase gross profit from home visits.

(Source: the reference material of the Company)

2) Purchase: Developing the "at-home pick up service" meeting a wide range of customer needs

◎The At-home Pick up Service

"The at-home pick up service" which involves going to the homes of customers who made inquiries and conducting an appraisal and a purchase, is the main purchasing method.

In addition, the Company also carries out a "shipping purchase service", in which customers send products to be sold to the Company, and a "store purchase service", in which customers bring products directly to the Company.

The Field Sales Division, which is in charge of "the at-home pick up service," has approximately 360 assessors as of the end of 2022, with based in the Kanto, Kansai, Nagoya, Fukuoka, and other areas, to cover all parts of Japan.

"The at-home pick up service" can flexibly respond to purchase requests from customers who have difficulty using store purchases service or shipping purchase service and meet a wider range of customer needs, such as when there is a wide variety of products to be assessed, the quantity of appraisals is large, it is difficult to carry the products due to their weight, as well as when there are inquiries from distant customers and elderly customers.

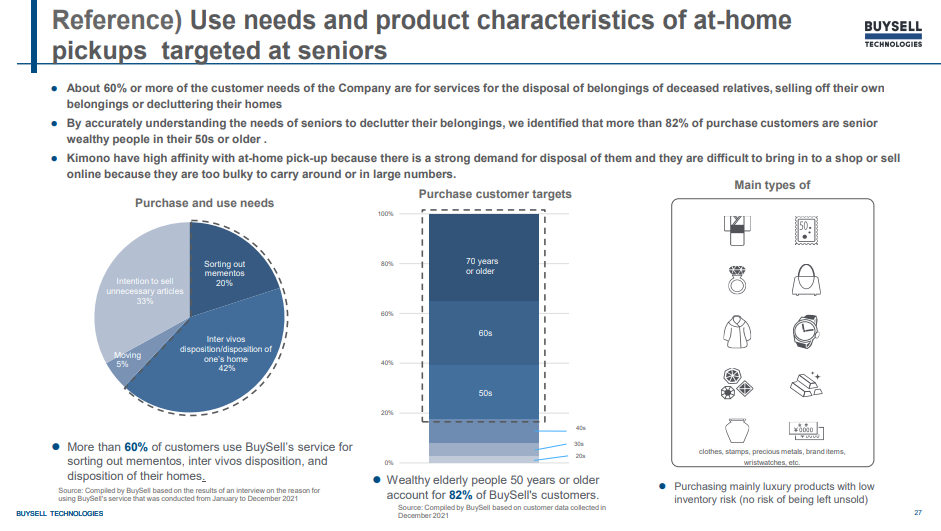

For example, if a customer wants to sell a large number of kimonos which weighs approximately 1 kg per piece, and it is difficult to carry them, "the at-home pick up service" in which the Company's assessor visits a customer's home to conduct an appraisal and a purchase, is highly compatible with such customer needs.

◎Assessor

The number of field sales assessors is also increasing steadily in parallel with the expansion of business scale, based on the company's recruiting capability. Since 2017, the company has been strengthening its recruitment of new graduates.

The company also focuses on the training of assessors to enhance customer satisfaction.

The Sales Enablement Department, a division specializing in education and training, has introduced a systematic education and training system for assessors and implements education and training programs tailored to each assessor in each center, based on the company's unique internal management index.

Considering the shortening of the training period as a KPI, they constantly review their educational programs. Several years ago, the training period was about 6 months, but currently, it is about 5 months.

The Company emphasizes the education of assessors and regularly conducts on-the-job training, including sales skills training and on-site training, to improve sales attitude, appraisal skills, and compliance awareness. In addition, the Company is working to achieve thorough compliance because the Company must provide customers with safety and security when its employees visit customers’ houses. The assessors alone cannot make a decision on the contract, and the compliance department calls the customer at the time of the contract and issues a decision call to confirm the contents of the sales contract (confirmation of the product, the price and the customer's satisfaction with the price), after which the contract is finalized.

Furthermore, the compliance department calls the customer again (follow-up call) after the assessor has left to receive the customer's candid opinions about the at-home pick up service, specifically about the assessor's attitude, compliance and customer satisfaction and so on.

The results of follow-up call, including customers’ voices, complaints and compliments are managed for each assessor, and the assessors are thoroughly informed of these to further improve their performance.

The company is also working to ensure that it complies with the cooling-off policy in accordance with laws and regulations.

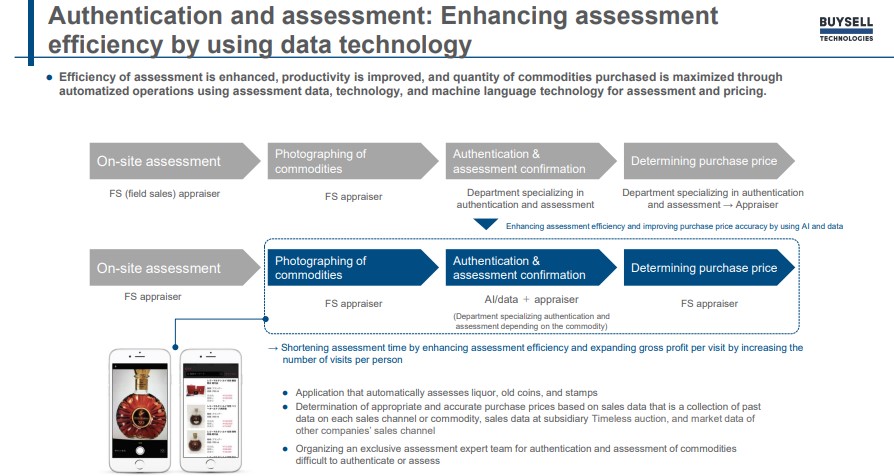

◎Authenticity Appraisal

To ensure accurate appraisal and prevention of counterfeit purchase and assessors' fraudulent appraisal, the Company's appraisal system requires not only an on-site appraisal by a visiting assessor but also a double check by another assessor who specialize in authenticity appraisal and appraisal, based on information from photos and videos sent from the visiting assessor using mobile terminals and such.

In addition, the company is using valuation data and technology to improve the efficiency and productivity of valuation and pricing decisions by automating operations using machine learning technology, etc., with the aim of maximizing the volume of purchases.

◎Products

It mainly deals with kimonos, stamps, old coins, precious metals, jewelry, brand-name items, watches, antiques, furs, alcoholic beverages and others, and focuses mainly on products with high selling prices.

(Source: the reference material of the Company)

◎Main Customers

There are many inquiries from senior wealthy people whose needs are aligned with the at-home pick up service, which is the Company's main service. In the FY ended December 2022, customers in their 50s and over accounted for approximately 82% of all customers.

In addition, senior customers use the Company's purchase services for disposition of one’s home, sorting out mementos and pre departure decluttering cleaning which account for approximately 60% of the reasons for using the services.

