Bridge Report:(1433)BESTERRA the Interim Period of Fiscal Year Ending January 2026

![]()

President Yutaka Honda | BESTERRA CO., LTD (1433) |

|

Company Information

Market | TSE Prime Market |

Industry | Construction business |

President | Yutaka Honda |

HQ Address | Kiba Park Building, 3-2-6 Hirano, Koto-ku, Tokyo, Japan |

Year-end | End of January |

Homepage |

Stock Information

Share Price | Share Outstanding | Market Cap. | ROE (Act.) | Trading Unit | |

¥1,046 | 9,224,300 shares | ¥9,648 million | 9.2% | 100 shares | |

DPS (Est.) | Dividend Yield (Est.) | EPS (Est.) | PER (Est.) | BPS (Act.) | PBR (Act.) |

¥40.00 | 3.8% | ¥61.06 | 17.1 x | ¥546.88 | 1.9 x |

*The share price is the closing price on October 16. Share outstanding, DPS, and EPS are from the financial results for the second quarter of the fiscal year ending January 2026. ROE and BPS are actual results in the previous fiscal year.

Consolidated Earnings

Fiscal Year | Net Sales | Operating Income | Ordinary Income | Net Income | EPS | DPS |

Jan. 2022 (Actual) | 5,966 | 488 | 721 | 1,391 | 165.48 | 16.00 |

Jan. 2023 (Actual) | 5,458 | -215 | -94 | -64 | -7.33 | 20.00 |

Jan. 2024 (Actual) | 9,394 | 246 | 407 | 231 | 26.08 | 20.00 |

Jan. 2025 (Actual) | 10,897 | 373 | 592 | 409 | 46.25 | 20.00 |

Jan. 2026 (Forecast) | 12,000 | 700 | 700 | 550 | 61.06 | 40.00 |

* The forecasted values were provided by the company. Unit: million yen. Net income is profit attributable to owners of parent.

This Bridge Report introduces the earning results for the interim period of the fiscal year ending January 2026 and other information of BESTERRA CO., LTD.

Table of Contents

Key Points

1. Company Overview

2. Interim Period of Fiscal Year Ending January 2026 Earnings Results

3. Fiscal Year Ending January 2026 Earnings Forecasts

4.Leading the Future-Medium-Term Management Plan 2030

5. Interview with President Honda

6. Conclusions

<Reference: Regarding Corporate Governance>

Key points

- In the interim period of the fiscal year ending January 2026, sales declined 11.6% year on year to 5.1 billion yen. They allocated manpower to the finalization of multiple completed projects, which were ordered before the current fiscal year, and the production completion reports. Sales dropped, as they engaged in marketing under the policy of choosing and receiving orders for projects whose gross profit margin is high, but their system for choosing and receiving orders has not been established to a sufficient degree. Operating income rose 6.8% year on year to 226 million yen. Gross profit margin rose year on year from 16.7% to 18.2%. Operating income margin improved year on year from 3.7% to 4.4%, as SG&A expenses dropped 6.6% as they curtailed R&D expenses in unprofitable businesses. Both sales and profit fell below the company’s forecast. They will pay an interim dividend of 15.0 yen/share, up 5.0 yen/share year on year, as forecast.

- For the fiscal year ending January 2026, sales are expected to grow 10.1% year on year to 12 billion yen and operating income is projected to rise 87.3% year on year to 700 million yen. The initial forecasts of sales and profit have been revised downwardly. In the fiscal year ending January 2026, they set a goal of achieving a high operating income margin, and have engaged in marketing activities under the policy of choosing and receiving orders for projects whose profit margin is high, so the profit margin of projects they have undertaken is recovering. However, they were not able to receive orders for some large-scale projects whose profit margin is high. A project was suspended for a reason attributable to the client after the commencement of the project, producing a significant effect and decreasing profit margin significantly. In addition, the improvement in profitability was not seen until the end of the interim period for some unprofitable businesses. The year-end dividend has not been revised, so they plan to pay 25.0 yen/share, up 15.0 yen/share from the end of the previous fiscal year, so the annual dividend amount will be 40.0 yen/share, up 20.0 yen/share from the previous fiscal year.

- We interviewed President Yutaka Honda, and regarding the current share price, he said “I don’t think share price is left untouched unreasonably,” and to shareholders and investors, he gave a message: “The plant demolition market will certainly grow. I believe that our company possesses technologies and the capacity of recruitment to survive the competition without fail. In the interim period, we failed to meet your expectations, but we will make efforts to meet your expectations from now on.”

- The performance in the interim period fell below the company’s forecast, due to the suspension of a project and the upfront posting of costs for additional projects, so the forecast for fiscal year ending January 2026 has been revised downwardly. After bottoming out in fiscal year ended January 2023, sales growth and profit have been improving. Through the interview with President Honda, we felt that he had confidence. It is expected that less profitable projects will disappear in fiscal year ending January 2027 or before and the plan for fiscal year ending January 2031 will be achievable. If they proceed with the strengthening of systems for marketing and estimating total costs, we can expect a lot, as the plant demolition market will certainly grow. Sales growth and profit margin are improving. If this upward trend continues, share price will probably improve.

1. Company Overview

As a specialist in plant dismantlement, BESTERRA manages the dismantlement of plants (metal structures) for iron-making, power generation, gas, petroleum, etc. Its core competence is “the method and technology for dismantling plants,” and it has many patented methods including international patents. The company concentrates its managerial resources on engineering (proposal, design, and work planning) and management (supervision and work management), and outsources actual dismantlement work to its affiliates, and so it does not own heavy machinery or construction teams (the risk of owning assets can be avoided), and it is unnecessary to procure materials, etc. and make transactions for material production (the inventory risk can be avoided).

In addition to the company, the group has acquired Hiro Engineering, which provides human resource services for design work, etc., 3D Visual KK, which handles 3D scan modeling and design work, and Yazawa Co., Ltd., which owns advanced technologies for removing asbestos as consolidated subsidiaries. Additionally, in August 2023, the company has also acquired Oda Corporation Co., Ltd., which mainly maintains work and main frame construction work, and its subsidiary, TOKEN Co., Ltd. as consolidated subsidiaries. As of the end of July 2025, there were five consolidated subsidiaries. Hiro Engineering and 3D Visual KK are scheduled to be transferred in November.

The corporate name “BESTERRA” was coined by combining the English word “Best (the superlative of ‘good’)” and the Latin word “Terra (the earth),” and infused with the ambition to “create the best earth.” By developing an integrated system for dismantling and recycling, the company aims to actualize an advanced recycling society and contribute to the earth environment.

1-1 Corporate ethos

Established in 1974 based on its corporate philosophy of "Contributing to the global environment through flexible ideas, creativity and technical prowess." The company offers a variety of high-value-added services, focusing on dismantling plant facilities, aiming to realize a society that is both decarbonized and characterized by a high degree of recycling.

Making sustainable demolition the norm. Sustainable demolition is upheld as an aesthetics principle. To strengthen ESG management, focusing on the three factors “environment,” “social,” and “governance” in order to contribute to achieving the SDGs, which are the goals for realizing a sustainable society. Rather than simply demolishing, the company provides sustainable demolition that is reasonable through the use of natural energy-based demolition techniques and the establishment of advanced environmental recycling systems.

1-2 Characteristics of the business

The company has a single segment consisting of demolition and maintenance business. For others, it engages in the human resource service business and the 3D scan, modeling, and design business. In the fiscal year ended January 2025, demolition and maintenance business accounted for 97.2% of total sales.

Demolition and maintenance business

In the demolition and maintenance business, the company works mainly on all types of plants in the fields of ironmaking, electric power, gas, petroleum, and petrochemicals, etc. The company offers services on overall engineering processes including proposals, designing, work planning, outsourcing/arrangement of equipment and materials, supervision, safety management, cost management, financial management, and handling of governmental procedures. It focuses on designing its unique demolition technologies and supervising demolition works based on demolition plans and uses specialized subcontractors for demolition works. The clients for plant dismantlement are leading companies that own plants for ironmaking, electric power, gas, petroleum, etc. In most cases, the equipment installation companies of the corporate groups of clients or leading general contractors are entrusted with dismantlement, and then BESTERRA serves as the primary or second-tier subcontractor.

Also, in the plant dismantlement business, BESTERRA receives valuable materials generated through dismantlement, such as scrap, and sells them to scrap handlers. Accordingly, the company estimates the value of valuable materials while comprehensively considering the material, quantity, price (market price of each material, such as iron, stainless steel, and copper), etc. and negotiates with clients about the fee for dismantlement work. In accounting, the gain from sale of valuable materials is included in revenue from dismantlement work and posted as part of sales from completed dismantlement work. In some cases, contractors (clients) dispose of (sell) scrap, etc. by themselves.

