| Ferrotec Corporation (6890) |

|

||||||||

Company |

Ferrotec Corporation |

||

Code No. |

6890 |

||

Exchange |

JASDAQ |

||

Industry |

Electric Equipment (Manufacturing) |

||

President |

Akira Yamamura |

||

HQ Address |

Nihonbashi Plaza Building, Nihonbashi 2-3-4, Chuo-ku, Tokyo |

||

Year-end |

March |

||

URL |

|||

* Stock price as of closing on June 10, 2013. Number of shares issued at the end of the most recent quarter excluding treasury shares.

|

||||||||||||||||||||||||

|

|

* Estimates are those of the Company.

|

|

| Key Points |

|

| Company Overview |

|

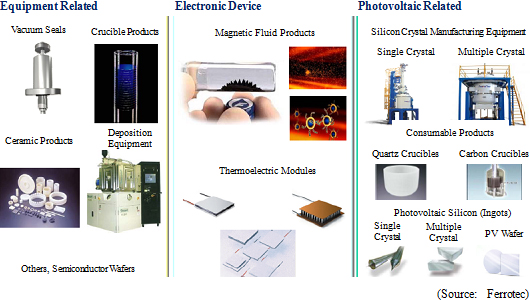

<Business Segments>

Ferrotec's operations can be divided into the equipment related business segment where vacuum seals, crucibles, and other ceramics products used in semiconductor, FPD, and LED related manufacturing equipment are manufactured, electronic device business segment where thermoelectric module application products are made, and photovoltaic business segment where silicon single crystal manufacturing equipment and crucibles used in devices are produced. In fiscal year March 2013, sales of the equipment related business, electronic device business, and photovoltaic related business segments accounted for 49.1%, 11.9% and 32.1% of total sales respectively, while saw blades, equipment part cleansing, machine tool, and other products not included in reported segments accounted for 6.9%. Ferrotec leverages its knowhow and technologies for vacuum seals, which are the main product of the equipment related business segment, in its silicon crystal manufacturing equipment.

|

| Management Strategy |

(1) Equipment Related Business Segment

With regards to vacuum seals, Ferrotec is expected to make a transition from the simple parts business model to a higher value added business model that provides modules, subassemblies, and engineering after services, in addition to pursuing synergies with its surface processing and cleansing operations. Furthermore, the Company will endeavor to develop applications in foods, pharmaceuticals, and medical equipment areas, while at the same time fortifying applications other than semiconductors and FPD. In the area of quartz products, Ferrotec will fortify its marketing operations to pursue synergies and sell its cleansing services to the Chinese factories of high profile customers from the United States and Taiwan.

(2) Electronic Device Business Segment

Ferrotec is implementing measures to fortify development of thermoelectric module products to meet customers' needs for diversified applications. At the same time in overseas markets, efforts to develop optical communications related field in China and Korea, and the cleansing equipment field in Korea are being implemented. Furthermore, Ferrotec's marketing function will also be fortified to cultivate the high functionality market in the United States. Efforts to automate production lines and reduce fixed costs are also being implemented.

(3) Photovoltaic Related Business Segment

Ferrotec will create a structure that can produce stable profits based on consumable products including quartz crucibles and multiple crystal square tanks, and photovoltaic cell silicon.

Quartz Crucibles, Multiple Crystal Square Tanks

In the photovoltaic cell related market in China, the new leadership has taken steps to restrict supplies. Therefore, stagnant capital investments and curtailed production have contributed to bankruptcies of some of the large panel makers. Consequently, quartz crucible manufacturers and multiple crystal square tank manufacturers have also been impacted, and there are currently only five crucible manufacturers and three multiple crystal square tank manufacturers operating in China. The photovoltaic cell market is expected to grow by 10% to 15% per annum and therefore supply shortages of quartz crucibles and multiple crystal square tanks are expected. In addition, Ferrotec is expected to cultivate demand from quartz crucibles for semiconductor circuits (future target is to achieve two thirds of sales from photovoltaic cells and one third from semiconductor applications), and to strengthen its position in Taiwan where it has 60% share in the multiple crystal square tank market with a high conversion rate and low pricing.

Photovoltaic Cell Use Silicon

Ferrotec will endeavor to expand its OEM supply of its P type wafers, which have attained a high conversion rate of over 19% using its unique technologies, and advanced N type wafers. Compared with loose abrasive grain (grinding and polishing abrasive grains used by mixing with water), Ferrotec's wafers sliced by using fixed abrasive grain diamond wire (core piano wire coated with diamond gains) are highly regarded by Japanese photovoltaic cell makers.

Production Devices

With regards to the photovoltaic cell related realm, Ferrotec will adopt a selective strategy for taking orders in view of profitability, and leverage its advanced technologies in glass processing, general use polishing, core drill, NC lathe and other equipment, and develop applications for its general use equipment in general industries other than photovoltaic cells.

|

| Fiscal Year March 2013 Earnings Results |

Sales Fall 36.1%, Ordinary Loss of ¥3.465 Billion (¥3.287 Billion Ordinary Income in Previous Term)

Sales fell by 36.1% year-over-year to ¥38.424 billion during fiscal year March 2013. Difficult operating conditions of the photovoltaic cell panel makers contributed to a 54.9% year-over-year decline in sales of the photovoltaic related business segment. Declines in capital investments and production of the semiconductor and FPD industries contributed to a 24.2% fall in sales of the equipment related business segment, and weak demand for thermo modules led to a 14.5% year-over-year decline in electronic device business segment.