(Source: the reference material of the Company)

3) Sales:

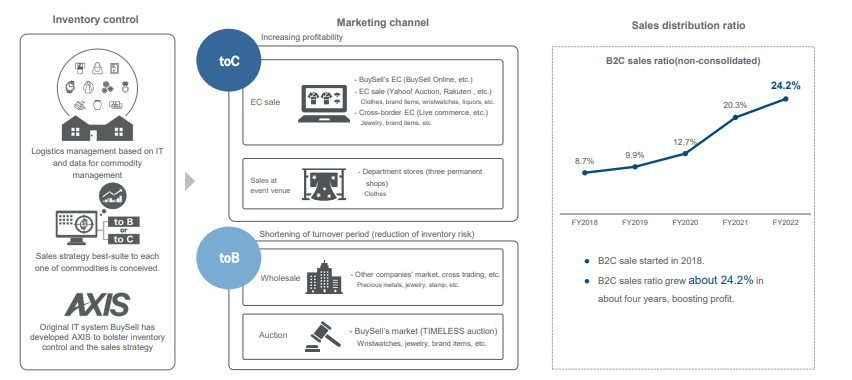

◎Inventory Management

After the cooling-off period, purchased products are managed centrally from inspection to exhibition by more than 300 staff including part-time job in the Company's own warehouse in Funabashi, Chiba Prefecture.

AXIS, an IT system developed by the Company, manages inventory for each product, and processes cooling-off requests.

The product is sent to the most suitable sales route, taking into account various aspects such as the characteristics and condition of the product as well as the market environment.

◎Sales System

After planning sales strategies based on inventory status, the Company sells purchased products through sales channels such as antique markets, auctions for dealers, e-commerce sales, special events and others.

(Source: the reference material of the Company)

For corporate sales through antique markets and auctions, the Company uses face-to-face auction formats for each product, and repeats negotiations with business partners until they find a sales partner that can produce a higher Profit Margin. In the FY ended December 2022, approximately 76% of Sales comes from corporate customers.

In addition, the company holds an auction of kimonos regularly at Narashino Warehouse, and actualizes appropriate sales at each quality level and the distribution of more goods through TIMELESS Auction, which is held by TIMELESS Corporation, which was acquired as a subsidiary.

On the other hand, in sales to end-user general consumers, in order to provide high-quality products, the Company conducts EC sales (Rakuten Market, Yahoo! Auctions and others) and sales at department store events. It operates two e-commerce sites, "BuySell Online" which was launched in July 2018 and focuses on the sales of reused kimonos, and " BUYSELL brandchée ", which was opened on February 2020 and focuses on selling luxury reuse products such as brand-name items, watches, jewelry and alcoholic beverages. The company is also running a live commerce business for the Chinese market.

The Company aims to maximize Profits by expanding sales to general consumers while shortening the inventory turnover period (reducing inventory risk) through sales to corporations. The ratio of toC sales(non-consolidated), which started in 2018, was initially about 9%, but grew to 24.2% in FY 12/22, driving profit growth.

By formulating optimal sales strategies for each product according to demand trend and building various sales channels, the Company is steadily accumulating results in sales, which is the third key to the success of the reuse business.

[1-5 Strengths and Features]

1) Maximization of synergy with a broad range of purchase and sales channels

The company is striving to maximize synergy by utilizing the strengths of the company and its subsidiary, TIMELESS, based on a wide array of purchase and sales channels of the two companies. Among many players in the reuse market, the Company has a unique business model of purchasing "luxury products" with a high unit price though a non-store-type "the at-home pick up service" which is unmatched by other competitors and constitutes a clear differentiator.

2) Strong Customer Base Centered on Senior Customers

As mentioned above, customers in their 50s and over make up approximately 82% of the Company's customer base. According to the Company's survey, 80% of the customers are satisfied with the responsiveness of the company's services, and the trust of senior high net worth individuals is strong.

This strong customer base will be a great advantage in future business development.

3) High Quality Management Team

One of the factors supporting the Company's growth is its excellent marketing strategy. According to President Iwata, no other start-up can run TV commercials as cost-effectively as the Company.

Running successful TV commercials requires familiarity with the industry structure including which players exist and what kind of setups are required, but at the Company, President Iwata who is from a major advertising company and have a great deal of knowledge, experience, and expertise, are strongly promoting a cross-marketing strategy.

In addition, in order to pursue sustainable growth by earning the trust of customers as well as to list the Company, it is essential to have a complete compliance system, and cash management in the purchase process is also an important point. Under the leadership of Mr. Koji Ono, who was appointed as Director and CFO in October 2016, the Company has been working to improve operations from an accounting perspective.

At the annual meeting of shareholders in Mar. 2021, a new director and CTO was appointed. The CTO Masayuki Imamura has the experience of engaging in a variety of digital transformation (DX) projects.

The Company runs its business with six high-quality executives, including two outside board directors, covering both offense and defense.

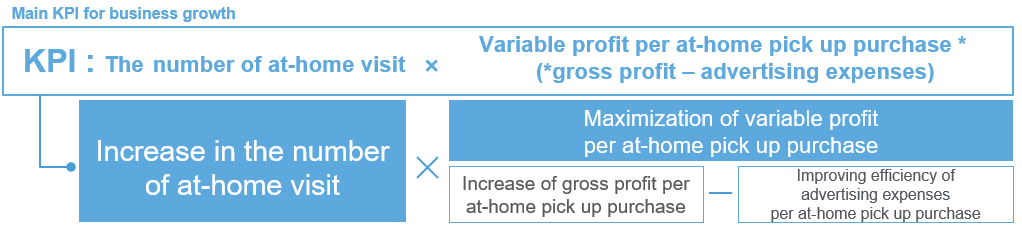

4) Main KPIs: "the number of at-home visit" x "Variable profit per at-home pick up purchase"

The Company has set "the number of at-home visit" x "Variable profit per at-home pick up purchase" as the main KPIs for the reuse business.

It pursues an increase in the number of inquiries by raising awareness in order to increase "the number of at-home visit", and seeks to maximize Variable profit per at-home pick up purchase by increasing the purchase of high-priced products and optimizing advertising expenses.

(Source: the reference material of the Company)

(Source: the reference material of the Company)

2. The second quarter of Fiscal Year Ending December 2023 Earnings Results

(1) Business Results

| 2Q of FY 12/22 (cumulative total) | Ratio to Sales | 2Q of FY 12/23 (cumulative total) | Ratio to Sales | YoY |

Net Sales | 15,092 | 100.0% | 19,561 | 100.0% | +29.6% |

Gross Profit | 8,853 | 58.7% | 11,449 | 58.5% | +29.3% |

SG&A | 7,295 | 48.3% | 10,136 | 51.8% | +38.9% |

Operating Income | 1,558 | 10.3% | 1,313 | 6.7% | -15.7% |

Adjusted EBITDA | 1,806 | 12.0% | 1,887 | 9.6% | +4.5% |

Ordinary Income | 1,552 | 10.3% | 1,291 | 6.6% | -16.8% |

| Current Net Income | 929 | 6.2% | 635 | 3.2% | -31.6% |

* Unit: million yen.

Created by Investment Bridge based on disclosed material of the company.