Furthermore, Oda Corporation Co., Ltd. and TOKEN Co., Ltd., which became consolidated subsidiaries in August 2023, will be part of the demolition and maintenance business, with maintains work and main frame construction work for various plants as their core business.

*Two standards for posting revenue and seasonality of revenue posting of the company

The standards for posting revenue from contracts can be classified into the completed contract method, in which revenue is posted when works are completed, and the percentage-of-completion method, in which revenue is posted according to the progress of works. The company basically applies the percentage-of-completion method to large-scale projects whose period exceeds 3 months from the fiscal year ended January 2023 (the completed contract method is applied to projects that do not meet the aforementioned criteria). The timing of posting revenue (the completion of demolition work) from works for which the completed contract method is used is often affected by the capital investment plans of clients. In the case of BESTERRA, revenue tends to be posted in the first quarter (February to April) and the fourth quarter (November to January) (the seasonality of revenue posting). However, the variation in quarterly performance may mislead investors, so the company is expanding the scope of application of the percentage-of-completion method step by step, to equalize the timings of revenue posting.

Others

In response to the chronic shortage of skilled construction workers, the company began providing human resource services in January 2013, and in March 2018, it made Hiro Engineering, which handles human resource services such as design work, a subsidiary. In January 2015, the company began offering a 3D measurement service as well. It established 3D Visual KK in December 2019, and 3D scan modeling and design business was transferred from INTER ACTION Corporation (securities code: 7725) in February 2020.

1-3 Strengths

① An excellent client base, efficient dismantlement management based on plenty of experience, and intellectual property, such as patented methods

The strengths of the company are excellent client assets, efficient dismantlement management based on plenty of experience, and intellectual property, such as patented methods. The clients are basically engineering subsidiary companies of leading companies in ironmaking, electric, gas, coal oil fields, and major general contractors, which are excellent clients with no credit concerns. The clients of the leading companies highly evaluate the company’s total management (low cost and high efficiency) of plant dismantlement that it cultivated experiences for over 40 years. Another strength is the various technologies and know-how that the company has accumulated through environmental protection construction projects, etc., which have become its actual and potential intellectual property, including the recycling of waste materials.

The company operates business under the concepts of "unbreakable by its creators (new ideas)," "the only one company specializing in plant dismantling," and "asset-light management.”

Patented methods, etc.

“Apple peeling demolition method” and fusing robot “Ringo☆Star”

The “apple peeling demolition method” is a method of dismantling a large spherical tank, such as gas holders and oil tanks, by cutting it in spirals from the center of the ceiling of the enclosure part. The cut part spirals down to the ground gradually under the force of the earth’s gravity (natural energy). The method enjoys superiority in a work period, cost, and safety, and has considerable competitive advantages, realizing “greater promptness, higher cost efficiency, and added safety.” Furthermore, the company offers a robot for the fusing process, “Ringo☆Star,” which automates the “apple peeling demolition method.” (The company is also working to expand the range of applications for “Ringo☆Star” by developing a new attachment).

Environment-related methods

The company has cultivated experiences and business results of a multitude of environment-related demolition works, using the “fireless methods” which do not require the use of fire. For example, although polychlorinated biphenyls (PCBs) are considered as a toxic substance and therefore totally abolished today, it had been used for many years in transformers and condensers because of its excellent thermal stability and chemical stability (electric insulation characteristics). In many cases, transformers and condensers are disposed of in conjunction with plant demolition works; however, because PCBs gasify when they are treated at the high temperature, posing a risk of inhaling the gas so generated, any firearms (such as gas cutting machines) cannot be used in demolition and withdrawal involving PCBs. The company is skillful at fireless and quasi-fireless methods using saber saws (which cut off objects with their saw blades moving in a reciprocating manner) that can cut off objects thicker than the thickness, which, in the industry, had been considered impossible to cut, through numerous devices, including measures against seizure of motors and recycling of blades. BESTERRA has applied for joint patents with Hitachi Plant Construction, Ltd. for a transformer dismantling method, a transformer dismantling jig, and a cutting device for dismantling a transformer.

Windmill demolition works

The number of power-generating wind turbines continues to increase by about 20% annually worldwide, but the demand for dismantling is expected to increase in the future due to wear and tear and economic obsolescence. According to the company's data, the global wind power generation amount has continued to grow at an annual rate of about 20%, reaching 486,790 MW (about 340,000 onshore units and about 4,000 offshore units). In Japan, there were 2,574 wind turbines as of the end of 2021, mostly onshore, but the trend is shifting toward offshore wind power. Meanwhile, as the useful life is approximately 15 to 20 years, and the windmills for power generation established in the early stage are reaching the application limit. Moreover, not a few plants need to be dismantled due to damage or fatal failure caused by thunderbolts or typhoons.

How to knock down a power-generating wind turbine (international patent application)

Dismantling of windmills is usually done using scaffolding erected on the outside of the supports. As some windmills have been built in mountain districts and on the sea, demolition of them is highly difficult. The company has devised a method for dismantling wind turbines that does not require scaffolds and has already acquired a domestic patent for “Method of knocking down a power-generating wind turbine.” International patents are pending for “Method of knocking down towering structures using their bases” and “Method for dismantling tower-shaped equipment for wind power generation.” Safety of workers can be improved dramatically, and the work period can be shortened by using these patent-based methods.

② Age structure that enables sustainable business growth

Approximately half of the company's employees are aged 20 to 30 years. In the entire construction industry in Japan, employees aged 20 to 30 years account for 26%, and those aged 50 to 60 years make up about 50%. Therefore, the company has a workforce composition that enables sustainable business growth. The company will keep recruiting dismantlement supervisors actively and diversify employees by recruiting more women and non-Japanese people.

Meanwhile, the company's re-employment system after retirement is also well-established. Employees retain 100% of their pre-retirement salary. Employment is guaranteed as contract employees until age 65. Employees may continue working beyond age 65. The company is also expanding its educational programs to facilitate the transfer of skills from veteran employees to newly hired employees.

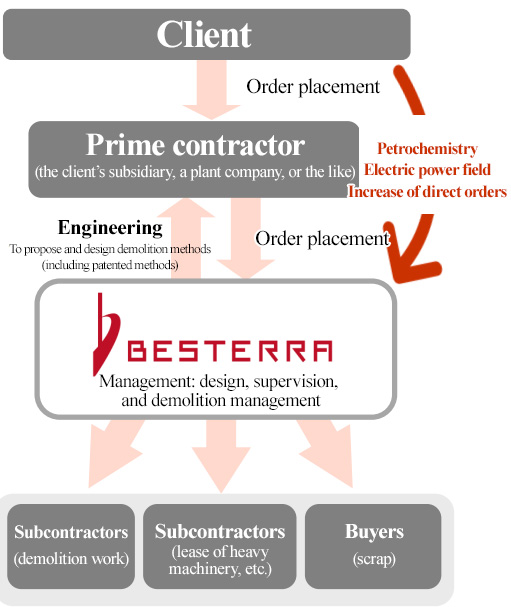

1-4 Business model (business structure chart)

| 1 Key Role in Large-Scale Plant Demolition Engineering (Proposal, Design, and Demolition Planning) Management (Supervision and Demolition Management) |

2 The actual demolition work is performed by subcontractors, while BESTERRA primarily handles on-site supervision and demolition management. | |

3 The company's core competency lies in providing plant dismantling methods and technologies. (Asset-light management) It does not own demolition machinery or labor teams. → Avoiding Asset Ownership Risk There are no purchasing or production transactions for materials or other items. → Avoiding inventory risk |