Equipment Related Business

Sales and operating income declined by 24.2% and 94.5% year-over-year to ¥18.867 and ¥0.137 billion respectively. Overall demand stagnated despite favorable trends for quartz and ceramics products used in semiconductor and FPD manufacturing processes and in applications for smartphone semiconductors. The growing request for price reduction since the mid-year also contributed to the fall in sales. Furthermore, sales of vacuum seals used as semiconductors and FPD manufacturing equipment parts also fell due to weak capital investments. However, silicon wafer processing for small diameter wafers maintained robust sales.

Electronic Device Business

Sales and operating income declined by 14.5% and 53.7% year-over-year to ¥4.563 and ¥0.257 billion respectively. Demand for thermoelectric modules from testing devices and biotechnology related equipment applications proved resilient. However, a difficult operating environment continued until the mid-year, which led to a decline in sales of temperature controller for automobile seats. Weak consumer spending also contributed to declines in shipments to consumer equipment applications. At the same time, strong automobile sales in developing countries contributed to an increase in sales of magnetic fluid used in automobile speakers.

Photovoltaic Related Business

Sales declined by 54.9% year-over-year to ¥12.345 billion and an operating loss of ¥3.934 billion was incurred (compared with an operating income of ¥775 million in the previous term). Increases in the use of photovoltaic cells in Japan, China and the United States were offset by declines in Europe and worldwide demand remained flat with the previous term. At the same time, the price of photovoltaic panel declined due to an oversupply primarily by Chinese manufacturers. Subsequently, these conditions led to deterioration in profits of the panel makers and caused their capital investments to freeze. Against this backdrop, demand for silicon ingots and wafers, and silicon crystal manufacturing equipment declined, causing sales of crucibles, square tanks and other consumable goods to decline as customers adjusted their production schedules.

|

| Fiscal Year March 2014 Earnings Estimates |

Sales to Rise 9.3%, Ordinary Income of ¥700 Million

While difficulties in the silicon crystal manufacturing equipment are expected to contribute to a 9.5% year-over-year decline in sales of the photovoltaic related business, investments for miniaturization of semiconductors and for mobile applications of FPDs should boost sales of the equipment related business by 18.2% year-over-year. At the same time, an increase in the sales of thermoelectric modules on the back of recoveries in consumer products and temperature controllers for automobile seats is expected to allow sales of electronic devices to rise by 15.8% year-over-year.

Equipment Related Business: Sales Rise 18.2% to ¥22.305 Billion

Vacuum seals sales are expected to rise by 14.0% year-over-year to ¥5.340 billion. At the moment, in addition to the restart of investments primarily by large semiconductor companies, investments on FPD for large LCD television, small and medium sized high resolution LCDs for mobile handsets, and organic EL manufacturing equipments in China are expected to recover as well. Furthermore, signs of a recovery in robot manufacturers have also been observed. In addition, Ferrotec is implementing efforts to expand its customer base by providing engineering after services, and cultivating demand for equipment sub-assemblies and chambers from general industries.

Electronic Device Business: Sales Rise 15.8% to ¥5.282 Billion

Sales of the core product of thermoelectric modules are expected to rise by 15.5% year-over-year to ¥4.764 billion. Sales to automobile heated seat applications are expected to grow on the back of the adoption of new product models. In addition, consumer products, biotechnology equipment, semiconductor, and optical applications are expected to keep strong trend. Also, new product applications for electric shavers and water purifying equipment are being developed. Ferrotec is implementing measures to expand its share of the United States and China optical communications markets, and to increase profitability through the sale and certification of power device boards. In particular, the Company is fortifying it marketing capabilities in the high functionality market in the United States. In addition to these moves, automation of production lines is being promoted as a means of reducing fixed costs.

Photovoltaic Related Business: Sales Fall 9.5% to ¥11.173 Billion

Sales of quartz crucibles, including multiple crystal and square tank products, are expected to rise by 13.8% year-over-year to ¥6.268 billion. Volumes are expected to increase on a bottoming in photovoltaic cell demand. Efforts to raise the share of semiconductor applications to overall sales are also being considered. At the same time, Ferrotec is now enjoying the benefit from competitors' withdrawal from the multiple crystal square tanks and its capacity utilization rate is currently trending around 90%. In addition to differentiation by getting certified as heat resistant products for a long period of time, efforts to recycle materials and extract cost reductions in the refining process are being implemented at the Yinchuan Plant. Moreover, Ferrotec seeks to expand its share by quickly acquiring certification for eight inch applications for semiconductor use.

|

| Conclusions |

|

Disclaimer

This report is intended solely for information purposes, and is not intended as a solicitation to invest in the shares of this company. The information and opinions contained within this report are based on data made publicly available by the Company, and comes from sources that we judge to be reliable. However we cannot guarantee the accuracy or completeness of the data. This report is not a guarantee of the accuracy, completeness or validity of said information and or opinions, nor do we bear any responsibility for the same. All rights pertaining to this report belong to Investment Bridge Co., Ltd., which may change the contents thereof at any time without prior notice. All investment decisions are the responsibility of the individual and should be made only after proper consideration.

|