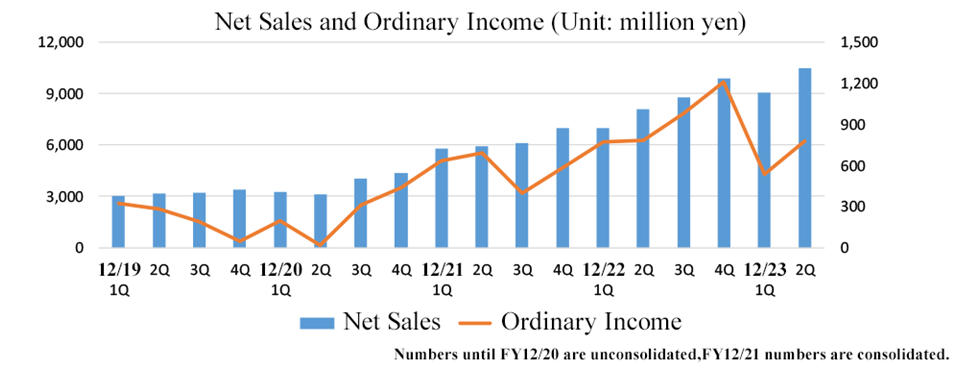

The sales in the cumulative second quarter of the term ending Dec. 2023 were 19,561 million yen, up 29.6% year on year. Regarding sales of each company, Timeless's sales increased 28% year on year, exceeding the forecast. This is because the number of visitors to department stores, which are the main locations for opening stores, has recovered as the coronavirus crisis has subsided. Thus, purchases of high-value items have been strong. The inclusion of Four Nine, which became a wholly-owned consolidated subsidiary in the term ended Dec. 2022, also contributed to the increase in sales. On the other hand, on a non-consolidated basis, the increase was only 15%. Due to the impact of the serial robberies that occurred in January 2023, the number of inquiries about at-home pickup decreased, and the number of at-home visits, which is a primary KPI, increased by only 10% year on year to 121,294. In the store business, the company opened 13 BuySell stores in the first half, making steady progress toward its full-year plan of opening 20 stores. Timeless also opened 23 stores in the first half with respect to its full-year plan of 25 stores, and Four Nine also opened 215 stores in the first half with respect to its plan of 266 stores.

Gross profit was 11,449 million yen (gross profit margin: 58.5%), up 29.3% year on year. Although there was a deterioration of the product mix due to the inclusion of Four Nine (gross profit margin in the 20% range), which also purchases products at directly managed stores, in the scope of consolidation, profit remained at the same level as in the same period of the previous year due to the success of measures to improve the gross profit per at-home visit. (It exceeded the company's forecast).

Operating income was 1,313 million yen, down 15.7% year on year. SG&A expense ratio increased 3.5 points year on year due to additional investment in promotions to improve appointment acquisition in response to a decrease of inquiries regarding at-home pickup and an increase in the number of new graduates and mid-career hires (up 364 year on year). Thus, operating income declined.

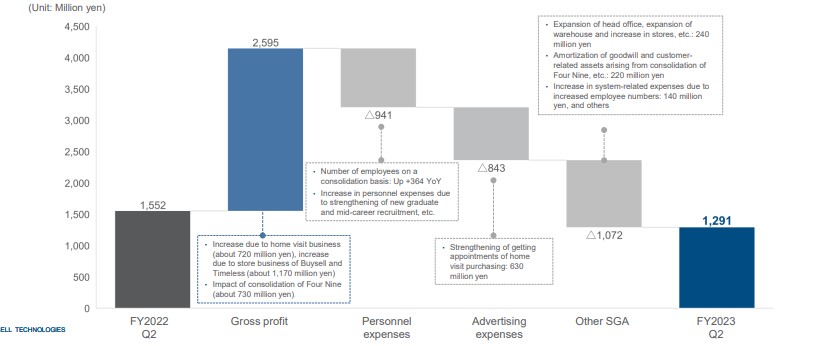

Analysis of Changes in Profit (Consolidated Ordinary Income)

(Source: the reference material of the Company)

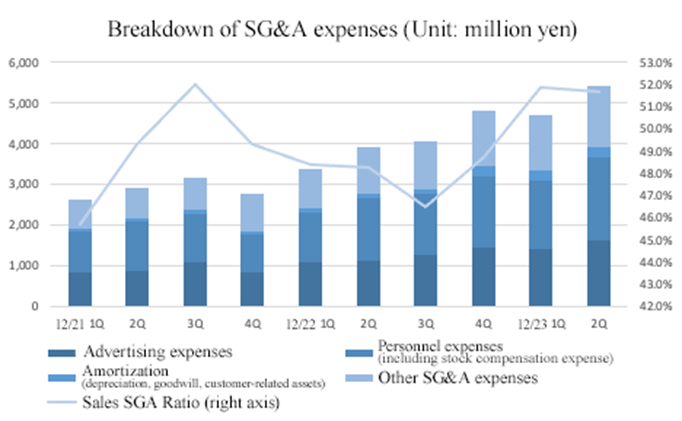

(Main SG&A expenses)

Created by Investment Bridge based on disclosed material of the company.

SG&A expense ratio remained high. This was because goodwill amortization increased from the fourth quarter of the term ended Dec. 2022 due to the inclusion of Four Nine in the scope of consolidation, the number of employees fresh out of college increased in April, and the advertising expenses augmented as the company strengthened promotions in the second quarter in response to the decrease in the number of inquiries related to the at-home pickup service.

(2) Trends in major KPIs for the at-home pickup service

| FY12/21 | FY12/22 | FY12/23 | |||||||

1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | |

Number of at-home pick up (quarterly) | 43,318 | 51,393 | 52,553 | 62,262 | 49,174 | 60,929 | 64,859 | 68,359 | 57,724 | 63,570 |

Variable profit per at-home pickup (quarterly) | 42,437 | 42,658 | 38,673 | 38,031 | 47,179 | 46,133 | 40,830 | 48,371 | 40,757 | 46,644 |

Gross profit per at-home pickup (quarterly) | 60,172 | 58,966 | 57,447 | 53,885 | 65,354 | 61,503 | 56,907 | 65,436 | 59,487 | 66,603 |

Advertising expenses per at-home pickup (quarterly) | 17,734 | 16,308 | 18,773 | 15,854 | 18,175 | 15,370 | 16,077 | 17,066 | 18,729 | 19,958 |

Although variable profit per at-home visit decreased 13.6% year on year in the first quarter (January-March), it increased 1.1% year on year in the second quarter (April-June). While the company strategically extended the inventory turnover period for the B2C products to contribute to profits in the second half, gross profit per at-home visit increased 8.3% year on year. On the other hand, advertising expenses per at-home visit increased 29.9% year on year as the company struggled to acquire inquiries regarding the at-home pickup service. As a result, the growth in variable profit remained modest. Gross profit per at-home visit has exceeded the previous year's results and the company's forecast. The company aims to improve brand recognition and marketing media by adopting a new mascot ("Chibi Maruko-chan" was adopted as the company's mascot in August 2023) to increase the number of inquiries and at-home visits in the second half of the year.

| FY12/18 | FY12/19 | FY12/20 | FY12/21 | FY12/22 | FY12/23 | ||||

1H | 2H | Full | 1H | 2H(est.) | Full(est.) | |||||

<The at-home pickup services> |

|

|

|

|

|

|

|

|

|

|

Number of Inquiries | 247,788 | 275,062 | 297,552 | 350,204 | 195,000 | 218,385 | 413,385 | 220,462 | 287,538 | 508,000 |