1-5 ROE analysis

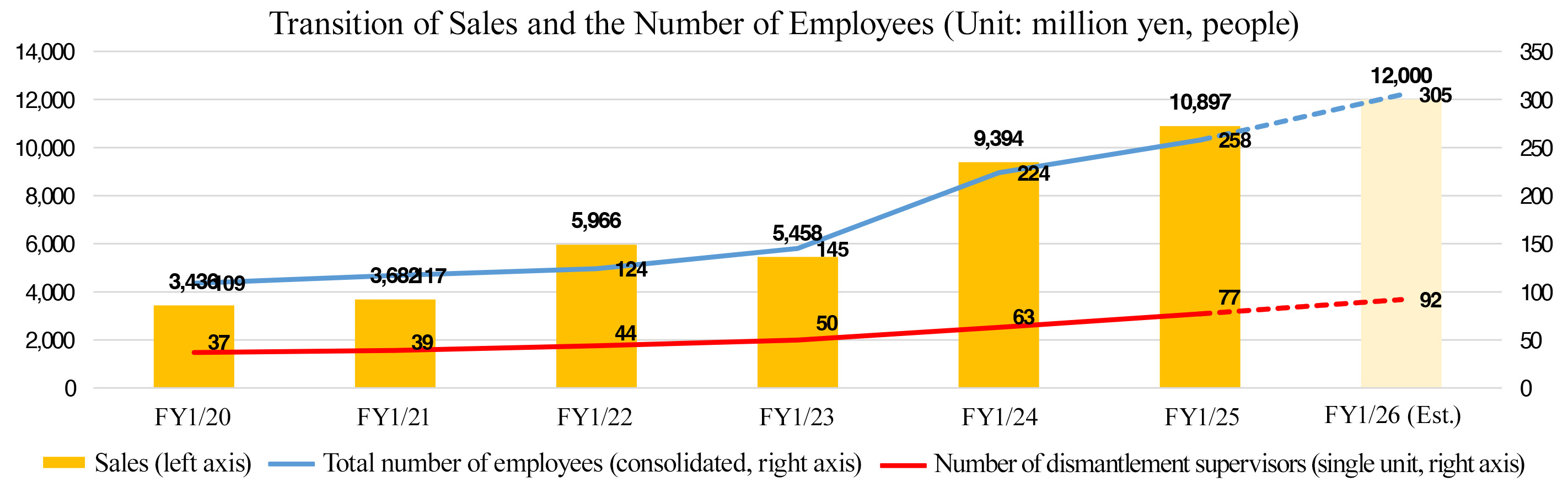

| FY 1/19 | FY 1/20 | FY 1/21 | FY 1/22 | FY 1/23 | FY 1/24 | FY 1/25 |

ROE (%) | 23.8 | 2.3 | 5.6 | 40.6 | -1.5 | 5.5 | 9.2 |

Net Income to Sales Ratio (%) | 12.62 | 1.75 | 3.87 | 23.32 | -1.18 | 2.46 | 3.76 |

Asset Turnover Ratio (Times) | 1.08 | 0.72 | 0.67 | 0.80 | 0.63 | 0.97 | 0.99 |

Leverage (Times) | 1.75 | 1.85 | 2.14 | 2.19 | 2.01 | 2.28 | 2.45 |

The ROE in the fiscal year ended January 2025 is higher than that in the previous fiscal year. Leading the Future, the medium-term management plan 2030 (see below), targets “an ROE of 20% or higher in the fiscal year ending January 2031.”

2. Interim Period of Fiscal Year Ending January 2026 Earnings Results

2-1 Consolidated results

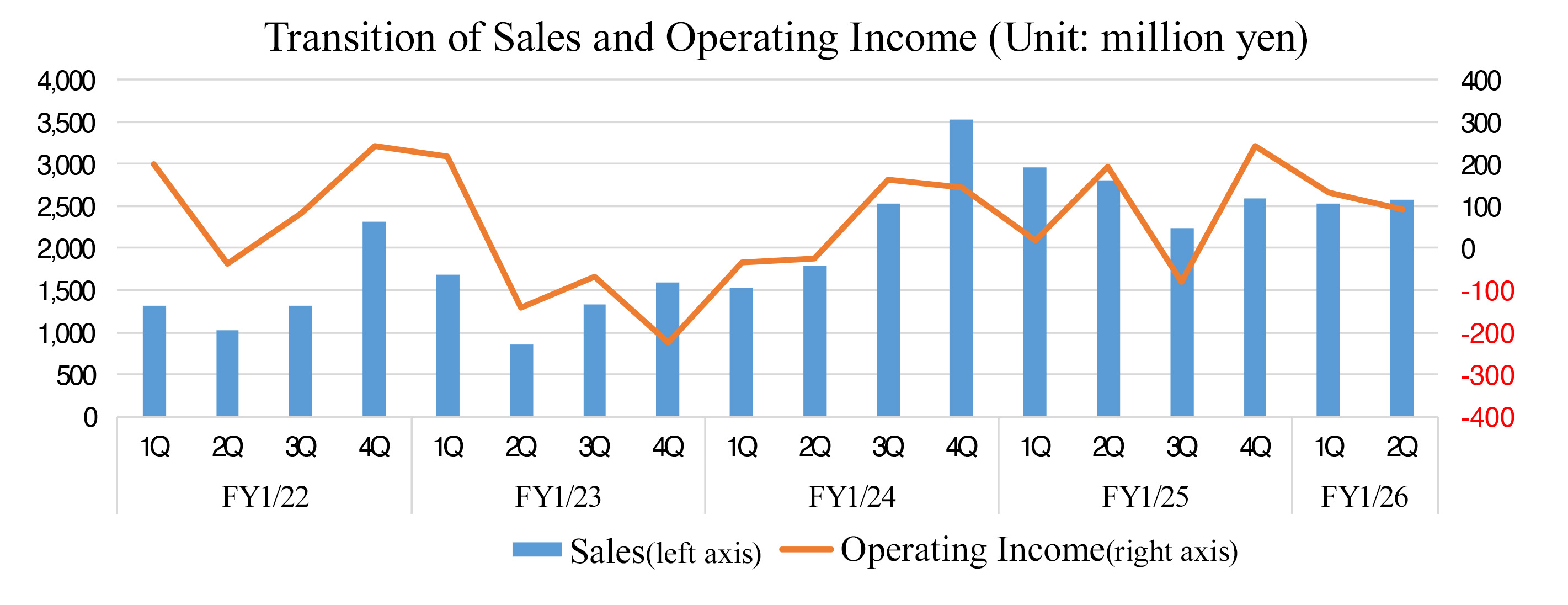

| FY 1/25 Interim period | Ratio to sales | FY 1/26 Interim period | Ratio to sales | YoY | Company forecast ratio |

Sales | 5,767 | 100.0% | 5,100 | 100.0% | -11.6% | -2.7% |

Gross profit | 960 | 16.7% | 925 | 18.2% | -3.6% | - |

SG&A expenses | 749 | 13.0% | 699 | 13.7% | -6.6% | - |

Operating income | 211 | 3.7% | 226 | 4.4% | +6.8% | -35.9% |

Ordinary income | 258 | 4.5% | 215 | 4.2% | -16.8% | -45.3% |

Interim net income | 127 | 2.2% | 220 | 4.3% | +73.4% | -37.0% |

*Unit: million yen. Net income is net income attributable to owners of the parent company.

Sales declined but operating income rose

Sales declined 11.6% year on year to 5.1 billion yen. Multiple large-scale projects, which were ordered before the current fiscal year, have been completed, and they allocated manpower to the finalization of multiple completed projects and the production completion reports. Sales dropped, as they engaged in marketing under the policy of choosing and receiving orders for projects whose gross profit margin is high, but their system for choosing and receiving orders has not been established to a sufficient degree.

Operating income rose 6.8% year on year to 226 million yen. Gross profit margin rose year on year from 16.7% to 18.2%. Operating income margin improved year on year from 3.7% to 4.4%, as SG&A expenses dropped 6.6% as they curtailed R&D expenses in unprofitable businesses. In non-operating revenues, dividends received decreased, while in non-operating expenses, commissions paid augmented, so ordinary income declined 16.8% year on year to 215 million yen. As an extraordinary income, a gain on sale of investment securities was posted, and interim net income rose 73.4% year on year to 220 million yen.

Both sales and all kind of profit fell below the company’s forecast.

They will pay an interim dividend of 15.0 yen/share, up 5.0 yen/share year on year, as forecast.