CPA | 7,777 | 9,502 | 10,050 | 10,223 | 9,343 | 9,909 | 9,642 | 10,654 | 14,799 | 13,000 |

Number of Employees | 215 | 240 | 271 | 314 | - | 360 | 360 | 460 | - | - |

Sales ratio of "toC" (non-consolidated) | 8.7% | 9.9% | 12.7% | 20.3% | - | - | 24.2% | 26.3% | - | - |

<Store operations> |

|

|

|

|

|

|

|

|

|

|

Number of BuySell stores | - | - | 3 | 5 | - | - | 10 | 13 | - | 20 |

Number of Timeless stores | - | - | 9 | 15 | - | - | 19 | 23 | - | 25 |

Number of Four Nine stores | - | - | 100 | 156 | - | - | 207 | 215 | - | 266 |

Of which, directly managed stores | - | - | 16 | 19 | - | - | 17 | 19 | - | 20 |

Of which, franchise stores | - | - | 84 | 137 | - | - | 190 | 196 | - | 246 |

Regarding the number of BuySell stores, KITTE Nagoya and Kichijoji stores were already opened in the third quarter. Two more stores are scheduled to be opened during the third quarter, and it is progressing smoothly. The opening of Four Nine stores has slowed down a bit, but as business talks with major franchise owners are progressing, it does not seem to impact the medium-term store opening plans.

(3) Financial Condition and Cash Flows

◎ Main BS (Consolidated)

| End of 12/22 | End of 6/23 | Increase and Decrease |

| End of 12/22 | End of 6/23 | Increase and Decrease |

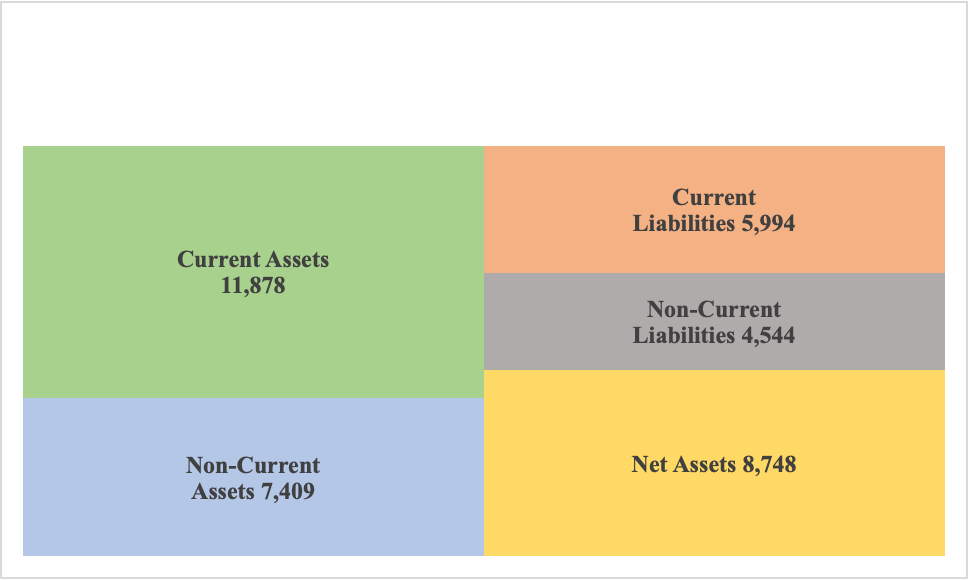

Current Assets | 10,448 | 11,878 | +1,429 | Current Liabilities | 5,690 | 5,994 | +304 |

Cash Equivalent | 6,999 | 8,232 | +1,233 | ST Interest Bearing Liabilities | 1,717 | 2,185 | +468 |

Inventories | 2,794 | 2,854 | +60 | Non-current Liabilities | 3,715 | 4,544 | +828 |

Noncurrent Assets | 7,196 | 7,409 | +213 | LT Interest Bearing Liabilities | 3,333 | 4,176 | +843 |

Tangible Assets | 717 | 873 | +155 | Liabilities | 9,406 | 10,539 | +1,133 |

Intangible Assets | 5,690 | 5,572 | -118 | Net Assets | 8,238 | 8,748 | +509 |

Investment, Others | 788 | 964 | +176 | Retained Earnings | 4,875 | 5,220 | +344 |

Assets | 17,664

| 19,287 | +1,642 | Total Liabilities and Net Assets | 17,644 | 19,287 | +1,642 |

* Unit: million yen

Created by Investment Bridge based on disclosed material of the company.

Product inventory is almost unchanged from the end of the previous fiscal year. This was due to the fact that non-consolidated inventory steadily increased in line with the company's policy to strengthen B2C sales, and purchases of Timeless, which had temporarily reduced inventory due to strong sales in the first quarter, were robust. The inventory turnover period was shortened from 66.2 days at the end of the previous fiscal year to 62.7 days. Although the inventory turnover period for non-consolidated inventory and Timeless products increased from 68.6 days in the same period of the previous year to 70 days, it was shortened due to the impact of the inclusion of Four Nine, which has a short turnover period, in the scope of consolidation. Interest-bearing debt increased as the company borrowed working capital for its strategy to increase inventory.

◎Cash Flow(Consolidated)

| 2Q of FY 12/22

| 2Q of FY 12/23

| Increase and Decrease |

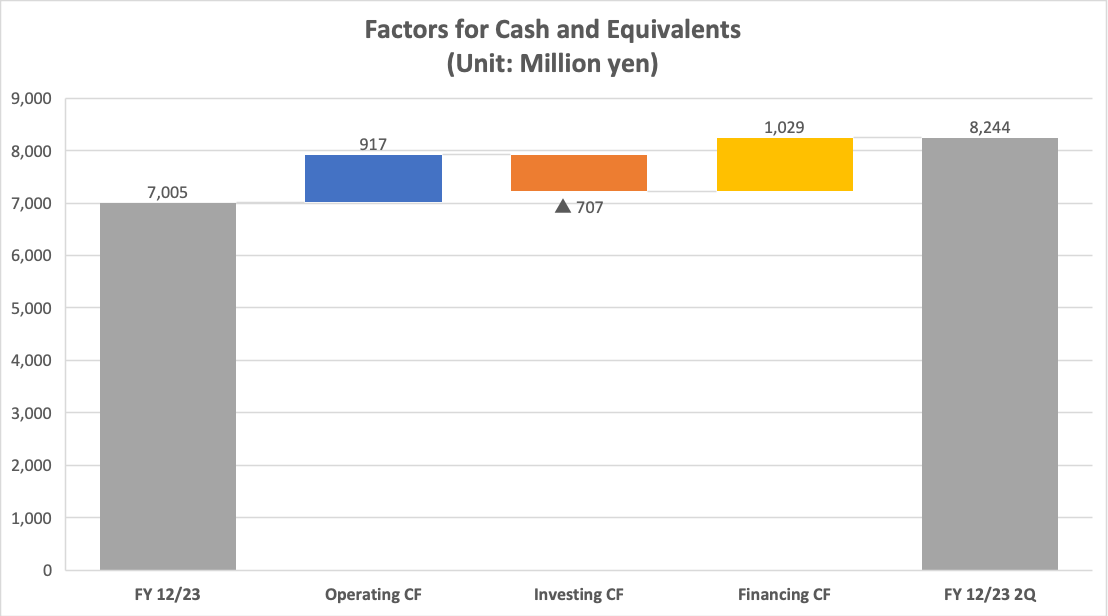

Operating cash flow(A) | 669 | 917 | +248 |

Investing cash flow(B) | -333 | -707 | -373 |

Free cash flow(A+B) | 335 | 209 | -125 |

Financing cash flow | 832 | 1,029 | +196 |

Cash and Equivalents at the end of term | 5,963 | 8,244 | +2,280 |

* Unit: million yen

Created by Investment Bridge based on disclosed material of the company.