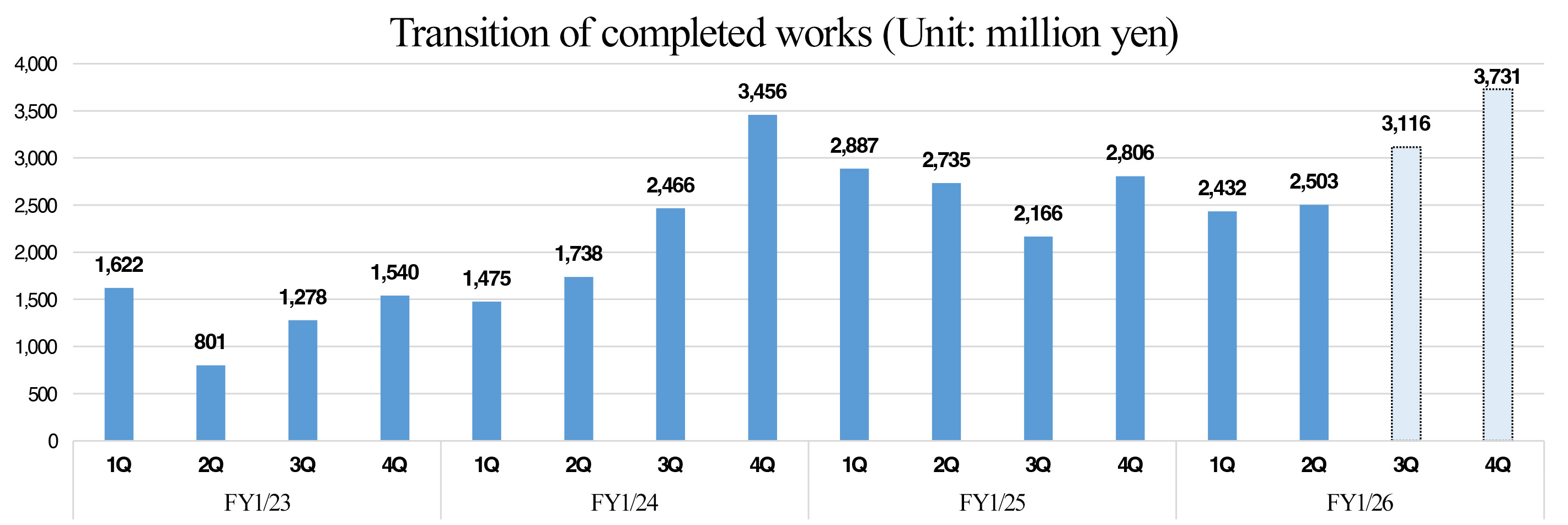

The number of completed works (rough estimates)

| FY 1/25 Interim period | Composition ratio | FY 1/26 Interim period | Composition ratio | YoY |

Electric power | 1,687 | 30% | 740 | 15% | -56% |

Steelmaking | 1,068 | 19% | 1,974 | 40% | +85% |

Petroleum/petrochemical | 1,855 | 33% | 1,283 | 26% | -31% |

Gas | 56 | 1% | 49 | 1% | -12% |

3D | 56 | 1% | 49 | 1% | -12% |

Environment | 225 | 4% | 148 | 3% | -34% |

Others | 675 | 12% | 691 | 14% | +2% |

Total of completed works | 5,622 | 100% | 4,936 | 100% | -12% |

*Unit: million yen. Prepared by Investment Bridge Co., Ltd. based on company data.

In particular, the number of orders received in the iron-making industry was healthy, accounting for a larger proportion of the amount of completed projects. Sales dropped in the electric power industry, but large-scale projects whose profit margin is high have been contributing to sales from the middle of 2Q.

In fiscal year ending January 2026, the amount of completed projects is expected to be larger in the second half. In fiscal year ended January 2025, the amount of completed projects was larger in 1Q and 4Q. For fiscal year ending January 2026, the amount of completed projects is expected to increase gradually.

Breakdown of SG&A

| FY 1/25 Interim period | Ratio | FY 1/26 Interim period | Ratio | YoY | Major change factors |

Personnel expenses | 361 | 6.3% | 350 | 6.9% | -3.0% |

|

R&D expenses | 35 | 0.6% | 6 | 0.1% | -82.9% | Robot Development, System development |

Fees and compensation paid | 93 | 1.6% | 107 | 2.1% | +14.5% | Marketing cooperation expenses (12 million yen) |

Recruiting expenses | 29 | 0.5% | 24 | 0.5% | -16.1% | Advertising media, introduction commissions |

Others | 227 | 3.9% | 209 | 4.1% | -7.7% | Amortization of goodwill, etc. |

Total SG&A expenses | 749 | 13.0% | 699 | 13.7% | -6.6% |

|

*Unit: million yen. Ratio is ratio to sales.

SG&A expenses decreased, due to the curtailment of R&D expenses in unprofitable businesses, the drop in depreciation/amortization caused by the impairment of goodwill in the previous fiscal year, etc.

Through active recruitment activities, the number of dismantlement supervisors increased by 10 from the beginning of the fiscal year to 87 by September. In the fiscal year ending January 2026, the company plans to increase the number of dismantlement supervisors by 15.

2-2 Orders received and the backlog of orders

| FY 1/25 Interim period | FY 1/26 Interim period | YoY |

The backlog of orders at the beginning of the term | 7,087 | 7,197 | +1.6% |

The amount of works received | 4,710 | 4,186 | -11.1% |

The amount of completed works | 5,622 | 4,936 | -12.2% |

The backlog of orders at the end of the term | 6,174 | 6,447 | +4.4% |

*Unit: million yen

They received orders, which amount to 2,846 million yen, in 2Q, under a favorable environment where they started receiving orders for large-scale dismantlement projects in the Keihin/Kurashiki region. Large-scale projects whose profit margin is low were all completed in 2Q, so the gross profit margin of order backlog is increasing.

Orders received by sector (Amounts are approximate.)

| FY 1/25 Interim period | Ratio | FY 1/26 Interim period | Ratio | YoY |

Electric power | 1,235 | 20% | 645 | 10% | -48% |

Steelmaking | 3,087 | 50% | 3,224 | 50% | +4% |

Petroleum/petrochemical | 1,544 | 25% | 1,934 | 30% | +25% |

Gas | 0 | - | 64 | 1% | - |

Environment | 123 | 2% | 387 | 6% | +213% |

Other | 185 | 3% | 193 | 3% | +4% |

Total order received | 6,174 | 100% | 6,447 | 100% | +4% |

*Unit: million yen

The order receipt environment remains healthy, thanks to the growth of demand for dismantlement in the fields of iron making, electric power, oil, and petrochemistry. In particular, the demand for dismantlement is expected to be large in the Keihin/Kurashiki region in the coming two fiscal years, and they have also received many business inquiries from other industries.

2-3 Financial condition

Financial condition

| January 2025 | July 2025 |

| January 2025 | July 2025 |

Cash | 1,599 | 1,612 | Payables | 1,185 | 1,316 |

Trade receivables | 5,137 | 3,752 | Borrowings and Bonds | 3,752 | 1,054 |

Current Assets | 7,130 | 5,753 | Liabilities | 6,192 | 3,187 |

Investments, Others | 3,473 | 2,252 | Net Assets | 4,853 | 5,225 |

Noncurrent Assets | 3,916 | 2,660 | Total Liabilities, Net Assets | 11,046 | 8,413 |

*Unit: million yen. Trade receivables include notes and accounts receivable, accounts receivable from completed construction contracts, and contract assets.

Total assets decreased 2.63 billion yen from the end of the previous fiscal year to 8.41 billion yen, mainly due to a decrease in trade receivable and investment securities. Total liabilities decreased 3 billion yen from the end of the previous fiscal year to 3.18 billion yen, through the repayment of debt, etc. Net assets increased by 0.37 billion yen to 5.22 billion yen due to the exercise of warrants, etc.

Capital-to-asset ratio rose 18.2 points from the end of the previous fiscal year to 62.1%.

2-4 Topics

① Basic Agreement for the Transfer of Group Companies

The company has reached a basic agreement with Suido Kiko Kaisha, LTD. regarding the transfer of shares in two non-core consolidated subsidiaries. This is aimed at optimizing their business portfolio and concentrating resources on the rapidly growing plant dismantling business. However, the impact on sales and operating profit is forecast to be reflected from the fourth quarter.