Operating cash flow was 917 million yen due to the quarterly profit before taxes of 1,291 million yen and increased funds such as depreciation and amortization of 185 million yen and goodwill amortization of 180 million yen. There was a cash outflow of 707 million yen from investing activities. This was due to the payments for the acquisition of tangible fixed assets and deposits for the head office expansion and new store openings, which amounted to 421 million yen, and the expenditure of 289 million yen for the acquisition of intangible fixed assets for the development of in-house systems. There was a cash inflow of 1,029 million yen from financing activities, due to 2,192 million yen in income from long-term loans and 291 million yen in dividends, even though the company repaid long-term loans of 805 million yen. As a result, the balance of cash equivalents at the end of the period was 8,244 million yen.

(4) Topics

◎ Improving advertising with the new mascot

In mid-August 2023, "Chibi Maruko-chan" was appointed as the company's new mascot. In addition to its high level of national recognition, the company determined that the time setting of "Chibi Maruko-chan" is highly compatible with the products the company purchases (kimonos, records, cameras, etc.). In the second half, the company plans to attract more customers through aggressive promotions.

(Source: the reference material of the Company)

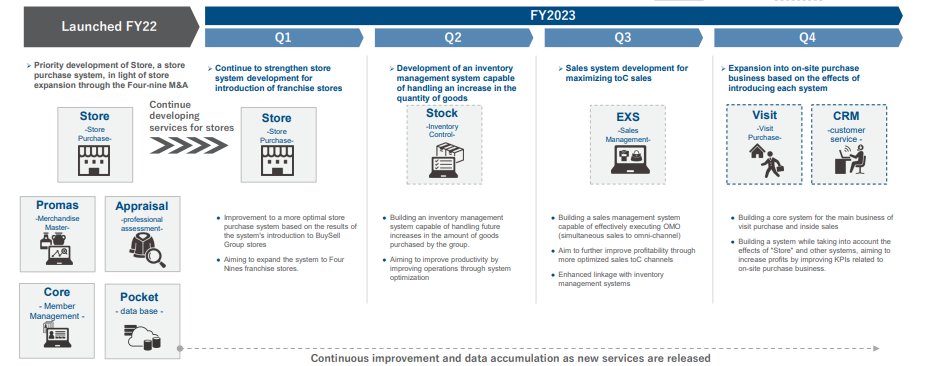

◎ Steady Progress Toward Expansion of Technology Organization

In order to not only achieve the goals of its medium-term management plan, but also sustain high growth, the company is actively working to strengthen its data-driven management through the establishment of data bases and the utilization of technology. In the term ended Dec. 2022, the number of employees in the Technology Strategy Division increased 34 from the end of the previous fiscal year to 70. The recruitment of engineering managers and personnel who can become technical leaders from major IT companies has materialized, which is noteworthy from the perspective of human capital management.

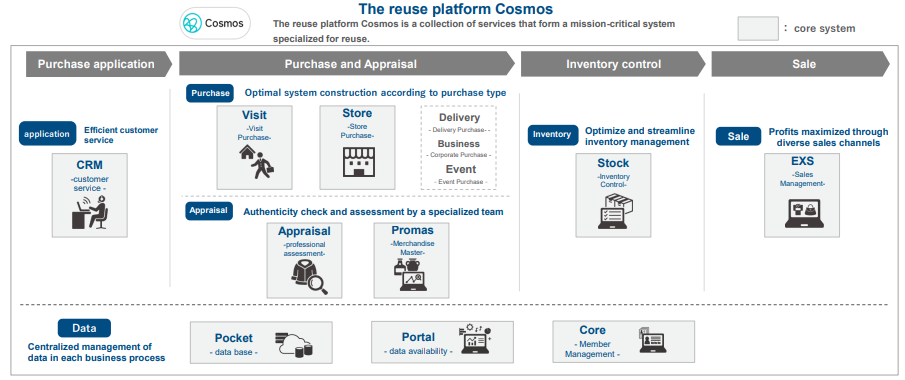

In terms of product development, the company is focusing on the development of “Cosmos,” an in-house developed platform that provides comprehensive services for everything related to the Reuse Business, including purchasing, sales, customer management, inventory management, sales management and data analysis. In the term ended Dec. 2022, in light of the M&A of FOUR-NINE, the company prioritized the development and launch of “Store,” a dedicated storefront purchase system. This launch has already materialized the following benefits: a 40% reduction in response time from the start of customer services to the signing of a contract, a reduction in the system training period for new assessors from one month to one day, and an improvement in gross profit margin by stores through faster PDCA based on various types of data.

The company plans to launch major systems one by one in the term ending Dec. 2023 as well. The future core system for the main business of the At-Home Pick up Purchase Business, “Visit,” is scheduled to be launched in the 4Q of the current term and will support growth after the end of the medium-term management plan period.

(Source: the reference material of the Company)

(Source: the reference material of the Company)

3. Fiscal Year Ending December 2023 Earnings Forecasts

(1) Business Results

◎Consolidated Financial Forecast

| FY 12/22 | Ratio to Sales | FY 12/23 Est. | Ratio to Sales | YoY |

Net Sales | 33,724 | 100.0% | 44,600 | 100.0% | +32.2% |

Gross Profit | 19,864 | 58.9% | 25,750 | 57.7% | +29.6% |

SG&A | 16,169 | 47.9% | 21,200 | 47.5% | +31.1% |

Operating Income | 3,694 | 11.0% | 4,550 | 10.2% | +23.2% |

Adjusted EBITDA | 4,339 | 12.9% | 5,650 | 12.7% | +30.2% |

Ordinary Income | 3,672 | 10.9% | 4,500 | 10.1% | +22.5% |

Net Income | 2,268 | 6.7% | 2,800 | 6.3% | +23.4% |

*Unit: million yen.

Focus on Sustainable Growth Beyond the Final Year of the Medium-Term Plan While Increasing the Probability of Achieving the Plan

Sales are expected to increase 32.2% year on year to 44,600 million yen, operating income to rise 23.2% year on year to 4,550 million yen, and adjusted EBITDA to grow to 5,650 million yen.

The company aims to achieve its initial plan by focusing on measures to recover the number of inquiries in the at-home pickup business, which was the only issue in the first half.