Overview of Subsidiaries Scheduled for Transfer

| Business overview | Number of employees | Net sales for the fiscal year ended January 2025 | Operating income for the fiscal year ended January 2025 | Scheduled date of share transfer |

Hiro Engineering Co., Ltd. | Worker dispatching business Design‐contracting business | 25 | 194 million yen | 2 million yen | November 28, 2025 |

3D Visual KK | 3D Scanning and Modeling Services, and Other Related Businesses | 16 | 125 million yen | -58 million yen |

Group Companies After the Transfer Net sales for the fiscal year ended January 2025, Unit: million yen

| Net sales | Overview and Features |

Yazawa Co., Ltd. | 316 | This company provides specialized technologies for dealing with hazardous substances and environmental pollution, including measures against asbestos represented by the “Yazawa Asbestos Removal Method” and measures against dioxins. |

ODA Corporation Co., Ltd. | 1,000 | Based in Kurashiki City, Okayama Prefecture, where the Mizushima Industrial Complex is located, this company has an extensive track record of projects as its core business, specializing in maintenance work for various plants and structural construction. |

TOKEN Co., Ltd. | 264 | This company undertakes large-scale repair projects for condominiums, commercial buildings, and similar structures. By disclosing all costs—including materials and labor expenses—it provides appropriate repair services. |

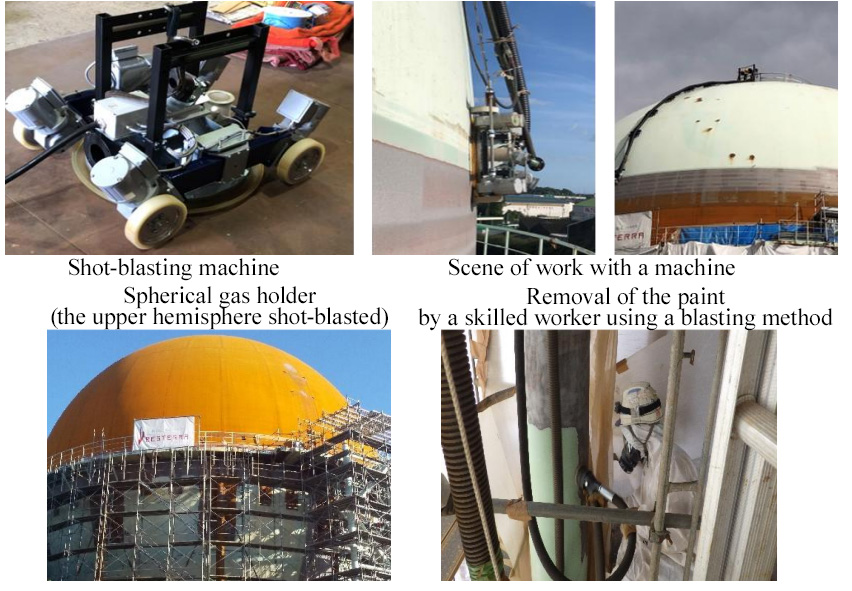

② Joint application for a patent concerning surface treatment of spherical gas holders

Patent application filed jointly with business partner MITANI SANGYO Co., Ltd. for removal of surface coating against harmful PCB-containing paint films on spherical gas holder surfaces.

Key Points of the Technologies Applied for Patent

✓ Surface treatment time for spherical gas holders reduced to about one-third of conventional methods!

Shot-blasting machines perform the work automatically instead of a person. This eliminates the need for numerous workers and large-scale scaffolding installations.

✓Uniformly and precisely removes material only where needed, drastically reducing dust volume and industrial waste disposal costs!

The shot-blasting machine rotates horizontally around the surface for uniform and efficient application. This reduces dust generation and lowers industrial waste disposal costs.

| In the conventional vertical methods, when performing circular work in the horizontal direction, there is a possibility that the robot may not return to its original starting position if the angle deviates from the horizontal direction set as 0 degrees.

For the horizontal method under patent application, challenges are being solved by developing a horizontal positioning fixture for robots and improving the control system.

As a result, a 64% (106 hours) reduction in man-hours was achieved! By automatically rotating horizontally around the outer circumference, it enables uniform work along the shortest distance with high precision. |

(Source: The company)

3. Fiscal Year Ending January 2026 Earnings Forecasts

Full-year consolidated earnings forecast

| FY 1/25 Act. | Ratio to sales | FY 1/26 Est. | Ratio to sales | YoY | Previous forecast |

Sales | 10,897 | 100.0% | 12,000 | 100.0% | +10.1% | 13,000 |

Operating income | 373 | 3.4% | 700 | 5.8% | +87.3% | 1,200 |

Ordinary income | 592 | 5.4% | 700 | 5.8% | +18.2% | 1,280 |

Net income | 409 | 3.8% | 550 | 4.6% | +34.2% | 950 |

*Unit: million yen

Forecast double-digit growth of sales, and significant growth of profit.

For the fiscal year ending January 2026, sales are expected to grow 10.1% year on year to 12 billion yen and operating income is projected to rise 87.3% year on year to 700 million yen. The initial forecasts of sales and profit have been revised downwardly.

In the fiscal year ending January 2026, they set a goal of achieving a high operating income margin, and have engaged in marketing activities under the policy of choosing and receiving orders for projects whose profit margin is high, so the profit margin of projects they have undertaken is recovering. However, they were not able to receive orders for some large-scale projects whose profit margin is high due to the insufficient development of a selective order system. From the fiscal year ending January 2026, a project was suspended for a reason attributable to the client after the commencement of the project, producing a delay in recording sales due to delays in construction progress. In terms of profits, the profit margin for this project also declined due to waiting losses incurred when the project was suspended and delays in the removal of scrap. In addition, the improvement in profitability was not seen until the end of the interim period for some unprofitable businesses (design, software development and sales, engineer dispatch). As a result, sales and profit forecast have been revised downward.

The year-end dividend has not been revised, so they plan to pay 25.0 yen/share, up 15.0 yen/share from the end of the previous fiscal year, so the annual dividend amount will be 40.0 yen/share, up 20.0 yen/share from the previous fiscal year. The expected dividend payout ratio is 65.5%.

4.Leading the Future-Medium-Term Management Plan 2030

The fiscal year ending January 2026 marked the final year of the medium-term plan “Decarbonization Action Plan 2025.” Initially (at the time of announcement in March 2021), they aimed for sales of 10 billion yen and an operating income of 1 billion yen. However, it achieved the target sales one year ahead of schedule due to a favorable order receipt environment and proactive recruitment efforts to strengthen its organizational structure. The company's current outlook calls for sales of 12 billion yen and an operating income of 700 million yen. However, it is expected to fall short of its target operating income margin of 10%, and improving the earning capacity have become an issue.

4-1 BESTERRA's Goals

BESTERRA's unique position gives it a path to contribute to the global environment, and achieving this requires growth in both quality and quantity.

Purpose: Contributing to the Global Environment

Our corporate value is summed up in one sentence: “Contributing to the global environment through flexible ideas, creativity, and technical prowess,” representing our corporate philosophy.

Long-term Vision: Contributing to a Circular Economy

Dismantling is the entry point to the venous industry and the starting point for recycling. The company will work with companies in the venous industry to contribute to the realization of a circular society by viewing the items recovered through demolition work as resources that create new value.

Medium-term Vision: Leading Company in the Demolition Industry

The company aims to be a guide for the demolition industry, not only in terms of size but also in terms of technical expertise, human resources, and ethical standards. It will lead the demolition industry and improve its status in response to social issues such as “the deterioration of infrastructure,” “carbon neutrality,” and “the decrease of workers in the demolition industry due to the declining population.”

Opportunity: Big Market and Distinctive Advantages

Since there are not any major competitors in the market with a demand of one trillion yen, the company has significant opportunities due to its unrivaled strengths.

Originality: Assets cultivated for 50 years of history

Under the philosophy of “Making Demolition Beautiful,” the company has developed a number of innovative demolition techniques and patented methods. By promoting a management approach focused on not owning assets, the company has established a unique position as a firm that thinks about innovative demolition.

Under the long-term vision, the company aims to contribute to a circular economy by achieving sales of 100 billion yen and an operating income of 10 billion yen as soon as possible.

Under the medium-term vision, the company aims to become a comprehensive leader in the demolition industry, possessing not only a large company size, but also technological capabilities, human resources, and ethical standards that set the benchmark for the demolition industry.

4-2 Market Conditions

Expanding the Demolition Market

○ Over the next 30 years, the ratio of facilities that have been in operation for over 50 years will increase at an accelerating rate.

○ Similarly, plant facilities constructed after the period of rapid economic growth in the 1960s will rapidly deteriorate.

○ Due to the conversion to natural energy, the demand for dismantling and replacement of onshore wind power-generation facilities, etc. will increase.

As a result, it is forecast that the demolition market in Japan will continue to expand at an accelerating pace.