Despite continuing to recruit new graduates and mid-career personnel actively, the rise in ground rent due to warehouse expansion and the increase in the number of stores and the augmenting depreciation due to the inclusion of Four Nine in the scope of consolidation, the expansion of the number of BuySell, Timeless, and Four Nine stores is forecast to result in profit growth by more than 20% year on year. The acquisition of Four Nine is expected to increase sales by 6,350 million yen and operating income by 530 million yen (operating income is before the deduction of depreciation).

The dividend forecast is 25.00 yen per share, up 5.00 yen per share from the previous year. The dividend payout ratio is expected to be 13.0%.

(Main SG&A expenses)

| FY 12/18 | FY 12/19 | FY 12/20 | FY 12/21 | FY 12/22 | FY 12/23 Est. | YoY |

Advertising Expense | 1,927 | 2,613 | 2,990 | 3,905 | 4,970 | 6,000 | +20.7% |

Labor Costs | 1,745 | 2,084 | 2,349 | 3,087 | 6,014 | 8,100 | +34.7% |

* Unit: million yen. Previous FY 12/20 numbers are non-consolidated.

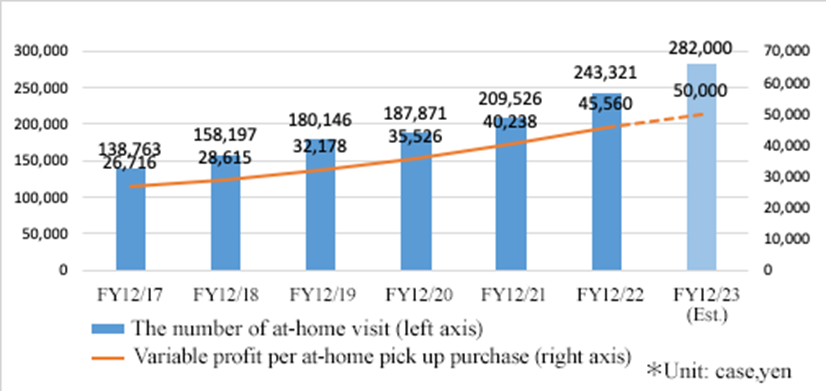

(Transition of KPIs)

| FY 12/21 | FY 12/22 | FY 12/23 Est. | YoY |

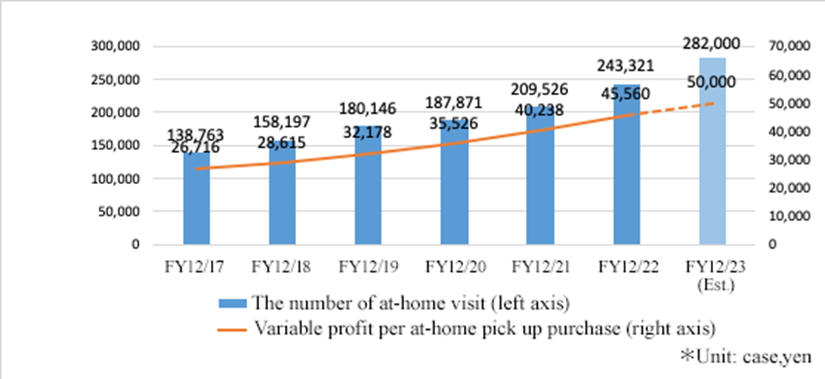

The Number of At-home Visit | 209,526 | 243,321 | 282,000 | +15.9% |

Variable Profit per At-home pick up Purchase | 40,238 | 45,560 | 50,000 | +9.7% |

* Unit: case, yen

(Source: the reference material of the Company)

4. Conclusions

If we look at the company's forecast for the term ending Dec. 2023, some may feel uneasy about the probability of achieving its medium-term management plan. In the short term, there are some concerns about the current marketing measures, but from a medium/long-term perspective, we consider these efforts, which are aimed at achieving dynamic growth, to be progressing smoothly. Given the accurate management decisions such as inventory control in the second half of the term ended Dec. 2022, subsequent inventory accumulation, fine-tuning of marketing measures in light of the external environment in the current first half, and progress in various KPIs, the probability of achieving the medium-term management plan has increased. Not only that, but the expected long-term growth rate has not decreased in any way. In order to secure this expected growth rate, the company should smoothly progress the expansion of human capital centered on engineers, the development of in-house development platforms, and launch of new services, including external sales.

<Reference1: Medium-term Management Plan 2024(announced in Feb. 2022)>

The company announced a three-year medium-term management plan for 2024 as follows.

(1) Ideal state

The following four are the goals to be achieved by 2024.

☆ | To establish a position as a reuse tech company by promoting the integration of reality x technology (IT and DX) |

☆ | To maintain a solid leading position unrivaled by any other company in the reuse at-home pick up service |

☆ | An average annual growth rate of approximately 40% in consolidated ordinary profit during the three years of organic growth (FY 12/2024) |

☆ | To establish a corporate governance structure that balances sustainable growth and governance tightening to maximize shareholder value |

(2) Management Strategy

① Basic policy

As mentioned in the Company Overview section, the growth potential of the reuse market is extremely large.

The company believes that in this explicit market, which is estimated to be worth 3 trillion yen in 2022, all purchase channels (stores, home delivery, etc.) will be available, although the customer base ranges from young people to senior citizens, competition is intense.

On the other hand, in the dormant reuse market, which is estimated to have hidden assets of 37.1 trillion yen, the main need is to sell items for clearance and disposal, so at-home pick up services are advantageous because they allow direct access to unwanted items in customers’ houses; the customer base is mainly senior citizens who have many hidden assets, and competition is not expected to be as intense as in the explicit market.

Therefore, the company's basic policy is to "expand market share by strengthening purchase channels such as stores and M&A" in the explicit market and to "place the highest priority on investment for growth in the at-home pick up service and maintain a leading position" in the latent market.

② Competitive advantage in potential markets

The company's mainstay business is the at-home pick up service, which allows direct access to "hidden assets" lying in the home by visiting customers at their residences. The company's strength lies in its ability to purchase goods such as kimonos and stamps, which are in high demand for disposal, as well as the fact that approximately 60% of its customers use the service for estate liquidation and home clearance, and that 82% of its customers are seniors in their 50s or older.

These points are the source of the company's competitive advantage in the "hidden assets" market, a reuse market with large growth potential.

③ Five Management Strategies

The company has set forth five management strategies to realize its vision.

A | To accelerate technology investments, particularly in IT and DX enhancement |

B | To continue to strengthen the at-home pick up service and toC sales |

C | To expand the purchase store business |

D | M&A |

E | New Business |

Based on "A," the company aims for organic growth in "B" and "C," and inorganic growth in "D" and "E."

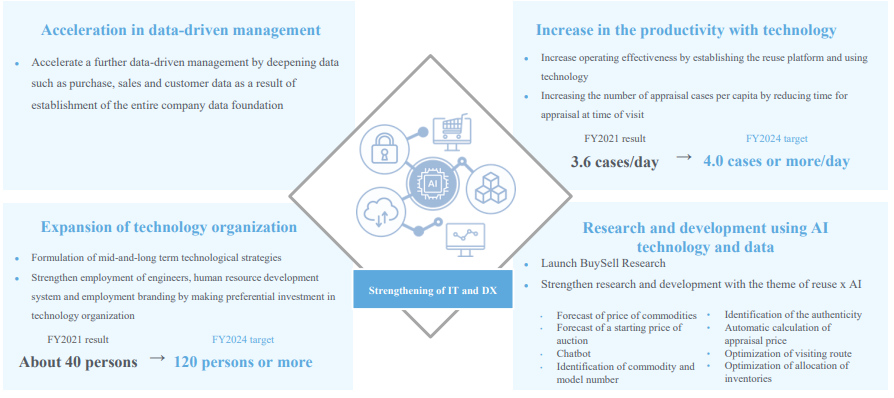

[A: To accelerate technology investments, focusing on IT and DX enhancement]

They will accelerate business growth by improving productivity through the use of technology and deepening data-driven management through the development of data infrastructure.