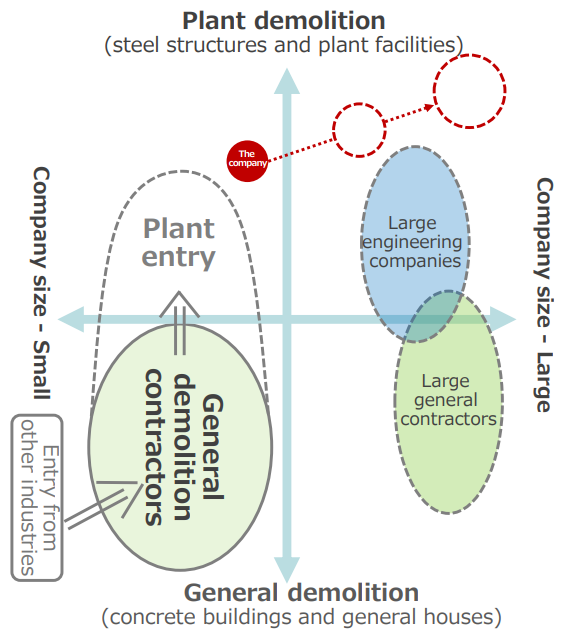

Competitive Landscape in the Plant Demolition Industry

Enhancing specialization in plant demolition leads to a differentiated position.

| Expertise in Plant Demolition ○ Safety standards ○ Understanding the materials used in the structure ○ Understanding the manufacturing process ○ Handling heavy objects ○ Demolition planning ○ Demolition management

The number of licensed contractors has grown significantly since the establishment of the “Demolition Work” licensing category in the construction industry in 2016. Number of licensed contractors in the “Demolition work” category End of March 2016: 29,335 End of March 2017: 43,186 End of March 2021: 60,926 End of March 2023: Approximately 65,800 (up 2,447 year on year) End of March 2024: Approximately 68,200 (up 2,387 year on year) The number continues to increase at a rate of over 2,000 companies per year. The aging of buildings built at a time of rapid economic growth and the advancement of measures to deal with unoccupied properties are the primary drivers for the rising need for demolition work. |

(Source: The company)

Trends in the Plant Dismantling Industry

The scale of the plant dismantling market is estimated to be between 700 billion and 1 trillion yen annually.

Electric Power | The Seventh Strategic Energy Plan announced by the Agency for Natural Resources and Energy is aimed at increasing the proportion of renewable energy to 40-50% and limit the proportion of thermal power to 30-40% by 2040. To strike a balance between decarbonization and a stable energy supply, the agency intends to decrease the amount of thermal power generation, mainly inefficient coal-fired power generation, and maximize the use of renewable energy with high decarbonization effects as the primary power source. |

Iron and Steel Making | Due to shifts in demand and the need for environmental measures in Japan, facilities are being reorganized. The demand for iron and steel in Japan is decreasing due to economic stagnation, population decline, and the development of the steel industry in the Asia region. In addition, the conversion of blast furnaces to electric furnaces and research on hydrogen reduction-based iron and steel production are being promoted for decarbonization, making the restructuring of facilities an urgent priority. |

Petroleum and Petrochemicals | Numerous industrial complexes were constructed during the period of rapid economic growth, and have been in operation for more than 50 years. Ethylene plants, in particular, are facing declining demand and utilization rates, prompting several companies to consider restructuring their facilities. In the Chiba area, Maruzen Petrochemical Co., Ltd. and SUMITOMO CHEMICAL COMPANY, LIMITED along with Idemitsu Kosan Co., Ltd. and Mitsui Chemicals, Inc. have each expressed their intention to consolidate their facilities. In the Mizushima area, Asahi Kasei Corporation and Mitsubishi Chemical Corporation are planning production system optimization. |

Wind Power | As of the end of 2024, there were 2,720 units in Japan, most of which were onshore. It is expected to shift to large-scale offshore wind power in the future. In addition, the service life of onshore wind turbines is about 15-20 years, and the purchase period of the FIT (Feed-in Tariff) is 20 years; hence, a rapid increase in demolition demand is expected. Furthermore, it is assumed that there are a considerable number of turbines that need to be dismantled due to damage or critical failure caused by lightning strikes, typhoons, etc. |

4-3 Numerical Targets and Measures

Basic Policy

To establish a strong foundation for becoming a top demolition company by seeking both qualitative and quantitative growth simultaneously.

Numerical targets for the fiscal year ending January 2031

Net sales: 30 billion yen, Operating income: 3.3 billion yen (operating income margin: 11%), ROE: over 20% or higher

Quantitative Targets of KPIs

(Unit: million yen)

| FY 1/25 Results | FY 1/26 Forecast | FY 1/27 Plan | FY 1/28 Plan | FY 1/29 Plan | FY 1/30 Plan | FY 1/31 Plan |

Sales | 10.897 | 12,000 | 14,000 | 17,000 | 20,000 | 24,500 | 30,000 |

Operating income | 373 | 700 | 1,200 | 1,600 | 2,000 | 2,600 | 3,300 |

Operating income margin | 3.4% | 5.8% | 8.5% | 9.4% | 10.0% | 10.6% | 11.0% |

EPS | 46 yen | 61yen | 86 yen | 114 yen | 144 yen | 187 yen | 238 yen |

ROE | 9.2% | 11.0% | 15.0% | 17.0% | 18.0% | 19.0% | 20.0% |

Number of Dismantling Supervisors | 77 | 92 | 105 | 126 | 145 | 172 | 205 |

Key Initiatives

1.To increase competitiveness by pursuing quality, developing decarbonized demolition methods®, and using artificial intelligence (AI)

To establish a technological brand that leads the industry by developing new demolition methods and applying for patents through the combination of creativity and AI.

◼ Integrating R&D with AI to enhance technical capabilities and competitiveness

・Leverage AI to formalize the knowledge gained by specializing in plant demolition and the expertise acquired in demolition methods.

・Develop a new unique demolition method by combining the explicit know-how, creativity of employees, and AI.

・Improve risk prediction and demolition management and ensure quality control and safety even amid the expansion of the business scale by integrating proprietary safety standards and technology with AI.

・Systematize the achievements as intellectual property, actively promote patent applications, and establish a technology brand that leads the industry.

◼ Visualizing the added value of Decarbonized Demolition® to enhance competitiveness

・Visualize GHG (greenhouse gas) emissions at the demolition site, while comprehensively proposing the company’s “Decarbonized Demolition®” method to provide environmental value to customers.

・Maximize the recycling rate through AI analysis to reduce environmental impact and enhance profitability and competitiveness.

・Explore new business opportunities in cooperation with the venous industry, based on Decarbonization Demolition®, to realize a circular economy.

2.Accelerating growth by pursuing quantity, expanding bases to areas with many plants

Establish a foundation for sustainable growth by maximizing the ability to receive orders and recurring revenue through the expansion of bases into regions with many plants.

◼ Sales strategy and business base expansion for maximizing the number of orders received

・Develop sales strategies and systems based on market analysis that takes into account industry trends, regional characteristics, and facility conditions.

・Maximize sales by opening new sales bases mainly in areas with many plants, such as Osaka and Yokkaichi, to accelerate nationwide development.

・Acquire projects and expand recurring revenue by expanding demolition bases.

◼ Establishing a base structure, strengthening management, and diffusing their corporate culture

・Optimize the head office support and regional bases’ organizational functions, enhancing the organization's capacity to adapt to scale expansion through the proper delegation of authority.

・Strengthen base management and promote culture-diffusing initiatives to maintain and evolve the company's cultural strengths as employees increase.

◼ Strengthening the network of partner companies and procurement functions

・Expand and strengthen our nationwide network of partner companies to match sales growth.

・Evolve our outsourcing strategies and purchase functions to enhance competitiveness and profitability.

3.Setting the groundwork for the future: exploring overseas markets and establishing foundations for future expansion

Conduct research and explore collaboration in promising markets to establish a foundation for overseas expansion, which will be a future growth driver.

◼ Identifying target countries and conducting feasibility studies

・Conduct market research targeting promising markets such as Singapore and South Korea to lay the groundwork for future expansion.

・Investigate and analyze plant demolition requirements, methodologies, project timelines, costs, and scrap distribution channels to accumulate insights directly applicable to overseas business development.

・Establish relationships with potential local partners and explore opportunities for collaboration.

・Organize the legal framework and a regulatory environment, and advance preparations for market entry, including the establishment of a local subsidiary.

◼ Approaching overseas plants with a focus on Japanese companies

・Conduct surveys on Japanese companies with overseas plants to identify their needs and opportunities to receive orders.

・Explore potential collaboration with engineering companies undertaking demolition work at overseas plants to develop new routes for receiving orders.

・Leverage existing customer relationships to establish a foundation for future overseas expansion.

4-4 Trend in each field

4-4-1 Electric power field

In the 7th basic energy plan announced by the Agency for Natural Resources and Energy, the company aims to increase the ratio of renewable energy to 40-50% by 2040 and keep the ratio of thermal power generation 30-40%.

From the viewpoints of stable supply of energy and decarbonization, the company will adopt renewable energy, which has a significant decarbonization effect as a core power source, as much as possible, and reduce the output of thermal power generation, mainly inefficient coal-fired one.

Major plans to dismantle thermal power plants

J-POWER | Matsushima Thermal Power Plant was dismantled at the end of FY 2024. Takasago Thermal Power Plant is to be dismantled in FY 2028. Takehara and Matsuura Thermal Power Plants are to be temporarily stopped or dismantled or used as a standby power system. |

JERA | Kashima Thermal Power Plant No. 1-6 were dismantled in March 2023. All of coal-based thermal power plants, which are inefficient, are scheduled to be stopped or dismantled by 2030. |

Chugoku Electric Power | Kudamatsu Power Plant No. 2 was dismantled in January 2023. Mizushima Power Plant was dismantled in April 2023. Shimonoseki Power Plant No. 1-2 were dismantled in January 2024. |

In addition, several companies, including Tohoku Electric Power, Kyushu Electric Power, and Shikoku Electric Power, plan to dismantle their thermal power plants.

4-4-2 Ironmaking field

Equipment is being upgraded to cope with the changes in domestic demand and take environmental measures.

The demand for iron and steel in Japan is declining, due to the economic downturn, the shrinkage of the population, the growth of overseas ironmaking industries, etc. In addition, it is imperative to upgrade equipment, as the shift from blast furnaces to electric furnaces and research into hydrogen-reduction ironmaking are progressing for decarbonization.

Decarbonization in production of iron and steel

Shift to electric furnaces | Nippon Steel: Switch from blast furnaces to electric furnaces in the Yahata District; construction of new electric furnaces in the Hirohata District JFE Steel: Replaced a blast furnace with a large-sized electric furnace in the Kurashiki District |

Hydrogen-reduction ironmaking | Nippon Steel: A 43% reduction in CO2 emissions was observed in a test conducted from November to December 2024 |

Growth of demand for highly functional steel materials

The demand for fuel-efficient automobiles and highly efficient power generation equipment for achieving carbon neutrality is growing, so each company puts energy into the production of highly functional steel materials. Accordingly, the replacement and upgrade of production equipment can be expected.

4-4-3 Fields of petroleum and petrochemical

As petrochemical complexes have deteriorated and ethylene equipment decreased due to the change in domestic demand, the integration and disposal of equipment have been progressing.

Most complexes were constructed in the high economic growth period, so the company has been operated for over 50 years. For the replacement, integration, and dismantlement of equipment, the demand for plant demolition is growing.

(Taken from the reference material of the company)

Integration and dismantlement of ethylene plants

Several companies are discussing the replacement of ethylene plants in complexes, as demand and utilization rate have declined. In Chiba, Maruzen Petrochemical, Sumitomo Chemical, Idemitsu Kosan, and Mitsui Chemicals expressed their intention to integrate equipment. In the Mizushima area, Asahi Kasei and Mitsubishi Chemical plan to optimize the production structure.

Decline in demand for plastics and decrease of production equipment

Plastics account for 60% of petrochemical products. Recently, the demand for plastics has shrunk and production amount has been decreasing, as companies have taken environment-conscious measures. Accordingly, plant equipment is projected to decrease.

4-4-4 Other manufacturing fields

Due to digitalization and growth of demand related to electric vehicles, capital investment has increased and restructuring has become active.

While the rise in interest in utilization of AI and digitalization is increasing demand, the demand in the papermaking and other manufacturing fields is shrinking.

Automobile industry

The Ministry of Economy, Trade and Industry upholds the goal of increasing the ratio of electric vehicles to new cars sold to 100% by 2035, so an increasing number of hybrid cars and EVs are distributed. On the other hand, the production number of automobiles is declining.

Papermaking industry

As the domestic demand for paper and paperboard is shrinking, several companies are replacing or dismantling production equipment. Nippon Paper Industries will stop some production equipment by the end of 2025. Oji Holdings plans to close Fujinomiya Factory in January 2026.

Semiconductors

As enterprises put energy into the utilization of AI and digitalization, the investments in the upgrade and enhancement of capacity of semiconductor manufacturing equipment are increasing, and the production output of semiconductor manufacturing equipment is growing.

5. Interview with President Honda

We interviewed President Yutaka Honda, asking him to tell us about the progress in the interim financial results, the outlook for the fiscal year ending January 2026, the future growth strategies and business development, and the competitive edge of BESTERRA, and give a message to shareholders and investors.

President Honda was born in 1972 and is 53 years old. After working for TOKYU CORPORATION and en Japan Inc., he entered BESTERRA CO., LTD. in 2009. He assumed the position as a director in 2014 and then the post of president in February of 2023.

Q: Could you summarize BESTERRA’s business performance for the interim period of the fiscal year ending January 2026?

While operating income in the interim period went up from the same period of the previous year, it significantly fell below the forecast. One of the biggest factors behind it is the machinery depreciation and maintenance fees arising from the temporary suspension of a project that put some of our machinery on hold. This caused operating income to go below the forecast by about 100 million yen. In addition, a delay in streamlining 3D Visual KK, a subsidiary engaging in software development, pushed down operating income by approximately 30 million yen.

Q: BESTERRA downwardly revised the forecast for the fiscal year ending January 2026. Could you give us the details of the downward revision?

We downwardly revised the full-year sales forecast by 1 billion yen principally because we did not win orders. Although we expected that we would convert at least two of the seven inquiries that we got for large-scale projects into orders, we did not achieve success. It is highly regrettable that we almost succeeded in converting some of the inquiries into firm orders, but let the opportunities slip away, and our defeat in the price competition is the major reason for our failure in the inquiry-to-order process. This resulted directly in the downward revision to the profit forecast. It led to a decline in operating income by about 300 million yen. Of the remaining 200 million yen, about 80 million yen was recorded as machinery depreciation and maintenance fees arising from the temporary suspension of a project that put some of our machinery on hold, and the financial impacts of the unprofitable subsidiaries including 3D Visual KK, which will continue in the interim period, stood at approximately 70 million yen.

Q: BESTERRA has set quantitative targets for the period up until the fiscal year ending January 2031. How much confident are you in the progress with the targets at the moment? We also would like you to go into detail about your company’s forecast of a significant increase in operating income margin.

We have set relatively ambitious quantitative targets; however, I believe that it is by no means impossible to attain them. The aim of setting the high targets is to encourage our employees to have a deeper awareness of numerical targets. The risk factors that could affect our company include suspension of projects and posting of sales or expenses in a wrong fiscal year.

Q: What about the competitive environment and the business expansion in overseas markets?

The plant demolition market is expected to grow gradually on the scale ranging from 700 billion yen to 1 trillion yen per year. I think that our competitor is ibokin Co., LTD. (securities code: 5699), not companies that have greater market share. As a side note, TANAKEN Inc. (securities code: 1450), which engages exclusively in demolition, does not undertake demolition of plants and therefore is not our competitor. In reality, our competitors vary from project to project because there are no companies that has a large market share. In the demolition industry, it is common that companies establish spin-out businesses, which means that TANAKEN and our company are assumingly the only companies that strive to grow in the industry.

While operating the overseas business mainly in South Korea and Singapore at the moment, we consider breaking into the markets in Malaysia and Indonesia because many plants have been built there. No demolition companies take large market share overseas as in Japan.

Regarding merger and acquisition (M&A), our attitude about them was positive in the past, but we are less active in conducting M&A now.

Q: Could you tell us about your company’s strengths and challenges?

The technical capability is one of our strengths. Our apple peeling demolition method can be used throughout the world. We, however, was not successful in the licensing business. I think that our recruitment capability is another strong point. Our company possesses an overwhelmingly great strength in recruitment of personnel compared to other demolition companies or companies in the entire construction industry. I believe that this is because we are highly regarded for our efforts to solve social issues. Furthermore, we have employed a number of women, raising the ratio of female employees at our company.

The challenge that faced us previously was personnel recruitment, which has been resolved by now. Our current challenge is to develop a sales structure and a cost estimation system.

Q: Your company’s financial condition has improved considerably during this interim period. Could you tell us about your thoughts on shareholder returns? What is your rough estimation of equity ratio?

We roughly estimate equity ratio at around 50%. It reached 62.1% at the end of this interim period owing to the gain on sales of securities. While increasing dividends and giving shareholder benefits are some of our options, I cannot make any decision at my own discretion. We will discuss this matter at meetings of our board of directors. We have adopted a progressive dividend system with the rough estimation of payout ratio being 40%. We made a downward revision to the business performance for this period, but did not revise dividends. This has resulted in a high estimated payout ratio.