They aim to become a reuse tech company by promoting the fusion of reality (people and products) and technology (IT and DX).

(Source: the reference material of the Company)

[B: To continue to strengthen the at-home pick up service and toC sales"]

◎Area expansion strategy for the at-home pick up service

The company aims to achieve further growth by increasing the number of at-home visits and maximizing variable profit per visit in each area through the development of optimal marketing strategies and the allocation of offices and personnel to each regional area, in addition to the metropolitan areas centered on Tokyo, Nagoya, and Osaka.

In the Tokyo, Nagoya, and Osaka areas, where the volume of inquiries and purchases is high, and gross profit per visit is high, but competition is fierce and advertising expenses tend to be high, the company will further strengthen its foundation through ongoing investment.

On the other hand, in the priority regional areas, where gross profit per visit is lower than those in the Tokyo, Nagoya, and Osaka areas, but the competitive environment is not as fierce as in the Tokyo, Nagoya, and Osaka areas, investments will be strengthened because they enable efficient advertising with low advertising costs.

The company will develop a cross-media marketing strategy, which is one of the company's strengths, by dividing the areas into smaller segments. In addition, by increasing the number of offices, the company will strengthen its sales force with an optimized organization and staffing in each area.

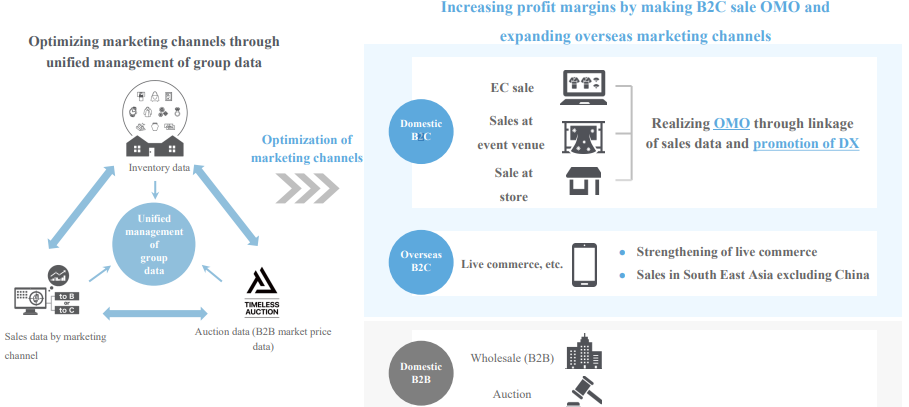

Strengthening of toC sales through the use of technology in sales

The company aims to improve profitability by optimizing sales channels through centralized management of group data such as "inventory," "sales by channel," "auctions," etc., promoting Online-Merge-Offline (OMO) in toC sales, and expanding overseas sales channels.

(Source: the reference material of the Company)

[C: Expansion of the purchase store business.]

They will accelerate store development while leveraging group synergies to strengthen the toC purchase channel, which is differentiated from at-home pick up service.

As of December 2021, BuySell had five stores in major cities nationwide, and its main products are kimonos, stamps, and old coins. Due to its large-scale marketing, the company is highly recognized for its at-home pick up service, which is a major advantage in attracting customers.

On the other hand, TIMELESS, whose main products are brand-name products, watches, and jewelry, has 14 permanent stores in department stores nationwide, whose good location and a sense of security are significant characteristics.

By leveraging the advantages and features of both companies, the company will accelerate store development through group synergies by promoting mutual customer traffic, marketing, data sharing, hiring and personnel exchanges, and other measures. The company aims to have over 50 group stores by 2024.

(Main KPI targets for the at-home pick up service)

| Results in 2021 | Goal in 2024 |

Number of at-home visits | 209,526 | 320,000 |

Variable profit per at-home visit (yen) | 40,238 | 51,000 |

Gross profit per at-home visit (yen) | 57,324 | 72,000 |

Advertising expense per at-home visit (yen) | 17,086 | 21,000 |

Number of inquiries | 350,204 | 508,000 |

CPA (yen/case) | 10,223 | 13,000 |

Number of employees (people) in FS business (at-home visits) | 314 | 500 |

Highly Ranked Appointment Ratio (%) | 44.4 | 50 |

Ratio of toC sales (%) | 20.3 | 30 |

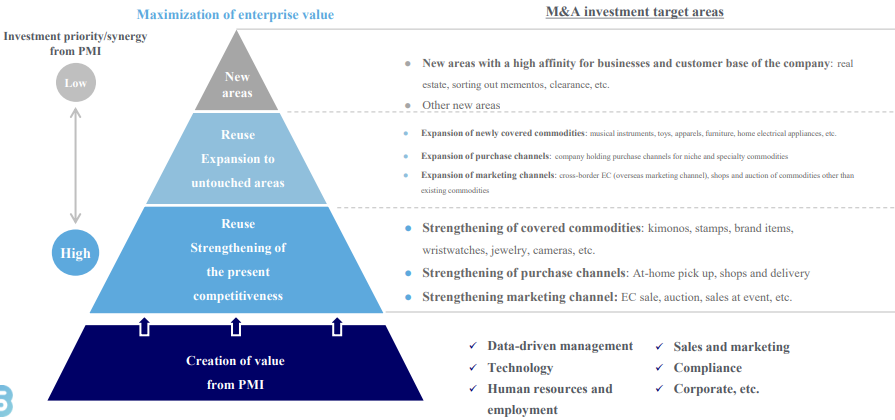

[D: M&A Strategy]

The company will focus on M&A in the reuse domain, giving priority to executing investments that contribute to strengthening existing competitiveness and developing areas that have yet to be reused.

In addition, the company aims to increase corporate value by enhancing return on investment through strategic M&A in areas where there is a high probability of creating synergies through PMI.

TIMELESS, which became a subsidiary in 2020, has contributed significantly to the enhancement of the Group's corporate value by generating group synergies through effective PMI after M&A, generating profits that significantly exceeded the burden of goodwill amortization, and improving EPS over the dilution impact of the stock swap.

Based on this track record, the company will continue to pursue effective M&A activities.

(Source: the reference material of the Company)

[E: New Business]

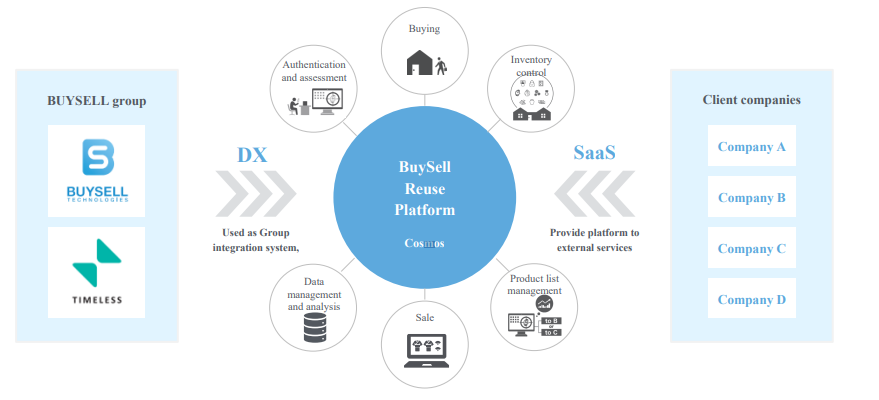

Scheme of changing the reuse platform into SaaS

The platform that has been used within the company group up to now was launched as the BuySell reuse platform (Cosmos) and was converted to SaaS. By providing this platform to outside vendors, the company will create a new pillar of revenues. The platform will provide a full range of functions from purchasing to selling and will realize a world in which a variety of reuse vendors use the BuySell Reuse Platform.

In addition, the company will use the platform as an integrated group system through the promotion of DX in pursuit of greater efficiency and maximization of earnings.

(Source: the reference material of the Company)

Promoting commercialization in the areas of liquidation and disposal needs and seniors

The company has been promoting a model of sending customers through alliances, focusing on areas that have a high affinity with the company's main customers, such as seniors and their clearance and disposal needs (collection of unwanted items, real estate sales, insurance, inheritance and counseling for end-of-life preparation, etc.), and aims to launch a business within its own group in addition to this model.

(3) Investment and Financial Strategy

① Capital Allocation Policy

Based on the ability to generate operating cash flow based on high-profit growth and flexible debt financing based on a stable financial base, the company aims to secure funds to invest in businesses and M&A for growth and allocate capital for sustainable growth.

Investment resources will be allocated in the following order of priority: "operating CF from business," "interest-bearing debt," and "equity."

Regarding capital allocation, in addition to business investments for organic growth, priority will be given to strategic investments for inorganic growth, mainly M&A.

② Investment Policy

The company is actively pursuing strategic investments in M&A for non-continuous growth and business investments for sustainable growth based on a disciplined investment policy.

Regarding business investment, the company will invest in technologies for enhancing IT and DX, marketing, human resources (recruitment and organizational strengthening), relocation and expansion of warehouses, store expansion, and strengthening of the compliance system. The company will control the allocation of funds while considering the forecast profit.

In M&A, from the perspective of maximizing corporate value and synergies, priority will be given to majority investments that can be consolidated into a consolidated group. The company will implement disciplined investment practices such as setting a maximum EV/EBITDA multiple and targeting profitable companies or companies with a high probability of becoming profitable in the short term.

For new businesses, the initial investment will be limited, and after carefully examining business profitability and growth potential, the investment limit will be gradually expanded in phases where the return on investment can be expected.

③ Financial Policy

To enable aggressive business investment and M&A activities while securing investment funds, the company maintains the stability of its financial base through disciplined financial management while emphasizing investment for growth.

The company's financial discipline includes a net D/E ratio of 0.5 or lower, a Net Debt/EBITDA ratio of 1.0 or lower, and a capital adequacy ratio of 40% or higher.

④ Shareholder Return Policy

The company's basic policy is to return profits to shareholders through stable and continuous dividends, while aiming to increase TSR (Total Shareholder Return) through medium- and long-term share price appreciation by increasing EPS through prioritizing investments for growth.

The target consolidated dividend payout ratio is 20%. They will maintain the current dividend policy.

(4) Governance Structure and ESG/SDGs

① Strengthen the corporate governance structure

With the aim of enhancing corporate value, further improving governance, and increasing management transparency and objectivity, the company will shift to a system in which independent outside directors constitute a majority of the Board of Directors, along with the transition to a company with an audit committee.

In addition, the company will continue to operate a voluntary Nomination and Compensation Advisory Committee, which is chaired and majority-owned by outside directors and will increase the ratio of female directors from the perspective of promoting diversity on the Board of Directors. The number of female directors increased by two to become three out of a total of eleven directors.

In addition, by nominating directors based on a skills matrix that defines key areas of expectation for directors, the composition of the Board of Directors will be changed to enable both medium- and long-term growth of the group and stronger governance.

② ESG/SDGs

From the perspective of the sustainability of business activities required by society, the company established a sustainability strategy policy focusing on compliance, risk management, and organizational and human resource management.

The two pillars of the strategy are "compliance and risk management" and "organization and human resource management."

Under "Compliance and Risk Management," the key measures are to strengthen corporate/service governance, enhance information security, and maintain/improve reliability in at-home pick up service.

In the area of organizational and human resource management, the key measures are strengthening recruitment and training, improving employee engagement, and bridging the skills and gender gap.

(5) Business Performance Targets

The organic and inorganic targets for 2024 are as follows

① Organic Targets

| Actual results for FY 12/21 | Target for FY 12/24 | CAGR |

Net sales | 247 | 465 | approx. 23% |

Ordinary Income | 22.9 | 60 | approx. 38% |

Ordinary Income Ratio | approx. 9% | approx. 13% | +4pt |

*Unit: Hundred million yen. Organic growth of existing businesses of BuySell and TIMELESS. The impact of future M&A is excluded. CAGR: compound annual growth rate.

② Inorganic Targets

They aim for non-continuous growth through aggressive promotion of M&A.

The recurring profit target for FY12/2024 is 6 billion-plus yen.

To lay the foundation for long-term business sustainability and growth in FY12/2024 and beyond.

<Reference2: Regarding Corporate Governance>

Organization type, and the composition of directors and auditors

Organizational Type | Company with Audit & Supervisory Committee |

Directors | 11 directors, including 6 outside directors |

Auditors | 3 auditors, including 3 outside auditors |

Corporate Governance Report

The latest revision date: March 24, 2023

<Fundamental Concept>

The Company recognize that establishing corporate governance is essential in order to increase corporate value, maximize shareholder returns, and build good relationships with stakeholders such as customers, business partners, employees, local communities, and government agencies.

To this end, the Company believe that it is important to establish a decision-making body that responds quickly and fairly to changes in the business environment, pursue Profits through its businesses, ensure that its financial soundness and improve its credibility, actively disclose information to fulfill accountability, build an effective internal control system, and ensure that audit and supervisory board members maintain their independence and fulfill their audit functions.

<Reasons for not implementing each principle of the Corporate Governance Code>

The Company has implemented all the basic principles of the Corporate Governance Code.

This report is not intended for soliciting or promoting investment activities or offering any advice on investment or the like, but for providing information only. The information included in this report was taken from sources considered reliable by our company. Our company will not guarantee the accuracy, integrity, or appropriateness of information or opinions in this report. Our company will not assume any responsibility for expenses, damages or the like arising out of the use of this report or information obtained from this report. All kinds of rights related to this report belong to Investment Bridge Co., Ltd. The contents, etc. of this report may be revised without notice. Please make an investment decision on your own judgement. Copyright(C), All Rights Reserved by Investment Bridge Co., Ltd. |