Q: What do you think about the current price level of the shares in your company?

I understand that the shares in our company are not left unfairly low at present. While it is true that our price earnings ratio (PER) and price book-value ratio (PBR) were higher at some point in time, I believe that it was because the market expected our company to grow. We have no choice but to accept the share price level considering our company’s current business performance; however, the price of the shares in our company will increase if the market becomes aware of our company’s potential to grow more.

Q: Finally, could you send a message to shareholders and investors?

It is certain that the plant demolition market will grow. While there is competition, I believe that our company has the technical and recruitment capabilities that allow us to win them without fail. We could not live up to your expectations in this interim period, but we will endeavor to satisfy what you are expecting of us.

6. Conclusions

The performance in the interim period fell below the company’s forecast, due to the suspension of a project and the upfront posting of costs for additional projects, so the forecast for fiscal year ending January 2026 has been revised downwardly. After bottoming out in fiscal year ended January 2023, sales growth and profit have been improving. It seems that the strengthening of their marketing and cost estimation systems, which is a challenge for improving profit margin, has been progressing steadily, although it is delayed. In fiscal year ended January 2025, group companies struggled, but they transferred two subsidiaries to concentrate on their core business, so their approach of putting importance on profit has been enhanced further. Through the interview with President Honda, we felt that he has confidence about the results. In fiscal year ending January 2027, there will be no longer less profitable projects that have been continued since last year. Accordingly, operating income margin is expected to is expected to considerably improve to 8.5%, while the forecast for fiscal year ending January 2026 is 5.8%. A road map toward completing the plan for fiscal year ending January 2031 is likely to become feasible. President Honda, who took up the post in 2023, sowed various seeds, and they are about to bear fruit.

The recent problem about human resources is being overcome through the enhancement of their recruitment capacity. If they proceed with the strengthening of systems for marketing and estimating total costs, we can expect a lot, as the plant demolition market will certainly grow.

In the interim period, the forecast was revised downwardly, but sales growth and profit margin are improving. If this upward trend continues, share price will probably improve.

Shareholder Returns

The company will pay stable dividends with a target payout ratio of 40% and a DOE of 3.5% or higher.

In the fiscal year ended January 2023, the company changed (expanded) its shareholder benefits and established the "Besterra Premium Benefits Club."

For details of the "Besterra Premium Benefits Club," please refer to the following URL:

https://besterra.premium-yutaiclub.jp/

<Reference: Regarding Corporate Governance>

◎ Organization type and the composition of directors and auditors

Organization type | Company with an audit and supervisory committee |

Directors | 7 directors, including 4 outside ones |

Auditors | 3 auditors, including 3 outside ones |

◎ Corporate Governance Report Update date: April 25, 2025

Basic policy In order to promote sound business administration and win social trust sufficiently, our company recognizes corporate governance as the most important issue, puts importance on the improvement of the soundness, transparency, and fairness of business administration, and complies with laws and regulations thoroughly, and all executives operate business while keeping in mind that “the violation of laws or regulations would lead to management responsibility.” In detail, our company disseminates and executes business pursuant to laws, regulations, and in-company rules thoroughly, by developing appropriate systems for making decisions about business administration, fulfilling duties, supervising work, conducting internal control, etc. It is also important to reform management systems for “achieving appropriate share price” and “increasing share price sustainably” to emphasize shareholders and strengthen the function to check business administration, to establish global-level corporate governance. The results of such efforts would win the trust of society, increase corporate value, and satisfy shareholders.

<Reasons for Non-compliance with the Principles of the Corporate Governance Code (Excerpts)>

[Supplementary Principle 4-1-3]

We do not have a concrete plan regarding the successor of the CEO. As for the Board of Directors, the policy regarding the selection of successors is to take into consideration the personality, insight and accomplishments of each candidate and select a suitable person. In case of formulating and conducting a plan regarding the successor, we shall ensure the fairness, transparency and objectivity of the decision process and appropriately proceed with the selection by involving the Nomination and Compensation Committee, an advisory institution to the Board of Directors where outside directors account for the majority, alongside proactive involvement of the Board of Directors.

[Supplementary Principle 4-3-3]

While we have not clearly established objective, timely and transparent proceedings for the dismissal of the President or CEO, we assess the effectiveness of the Board of Directors every year and shall progress with objective, timely and transparent proceedings through the involvement of the Nomination and Compensation Committee, where outside directors account for the majority, in regard to the nomination and compensation of directors.

<Disclosure Based on the Principles of the Corporate Governance Code (Excerpts)>

[Principle 1-4 Strategically held shares]From the viewpoint of business expansion based on maintaining and strengthening long-term, stable partnerships with business partners, etc., we will acquire and hold the shares of business partners, etc., if we judge that this will contribute to the improvement of our mid/long-term corporate value. For equity investments premised on forming business alliances, the management meets with and receives explanations of the operating environment, business strategy, and purposes of the capital alliance from representatives of the other party. Based on this, the Board of Directors comprehensively evaluates the appropriateness of the stock valuation report and judges whether the deal should take place. For strategically held shares, the Board of Directors constantly checks whether the holding of such shares will contribute to the improvement of our corporate value and confirms the purpose and rationality of said holding based on that check. Our company will appropriately buy/sell shares and exercise voting rights in accordance with relevant regulations, based on a comprehensive evaluation from the viewpoint of improving our corporate value.

[Supplementary Principle 3-1-3 Measures for sustainability]

Our company discloses initiatives concerning sustainability in the mid-term management plan and on our website. Moreover, in order to clarify initiatives for sustainability, we set up a Sustainability Committee as an advisory institution of the Board of Directors to control and manage the initiatives in addition to establishing the basic sustainability policy. Furthermore, we view the recruitment and education of human resources as an important challenge for improving our corporate value in the mid- to long-term and we shall create a system which will allow for independent building of career and build a free and lively corporate culture based on diversity to seek the reinforcement of human capital. As for risks and opportunities for gaining income related to climate changes, we have responded to the proposal by TCFD in expressing the endorsement of TCFD and participating in TCFD Consortium, and we are proactively working to enrich the quality and quantity of disclosures based on TCFD and equivalent frameworks and forge ahead with the enrichment of disclosure on our company website, etc.

[Principle 5-1 Policy on constructive dialogue with shareholders]Regarding requests from shareholders for dialogue (interviews), our company believes that we should express a positive attitude within a reasonable scope in order to contribute to sustainable growth and medium- and long-term improvement of the corporate value of our company. Aiming to promote constructive dialogue with shareholders, with the management department designated as a department in charge of IR activities, our company holds financial results briefings targeted at financial institutions and investors semiannually and discloses corporate information as needed on our website and through the system of optional disclosure offered by Tokyo Stock Exchange.

[Actions to Achieve Management Conscious of Cost of Capital and Stock Price]

Our company has formulated the "Decarbonization Action Plan 2025," which clearly defines its contribution to a more decarbonized society and defined key strategies and implemented various measures to improve its corporate value over the medium/long term. Our company estimates that the current cost of shareholders’ equity is 6.6%, so regarding the balance between capital cost and return on capital, the ROE in fiscal year ended January 2025 was 9.2% (equity spread: 2.6%) exceeded the cost of shareholders’ equity. Based on the evaluation of the current situation, our company aims to achieve an ROE of 13% or higher and improve PBR further by operating business steadily for achieving sales of 13,000 million yen and an operating income of 1,200 million yen in accordance with the new medium-term management plan “Decarbonization Action Plan 2025,” which will end in fiscal year ending January 2026, and improving our earning capacity through the expansion of business scale, and will enhance our initiatives, including optimal growth strategies and financial strategies.

[Status of holding of dialogue with shareholders and so on]

In FY 2024, we held a financial results briefing session for institutional investors and analysts twice a year and an individual meeting 30 times a year, explaining the outline of financial results, our earnings forecast, and the progress of the medium-term plan. As IR activities for individual investors, we held a company briefing session, participated in an exhibition, or the like three times a year.

This report is not intended for soliciting or promoting investment activities or offering any advice on investment or the like, but for providing information only. The information included in this report was taken from sources considered reliable by our company. Our company will not guarantee the accuracy, integrity, or appropriateness of information or opinions in this report. Our company will not assume any responsibility for expenses, damages or the like arising out of the use of this report or information obtained from this report. All kinds of rights related to this report belong to Investment Bridge Co., Ltd. The contents, etc. of this report may be revised without notice. Please make an investment decision on your own judgment. Copyright(C) Investment Bridge Co., Ltd. All Rights Reserved. |